Market Insights

August 19, 2025

Portfolio checklist: A look under the hood

Sign up here to receive the Market Ethos by email.

It’s that time of year again. Just as families are replenishing supplies and checking off back-to-school lists, investors can also take the opportunity to conduct a portfolio checklist/review. After a sustained run in equities, particularly in certain sectors and individual names, portfolio concentration may be higher than intended. This is not about stepping away from the market, rather, it is about understanding what you own, identifying areas where exposure may have grown disproportionately, and ensuring your investment profile remains consistent with your objectives.

Concentration risks in a market on a high

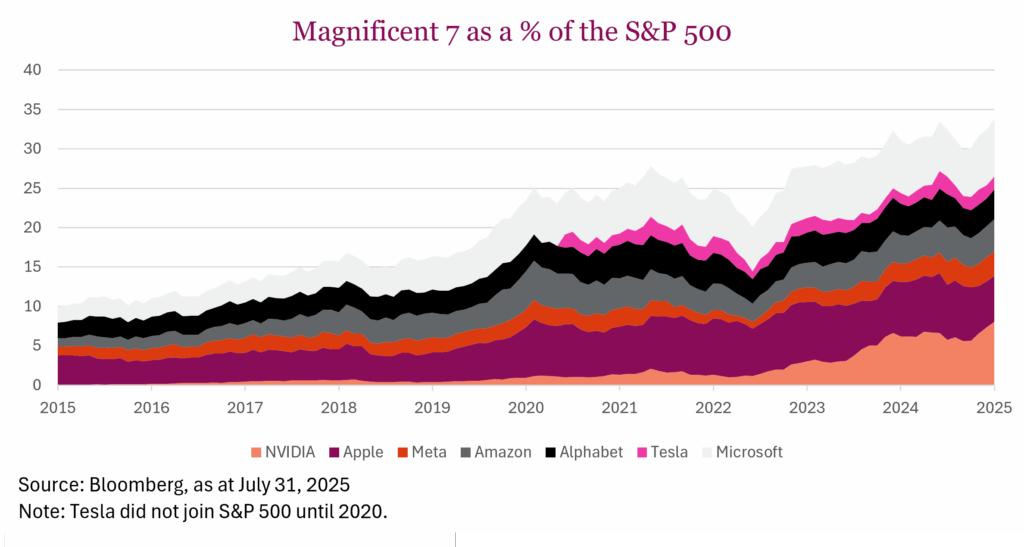

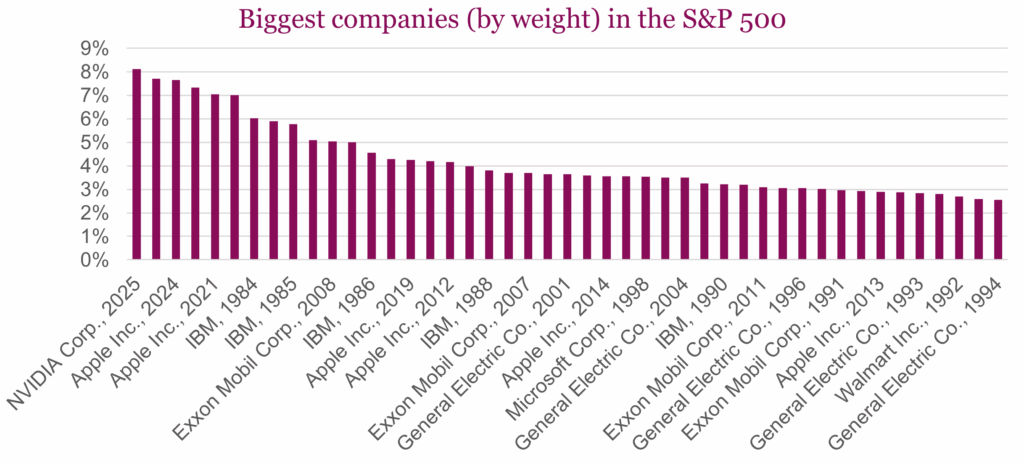

In the U.S., the S&P 500 has never been as concentrated in a single stock as it is today. Nvidia now represents more than 8% of the index, the highest weighting for any company in its history and surpassing even Apple’s dominance during the pandemic. Microsoft follows at roughly 7.1% and Apple at about 6.3%, both ranking among the largest index weights ever recorded. Nvidia’s market capitalization has grown approximately 45% over the past year and +1,400% over the past five years, reaching $4.3 trillion at the time of writing, about 37 times the average size of an S&P 500 constituent. Technology now makes up nearly 34% of the index, up from 26% at the end of 2020. Direct comparisons to earlier years are complicated by the 2018 GICS sector reclassification, which moved Alphabet, Meta, and several other large companies out of tech and into the expanded communication services sector (previously telecom), while Amazon has always been classified in consumer discretionary.

