Investor Strategy

July 8, 2025

Halfway check-in: Comfortably numb?

Sign up here to receive the Market Ethos by email.

- Nice finish to first half

- False crises

- Economic growth scare in second half?

- Equity position check-in

- Market cycle & portfolio positioning

- Final note

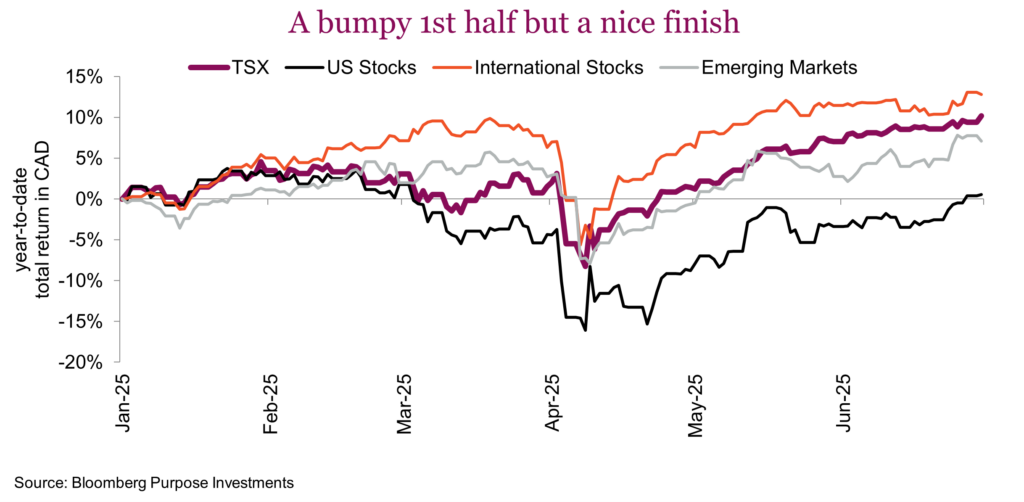

Nice finish to first half

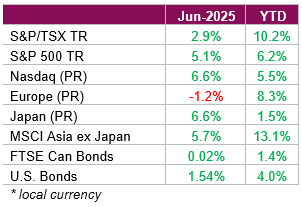

Equity markets continued to march higher in June, with major indices reaching record highs. The moves higher were even more impressive when you consider the rising geopolitical tensions in the Middle East and ongoing trade tensions that investors were left to contend with during the month. While these types of events would normally be enough for investors to take a step back, tensions quickly eased, restoring risk appetite. In Canada, the TSX rose 2.9% on a total return basis, supported by higher oil prices and strong commodity demand. U.S. markets outperformed, with the S&P 500 TR and Nasdaq (PR) gaining 5.1% and 6.6%, respectively, lifted by strength in tech stocks and rising expectations of potential Fed rate cuts as early as September. Asian equities also saw solid gains, with Japan’s Nikkei up 6.6% and MSCI Asia ex-Japan rising 5.7% on the back of easing trade tensions. Meanwhile, European markets lagged, with the Euro Stoxx 50 down -1.2% in local terms.

