Investor Strategy

February 4, 2025

Can’t we all just get along?

Sign up here to receive the Market Ethos by email.

Executive summary

- As January goes, so goes the year?

- Tariff time, on hold for now

- What happens when the earnings growth slows?

- Market cycle & portfolio positioning

- Final thoughts

2025 is off to a great start but also with added volatility. The only certainty in this noisy headline driven world is that by the time you read this, things may very well have changed. We continue to believe sudden portfolio reactions to this constantly changing environment is not a good strategy but instead monitor and look for potential market overreactions to create portfolio opportunities.

As January goes, so goes the year?

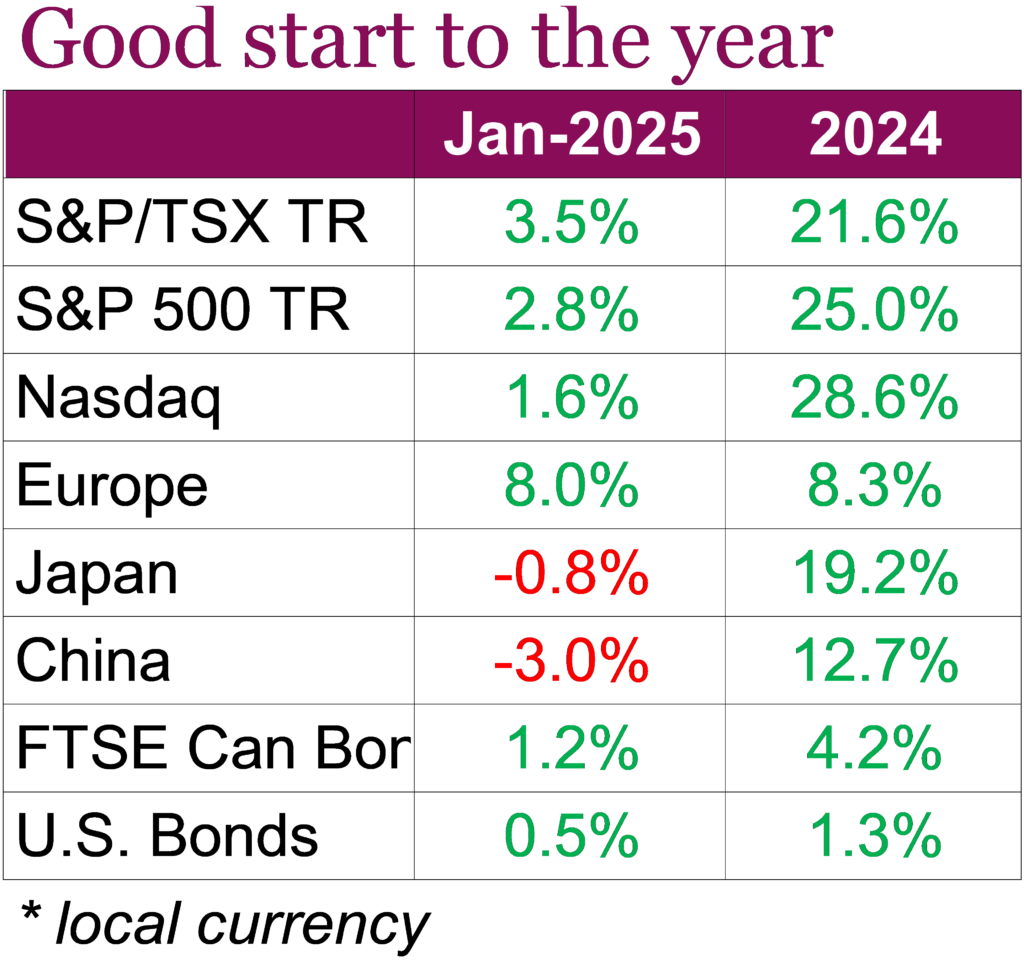

Markets started the year off on a positive note, recovering from December’s selloff. Despite multiple headwinds and increased uncertainty, investors were encouraged by strong corporate earnings, positive economic prints, and the new U.S. administrations pro-growth agenda. Bucking the trend from last year, the TSX led the pack, rising 3.5% on a total return basis over the month, outpacing the S&P 500’s 2.8% return and the Nasdaq’s 1.7% rise. While U.S. markets were initially set to outperform Canadian equities, U.S. equities gave back most of their gains following the announcement of a new Chinese AI chatbot called DeepSeek that rivals U.S. versions at a fraction of the price. Investors were forced to reassess the value they were placing on AI initiatives which created a selloff in some of the mega cap tech names that dominate U.S. indexes.