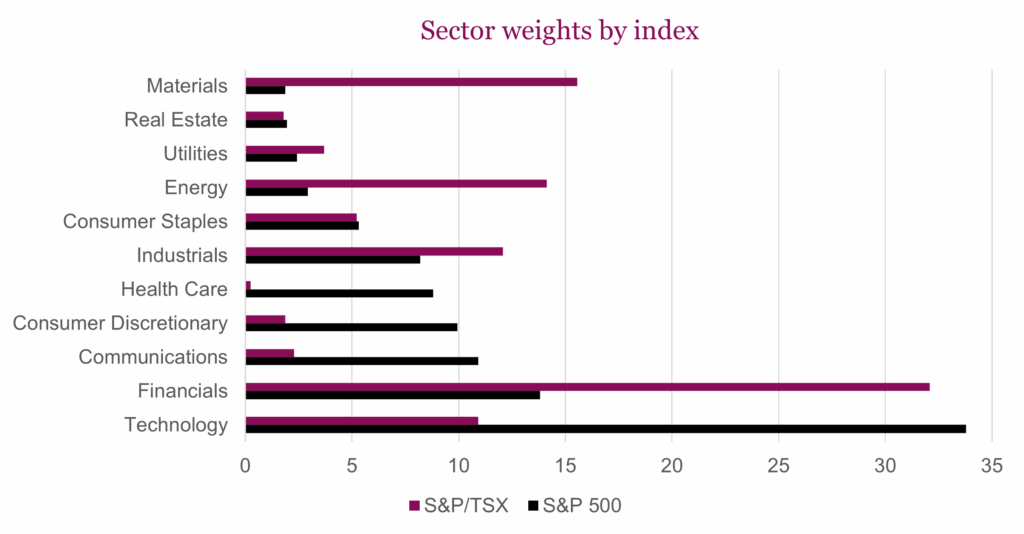

Canada’s market tells a similar story, albeit with different drivers. RBC holds roughly a 6.7% weight in the S&P/TSX, with Shopify close behind at 6.1%. Financials dominate at approximately 32% of the index, while materials, boosted by gold’s strong performance, now represent about 15.5% of the index. Energy, industrials, and technology also hold double-digit weightings. While these concentrations are far below historical extremes, it is worth recalling that in 2000, Nortel comprised more than one-third of the then–TSE 300, an extraordinary level of dominance that influenced index performance until its collapse. We are certainly not drawing parallels to the current situation, but history underscores that extreme concentration can carry its own risks and consequences.

While record highs in major equity indexes make security and sector concentrations the most obvious starting points for a portfolio review, the checklist does not need to end there. Other elements such as geographic exposure, asset class balance, style tilts, currency risk, fixed income structure, and liquidity needs should also be assessed. The specific areas to focus on will vary by investor, but a thorough review ensures the portfolio reflects both current market conditions and individual objectives.

Seasonality offers a good time for a look under the hood

Concentration risk can amplify market swings and unintended exposures can accumulate over time. Ask yourself: Does any single stock account for more than 6–8% of your portfolio? Is any sector more than 20–25% of your equity exposure? Do you hold multiple funds or ETFs that overlap significantly in their top holdings? Have recent winners created an unplanned bias? Do your holdings still align with your long-term investment objectives and risk tolerance?

Rebalancing is not an exercise in market timing. It is a disciplined process rooted in the principle that long-term success comes from time in the market rather than timing the market. By trimming positions that have grown beyond intended levels, you can lock in gains, reduce single-stock and sector risk, and preserve a balanced allocation while continuing to participate in market opportunities.

Concentrated positions have delivered strong returns in recent years, but leadership can change quickly. A portfolio review, similar to preparing for a new school year, can help keep you organized, intentional, and well positioned to navigate both the opportunities and the risks that the next season may bring.

Source: Charts are sourced to Bloomberg L.P., and Richardson Wealth unless otherwise noted.

Authors: An Nguyen, VP Investment Services; Phil Kwon, Head of Portfolio Analytics; Andrew Innis, Analyst

Disclaimers

Richardson Wealth Limited

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson Wealth Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by the author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Richardson Wealth does not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise.

Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice.

The particulars contained herein were obtained from sources which we believe are reliable, but are not guaranteed by us and may be incomplete. This is not an official publication or research report from Richardson Wealth, and is not to be used as a solicitation in any jurisdiction.

This document is for informational purposes only, and is not being delivered to you in the context of an offering of any securities, nor is it a recommendation or solicitation to buy, hold or sell any security.

Richardson Wealth Limited, Member Canadian Investor Protection Fund.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.