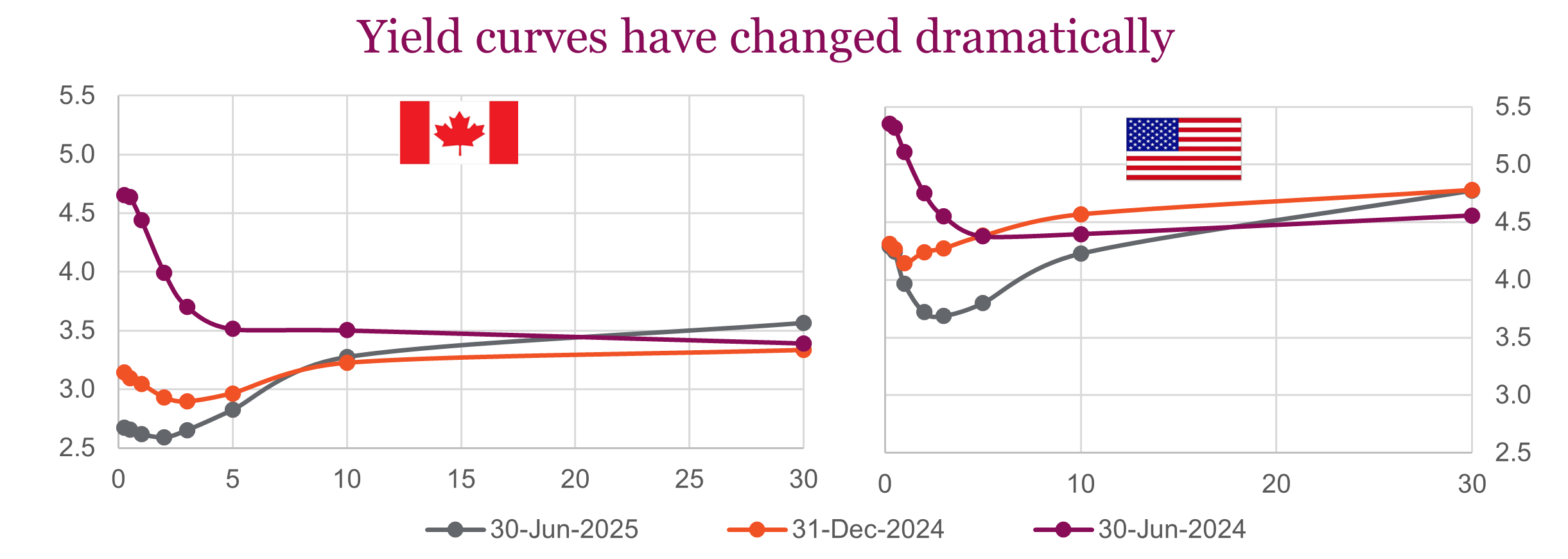

In fixed income, Canadian aggregate bonds were flat in June, while U.S. bonds rose 1.5% as Fed Chair Jerome Powell reaffirmed a data-dependent stance, with markets now pricing in two cuts for 2025. Treasury yields continued to move lower during the month with markets increasing their Fed rate cut expectations through the remainder of the year. The monetary policy-sensitive 2-year Treasury yield declined nearly 20 bps over the month, causing the slope of the Treasury curve to steepen as concerns about the federal budget deficit kept pressure on long-term Treasury prices. This came as Trump’s “One Big Beautiful Bill” made it past the finish line, with the House passing a sweeping $3.4 trillion in tax cuts and spending package. The bill slashes taxes by $4.5 trillion and is expected to increase the federal deficit but eliminates the risk of a near-term debt default by raising the debt ceiling.

The U.S. dollar continued to weaken over the month, including against the Canadian dollar, as improved global risk sentiment and narrowing rate differentials weighed on the currency. Commodities were volatile, with oil briefly nearing $80 per barrel before retreating on rising ceasefire hopes. Overall, June reflected a risk-on environment supported by softening inflation, a more dovish Fed tone, and reduced geopolitical stress. Equities led performance across regions, capping a strong first half of the year. However, signs of underlying economic fragility are emerging. Let’s dig a little deeper into the first half of the year, and see what’s in store for the remainder of 2025.

False crises

Markets have performed well during the first half of 2025 but this strength certainly masks a lot of volatility and uncertainty. The main recurring theme appears to be false crises. Whether it is trade, escalating war in the Middle East, terrible sentiment economic data, a spike in credit spreads or deficit concerns over government bond issuance, all have rattled markets only to see the risks fade. We are not saying these risks are actually gone but the market has consistently reacted then recovered, for now placing them all in the ‘false crises’ category.

The trade war isn’t over, there isn’t peace in the Middle East, economic data isn’t good and deficits are still a problem, but the market says it doesn’t care. Or at least it doesn’t care at the moment. While 2025 has been a macro-driven year so far, with headlines driving most of the market moves in both directions, taking a more calm or non-reactionary approach to headline announcements has proven ideal for investors’ portfolios.

U.S. policy has certainly dominated headlines — primarily from tariffs, but also DOGE, tax policy and changes to regulation. If this were any other year, policies outside the U.S. would have garnered more attention. Germany relaxing deficit rules, China apply increased fiscal spending with some early signs the real estate crisis may be finally abating and even Canada’s move towards a more business friendly policy (Yay!). Add in central banks remaining in cutting mode, and the takeaway for markets is that while the policy uncertainty is a negative, many policies have been supportive of markets.

Perhaps more impactful is that the market is becoming more numb, or accustomed, to this level of policy uncertainty. Market reactions to even bad news on tariffs has become muted, as can be seen with the recent flare up for Canada/U.S. or Japan trade talks. Dare we say markets are becoming used to Trump’s steady flow of announcements, or at least not taking them at face value? Once again this reinforces our strategy of not reacting to the headlines. Instead we calmly wait and if the market does potentially overreact, we then take opportunistic action.