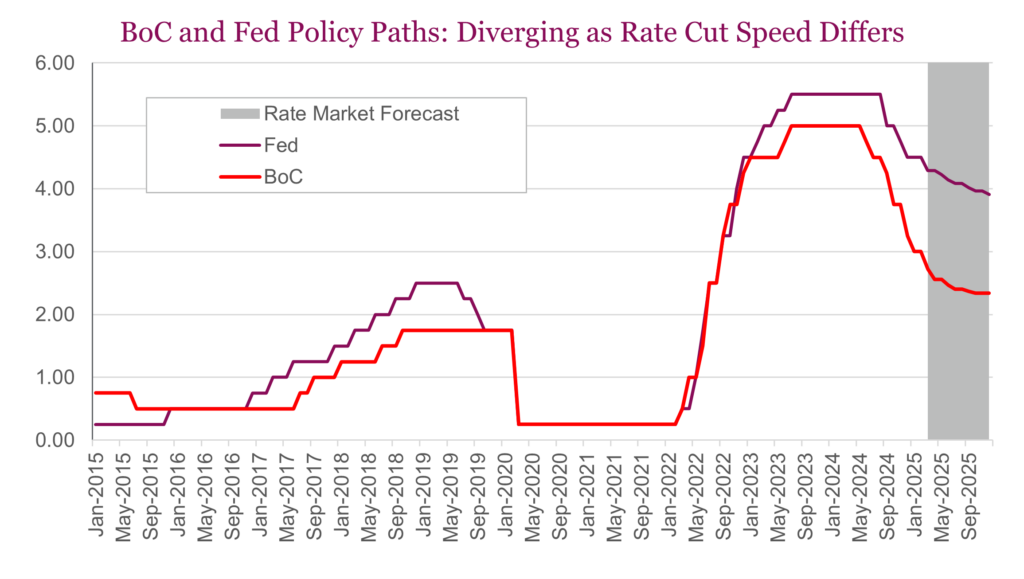

On the economic front, it was a busy month for central banks as they assess inflation outlooks given U.S. trade uncertainties. We saw that Canada’s economy grew by an estimated 0.2% in December, reversing a –0.2% contraction in November, with fourth-quarter GDP expanding at an annualized 1.8% and full-year growth reaching 1.4%. The rebound was driven by gains in retail trade, manufacturing, construction, and real estate, supported by a series of interest-rate cuts from the BoC. Speaking of which, the BoC cut its overnight rate by 25 bps to 3% in January, while dropping guidance of any further adjustments to borrowing costs as the threat of potential tariffs from the U.S intensifies. The European Central Bank also lowered borrowing costs by a quarter-point, bringing their lending rate to 2.75%, citing a stalling economy and confidence that the 2% inflation target will be met. The Fed, however, diverged from other central banks and held interest rates steady at 4.25%-4.50%. The pause comes after a series of rate cuts last year, with officials in no rush to lower interest rates, emphasizing the need for further progress on inflation before making any adjustments. While The BoC and Fed’s policies diverged over the month, both bond markets finished the month up. The U.S. aggregate bond index finished 0.5% higher for the month while the FTSE Canada Universe Bond Index finished 1.2% higher.

While markets seemed to be gaining momentum over the month, sentiment quickly shifted within the last few trading hours of the month after Trump said he was going to follow through on his tariff threats. Trump announced a 25% tariff on imports from Canada and Mexico and a 10% tariff on Chinese goods, set to take effect early February, citing trade deficits, immigration, and fentanyl concerns, with the possibility of further increases. The move threatens to undermine USMCA protections, potentially sparking a trade war, as both Canada and Mexico have pledged retaliation. So let’s start with the topic that’s on everybody’s minds.

Tariff time, on hold for now

The only certainty in this noisy headline driven world is that by the time you read this, things may very well have changed. Heck, by the time you finish reading this note, things may have changed again. Even with last weekend’s announcements, the level of uncertainty remains high. With details on the response, then potential responses to responses, if the last couple of days were any indication, February is going to be bumpy.

President Trump’s second term has certainly started off with a lot of action via executive orders. It would appear the strategy is to get it out there and then deal with legal challenges or other backlash. This is reminiscent of his first term. Many things were said, sometimes those things would just fade away (haven’t heard much about Greenland lately), while others would persist and potentially become policy. But even things that became policy were often softened or adjusted. And some were reversed, with blame being thrown upon a cabinet member who would be let go as the source of the mistake. Only a few cabinet members lasted the full duration of his first term.

We do know President Trump is fond of using tariffs. Is the 25% blanket tariff (with energy at 10%) truly set, or is there a negotiating offramp? Everyone echoes the facts and logic – tariffs raise costs for consumers, including U.S. consumers. And most of Canada’s exports are energy, so tariffs have a quick impact on U.S. inflation. Take out energy, we are net importers from the U.S. and still much of our exports are intermediate goods or inputs into their manufacturing. But, does logic or do facts matter? This is the reason that while we can all agree on the negative impacts of tariffs, it sure sounds like we are about to live an economic experiment.

