Investor Strategy

3 November 2025

Everyone loves balloons until they pop

Sign up here to receive the Investor Strategy by email.

- October was not spooky

- Market mood still happy

- Sea of balloons

- Mr. Market has become Mr. Gullible

- Market cycle & portfolio positioning

- Final note

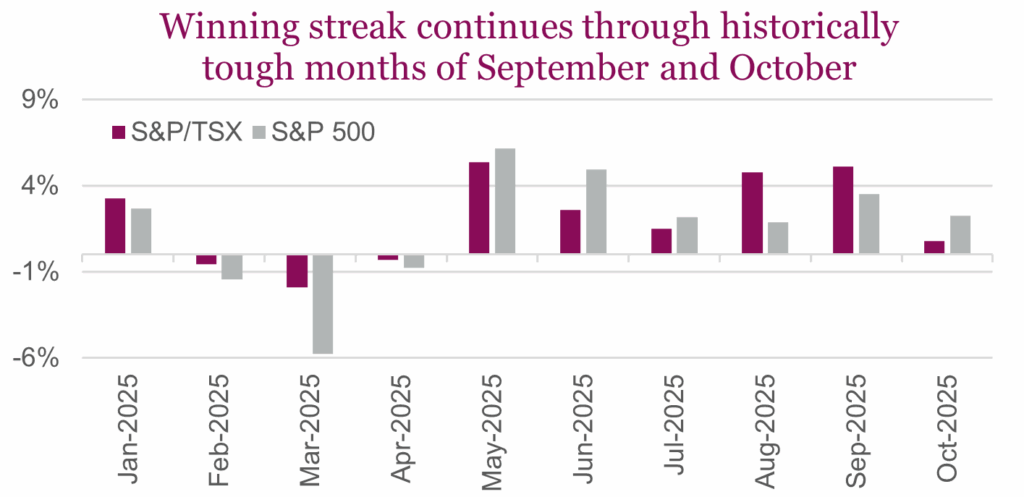

October was not spooky

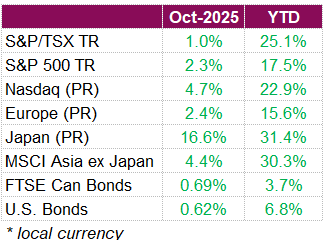

Markets extended their winning streak in October, with equities rising across regions despite ongoing political and economic uncertainty. The S&P 500 gained 2.3% on a total return basis, supported by optimism around AI, solid corporate earnings, and signs of easing U.S.–China trade tensions. By month end, roughly 80% of S&P 500 companies who released earnings, reported third-quarter results above expectations, underscoring the resilience of corporate profitability even in a slower economic environment. The Nasdaq rallied 4.7%, driven by strength in technology and AI-related names, while the S&P/TSX advanced 1.0%, extending its positive run despite a pullback in the Materials sector following an extended rally. Gold’s rally briefly lifted it to a record above $4,380 an ounce before retracing later in the month. The metal still ended October up 4.1% and remains nearly 50% higher year-to-date, helped by central-bank buying and investor interest in inflation hedges and currency diversification trades.

