Market Ethos

August 19, 2024

Bond buyers can be so sensitive

Sign up here to receive the Market Ethos by email.

Summary: There are many buyers of government bonds ranging from those big central banks, pensions, insurance companies, regular banks and investors (like you and me). The proportions of these cohorts change over time for many reasons. Today, we believe the groups whose demand is more sensitive to different yields have a larger representation. This could limit how far yields may come down, even in a recession, as lower yields may see many buyers stop or slow buying. We believe the overall elasticity of yield demand has risen.

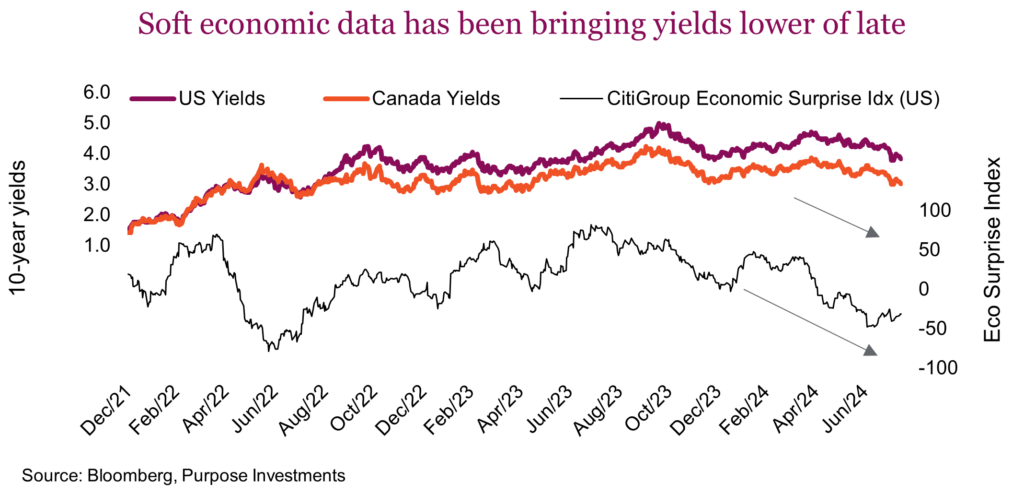

Bond yields have certainly moved lower during the past month or two. Early May had the 10-year U.S. Treasury yield around 4.75%, down to 3.9% as of mid-August. The drop in yields can be attributed to a couple key factors, softening of economic growth and calming of inflation. The same trajectory has been evident with Canadian bond yields. Nothing like a little more recession talk to get yields to fall.

The big question is how low will yields go? Naturally a lot depends on the data: from no landing, soft landing or hard landing. While we all have our views, the economy’s path is uncertain. But there is something we do know that may limit how far yields fall, even if the data gets a lot worse: who the buyers of bonds are today and their motivation.

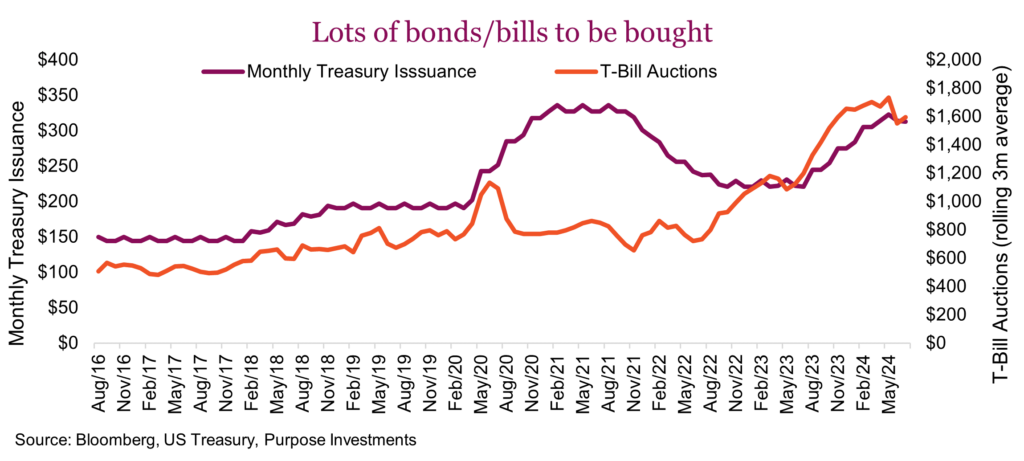

First, let’s talk supply. There is LOTS!!! U.S. Treasury bonds issuance runs about $300 billion per month and T-bills at about $1.5 trillion. Of course a lot of this issuance is simply previous notes maturing, and in most cases investors rolling the proceeds into the next issue. But you have to acknowledge the issuance of Treasuries spiked higher during pandemic, and more recently T-bills have moved materially higher. It is the size of the deficit that drives bond issuance above simply rolling maturities. The U.S. deficit is forecast to rise from $1.9T in 2024 to $1.94T in 2025, before dropping a bit then moving a lot higher past 2028. I’m sure we can all agree, there is no shortage of bonds/bills in the foreseeable future.