Estimates of these tariffs have it throttling back Canada’s economic growth by about 2%. Given current estimates of 1.9% growth in 2025, it doesn’t take much math to figure out that is a bad outcome. Potentially recessionary. Countering this would be the fiscal/monetary response. We can expect more rate cuts, that will not be supportive of our already cheap dollar. A drop in the dollar does somewhat shield exporters from the tariffs but also add more inflation to our economic system. Fiscal spending would likely ramp as well, that would also soften the economic blow.

On a positive note (figure we need some positive this week) our consumer does appear to be improving from a good base. Rate cuts have helped, surplus savings over the past few quarters as well and a record wealth level are all supportive. Housing enjoyed a bit of a recovery in 2024 and that does appear poised to continue. Rate cuts again are helping along with pent up demand. However, affordability remains a challenge. 2025 will likely be another year of a slow recovery following the 2022 highs.

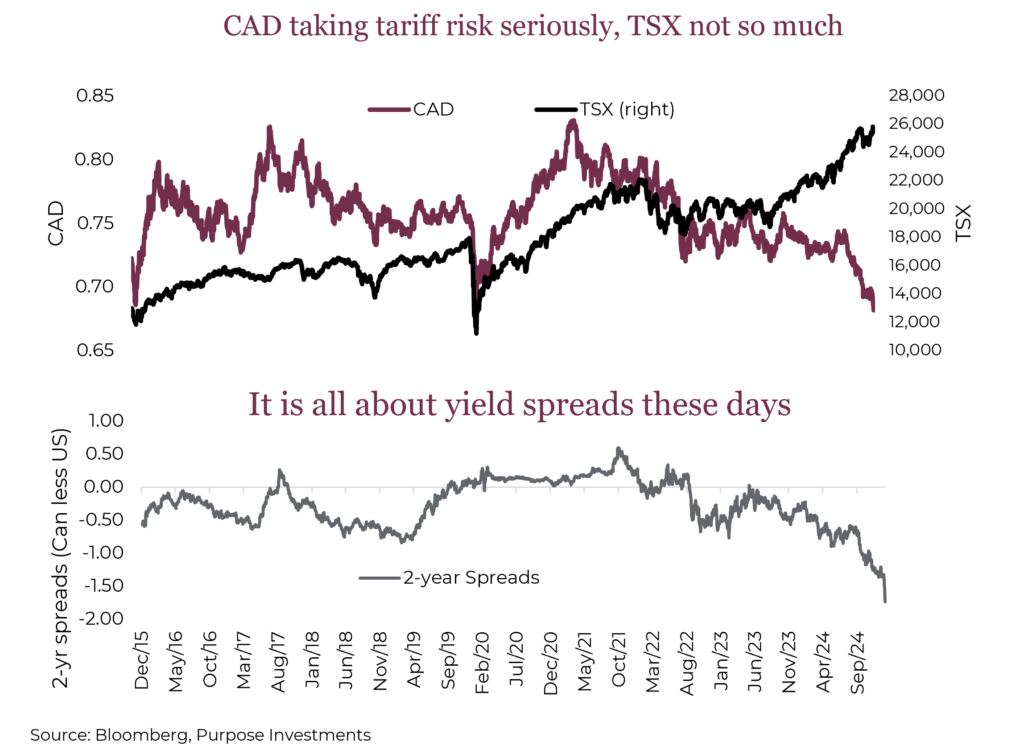

Even with pockets of improvement within the Canadian economy, this tariff war could easily overwhelm. While the impact is more acute for some industries, it also impacts decision making by companies for hiring, investing, etc. across the economy. So why has the currency market taken tariffs seriously, while the equity market is only reacting after the news?

The Canadian dollar was below $0.68, when tariffs were on the table, and the likely policy response of lower rates from the Bank of Canada. And yet the TSX was pretty much at its high last week, rising +24% over the past year and up more than the S&P in January. Is the currency market right or is it the equity market that is not taking tariffs too seriously?

Fact is the currency market is currently dominated by relative short-term interest rates, and given those historic spreads has the CAD trading down at these levels. The TSX is based on the value of its index members. Those company values are based on the value of future earnings. Yes, tariffs will hit those earnings, more for some, less for others, none for some. But for a month, a quarter, a year, two years? If a company is truly valued based on its lifetime projected earnings, perhaps a brief tariff- induced bump to the earnings isn’t a huge deal.

In the above chart we included the relative spread between 2-year yields in the U.S. vs Canada. Usually the Canadian dollar’s moves are dominated by relative 2-year yields and the price of oil. Today, it is 100% yields that matter as the anticipated policy/economic response to tariffs has further divergence between central banks and economies. Today the spread is 1.70. We had to look back to 1998 to find a similar spread.

