Market Ethos

June 16, 2025

Mind the cap

Sign up here to receive the Market Ethos by email.

One recurring discussion topic over the past few months has been the size factor — specifically what to do with small or mid caps. We have largely been avoiding the space, but thought this would be a good time to dive back in, sharpen our pencil and share some thoughts.

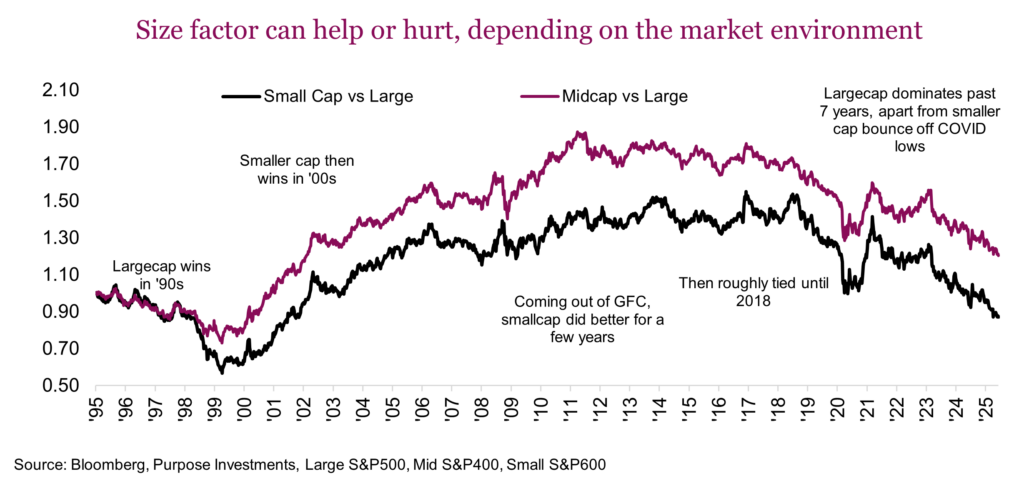

Super long term, there is lots of evidence of the size factor in the market, but it certainly isn’t a stable factor and can be very cyclical. The chart below is the relative performance of the small caps (S&P 600) and mid caps (S&P 400) each versus the large cap (S&P 500). A rising line means the smaller cap index is outperforming. One can easily see this is a very long cyclical relationship, with large winning in 90s, small winning in ‘00s to 2012, then large winning again since then.

There is also some research out there saying this isn’t cyclical, it’s structural. The rise of ETFs, and associated flows, are dominated by market cap-weighted index strategies. Of course, there are small and mid, even micro-cap ETFs, but the associated dollar flows are woefully smaller, favouring the large caps. Just ask any small cap portfolio manager, they will point out the amazing opportunities, or valuations in the space. But they’ll often share some frustration not knowing if or when this valuation discount will change. There may also be a supply issue as quality small companies can now stay private much longer than before, tapping private equity instead of public markets.

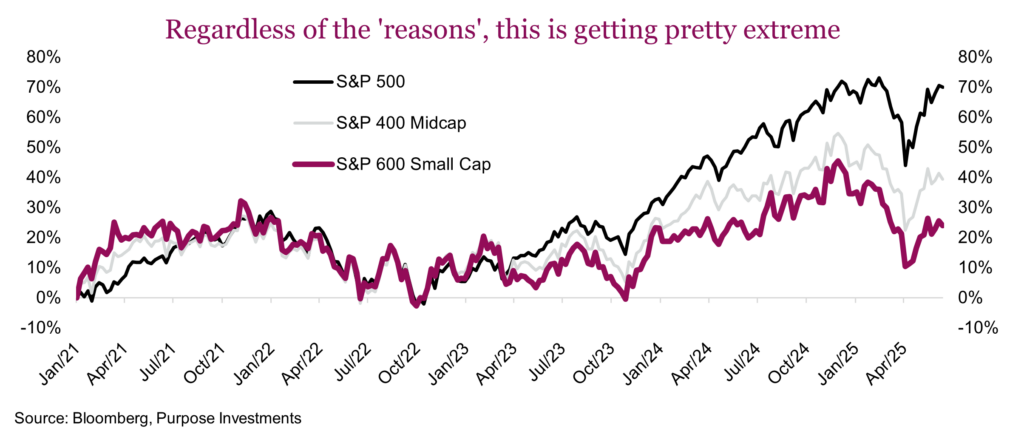

Money flows are certainly a contributing factor to the relative performance of the size factor, but this is getting a bit ridiculous. Since the end of 2020, we have the S&P 500 up +71%, S&P mid cap +40% and S&P small cap +25%. Perhaps the big question is whether this spread is creating a great opportunity?