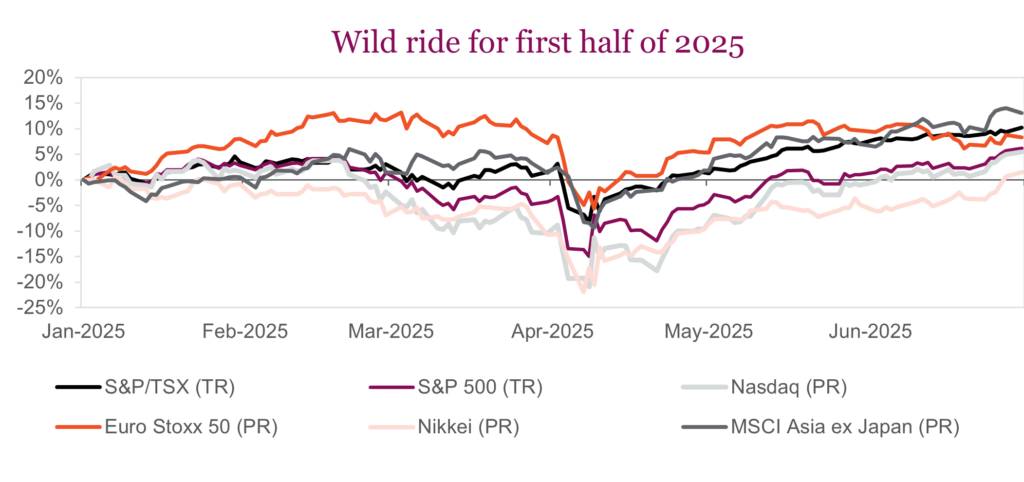

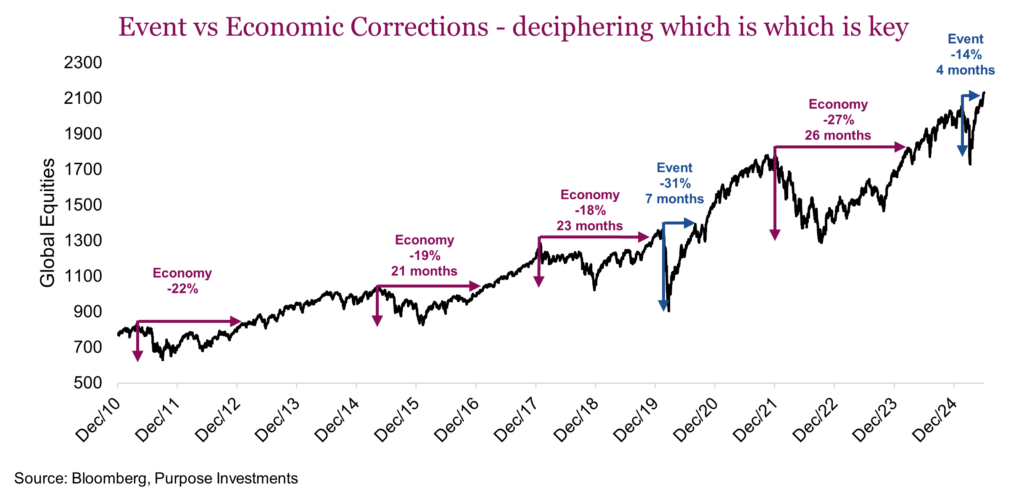

Markets have enjoyed a good start to 2025, albeit with one helluva ride. From initially underreacting to the policy threat of tariffs, then overreacting and now perhaps underreacting to what lies ahead. The important lesson for portfolio construction is trying to differentiate between event shocks and economic gyrations. The rule of thumb is that a shock, which can create market weakness, is an opportunity and you may have to be fast. On the other hand, economic weakness is something that doesn’t resolve itself nearly as quickly and may take quarters or years to resolve.

The past 15 years have been a great period for investors, as one can easily see with markets at all-time highs. This has also reinforced the ‘buy the dip’ mentality. But digging deeper into market corrections during this bull market uncovers a very useful distinction. Corrections caused by an event have proven very short term in duration before markets recover and march higher. Covid in 2020 was the big one, the trade policy event in 2025 was similar albeit not as extreme. Even the carry trade blow up in the summer of 2023 provides a third example. Down fast, and then up fast.

Other corrections that coincide with periods of economic weakness take a very different path. More gradual on the way down and on the way up, causing these corrections to last much longer. In 2011, markets fretted over a double dip recession in Europe while the U.S. & Asian economies were only mildly positive. 2015 and 2018 were both global economic growth scares led by China. And in 2022, while perhaps inflation induced, this too was rather economic in nature.

The economic periods of weakness simply take longer to sort themselves out. Not surprisingly, these periods also line up with the trajectory of earnings growth. This brings us to our expectations for the second half of 2025. Reflecting upon our 2025 outlook published in early December, not much has changed. We continue to be more cautious on U.S. equity exposure, leaning more so into international developed and emerging markets. Bond exposure remains higher quality with less credit exposure and a good amount of duration, but underweight in bonds instead relying on different types of diversifiers for defense. Our mantra of not reacting to headline news, like policy announcements, remains.

The only major difference is we are becoming increasingly concerned about a potential economic growth scare. And if this develops, it could prove to be a longer process to work its way through the system relative to those event-driven periods of weakness.