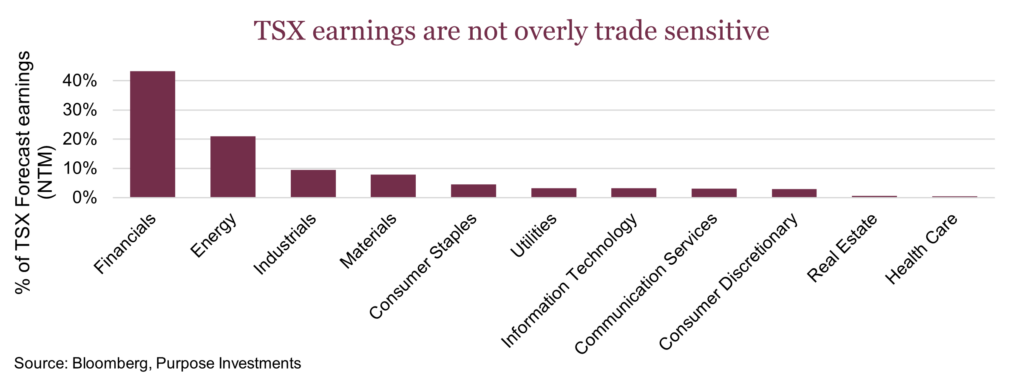

The TSX is finally falling on this tariff war news, as it is a negative. A few things to keep in mind, over 40% of TSX earnings come from financials that are not directly impacted. At least initially, unless the economic hit leads to bankruptcies. One could argue this tariff war is worse for the economy than the TSX. There just are not that many TSX index member companies, outside energy, that have material over the border trade.

Even with the recent announcements the uncertainty remains really high. Will negotiations find a better path before actual implementation or shortly afterwards? Will the policy response help or create a more challenged relationship? Will companies adapt to reduce the impact?

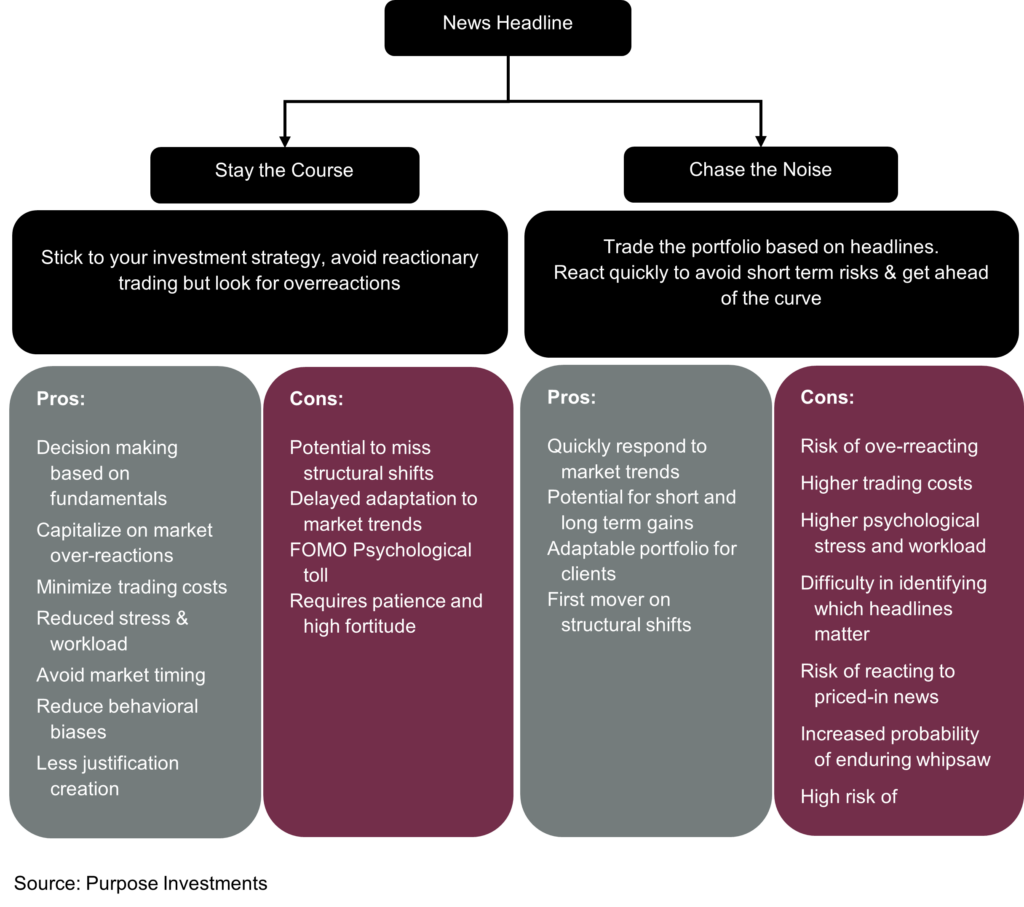

Perhaps of great importance is the impact on portfolios. Our strategy has been more of a steady hand approach. Certainly listen to what is being said/proposed, but remember the end result is often very different than what is said or announced. Or even more simply, should you change your portfolio whenever a headline hits that may or may not have longer term ramifications on asset prices? The following framework may help differentiate the approaches to headline news, and why we are the one on the left.