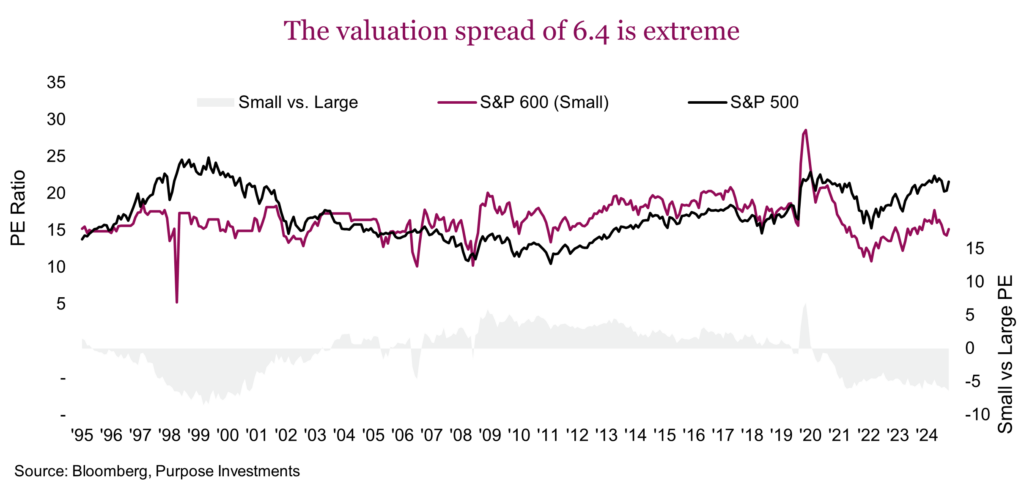

Valuations – This one is easy. For small caps, they are cheap at 15x forward earnings estimates compared to a long history average price-to-earnings ratio of 16.2x. On a relative basis vs large cap, they are VERY cheap with a 6.4 multiple point spread. Sure, the spread did get a bit higher in the late 1990s with a peak of 8.2, but we are talking outlier territory valuations in either case. It’s also worth noting the 1990s large cap outperformance set the stage for small cap outperformance for the following decade. Let’s agree, valuations offer one compelling reason to support smaller size allocations.

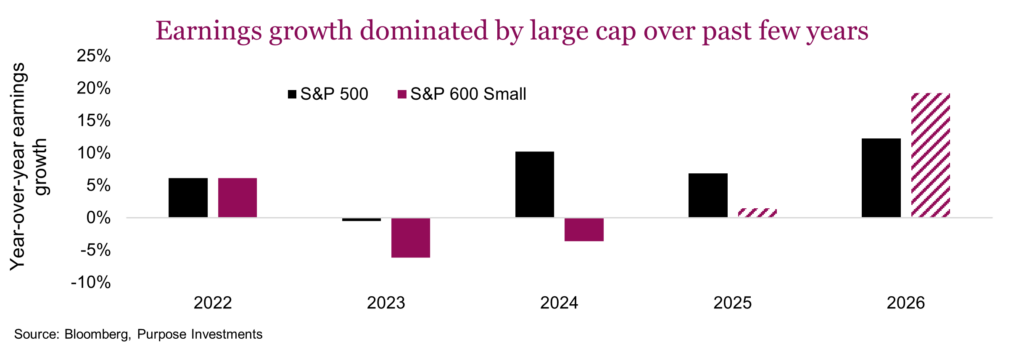

Earnings growth – Then again, valuations have been a compelling reason since late 2021 and that certainly hasn’t helped predict future relative performance. Given smaller cap earnings tend to be more volatile, perhaps a bit of a lower multiple is warranted. Arguably a more important factor for relative performance across the size factor is earnings growth. If earnings are growing faster in smaller caps versus large caps, this often carries over to relative performance. We would point out the dominance of large cap versus small caps since the early days of 2023 lines up with multiple consecutive years of higher earnings growth for large cap versus small caps.