Hits & Misses from our 2025 Outlook: Three-peat?

| Section | Key takeaway | How did we do? |

|---|---|---|

| Intro | Expected both economic & earnings growth to go more global, broadening market leadership outside the U.S. | Mixed results |

| Trump 2.0 | Very different starting points vs first term. Listen to the noise, but don’t react. Watch to see if the market materially overreacts and then acting may prove better for your portfolio. | Bang on |

| Can U.S. exceptionalism persist? | Prefer a defensive tilt in U.S. equity exposure as we expected elevated levels of volatility. | Good |

| Pledging allegiance to international equities | Earnings growth and valuations favour international equities and emerging markets | Great |

| Bond market dynamics | Yields to remain rangebound | Yep |

| Diversifiers – old & new | With equity / bond correlations higher, rely on diversifiers. Gold, either bullion or equities, look attractive as does bitcoin. | Nice gold run |

Economic growth scare in second half?

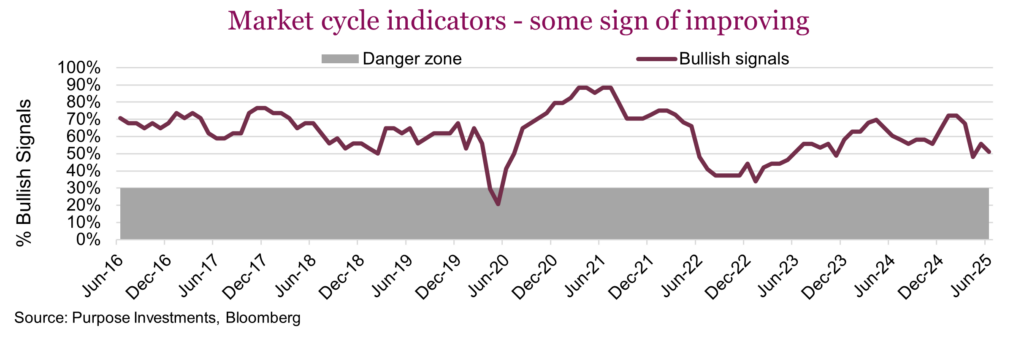

We would not blame anyone for throwing in the towel on trying to forecast the trajectory of economic growth, especially after 2022. As a quick refresher, to combat inflation, central banks tightened more aggressively than any period dating back to the 1980s. The yield curve, carrying a perfect record as an early signal of coming recessions, was deeply inverted. Sentiment data was in the dumps. Recession probabilities spiked higher and the chorus of recession calls grew louder and louder. We were in this choir but not fully convinced as the market cycle indicators did not weaken enough (see chart in Market Cycle section).

With the benefit of hindsight, there were some big factors that helped avoid a recession. The amount of savings accumulated during the pandemic enabled consumers to keep spending despite higher prices due to inflation and higher interest costs. Remember ‘revenge travel’? Meanwhile, employers were finding it hard to find workers as all these savings seemed to encourage people to stay out of the workforce longer. This made the labour market tight and caused wages to move higher. A job for anyone who wants one, at higher wages with lots of accumulated savings in the piggybank, that was certainly enough to offset those other signals/factors. Add to this U.S. fiscal spending that kept up at a higher pace. The end result? A few small negative GDP prints around the world but certainly no recession.

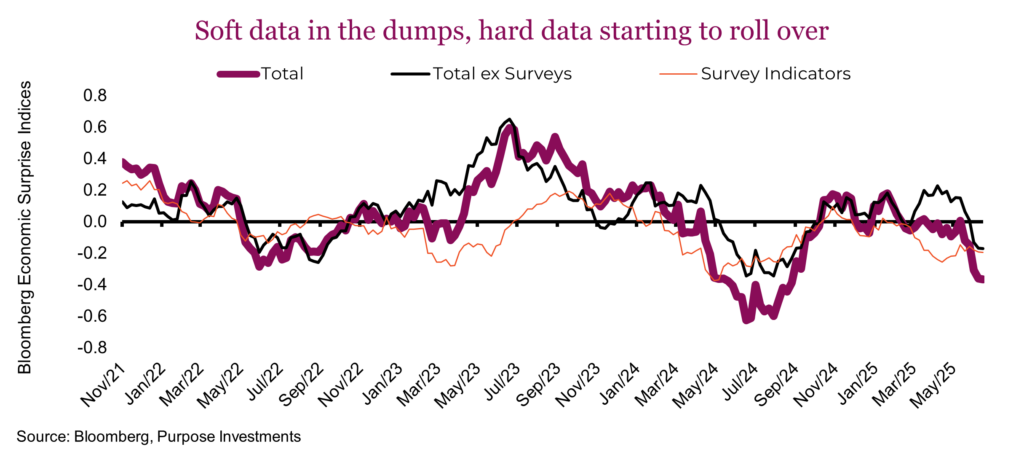

Investing is all about learning and updating your mental models. But that doesn’t mean what happened the last time will happen the next time. So here we are again with economic data softening and sentiment data in the dumps. Unlike in 2022, savings are largely gone, and those jobs are becoming increasingly harder to find. The uncertainty around tariffs has not helped, but make no mistake, this slowing started before the policy risk rose up.