Listen to what is being said or proposed or implemented and look for a potential market overreaction.

This is the playbook.

What happens when the earnings growth slows?

We have a clear tilt towards more equal-weighted U.S. exposure rather than market cap weighted. Though this tilt underperformed last year, when we regularly reexamine our rationale, the thesis remains sound. Abandoning process to chase performance works out occasionally, however over time process is the only aspect of investing that is repeatable. This isn’t the first time we’ve discussed the preference for equal weight, but it is a good time to revisit it.

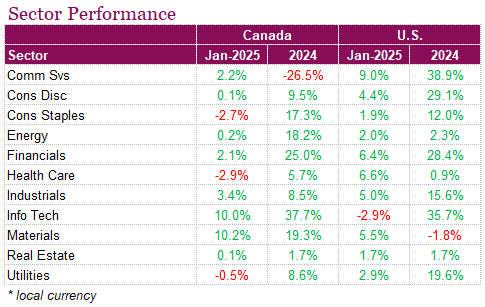

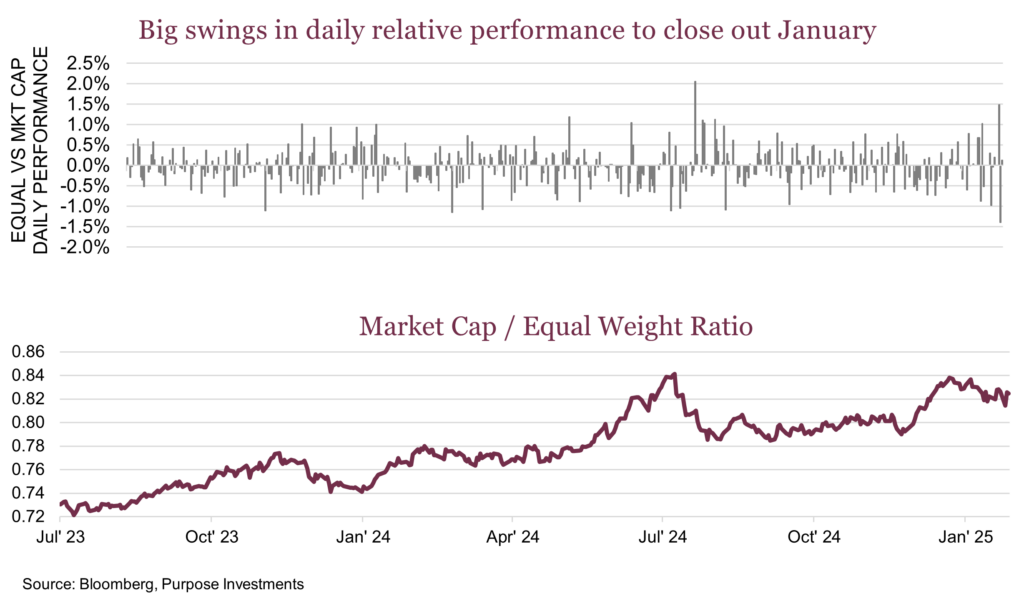

2025 is off to a promising start for the equal weight tilt. January saw a broad rotation within the S&P 500. Some of the top performing sectors were Health Care, Financials and Materials. Technology was only sector that declined, falling -1.1%. Equal weight did quite well rising 4.6% compared to the cap weighted index which rose 4.0%. January 27, or as we now call it ‘Deepseek Day’, was a glorious day for diversification. The big question now is whether this marks a pivotal turning point or just a speed bump for the AI-driven market.

This chart highlights the daily performance gap between the equal-weighted and cap-weighted S&P 500. The Deepseek moment brought about a number of unusual occurrences. We witnessed back-to-back extremes—one of the largest days of equal-weight outperformance in four years, immediately followed by the worst daily underperformance since 2020. We previously warned about heightened volatility in 2025, and this is volatility in action. It’s a seesaw market, but unfortunately, due to concentration risk, this volatility is directly tied to the world’s most-watched index.

Weird breadth happenings

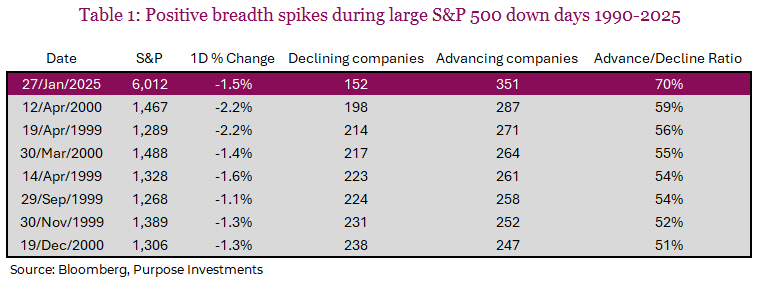

On January 27, the S&P 500 declined by 1.5%, yet 70% of its index members were up on the day. We dug into the data and found that such a divergence is extremely rare. The table below highlights similar occurrences since 1990, and strikingly, the only comparable periods were in 1999 and 2000. The table is not a harbinger of doom, it’s more due to the fact that that period was the last time the market was so concentrated. It does however, clearly express the risks of concentration within the market. The market can materially decline, even though the average stock is doing just fine.

