Market Ethos

23 March 2026

Waiting at the train station

Sign up here to receive the Market Ethos by email.

Someday this war’s gonna end

Lieutenant Colonel Bill Kilgore (Robert Duvall)

As hostilities broke out in the Middle East, markets were initially rather resilient. This resilience was likely supported by the view it could be a short-duration bombing event, similar to past episodes, amid improving global economic data. In fact, markets went up on the first trading day after the bombs started flying. After three weeks though, that resilience is fading and the conflict is weighing more heavily on markets.

Nobody knows how this conflict will evolve, but there is no shortage of views out there. Three near-term events we believe would elicit a more dramatic market reaction include: destruction of energy infrastructure, loss of American lives, and the prospect of boots on the ground. There have been minimal American casualties and boots on the ground still appears a very low probability at this time. However, there has been some energy infrastructure damage, which is contributing to more market weakness.

Our view from day one of this conflict was to see if markets showed enough weakness to create a potential opportunity. The general and very useful rule of thumb is market weakness from geopolitical events is just about always a buying opportunity unless there is a recession coming. Given the economic momentum, we continue to believe there is enough to absorb the hit from temporarily higher energy prices and disruption. That may change but for now that is our view. But this does not rule out continued weakness as the market multiple contracts due to uncertainty.

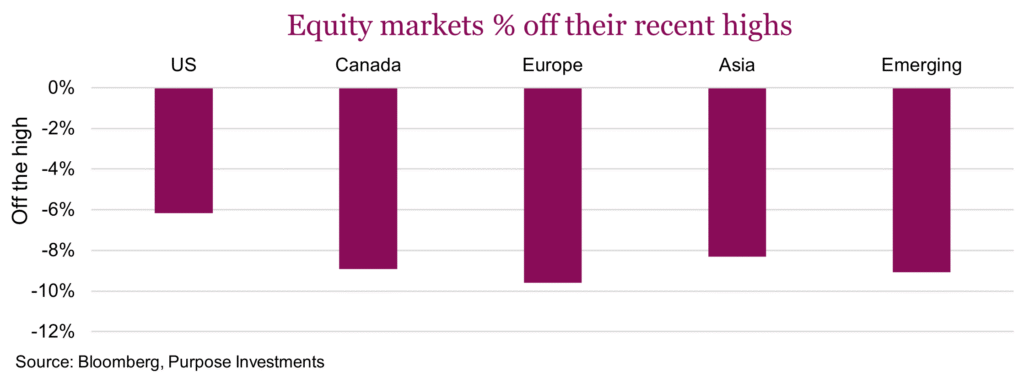

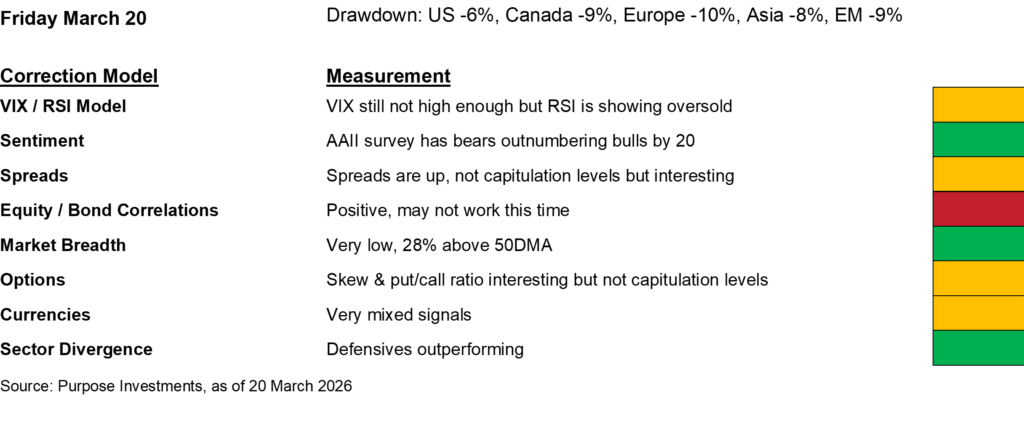

At the time of writing the S&P is now down -6%, TSX -9%, Emerging markets -9%, Europe -10% and Asia -8% since the conflict began. We wouldn’t call this a correction yet, but it’s getting close with some markets more interesting than others. On one hand the U.S. could pivot. President Trump does have a TACO reputation for a reason, when tariffs caused enough market angst, he pivoted. Could the same occur here? Gasoline prices, public polls on the conflict, mid-terms approaching, these are all factors that could elicit a pivot. Or things could get worse, either events in the Middle East or impact on the economy. That is the uncertainty thing.

Full disclosure, we do have a reputation for being early at times. But investing is like catching a train, it is ok to arrive at the station early — late not so much. And given our defensive tilt coming into this period of weakness, that does provide optionality to be more tactical. Without guessing at the war trajectory, here are some reasons to think about some dip buying:

Valuations – This pullback has certainly knocked a good amount of froth out of the markets. S&P 500 has just dipped below 20x, for the first time since tariff-induced market weakness. Generally, each market has seen their price-to-earnings fall by about two points. Europe is back below 15x, Emerging markets back down to 12x. We’re not saying things are cheap, but we’re certainly seeing a pullback and more intriguing valuations.