We could highlight the fact that leading indicators have been declining for a few years now, or that manufacturing PMI data in the U.S. is now back below 50. Housing prices have also started to roll over. Sentiment data, which has been weak for a few months, remains so. But now the hard economic data has started missing consensus forecasts based on the Bloomberg Economic Surprise tracking.

Note: survey indicators are often called soft data, with Total ex Surveys as hard data.

Meanwhile, the U.S. consumer is not in a position to spend to backstop the economy. On a positive note, the European consumer remains in great shape, and China is starting to improve. Nonetheless, the risk of an economic growth scare (our baseline) is rising. If just a growth scare, this could prove to be the second buying opportunity of 2025. But its duration may prove longer than many market participants may expect.

Equity position check-in

The first half of 2025 was marked by significant market turbulence, largely triggered by the announcement of higher tariffs on Liberation Day at the beginning of April. While global equity volatility normalized quickly after the initial shock, and the V-shaped recovery has been remarkable, equity markets remain susceptible to ongoing policy and geopolitical risks in the second half.

The factors driving equity performance in the second half of 2025 will likely be similar to the first half: a complex interplay of macro, geopolitical concerns and monetary policy. We anticipate a tug of war between weakening macro data from the tariff shock and the underlying resilience of the U.S. and global economy. Deregulation, tax cuts, and potentially lower short-term borrowing rates are expected to be the key drivers at least in the U.S. to help markets, along with a still-dominant AI theme.

U.S. equities: Resilience tempered by a number of concerns

Both the U.S. economy and consumers have shown resilience amidst extreme policy uncertainty year-to-date. Corporations delivered healthy earnings growth in Q1, with S&P 500 companies showing a solid 7.6% earnings surprise, significantly above the typical quarterly average. This is encouraging from a fundamental standpoint, combined with the Trump Administration’s pivot from tariffs to tax cuts and plenty of cash on the sidelines. The “pain trade” for equities remains to the upside. Markets are back at fresh new highs to begin the second half and we’ll likely see a continued push higher as the trend continues, but the line certainly won’t be straight.

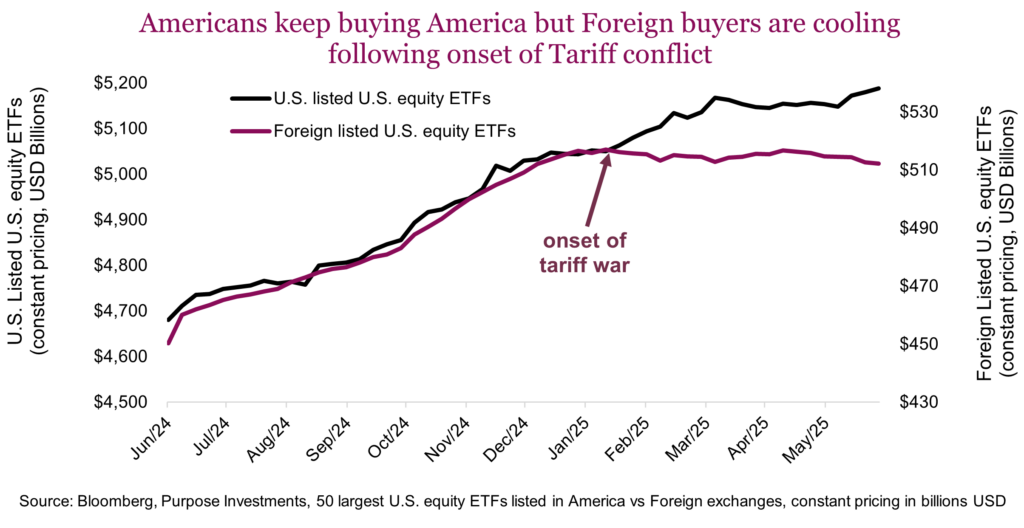

Retail activity slowed somewhat in June compared to May and remains well below levels seen during peak 2021 meme stock mania. The nature of retail buying has also shifted, demand for broad aggregate ETFs was still strong, however interest in single stocks has waned, with profit taking beginning to take place, a pattern that is eerily similar to previous market peaks. Retail’s buy the dip mentality has certainly paid off and while flows were dominated by ETFs, it’s interesting to see that the surge in demand for U.S. exposure is predominantly homegrown. The chart below shows evidence foreign (non-U.S.) buying of America may be waning, while domestic inflows continue. Foreign-listed U.S. equity ETFs would be the go-to ETFs for foreign investors looking to gain U.S. exposure. Interestingly, net-flows have been negative the past three months with an acceleration of net-selling over the past month. It’s not just Canadians who are going elbows up, that same sentiment is taking hold globally.

We remain weary and cautious on U.S. equities due to several factors:

- Underperformance: In the first half, the S&P 500 rose 6.2%, and only 0.6% in Canadian dollars, significantly lagging international markets which rose 20.3% or 13.9% in Canadian dollars. Canada as well managed to outperform so far this year with the TSX up 10.2% YTD. It’s quite the spread, and we believe the relative underperformance will persist.

