Market Ethos

September 8, 2025

Cautiously Canadian

Sign up here to receive the Market Ethos by email.

We are proudly Canadian — this is an awesome country with great people. With nearly a quarter century of asset allocation work, we would also say holding more Canada than our peers has been a frequent theme. Not always of course, and there have been times that holding more Canada was a disadvantage. Some may say we suffer a bit from home country bias. While familiarity with your home market is often comfortable, we believe our Canada view is a bit more thoughtful. Most of our clients are Canadian, with largely Canadian future liabilities, so owning a bit more Canada means less currency risk. Dividend tax credit is another big one. Not enough work in the asset allocation world incorporates tax.

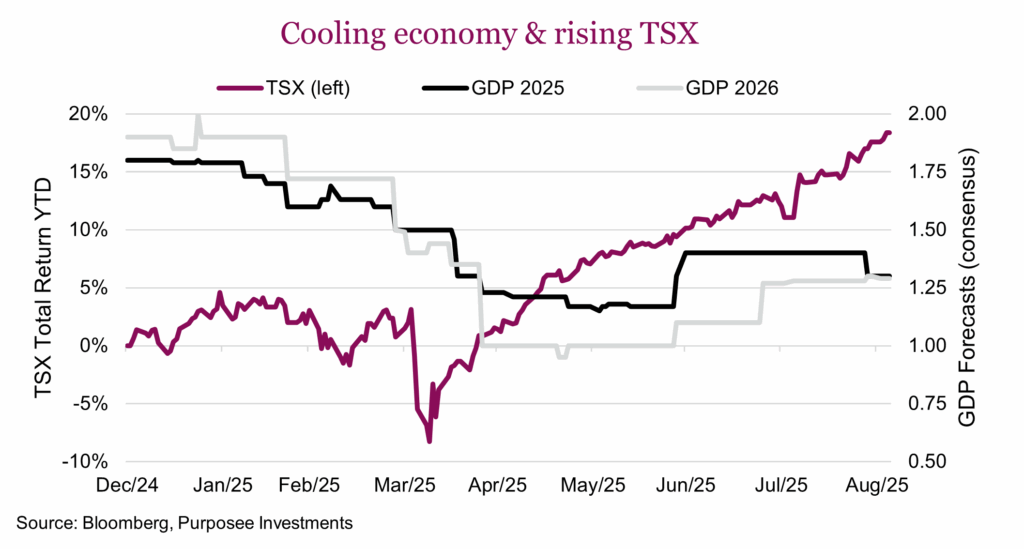

So far this year Canada has been great, even with all the headlines over tariffs and a recent negative Q2 GDP print. The TSX is up an impressive 18% so far this year, making Canada one of the better-performing markets — roughly double the return of global equities. We all know the TSX isn’t the Canadian economy, and this year certainly highlights that fact. Economic forecasts for 2025 growth have fallen from 1.7% down to 1.3% with 2026 consensus declining from 2.0% to 1.3%. Tariffs are taking a bite out of economic growth as is a tepid housing market. The stock market can move somewhat independently from the economy, but they are still somewhat tethered. So why is there such a big divergence?

Most of the TSX’s gains this year have come from two sectors: financials, which are dominated by the banks, and materials which are dominated by the golds. Materials have contributed 6.4% of the TSX’s 18.3% advance and Financials another 5.8%. So, two thirds of the market gains have come from these two sectors. Golds have nothing to do with Canadian economic growth, and those companies are printing a lot of earnings given record gold prices. Gold miners contributed a paltry 2.3% of TSX earnings in 2022 — over the next four quarters, that percentage has risen to 9%. In dollar terms we are talking $5 billion to $21 billion over a few years. That is a lot of bling.

We do like our gold exposure and naturally wish we had more. There are many reasons behind this admiration beyond simple price appreciation. But we do have some hesitancy, as those earnings can disappear as quickly as they appear. Materials and Energy are called cyclicals for a very good reason. That is why the golds, even after such strong gains, are not trading at a high multiple — in fact they are lower. The market usually does not pay a high multiple on cyclical earnings.

