Market Ethos

September 22, 2025

Gold: bull(ion)s vs bears

Sign up here to receive the Market Ethos by email.

The TSX is now up 22% so far in 2025, one of the leading markets globally. And much of this performance is thanks to the TSX having a healthy amount of gold miners in the index. The gold miners’ weight in the TSX has obviously been climbing, starting the year at 7.2% and now about 9.4%. This subcategory of the Materials sector is responsible for about one third of the TSX’s advance. The golds contributed 6.7% — without them the TSX would be a more average +15%.

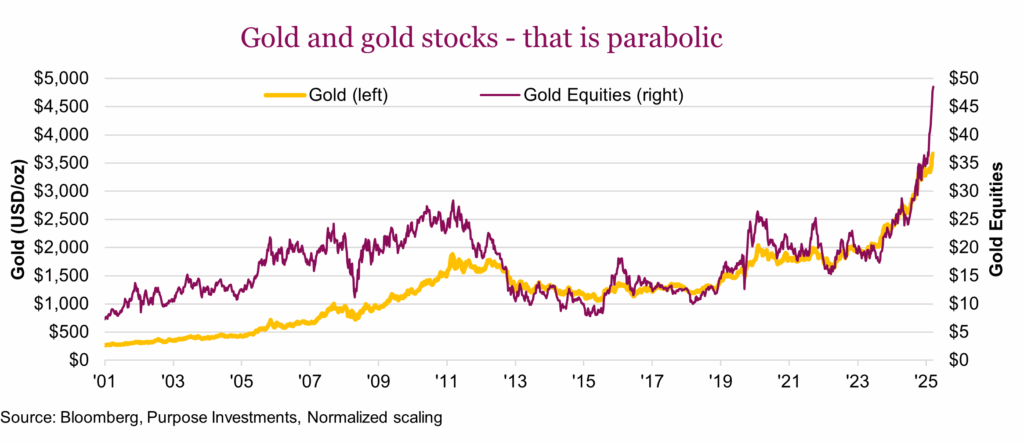

Gold bullion prices are up 40% this year, while the TSX Gold sub industry index is up 95%. This sharp rise is creating FOMO for investors with no gold exposure, and hesitation for those who already hold some. Those with no exposure are asking if it is too late to buy, while those with some exposure are wondering how high this could go — and looking to avoid taking the full ride.

So, for those who are looking to get in and those who are looking to get out here are the bull and bear cases:

Bull case for gold

There are the usual evergreen supporting arguments for holding some gold in portfolios. It provides crisis alpha, often performing well during periods of high market stress. It is a real asset, the OG real asset, with a long history of keeping up with inflation. It is often uncorrelated with other asset classes, especially when you want things to be uncorrelated. It provides currency protection in a world of fiat currencies. And of course, it is shiny and pretty and accessorizes well.

More recently, other factors have increased investor demand for gold exposure. Policy decisions in the U.S. are certainly contributing, across a large range. The Fed’s independence, inflationary policies, the decision years ago to seize assets of Russia’s central bank, are all causing some erosion of faith in the US dollar and boosting the desire to hold more gold. High debt levels with rising deficits have more investors wanting to store value in hard assets.