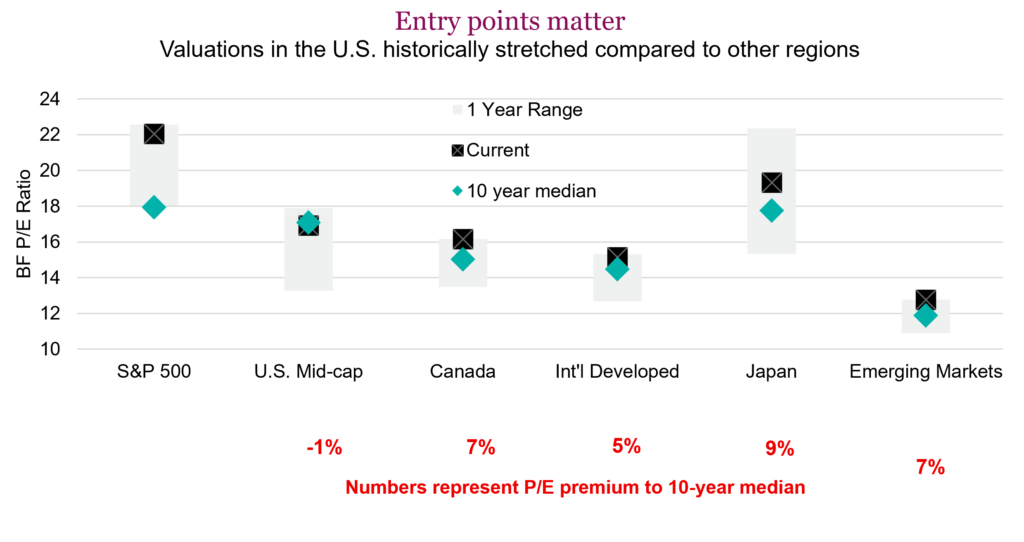

- Elevated valuations: U.S. stocks are currently overvalued relative to their historical averages, with a forward P/E of 22x the S&P 500 is currently trading 23% above its 10-year average. The chart below outlines valuations across the globe, and the U.S. remains the only outlier. Though valuations in Canada and international equities are currently at 1-year highs, they remain at least somewhat in line with long term averages, trading at a 7% and 5% premium respectively. Valuations are a key factor dictating potential future returns. Much like the beginning of the year, the current setup still favours equities outside of the U.S.

- Narrow market leadership: Against a backdrop of sluggish growth and higher-for-longer rates, we are likely to see a repeat of the 2023-2024 playbook of unhealthy narrow market leadership and high market concentration. The U.S. market rebound since April has been led by big tech once again, limiting broader market participation. Breadth isn’t completely terrible; on a technical basis, new highs continue to outnumber new lows, and the percentage of companies above key moving averages remains constructive. What is actually more concerning is the dispersion of the so-called Mag 7. As of June 30, only three of the seven (META, MSFT, NVDA) are in positive territory. Given the group makes up nearly a third of the market cap of the S&P 500, if they are not all moving higher, it limits the potential upside of the broader index.