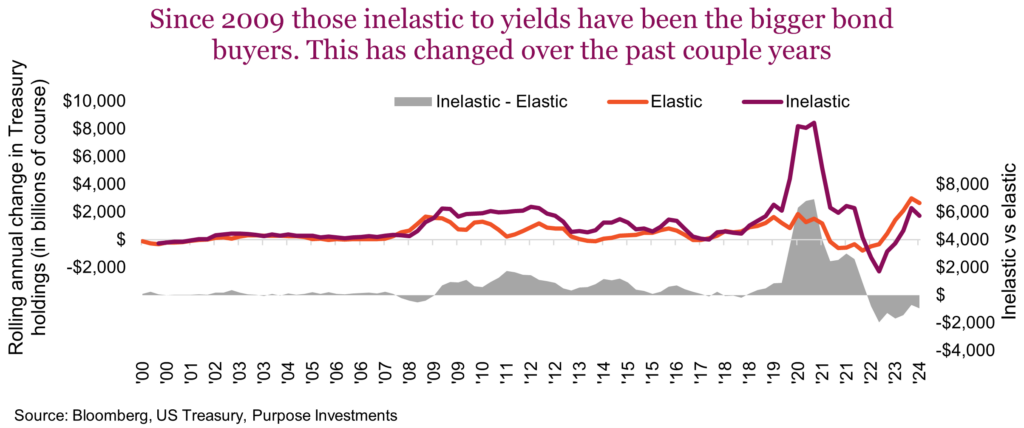

Now to the demand side and this is where things get interesting. There are many holders or buyers of Treasuries including households, hedge funds, pensions, insurance companies, the Fed, banks, foreigners, money market funds and mutual funds. Some of these buyers are sensitive (elastic) to different bond yields and some are not (inelastic).

Inelastic demand for yield: For pension and insurance companies it is more about asset/liability matching than the specific yield available in the market. They have a relatively inelastic demand for yield. Or the Fed, QE or QT has never been about buying or selling bonds because of the current yield available – completely inelastic. Banks buy treasuries often when they have excess capital and not enough demand for lending, not really caring about the level of yield.

Foreign central banks are an interesting one. The conspiracy folks say other global central banks are trying to diversify away from holding U.S. treasuries for political reasons. But most of these holdings are the result of global trade. Exporter sends stuff to that hungry U.S. consumer and receives USD back. So they exchange for their local currency at their private bank, and now that private banks has USD. They end up exchanging up the line to the central bank of the country, which then could sell or simply hold the USD. And holding the USD means buying and holding Treasuries.

Maybe they want to diversify reserves for political reasons. Or trade flows have gradually adjusted to tariffs and other factors, causing less direct export to the U.S. In May 2018, China exported $52 billion of goods to the U.S., in 2024 the average has been around $30 billion. When they buy Treasuries they do not care about the level of yield. Their demand too is inelastic to yields, now clearly a smaller buyer.

Elastic demand for yield: Households, money market funds, mutual funds, hedge funds, these are the groups that are very interested in what the current yield is. Me, you, clients, investors of all sorts have been attracted of late to investing in bonds, HISAs, money market, etc. because the yield available today is higher than it has been in many years. And why not. If your bonds can provide a 5-6% return for your portfolio, then you only need a bit more from equities to reach that 6-8% return baked into many financial plans. Or if cash can provide 4-5%, that is much more than near zero. Hence why the small trickle into cash products has ballooned to a raging river.

Inelastic demand for yield: Pensions, insurance companies, the Fed, banks, foreign central banks

Elastic demand for yield: Households/hedge funds, foreigners, money market funds, mutual funds

Why should we care as long as someone keeps buying the bonds to keep the government doing what it does? If yields fall, say from 4% to 3.5%, some of those elastic buyers may decide that just isn’t attractive enough. Or what happens if we reach 3%, or 2.5%? Because more of the current bond buyers are more sensitive to yields, even slowing economic growth may not push yields as far down as in the past. The lower yields go, the more buyers start to balk.

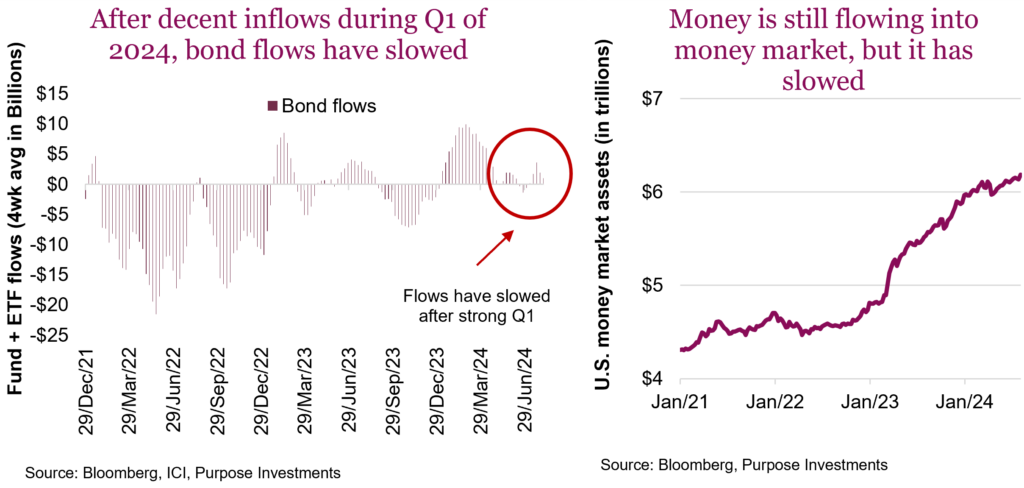

Yields on cash have not come down yet in the U.S., as the Fed has not started to cut. But it is likely coming soon. And perhaps that has even been enough as flows into money market funds have slowed; still positive but the raging river inflows have slowed to more of gentle river. And with that drop in bond yields over the past few months, the inflows to bond funds & ETFs has slowed quickly.

Final thoughts

With a higher proportion of bond/bill buyers having a higher elasticity of yield demand, this may result in a shortage of buyers should bond/bill yields fall too far. This may dampen how low yields go and also limit how high they could go, as higher yields would attract more buyers. Overall, greater elasticity of demand for yield may very well dampen the volatility of yield (and the price of course), keeping yields more rangebound than before.