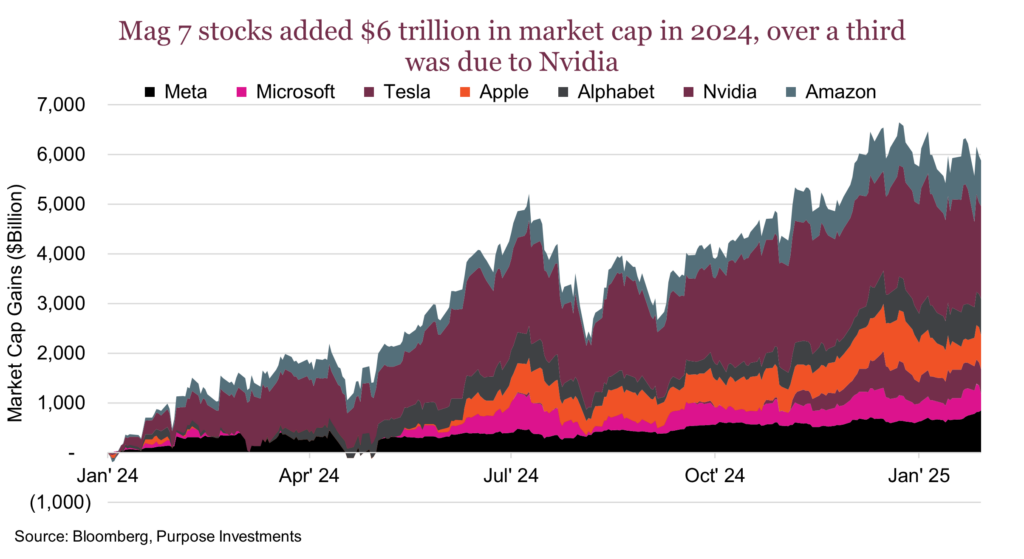

What’s also curious is how quickly the market turned on Nvidia, arguably its biggest champion over the past few years. We’re not going to go to ‘deep’ into the AI melt up, there’s no shortage of reports the past week discussing the details of AI training. What’s clear is that the stakes are high for the Magnificent 7 thanks to DeepSeek. Looking back, collectively the Mag 7 added over $6 trillion to the S&P market cap in 2024. The rest of the U.S. stock market gained $8 trillion. The size and scale of this concentrated advance is very rare. In our opinion, how quickly investors reacted to the DeepSeek news that came from a company out of China that few even knew about is an indication of how fickle sentiment can be when many investors are sitting on sizable gains.

If the disparity between earnings growth narrows, does the valuation gap?