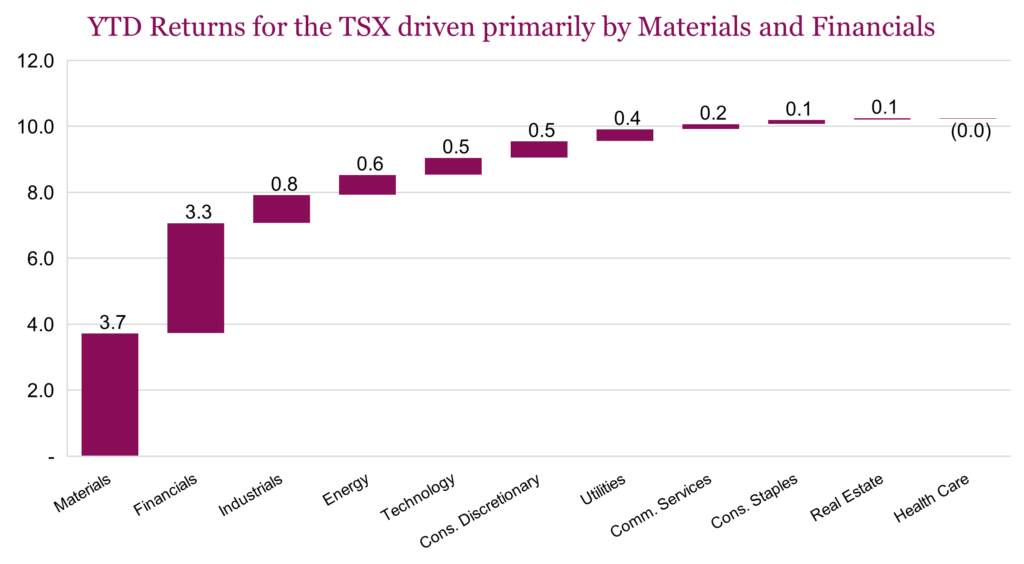

Canadian equities: Better than expected, but see moderation in the second half

The Bank of Canada is adopting a “wait-and-see” approach amidst declining domestic demand and rising unemployment. The economy is not the stock market, and this is especially so in Canada. Many of the largest sectors (Energy and Materials) are entirely dependent on global supply and demand dynamics and could care less what happens domestically. Financials are another matter, and quite frankly the banks have done very well all things considered. TD is the largest contributor to the TSX this year, up 35% and accounted for 13% of the first half’s return. In our multi-asset portfolios, we remain neutral on Canadian equities. Flows to Canada have improved recently, however in the second half Canadian markets would be hard-pressed to meaningfully move much higher without Energy names moving materially higher. Bank valuations are beginning to look somewhat stretched, and we’ve cooled on gold given this year’s advance. Valuations remain attractive, especially relative to our southern neighbour. Without a more positive economic backdrop, it is hard to become more constructive on Canadian equities given the uncertainty with its largest trading partner.

International equities: Remain overweight

International assets are viewed as increasingly attractive and have been leading global equities so far this year. Our broader strategy view remains that international markets should continue trading more favourably this year, with Europe, and Asian equities being favoured; as such we remain overweight heading into the second half.

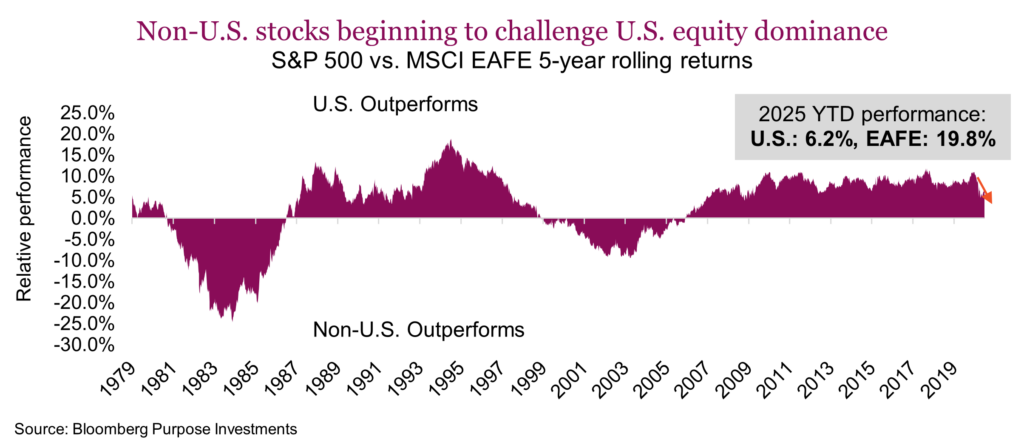

International stocks are currently valued closer to their historical averages, which potentially means greater price appreciation potential compared to U.S. stocks which appear stretched. In the first half of 2025, European equities were up 16.6% in Canadian dollars. U.S. equities have had a long runway of relative outperformance. The consistency of the outperformance on the rolling 5-year basis is impressive, but the relative outperformance is beginning to fade.

Europe’s economy has shown resilience, with data coming in better than expected despite the trade war. The Citi Economic Surprise Index for the Eurozone has been trending higher and stands at 32, compared to -3 for the U.S. Increased infrastructure and defense spending, notably Germany’s €1 trillion stimulus package, are positive tailwinds for European growth. Most major non-U.S. central banks are expected to continue gradual easing of monetary policy which adds to the tailwind.

International diversification is increasingly paying off. After years of U.S. outperformance, many global portfolios are significantly overweight U.S. assets, and a gradual rebalancing is expected as investors continue to add to non-U.S. assets. This stat we came across is interesting. A mere 1% shift of value from the 10 largest U.S. stocks to the 10 largest international stocks in the MSCI EAFE Index could increase their market cap by 7.5%. This diversification also provides exposure to different sectors besides big tech.

Emerging markets: Still room to run

While EM growth will have challenges in the second half due to tariff impacts, the outlook remains constructive. Again, monetary policy is easing across many emerging markets and is anticipated to continue. A weaker U.S. dollar is also helpful for emerging economies as it eases debt burdens, supports commodity prices and boosts overall economic activity in EM economies. Valuations are also quite attractive with a forward price-to-earnings ratio of 12.7x, a bargain compared to the U.S. and even other developed markets. Lastly, there is sentiment and positioning. EM exposure remains quite depressed after many years of underperformance.

Final thoughts

We have no crystal ball, and if the first half has taught investors anything it’s that the next 3½ years will be full of ambiguity and bursts of rapid change. Markets reflect the past, but investing is about positioning in the best way possible to anticipate what comes next. Given the uncertainty and our expectations for a bit of a growth scare, focusing on valuations and resilient growth is a good start. Stay long international equites, and start to fade the rally in the U.S as it extends.