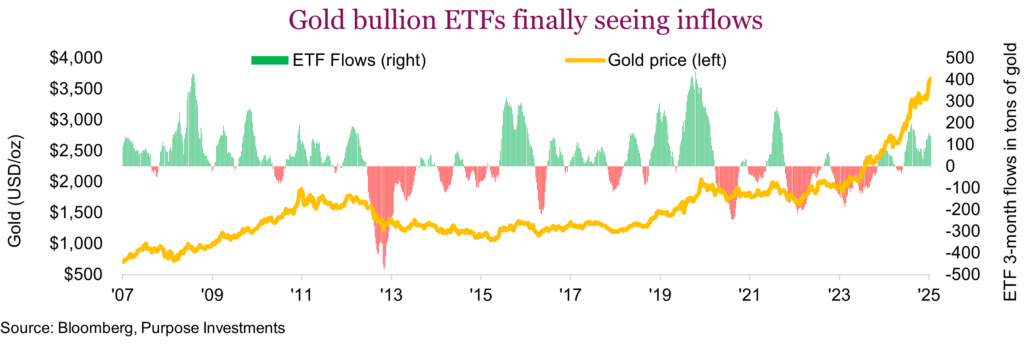

These reasons are all a little hard to quantify. One issue is that if a ‘hard asset’ can go up 100% over a couple years, it can also go down 50% just as easily and likely more quickly. So, we had better have some new tailwinds to keep this huge rally going. One could be flows. Fund flows into gold bullion EFTs have only recently turned positive and the magnitude is not huge by historical standards, meaning it could expand to levels seen during past gold runs. And gold miner ETFs (XGD, GDX, RING) have actually seen outflows. Perhaps part of this muted response, from a fund flow perspective, is because of crypto, with many traditional gold bugs having switched over. If these flows accelerate to the upside, enticing investors with past performance, that is a reason to be bullish.

Gold miners are now making a ton of money. In 2023, the gold miners in the TSX contributed about $6 billion in earnings for the index and is now over $21 billion based on forecasts for the next 12 months. With gold miners printing money, historically this could lead to a merger/acquisition binge. That hasn’t really taken off yet and if it did, could mean more upside.

So clearly there are some evergreen reasons to like gold and some more timely reasons. No question this could keep it going but after such gains, long investors are becoming weary.

Bear case for gold

There are many reasons to continue to love gold and want exposure in a diversified portfolio. We typically like its crisis alpha characteristic, so when there is no apparent crisis and gains are outsized, it certainly gives us pause. One risk is that after such strong gains, if a crisis did occur, gold exposure could easily be high on the list to take profits. That may mute its alpha crisis ability.

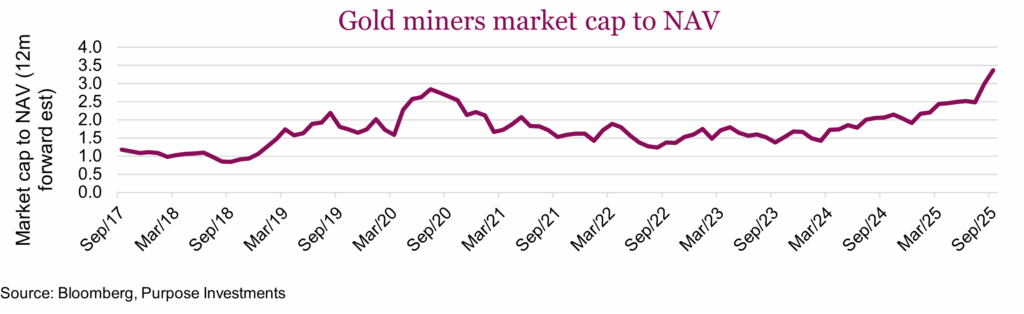

Technically speaking, things are extended. The RSI (relative strength) of gold bullion is 71, TSX miners 78. Usually anything over 70 is a sell signal. And while earnings have expanded, share prices have risen much faster. The chart below is the total market cap of miners to their net asset value based on forward 12-month estimates. Valuations are a tough one and our old rule of thumb is when folks start talking valuations regarding gold companies, we should be concerned.

Maybe some will say the Fed cutting rates is positive. But that is a challenging argument given gold broke its relationship to yields, both nominal and real, years ago. If rising yields over the past few years didn’t crush the price of gold (it didn’t), why would a few rate cuts lift the price?

Then there is Asia. Strong demand from Asia over the past few years, incrementally driven by China, has been a positive trend. Anecdotally, Chinese equity market investors suffered a flat decade in the 2010s, and during this period turned to real estate. Then that blew up, so gold became a popular destination. But now their equity market is performing well again, +40% over the past year. It would not be a leap for many to pivot back to stocks.

Or look at other valuation metrics for gold. Gold to copper, at 813x (oz to lbs), has never been higher with our data going back to mid-1980s. Same with gold to oil, at 58x. Of course, that is ignoring the brief period when oil went negative and back again,(that really messes with ratios).

Final thoughts

There you have it, reasons to be bullish, and reasons not to be. And we are sure we missed a few. As long-term holders of gold, for long-term reasons, we likely will always have some exposure. But with these kinds of fast gains, we also have to be profit harvesters. That could be right-sizing positions that have grown too large or pivoting some exposure from miners to bullion to reduce risk without exiting gold exposure. Remember the last time you were on an airplane and looked sideways out the side window? You probably didn’t see any trees, because trees don’t grow to the sky.