Sign up here to receive the Market Ethos by email.

Ok, we are going to keep this Ethos a bit shorter, simply because the rise in market volatility had us writing lots of content outside our regular weekly instalment. Some good feedback from our Investor Strategy which had a special edition on the carry trade. If you missed it, click HERE, as we did our best to explain the mechanical unwinding of the yen carry trade and how it was reverberating differently across parts of the market. Beneath the ‘carry trade’ talk, there has been an uptick in folks talking about recession once again. That will be our brief topic this week.

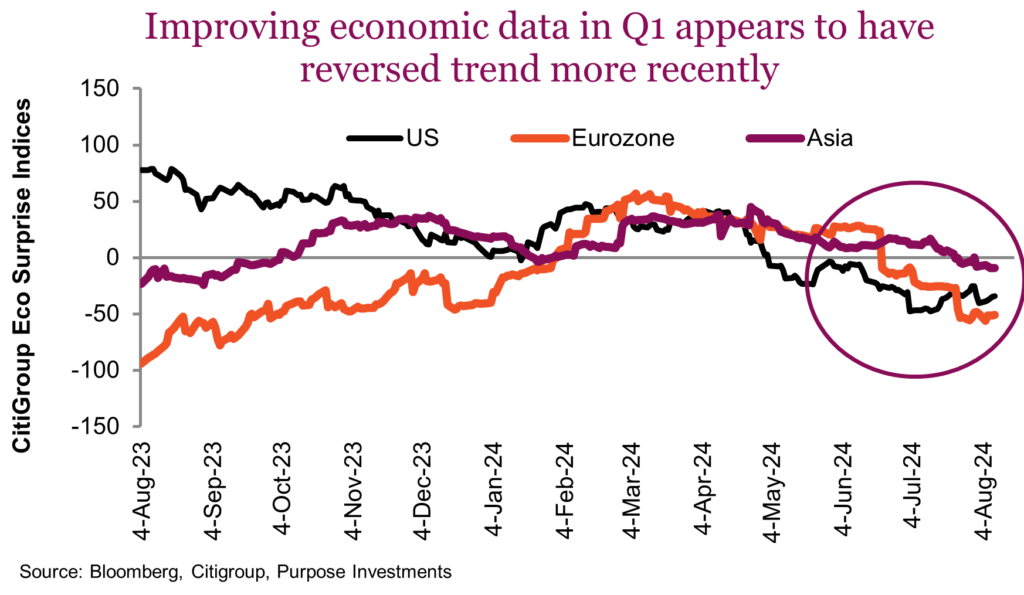

There is no denying the economic data has turned a bit softer. This isn’t new news either; in fact after a really strong Q1 and part of Q2, the data began rolling over. First in the U.S. and now more recently globally. The chart below is the Citigroup Economic Surprise index, measuring the data compared to consensus, adjusted for the importance of the data release. Sorry, Canada is not on here, but the chart is similar, strong for much of 2024 and then turning negative, fueled by our weak labour report on August 9.

The economic data has a lot of noise and since there are so many data releases, you can always find something good and something bad, if you look hard enough. The key is what is more important for the market today. And that answer is simple: US consumer or labour (labor as they say).

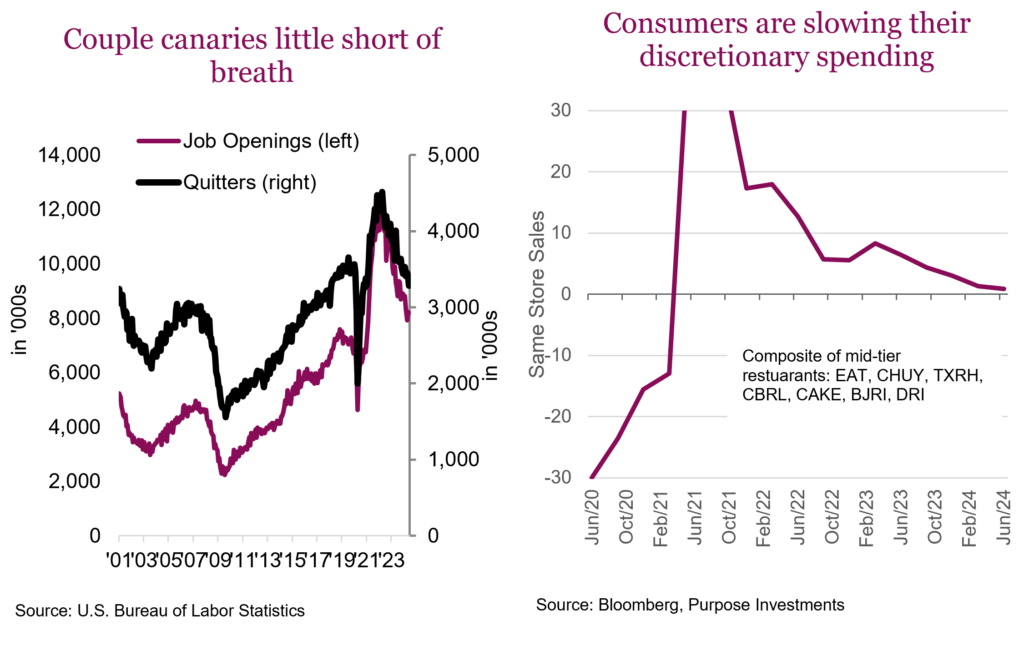

The U.S. consumer has been downshifting their spending patterns, which is often a sign of stress or retrenchment. We started highlighting rising credit card late payments and sit down restaurant same-store-sales many months ago (chart below on left). And the anecdotal pieces kept coming. This was supposed to be a record travel summer for airlines as capacity remains constrained (seems a major plane maker is running behind) and prices are high. Well, the seats were not selling and many guided lower and started discounting. Walmart highlighted increased spending among wealthier patrons. When the wealthy are back at Walmart, that is not a good sign. The list goes on.