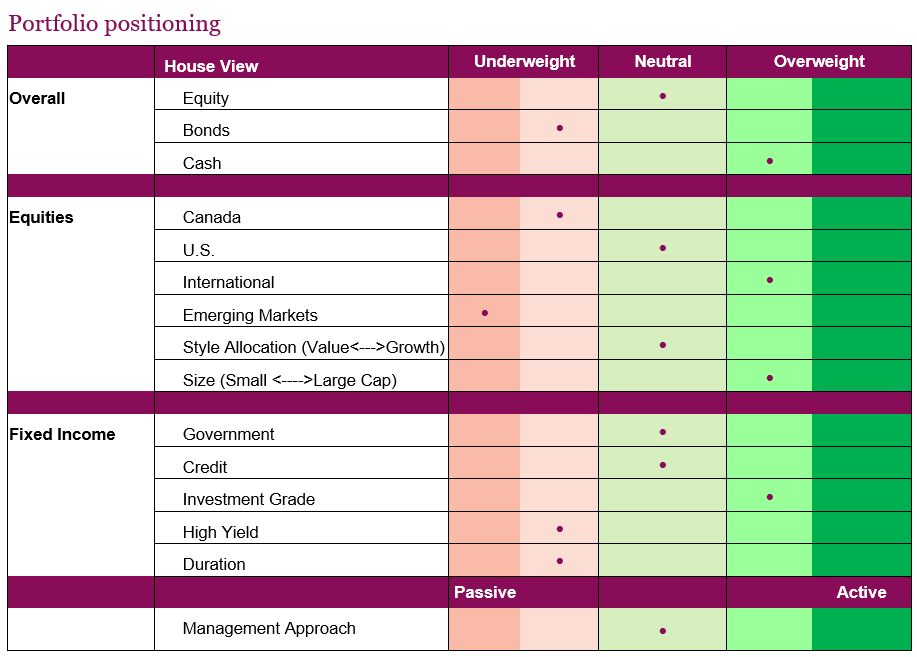

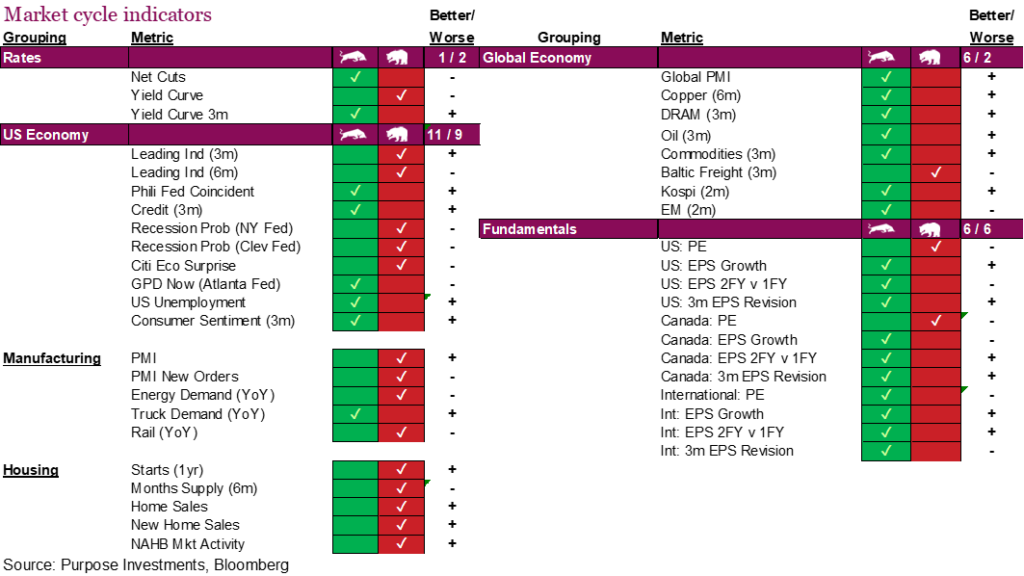

Market cycle & portfolio positioning

The market cycle indicators are still decently above the danger zone but the trend is to the downside lately. The weakness is more focused on the U.S. economy. Global economic signals remain stable with five bullish and three bearish, while fundamentals are also stable. On the U.S. side the yield curve has flattened combined with weakness in the two more cyclical components of the economy, namely housing and manufacturing. PMI and energy demand remained bearish and were joined by rail volumes. With softness in new home sales, all the housing indicators are now bearish.

The expectation is that economic growth continues to soften and at some point the market may react negatively. With higher quality bond exposure and duration plus our cash and defensives, there are many options to pivot taking advantage of any market weakness.

Final note

We would not put ourselves in the bearish camp, instead highlight the risk-to-reward ratio appears to be at least partially tilted for more risk than reward. This market has moved back from overreacting to bad news to overreacting to good news. As contrarians this has us dialing back a bit and leaning more on defense. Positioning for uncertainty remains paramount for 2025.