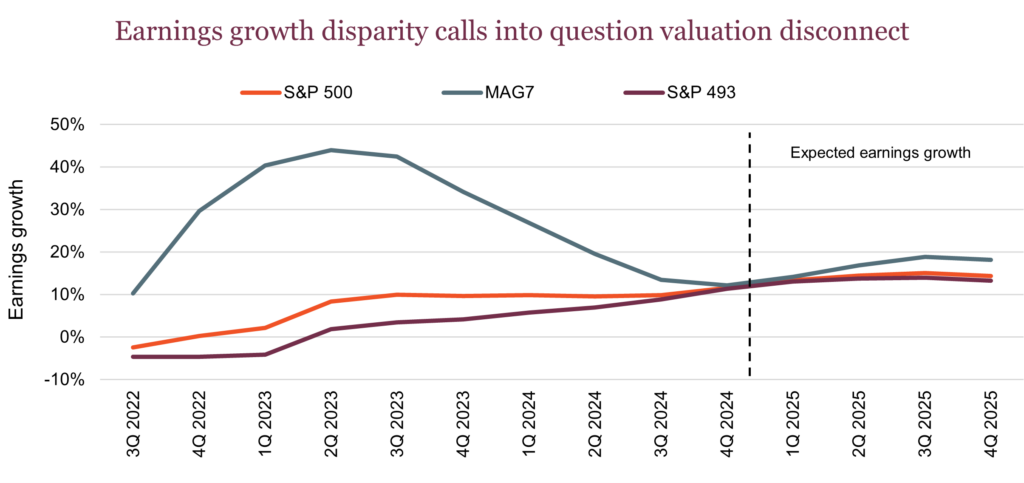

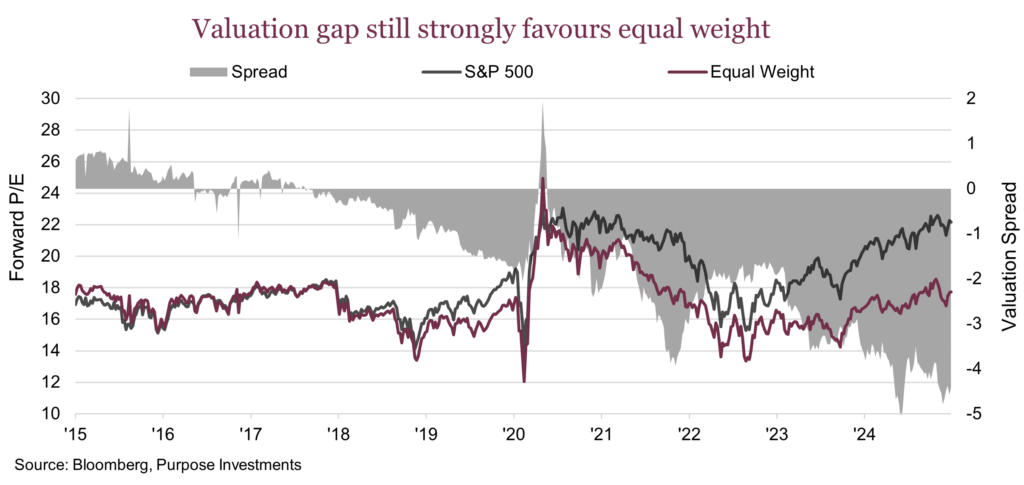

The valuations gap between the S&P 500 and the equal weighted index remains glaringly large. At -4.5 points the S&P 500 cap weighted index is much more expensive. Yes, it is more heavily tilted towards higher growth tech companies but we’re of the belief that valuations matter, especially if growth rates slow. High valuations are justified if growth expectations are high and more importantly accelerating. In the earnings growth chart below, we separate out the Mag 7 versus the rest of the members of the S&P 500. Over the past couple of years, the earnings growth of the Mag 7 was exceptional and helped support those high valuations. But now the earnings growth rate has started declining over the past year and looking ahead, earnings expectations are much more pedestrian and not all that different than the rest of the index. The earnings outlook questions why the valuation disconnect is nearly as large as ever.

The fact that the valuation gap remains this large while the earnings growth rates are converging, shows that it has more to do with excessive optimism rather than a clear and sustainable growth advantage. Sentiment is erratic; this past week is evidence. There should be concern over the valuations of semiconductor companies considering a few of these companies such as Nvidia have been trading at such high multiples. If DeepSeek is proof that leading-edge AI development can happen with less capital expenditure on expensive chips, then this may warrant a rethink of the earnings potential of the manufacturers behind AI. So is this the big AI bubble bursting? Actually no, the DeepSeek moment could actually a big gift to consumer and businesses who don’t have billions to spend on AI. It shows that the cost of implementing a quality AI model doesn’t have to be gargantuan. We read this somewhere, but it seems the most poignant. “This isn’t the end; it’s simply the end of the beginning.”

This divergence in valuations and convergence in earnings underscores why we prefer equal weighting over traditional cap-weighted U.S. exposure. The recent volatility is a glaring reminder of the concentration risks embedded in the S&P 500. When performance is dominated by so few, it amplifies the risk and instability of the market. In contrast, equal-weighted strategies offer a cost-effective way to gain broad participation to the U.S. economy, reduce concentration risk and provide a more balanced exposure. Another benefit is the tilt towards smaller cap companies domestically oriented companies which could benefit from the U.S.-centric policies coming from the current administration. The year has so far been good for equal weight and one final point to keep in mind is the famous saying, “As January goes, so goes the year.”

