Market Ethos

March 24, 2025

Question time

Sign up here to receive the Market Ethos by email.

This week we are testing out a new idea. Ok, it isn’t new as we borrowed the idea from a European bank research report, but it is new for Ethos. In any given month, there are many questions from advisors and investors, and not surprisingly there is some overlap. So, from time to time, we will use Market Ethos to provide relatively succinct answers to some of these questions.

Q: Is it too late to add to international equities?

A: Since 2010, the U.S. equity market has really dominated most others, thanks to significantly higher earnings growth. There have been periods when it looked like leadership was pivoting back to international markets, but those turned out to be false signals. So is the strong start for international developed equity market performance a new trend, or another head fake?

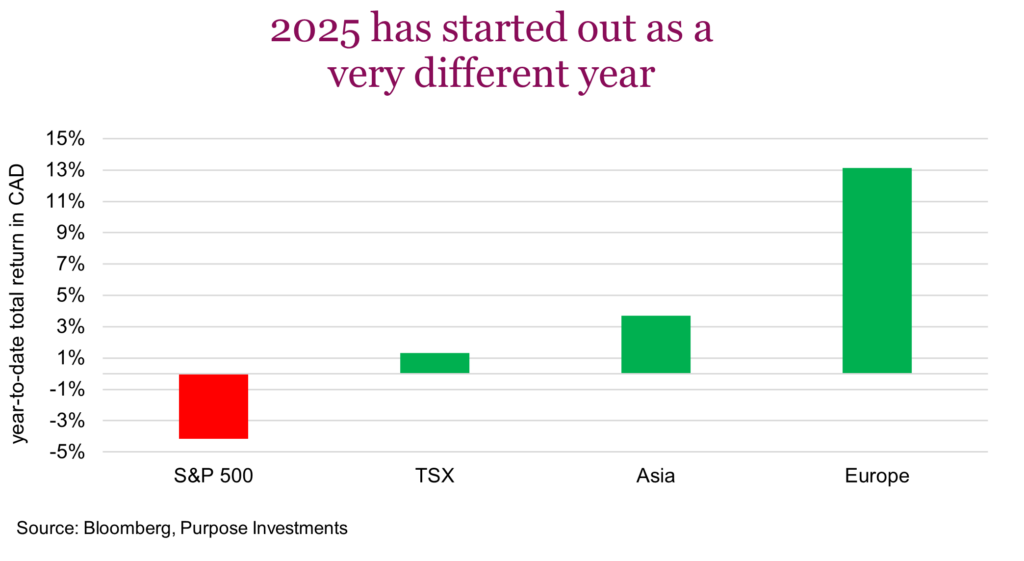

This year has started off with European exceptionalism standing out, compared to the U.S. As the end of Q1 nears, the S&P 500 is down -4%, Asia is up +4% and Europe is up a strong +13%. That is a pretty big delta. Adding greater importance to the question is the fact that most portfolios are likely overweight U.S. after so many years of relative outperformance compared to international.

At some point, the leadership will change. History tells us there are very long periods of relative outperformance which lead to long periods of underperformance. Unfortunately that will only become known in hindsight. The timelier question is whether this relative rally has legs.

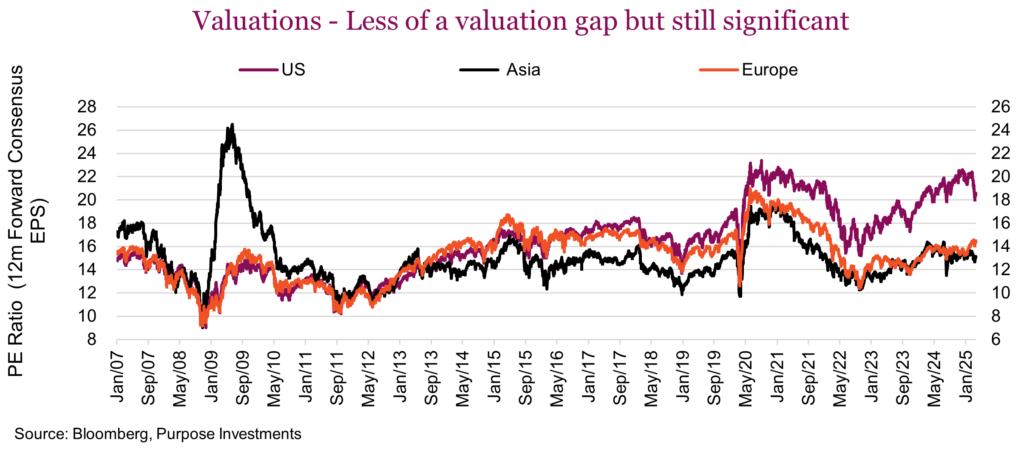

Valuations are a bit less compelling – Given the rally in Europe, and to a lesser extent Asia, combined with the drop in valuation for the S&P 500, the valuation gap has narrowed a bit. Europe and Asia are now about 14-15x while the U.S. is just above 20x. But we would point out valuations have not been a good predictor of relative performance, noting how the spread remained high for many years.

Sticking with fundamentals, the relative earnings growth gap is narrowing even faster. In December, the market consensus was for 13% U.S. earnings growth comparing 2025 estimates vs 2024. This has now fallen to 10%, still higher than Europe and Asia but moving in the wrong direction. Meanwhile, Europe has improved from a paltry 5% to 7%, with Asia going from 2% to 4%. This has the relative earnings growth rates narrowing.