Correction watch – Let’s be fair, valuations are nice, but they never market tops or bottoms on a short-term basis. Dusting off our correction watch indicators, things are looking a bit more interesting. These are a basket of short-term sentiment indicators designed to measure oversold markets or capitulation. We are not seeing everything flashing a ‘buy’ signal, but enough to pique our interest.

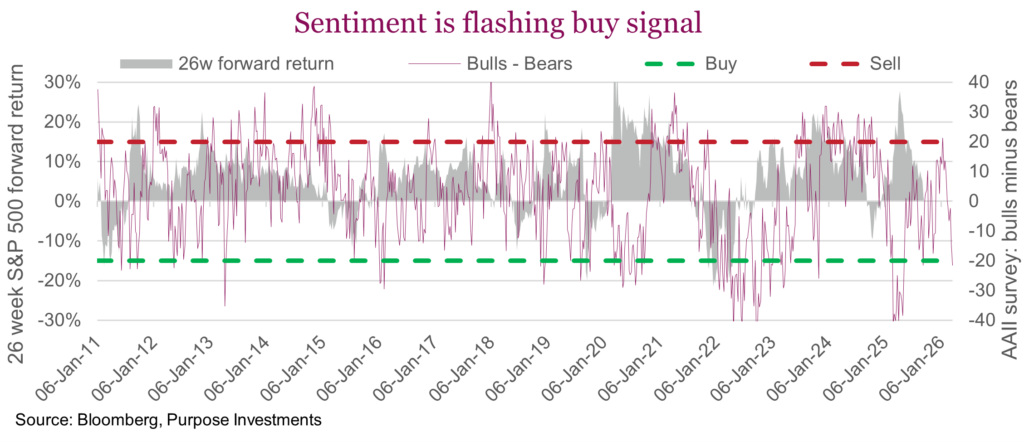

The VIX is up, but not enough. However, RSI for the S&P 500 is down to 32 which is bullish as an oversold signal, hence the yellow-coloured box. Sentiment, as measured by the American Association of Individual Investors survey from this week, has 30% bullish and 52% bearish. A spread of over 20 is a bullish signal.

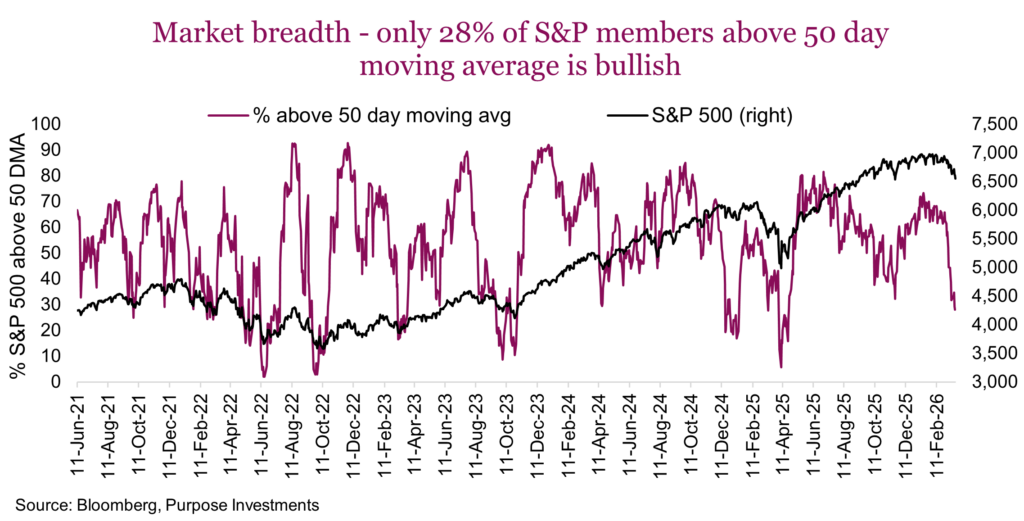

Corporate spreads have certainly risen off very low levels. This isn’t capitulation levels but is on the rise. Bond/equity correlations are positive given the potential inflation impulse from high energy prices. A more entrenched risk-off market would see yields falling so this signal is not encouraging. Market breadth, as measured by the percentage of S&P 500 companies trading in a bull trend, above their 50-day moving average, has fallen to 28%. That is getting close to capitulation levels.

Option indicators are elevated but not capitulation levels. This includes skew, a measure of how much tail insurance is costing investors. And the ratio of puts vs calls. Currency signals are sending mixed signals. Sector divergence with defensives winning is positive as this trend has been in place for a few weeks.

Final thoughts

So here we are with a few correction signals flashing ‘buy’ while most are not quite there yet. The risk of waiting for everything to align can lead to missing opportunities as well. We are keeping a close eye on the situation, and given our more cash heavy and defensive starting point does make it easier to be opportunistic during these times of market stress.