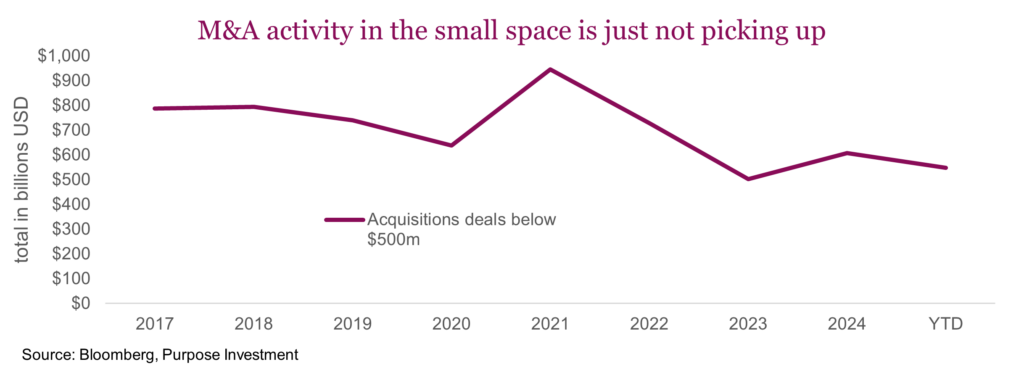

M&A – If valuations are so attractive, one would think acquisitions would be a more frequent occurrence. Unfortunately, the relative valuations are so attractive mainly because the large caps are trading at very high multiples. And higher yields have made the IRR hurdle on an acquisition higher. The following chart is the total annual dollar value of acquisitions below $500m. As we are 44% through 2025, this number has been adjusted to an annual pace.

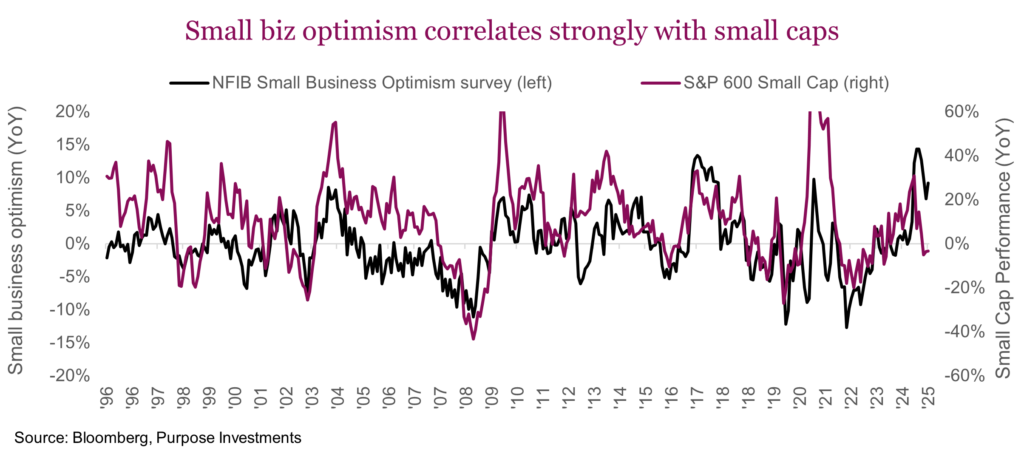

Confidence – With so much uncertainty in 2025, this may not be too surprising. Confidence is critical for smaller caps to outperform. CEO confidence has been falling in 2025, as has the NFIB small business optimism index. To be bullish on small caps one would have to believe corporate optimism is going to improve later this year. It is possible — some resolutions on trade or other policy headwinds may help. But if the economic data does soften later this year, that too will provide a confidence headwind.

Financial conditions – More Fed rate cuts should help smaller cap relative performance and there are likely some rate cuts coming later this year based on the consensus. How much this may drive performance is really hard to say, especially since we have enjoyed some pretty easy financial conditions over the past few years once you incorporate lending standards, spreads, capital availability, etc. Cuts would help.

| Factor to consider | Positive of negative for smaller caps |

|---|---|

| Valuations – spread of over 6x | Positive |

| Earnings growth – large relative to small | Negative |

| M&A Activity – still lacklustre | Negative |

| Economic & CEO confidence – weak but maybe overreacting | Tough one |

| Financial conditions – moving in right direction | Positive |

Final thoughts

Earnings growth has been decelerating in 2025 across most markets, which has been even more pronounced among smaller caps. Perhaps the valuation spread compensates for this somewhat, but we would want to see some signs of stability or potential turn in earnings growth to get excited. Or a turn in confidence and some M&A. The setup may be in place, but the catalyst appears to still be missing.