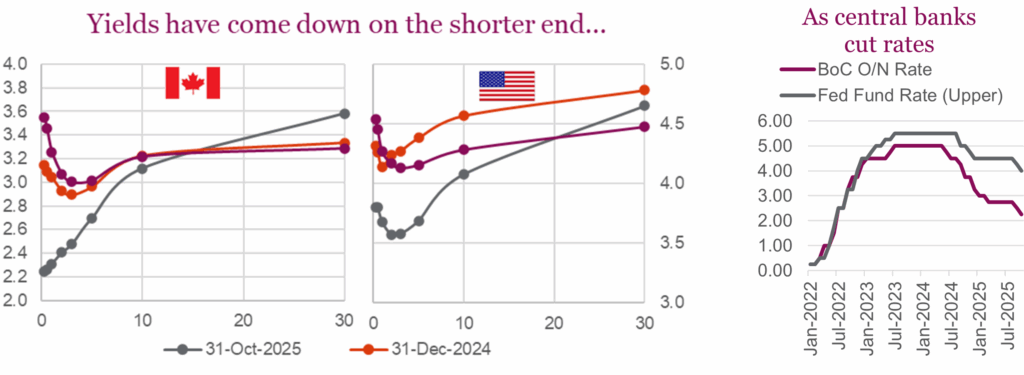

In Canada, economic data remained subdued as GDP contracted by 0.3% month-over-month and grew only 0.7% year-over-year, highlighting the drag from tariffs, weaker exports, and softer business investment. Trade negotiations between the U.S. and Canada remain stalled, with little progress on steel and aluminum tariffs. With concerns over slowing growth and the labour market, the Bank of Canada (BoC) cut its policy rate by 25 basis points to 2.25%, while signaling the potential end of its easing cycle. Policymakers struck a cautious tone, suggesting rates are now close to levels that can guide inflation back toward target, though they left the door open for further moves should growth slow more sharply. With yields lowering over the month, the Canadian bond market posted a modest gain of 0.69%, slightly outpacing the 0.62% return from U.S. Aggregate Bonds, as investors continued to price in a lower-rate environment even as central banks globally showed a more measured approach to additional cuts.

In the U.S., markets brushed off much of the negative news to close the month near record highs. The Fed cut rates by 25 basis points to a target range of 3.75–4.0% on the same day as the BoC, its second cut this year, but cautioned that investors should not assume another reduction in December. Despite this more hawkish tone, investors remain confident that rates are trending lower over the medium term, particularly as the government shutdown (now approaching the longest on record) delays key economic data and weighs on near-term sentiment. Meanwhile, an encouraging meeting between Presidents Trump and China’s Xi helped ease trade tensions, helping support risk assets. Overall, October reflected a cautiously optimistic market environment, which saw investors continue to balance near-term volatility against the tailwind of resilient corporate earnings, easing trade tensions, and AI euphoria. Looking ahead, November has historically been the S&P 500’s strongest month, with an average gain of 1.8%. Still, markets remain sensitive to developments on trade, geopolitical negotiations, and monetary policy direction.

Market mood still happy

2025 – the year that started off poorly but is well on its way to finishing strong. Having successfully crossed the historically volatility September/October chasm, will it be smooth sailing till year end? The headline news continues to rattle markets and occasionally soothe concerns. However, it is a broader firming of the global economy that is making this market advance less sensitive to headlines. The data has improved globally, with the caveat that much U.S. data is unavailable due to the 30+ day government shutdown. Meanwhile, inflation has not accelerated — it has cooled a bit, enabling bond yields to move lower. Lower bond yields equal multiple expansion. Then sprinkle on some AI- related excitement as the cherry on top.

Global equities were up a little over 2% in October, with the U.S. roughly inline and the TSX lagging a bit having given back some of those gold gains. Europe was a bit stronger, and Japan hit a home run, Ohtani-style. Markets have moved higher on the valuation spectrum but most are struggling with what to do now. Nobody wants to leave the party, but everyone is concerned about how long (and far) it has gone.