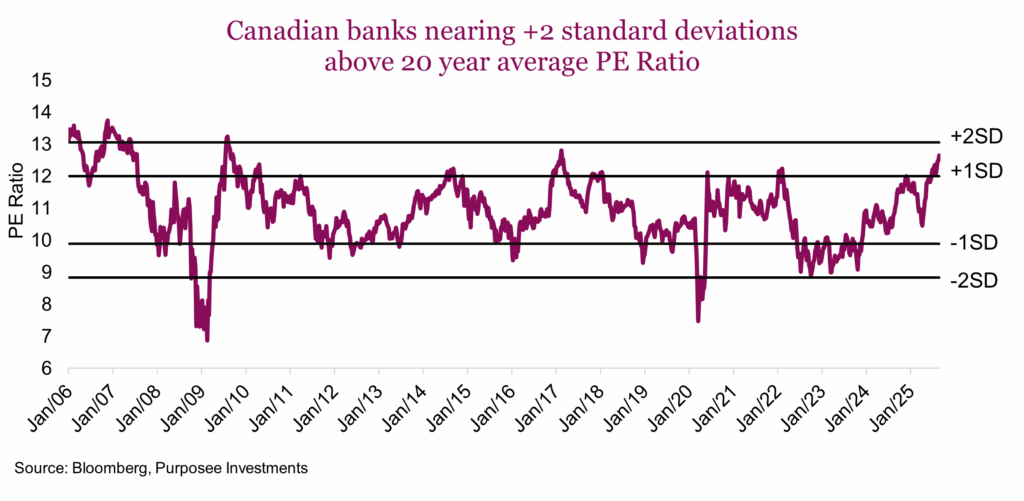

While gold may have nothing to do with the Canadian economy, Financials, dominated by banks, are a clear proxy for the Canadian economy. This is where things get a bit more challenging. The banks enjoyed a good quarter of earnings results but are now bumping up against a valuation ceiling.

The chart below is the price-to-earnings for the banks based on consensus estimates for the next twelve months. We added lines representing one or two standard deviations above or below the long-term average. With an economy slowing, that is at odds with paying historical premium valuations for bank shares. Given this part of the TSX is so important and large, it’s certainly a risk.

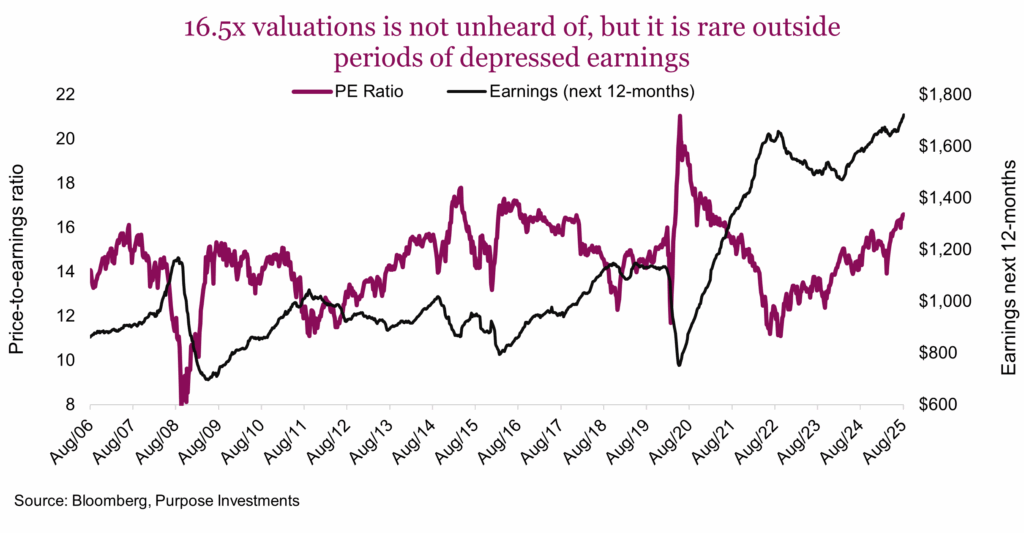

In aggregate, the TSX is certainly not as cheap as it has been over the past few years and maybe getting close to the expensive zone. Because of a rather sizeable weight of cyclicals in the TSX, aggregate valuations are not a big deal. At times when cyclical earnings are depressed, those sectors can trade at high multiples given the longer-term value of the companies. Energy could be in this bucket at the moment. Still, 16.5x is expensive for the TSX, even with decent earnings growth. Usually, the TSX trades at these or higher valuations because earnings are really depressed.

Of course, the TSX could move higher from here. Maybe banks see already stretched valuations push higher. Or the golds see some multiple expansion if the market believes these booster profits have longevity. Energy could see a rise that would likely lift the TSX or maybe another huge quarter from Shopify. Guess what we are getting at — another move higher for the TSX is becoming harder to fathom.

This may sound a bit too sanguine, but there is another factor we did not mention and that is flows. There is a trend afoot, with investors becoming a little less enamored with U.S. equities and incrementally allocating more to international markets. Some of that is landing in Canada. And it doesn’t take much to move the Canadian market. $100 billion can come out of U.S. equities without any much impact. On the other hand, $10 billion landing in Canada can move prices. This factor, if it continues or accelerates, easily dwarfs any concerns over valuations.

Final thoughts

We aren’t negative Canada, but we are not nearly as enamoured as we were few quarters ago. We can see some scenarios lifting the Canadian market higher, but the challenge is they are becoming fewer and farther between. Maybe more international inflows, maybe some more multiple expansion, maybe improving earnings growth, maybe energy comes back into vogue. It does feel we are stretching a bit. And given we have enjoyed over +18% this year with four months still to go, it’s already a helluva year.