Fiscal spending – After Covid, government spending went in divergent directions. Europe brought its deficits down steadily over the past few years, closer to pre-pandemic levels. Meanwhile the U.S. kept spending, still with a deficit but more aligned with a full-on recession or war. Much of the U.S. exceptionalism has been their willingness to spend, spend, spend. Not just government, but the consumer as well. A dollar hits an American’s pocket, time to go buy something. European consumers have been much more restrained, similar to their government.

This is changing. Today we now have the U.S. dialing down fiscal spending (DOGE) and Germany, followed by other European countries, increasing fiscal spending. This is a total flip and may lead to a continued boost for European earnings and a headwind for the U.S. Hard to say what the consumer is going to do, but consumer debt in Europe is about 52% of GDP compared to 70% in the U.S. Their consumer is in better shape.

Trump – Then there is Trump. Or more specifically the policy flip flopping, creating more uncertainty for the U.S. compared to other areas. Given that the wording out of the U.S. tends to be antagonistic, this is further leading money to relocate. Europe has just enjoyed some of the strongest inflows in many years. Could this be in part a patriotic reallocation? Maybe. It is certainly calling into question the sustainability of U.S. exceptionalism.

Currency has been another contributor. While the CAD/USD has remained relatively stable over the past month, make no mistake, both these currencies are falling vs the euro and yen. The euro and yen are still cheap.

While the valuation gap has narrowed somewhat, it still remains favourable for international developed markets compared to the U.S. And if the earnings revision momentum continues, so should the relative performance. Hard to say if this is the start of a longer-term secular trend of international outperformance. However in the near term, it could easily have legs. Many portfolios remain relatively underweight international. We don’t think it is too late, even for latecomers.

Q: If elevated volatility is anticipated for the rest of the year, what should be added to a portfolio to help manage the impact?

A: Our expectations for 2025 are rather muted. Global equity markets have enjoyed two very strong years and while a third is not impossible, it is less likely — especially considering the policy risks in today’s markets, including tariffs. However, our muted return expectations do not translate into a flat market. Instead, we believe there will be bigger swings, some up and some down. This puts additional focus on the defensive characteristics of a portfolio.

In years past, this would simply mean more bonds. The challenge is that inflation remains elevated and volatile, which may reduce the defensive characteristics of bonds. Higher inflation typically results in higher correlations between equities and bonds than in years past. The silver lining is that bonds now carry higher yields. Less portfolio defense but more performance contribution.

This creates an environment in which diversifying your defensives appears prudent. The biggest concern today is the uncertainty around tariffs. We do believe, even if the news is bad, this uncertainty will become less uncertain in the coming weeks or months. The market can often handle bad news better than uncertainty. And this may create a market bounce at some point. However, a bit further downfield, the current period of uncertainty may start showing up in earnings and in the economic data. This may lead to another challenging period for markets as people will start talking recession risks.

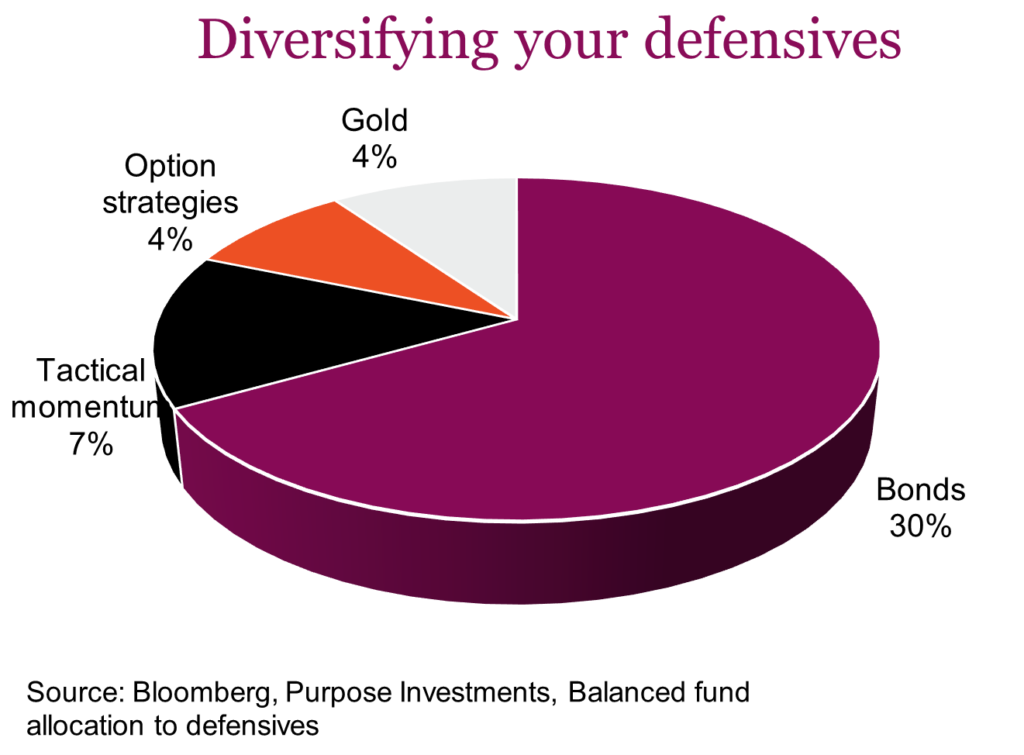

Bonds, with decent duration, remain the core of defense, especially if weak economic/earnings data fuels rising recession risk. But with higher inflation, looking for other sources of defense to complement is best. Volatility management alternative strategies, gold, tactical momentum are some of the defensive diversifiers we currently employ. For illustrative purposes, the chart below shares diversified defensives beyond bonds.

We believe taking a more diversified approach to a portfolio’s defense will be increasingly important in 2025.