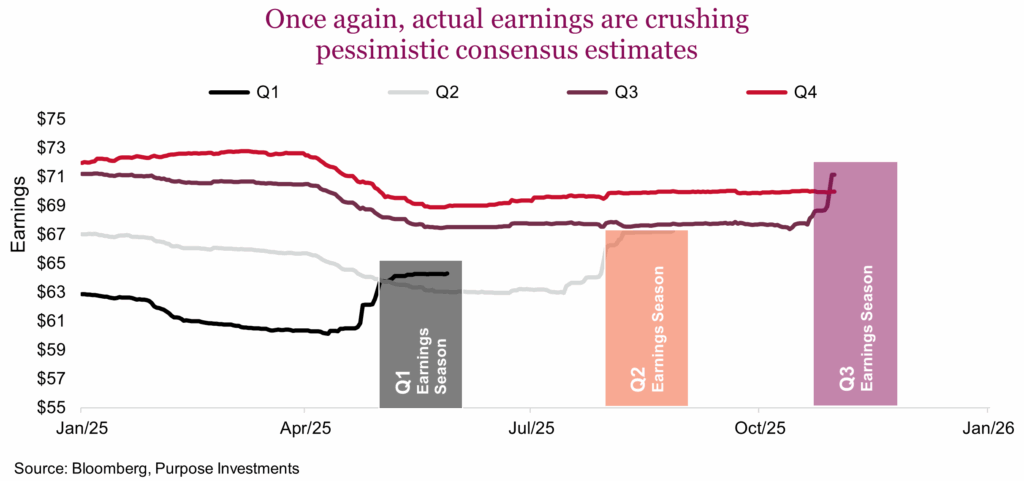

On a positive note, earnings season is ticking along nicely. For the S&P 500, over half of constituents have reported, and the pattern is similar to the last few quarters. After estimates were revised lower due to tariffs and uncertainty earlier in the year, actual results have been largely immune. This has quarterly results seeing a jump higher above estimates during the respective earnings season.

The general view was that tariffs and uncertainty would result in margin pressures for U.S. companies given reduced ability to pass on higher prices to a somewhat softened consumer. CPI has remained muted, so clearly not passing on higher costs. Yet margins remain strong. So, what gives? A weaker U.S. dollar and the robust capex-related spending on AI are solid positives for earnings and margins. But even at the sector level, margins remain solid. More likely companies are very good at pulling levers to sidestep tariffs, had previously stockpiled inventories or are making other changes to maintain margins. Likely as companies run out of levers to pull the impact will start to bleed into earnings and margins. But it may be gradual and probably less noticeable to a market hooked on headlines.

On another positive note, estimates for earnings in 2026 are on the rise. Over the past three months, 2026 global earnings estimates have moved higher by about 2%. Analysts are becoming more optimistic into 2026 from an earnings perspective. Clearly after being too pessimistic in 2025, analysts are more constructive for next year.

Hard to say what could upset the mood of this happy market. Inflation stirring, an AI wobble or maybe a good old fashioned economic growth slowdown. Or a total surprise. In the meantime, the party appears to keep going.

Sea of balloons

The term ‘bubble’ has become an overused and imprecise descriptor for today’s market. A more nuanced analogy for the current landscape of speculative investment is a ‘sea of balloons’. New technologies and business opportunities attract immense capital, creating speculative investment clusters, or balloons that inflate and deflate with capital flows. While the long-term trajectory of new technologies like the internet or AI is real, the rapid ascent and clustering of capital suggest a degree of exuberance. Now that the analogy is set, hopefully the AI-generated image shown here can help with the visualization. The challenge for investors is not just to ride the balloons that float highest but to disembark before they either pop in a crash or slowly lose altitude and fizzle out.

Thematic investing is a way to invest directly in each of these balloons. It is increasingly popular for individual portfolios, made significantly more accessible by the proliferation of ETFs. With over 275 thematic ETFs in North America representing $127 billion in assets, the options are plentiful, and issuers are highly motivated to productize every new idea. The size of some of these funds can be large enough to allow them to play a significant role in underlying stock performance — an effect that is exacerbated in emerging thematics where new funds often invest in companies that lack high trading liquidity.

Quantum computing offers a great case study on the impact of flows. This space is filled with former small-cap stocks that nobody had heard of that have recently become large-cap names, with performance certainly influenced by capital flows. While public investment provides a structural floor, the theme itself remains binary: it could either see sudden breakthroughs or a long, slow fizzle if commercialization fails to materialize.

Emerging clusters and new themes

The creation of new thematic ETFs continues to accelerate, with more launches this year than in 2024. This trend highlights a persistent investor appetite for novel growth stories. Among the most compelling new themes of 2025 is direct exposure to U.S. electrification. This includes everything from utilities to electrical component suppliers, a space where demand is outstripping supply and has rewarded investors with strong performance. Beyond broad AI exposure, new funds are also targeting niche areas like the AI data center buildout, humanoid robotics, and next-generation semiconductors. Other notable themes gaining traction include critical minerals and rare earths, which are essential for technology and defense, alongside health and wellness trends focused on longevity.