Softening consumers are not a huge deal, they have been very resilient for many quarters while inflation has been eroding wealth. One positive of the more fragile U.S. consumer, has been their job market. When jobs are plentiful and easy to find, people are more confident and spend more freely. But that appears to be starting to change. Lots of people still finding jobs but it is not as easy as it was a few months or quarters ago. Job openings are dropping, and people are quitting as well. If you are worried about finding a new job, it tends to result in people quitting less often.

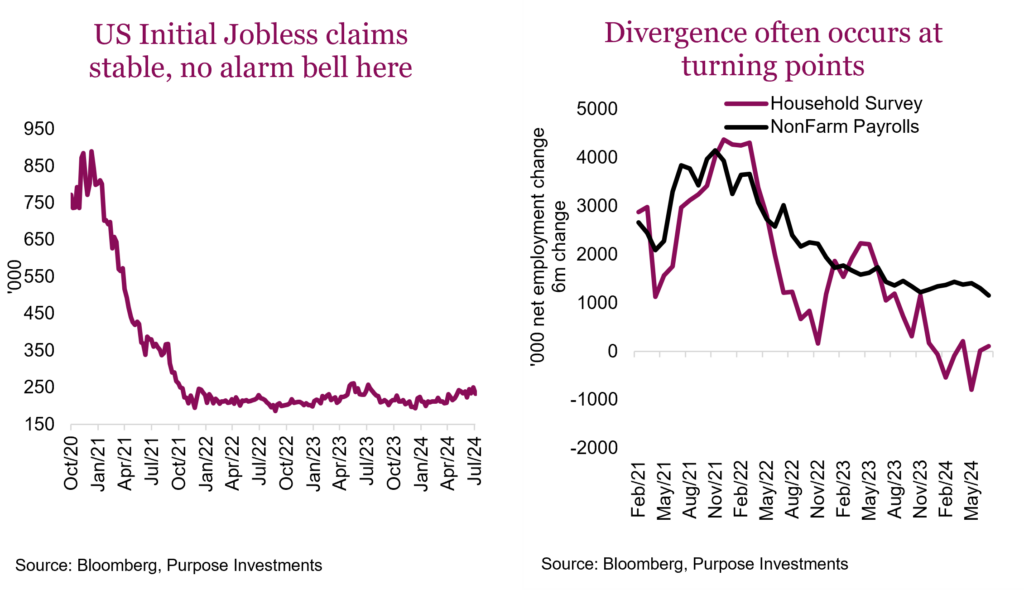

As a result, hard labour reports are now much more important than a few months ago. The official nonfarm payrolls will be more closely scrutinized; the only risk here is if the jobs have started to disappear, we may already be in a recession. Labour is a lagged indicator usually. The downtick in jobs in July was concerning, as is the divergence between the household and nonfarm surveys. There is often divergence at a turning point. But for something a bit timelier, people are starting to focus on initial jobless claims. So in the last couple weeks, the nonfarm report was weak, but the initial jobless claims were stable. See, it is easy to find data that can support or refute any view.

Final thoughts

The economy is slowing. But it is probably way too early to talk recession or even get too excited. Financial conditions have actually been easing for the past number of quarters, deficit spending still really strong, and parts of the economy are doing well. Probably a few oscillations, some better, some worse, for the economic data before recession risk become material. The only real certainty: economic talk will be on the rise.

Source: Charts are sourced to Bloomberg L.P., Purpose Investments Inc., and Richardson Wealth unless otherwise noted.

The contents of this publication were researched, written and produced by Purpose Investments Inc. and are used by Richardson Wealth Limited for information purposes only.

*This report is authored by Craig Basinger, Chief Market Strategist at Purpose Investments Inc. Effective September 1, 2021, Craig Basinger has transitioned to Purpose Investments Inc.

Disclaimers

Richardson Wealth Limited

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson Wealth Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.

Purpose Investments Inc.

Purpose Investments Inc. is a registered securities entity. Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Neither Purpose Investments nor Richardson Wealth warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise.

Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice.

The particulars contained herein were obtained from sources which we believe are reliable but are not guaranteed by us and may be incomplete. This is not an official publication or research report of either Richardson Wealth or Purpose Investments, and this is not to be used as a solicitation in any jurisdiction.

This document is not for public distribution, is for informational purposes only, and is not being delivered to you in the context of an offering of any securities, nor is it a recommendation or solicitation to buy, hold or sell any security.

Richardson Wealth Limited, Member Canadian Investor Protection Fund.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.

Related articles

Investor Strategy

No summer doldrums

August 7, 2024. Investor Strategy. EXTRA! EXTRA! Special edition on the carry trade. Sometimes, you are driving along nicely, and suddenly, your car is jolted…