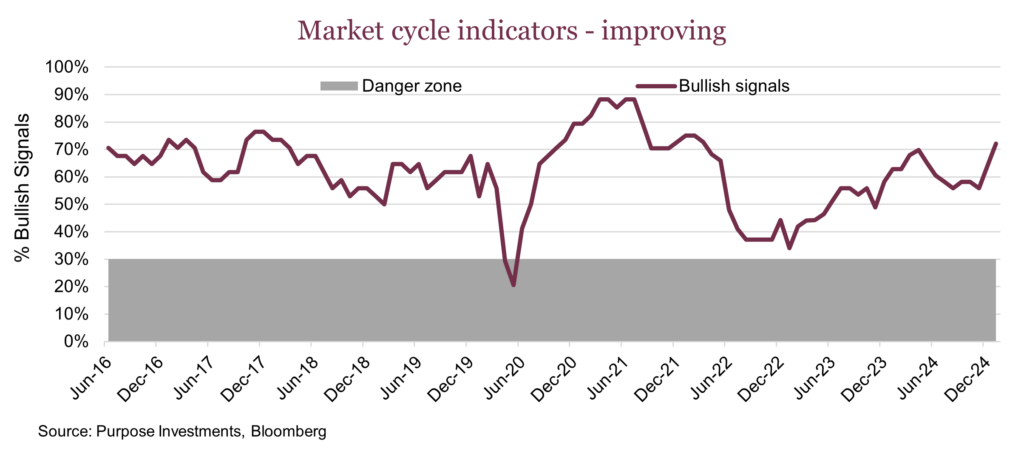

Market cycle & portfolio positioning

With all the uncertainty around potential policy changes (aka tariffs) we must acknowledge that the economy continues to show signs of improvement. So far in 2025 we have seen an uptick in data and signals, pretty much everywhere. The probability of a recession for the U.S. over the next year, based on consensus from economists, has dropped to 20%. The lowest or best reading since early 2022. Bit higher elsewhere including with Canada, UK and Japan all around 30%. Overall, pretty low risk …ending a policy mistake which is a possibility.

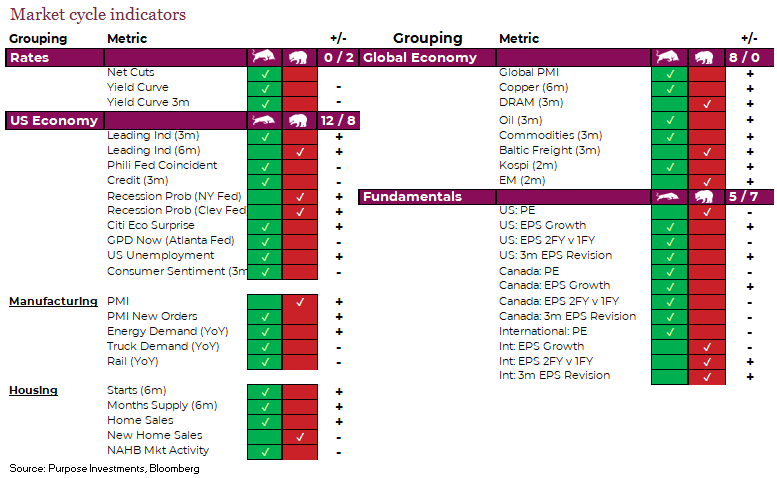

The U.S. economic indicators are responsible for much of the upward move in the Market Cycle indicators, but it is also a global story. The CitiGroup economic surprise indices are positive across all six of our major buckets including US, Canada, Eurozone, China, Japan and Emerging Markets.

It is this strong global economic backdrop that appears to be making equity market resilient even with a higher degree of policy uncertainty. Of course this could change and we would highlight the concentration in the U.S. remains a risk, highlighted by the DeepSeek hiccup, but it would take a lot to push the global economy into a recession.

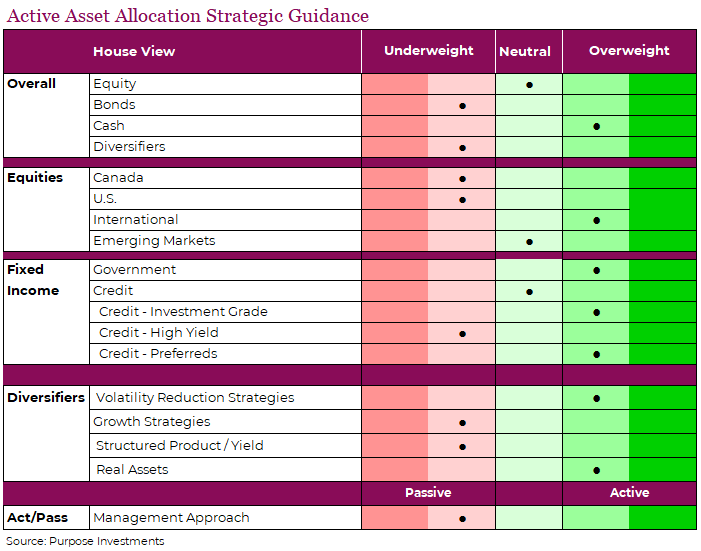

At the overall portfolio level no big moves so far. We remain equal weight in equities, with our bullishness based on the Market Cycle indicators tempered due to policy risk and concentration. This has us with a mild underweight in Canada and the U.S. with a mild overweight internationally. If we do experience a market reaction, and if deemed an overreaction, we would be opportunistic and have extra cash to put to work.

Asset Allocation Guidance

We do believe bond allocations should be a bit more tactical than in years past. Diversifiers have done well. While the need for volatility management hasn’t surfaced yet, the risk of a market pullback appears elevated. And the real asset (aka gold) has been doing very well.

We remain in the camp of waiting for any market overreaction to act. That is our playbook for an environment with so many moving parts and attention grabbing headlines.

Final thoughts

2025 is off to a great start but also with added volatility. Not too surprising given concentration in parts of the market and such a noisy policy environment. February is often a bumpier month, thankfully it is a shorter one too. We continue to believe sudden portfolio reactions to this constantly changing environment is not a good strategy, but instead monitor and look for potential market overreacts to create portfolio opportunities.