Performance leaders and laggards

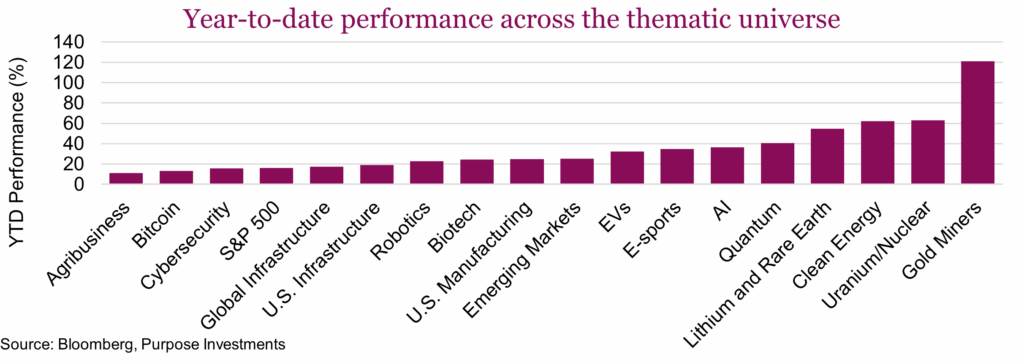

This year has seen a significant shift in thematic ETF performance. While dispersion remains wide, few themes are posting negative returns compared to last year. Surprisingly, despite the hype around big tech, cloud computing ETFs have been notable underperformers. The chart below focused on our curated list of prominent ETFs across a variety of thematics. The top-performing themes year-to-date paint a picture of a market driven by both new technologies and geopolitical forces. Gold miners stand out with their strong outperformance followed by nuclear and clean energy. AI, quantum and Rare Earths area also all delivering strong returns. Laggards include Agribusiness and Bitcoin, though both are still positive. Overall, the performance data shows broad positive performance across all major thematics.

Follow the capital

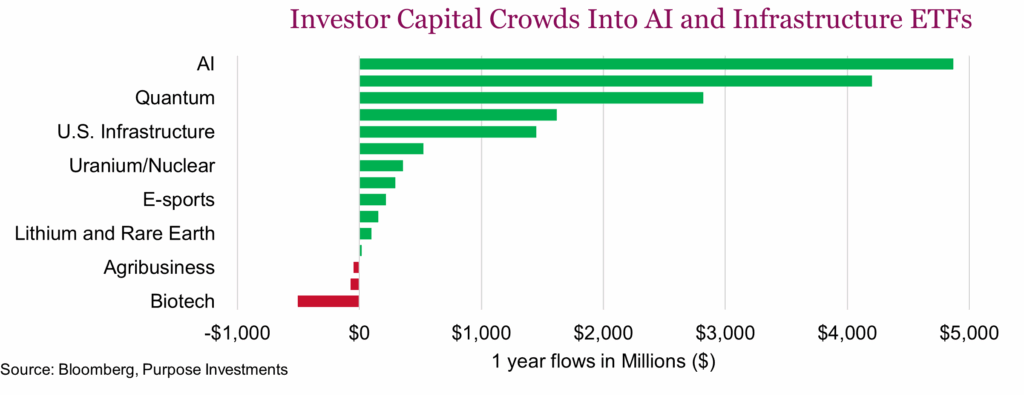

While performance charts show what has worked, capital flows reveal where investors have an increasing appetite for exposure. This year, the two are not always aligned, creating potential opportunities and risks. ETF fund flows act like the hot air heating the balloons, indicating where conviction and capital are chasing. This year, the themes attracting the most capital have been AI and global infrastructure. Each has added significant AUM as well as strong performance. Quantum computing is punching well above its weight, attracting more capital than many gold mining ETFs. Most other themes are showing moderate growth while a few like Biotech and EVs have actually seen net outflows. When viewed as a percentage of assets under management, the most popular new themes have been U.S. electrification, humanoid robots, and global defense. Collectively, the entire thematic universe has attracted over $25 billion in net flows this year, pretty impressive for what used to be regarded as niche investing.

