Market Ethos

April 28, 2025

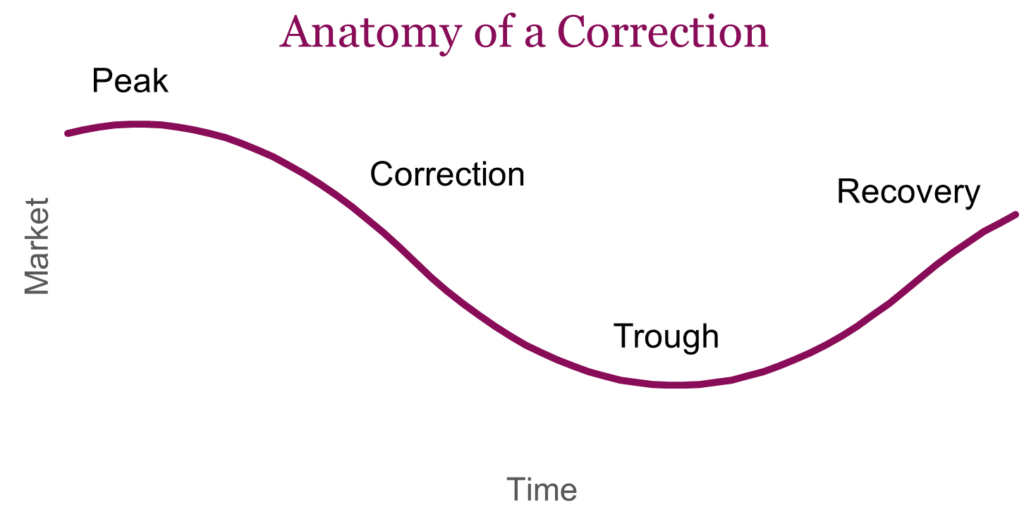

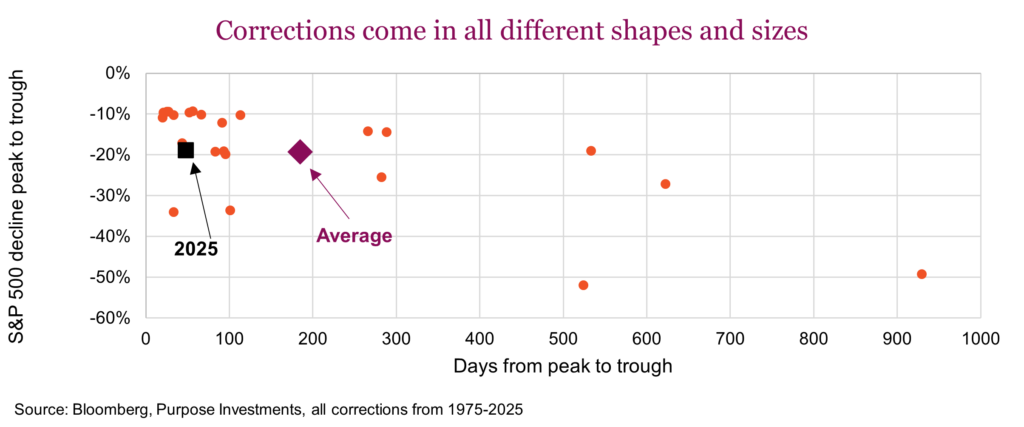

Corrections come in different shapes and sizes

Sign up here to receive the Market Ethos by email.

What happens in the stock market today has happened before and will happen again.

Jesse Livermore, Reminiscences of a Stock Operator

It is true that if you look back far enough you can come across very similar scenarios for just about anything that is happening. While it may be hard to believe there were past periods where U.S. government policy announcements induced corrections or sent markets haywire, it was actually more common decades ago. Government policy in more recent history, the last couple decades, has been more market friendly perhaps because of the percentage of the U.S. population with a 401k (their version of RRSP).

Corrections, or periods of market weakness, experience similar paths from correction to trough to recovery. But every correction is somewhat different. The starting point, the speed, the duration, the cause(s), the bottom and the recovery all vary substantially from one to the next. And to be frank, the last few corrections have been especially unique, assuming we can measure degrees of uniqueness. All would agree Covid was a very different period of market weakness — you would have to go back a long time to see a global health crisis causing markets to drop that fast and then recover that quickly. The inflation-induced correction of 2022 certainly was not a plain vanilla correction. And now we are in a 100% policy-induced correction.

Most of us have probably seen those statistics that talk about the average drop in markets, how long it takes to reach bottom and how long to recover. The challenge with these is that the ‘average’ hides so much variance in the data, does it really help provide insight? The following graph contains every S&P 500 correction since 1975, with the decline in the S&P 500 and the number of days to reach the bottom. To simplify, we will assume the current correction bottomed on April 8. That may or may not hold true as this year progresses. Clearly the variance in experiences is very high, limiting any insight from a simple ‘average’.

The variance in duration and depth of corrections isn’t the most challenging aspect of investing. The bigger challenge is the variance in performance of portfolio diversifiers or defensive holdings. Especially given the high level of uniqueness of the past few corrections. For instance, during the Covid correction bond yields fell, providing a good stabilizer while the US dollar rose. But international equity exposure fell as much as the S&P and gold declined as well, not offering much diversification benefit. In 2022, a correction triggered by rising inflation risks was very different. Bonds were clearly no winner, and neither was gold and international diversification. The U.S. dollar was the best diversifier for a portfolio. Now in 2025, international equities have held up much better, bonds have been flattish, the US dollar has not helped but gold is shining bright.

Herein lies the challenge. It would be understandable for investors to have shied away from international equities following Covid and 2022, believing the diversification benefit was kaput. Then came 2025 with international equities holding up better and rebounding strongly, almost back to all-time highs. Flows are currently very high into international equities. Or who hadn’t become frustrated with gold during the previous two corrections compared to the love of gold during this period of weakness. Inflows to gold bullion ETFs have taken off. And maybe bonds feel subpar so far this correction (we would point to large bond outflows in the past few weeks). Reacting after the fact is rarely a successful strategy when it comes to portfolio construction.

Diversify your defense

We cannot overstate the dangers of recency bias, even more elevated than normal due to the uniqueness of recent periods of market weakness. The inconvenient truth is different defensive strategies work better in some corrections than others. This applies to bonds, credit, commodity, international equities, factor exposures and alternatives. We don’t believe this current correction is over and weaker economic growth may be the next phase. This may flip what has worked so far, benefiting bonds and the U.S. dollar while perhaps hurting gold.

There are some key conclusions in our opinion. Just because a defensive diversifier has produced muted benefit in one of the more recent periods of weakness doesn’t mean it’s broken — it may just not be its kind of correction. Conversely, one type of diversifier that has worked well shouldn’t result in performance chasing as the next phase or correction may prove very different. Diversifying your defense across a number of different diversifiers has become paramount given unique corrections.