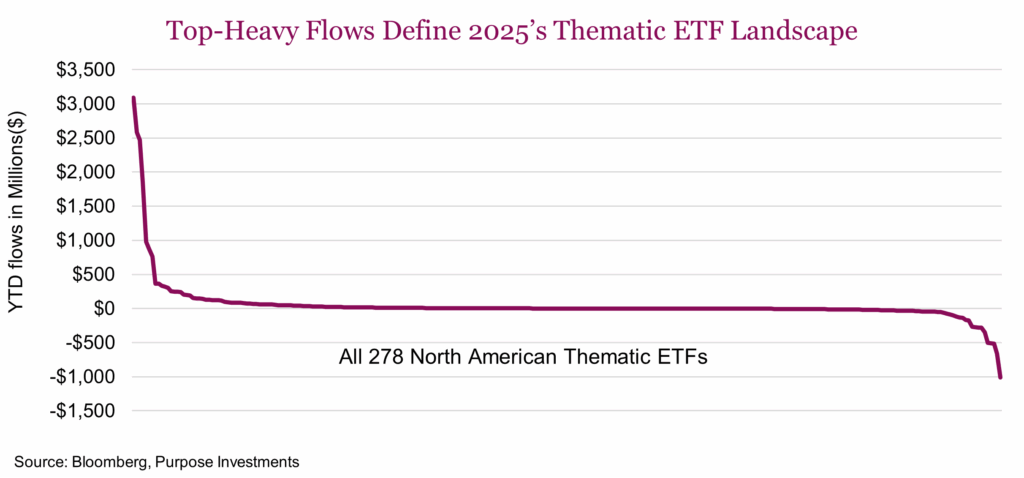

The chart below shows year-to-date fund flows for the entirety of the North American Thematic universe sorted from highest to lowest. What’s interesting about this chart is that it clearly shows how a very small number of ETFs have seen very large inflows (>$1 billion). The flow landscape is quite top-heavy. The majority of thematic ETFs cluster near zero, reflecting little investor interest and another small group of ETFs showing significant outflows, with some of the weakest losing nearly a billion dollars so far this year. Worth noting to be a ‘big loser’ from a fund flow perspective, you have to have previously been a big winner. Most balloons inflate and deflate over time. Overall, the thematic space is one with a few big winners with the bulk seeing limited demand.

Be systematic to stay aloft

The fizzling of former high-flyers like EV and disruptive tech ETFs underscores a critical point: thematic investing without a disciplined framework is merely trend-chasing. This is where a robust systematic approach becomes indispensable.

The current market is highly concentrated. Themes like AI, robotics, and self-driving cars exhibit extremely high correlations (up to 0.92), meaning that holding multiple, seemingly distinct themes can expose an investor to a single, concentrated risk or one giant balloon. True diversification in this environment means ensuring your portfolio consists of multiple, non-correlated balloons. Holding five different AI-related ETFs isn’t diversification; it’s building one giant, highly correlated balloon. A more robust approach combines AI with non-correlated themes like defense or critical minerals.

To avoid simply trend chasing, employing a systematic relative strength and momentum framework allows investors to objectively identify themes that are gaining traction while systematically reducing exposure to those that are losing altitude. Momentum can help identify which balloons are ascending, such as those with rising flows into rare earths and uranium, and which are fizzling.

Thematic investing can make a lot of money, but it can be risky without a strong sell discipline. For investors, the challenge heading into 2026 is not whether to participate in these investment themes, but how to do so with an approach that can withstand both the rapid pops and the slow leaks.

Mr. Market has become Mr. Gullible

The Mr. Market concept, introduced by Benjamin Graham, is a construct to explain how the market can love something one day and hate it another, often behaving in a manic fashion that appears based on mood swings. Given market returns of late, the mood of Mr. Market is obviously one of more exuberance. However, we do believe there could be something else afoot, this market appears to have become rather gullible. Bear with us here.

In years past, the market seemed to have a more discerning view regarding announcements, it was more of a ‘show me’ don’t just tell me. In the old days (not that long ago), when a company announced plans to buy another company, the target would often receive a price pop while the acquirer’s price would fall. This was the norm. The reason being, those synergies that are often used to justify the acquisition and claim it will not be dilutive, often fell short. Today, it seems both target and acquirer see a price pop on acquisition news.

Let’s talk Cameco (CCO), which rose +25% on October 28 after the U.S. signed a $80 billion pact for nuclear reactors to be built by Westinghouse Electric (49% owned by CCO). Don’t worry that the last large-scale nuclear reactor built in the U.S. started in 2009 and was finished in 2023, costing over $30 billion vs its original budget of $14 billion. Or how profitable this will be given the U.S. government is sharing in said profits. Or if small modular reactors (SMRs) become more economical in a few years, will that change the plans? The market appears willing to take the news at face valley and is perhaps overlooking any risks.

Companies appear to have figured out that markets are reacting very quickly and positively to announcements. Over the past week (Oct 22-29), Nvidia has made five announcements: $1B equity investment with Nokia, All-American AI-RAN stack for 6G, a collaboration with the U.S. Department of Energy and Oracle, a ‘Broader U.S. AI infrastructure push with national labs, and a manufacturing and robotics initiative. That was enough to help lift a $4.5 trillion dollar company above $5 trillion.

Or President Trump — the market seems to react to just about anything he says on Truth Social, even knowing that many announcements often fade away or are changed afterwards. A 100% tariff on China, now a deal. Likely a new Canada retaliatory tariff if the Jays had won. Too many examples here to list but the crux is the market is reacting.

We do believe the market has become more headline-reactionary and seems to take everything at face value. The ‘WHY’ this has happened is a guessing game. Just about anyone can create a news momentum trading strategy these days, AI has made coding much easier. Or perhaps our society has lost all patience and has become very ‘NOW’ minded. Or maybe just more fast money chasing things.

Not sure there are any huge implications for navigating a potentially more gullible market. Not reacting or not overreacting to headlines is still a good strategy. Or focusing more on actual earnings and results, less on what is being said. That will make you a contrarian in this increasingly headline-driven gullible market.

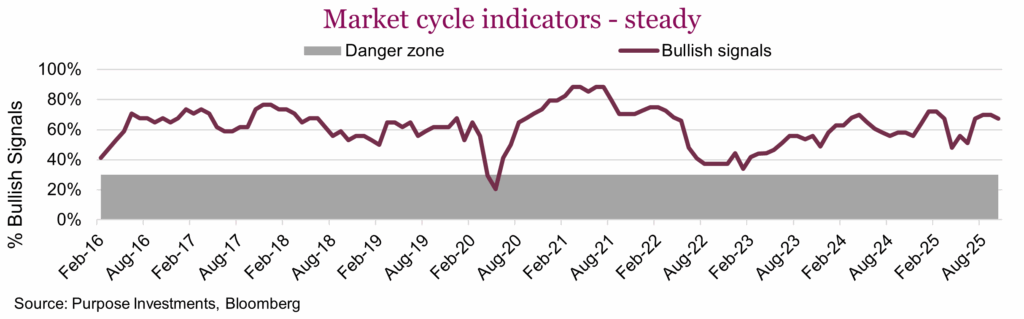

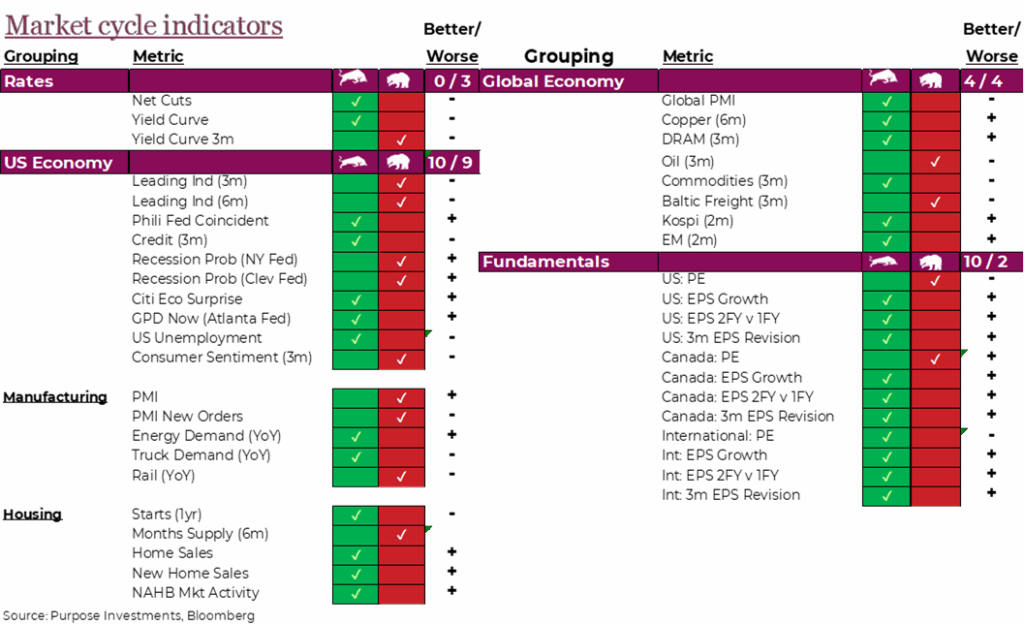

Market cycle & portfolio positioning

We have to begin this month’s Market Cycle update with a little caveat. Given the ongoing government shutdown in the U.S., which is now 30 days plus, some data updates are a bit stale. Only a handful of U.S. indicators are impacted but it’s worth noting the markets are flying with less visibility of the underlying economic temperature. If it goes on much longer, into next month’s update, we will remove the stale data for the time being. The good news is most data points are still timely and holding up in decent fashion.

On the good news side, we have seen a slight improvement in U.S. data, that is available. Energy demand improved, a sign the economy remains resilient. GDPNOW from the Atlanta Fed has improved (not one of our signals but noteworthy), and the Citigroup Economic surprise index remains positive. The better news comes from fundamentals. Earnings season is ticking along, and future estimates are improving. Global indicators also remain more bullish than bearish.

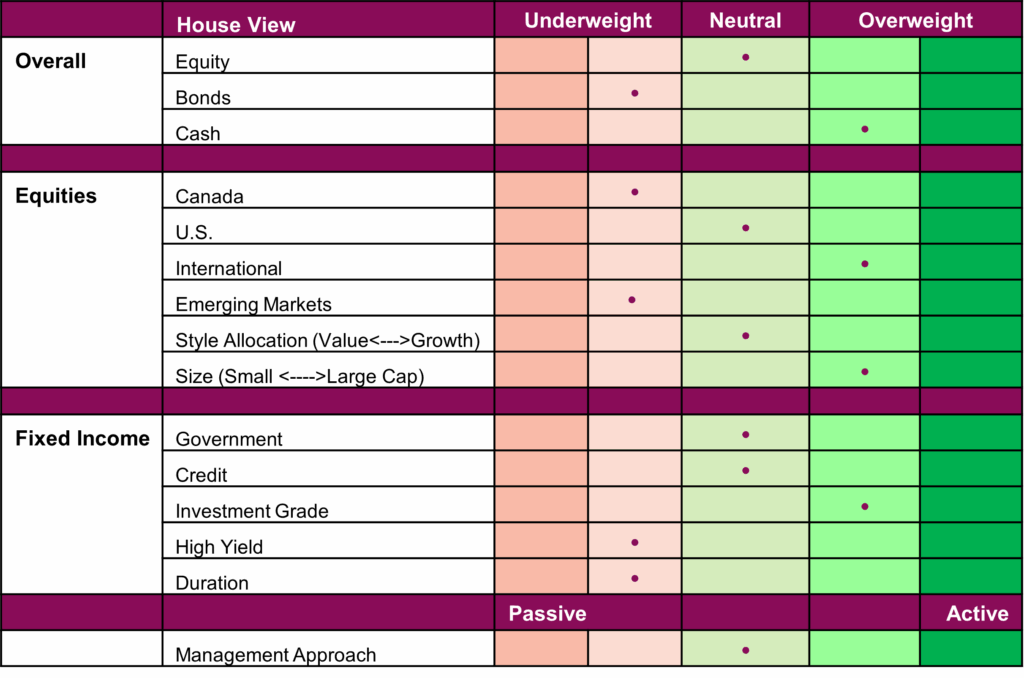

No change in positioning during the past month. Among equities, now underweight Canada after taking profits given strong gains and valuations looking stretched. U.S. equity remains market weight and we are still overweight international. Overall, we believe we have enough market exposure should this happy market continue but enough defense and optionality in case weakness materializes.

Portfolio Positioning

Final note

Hard to say what might upset this market but for now we believe the ideal path is reasonable offense. It doesn’t feel like the time to be adding, and harvesting some gains on such a strong year may prove prudent. Don’t leave the party yet, but try standing closer to the door.