Investor Strategy

August 2025

Making sense of the noise

Sign up here to receive the Investor Strategy by email.

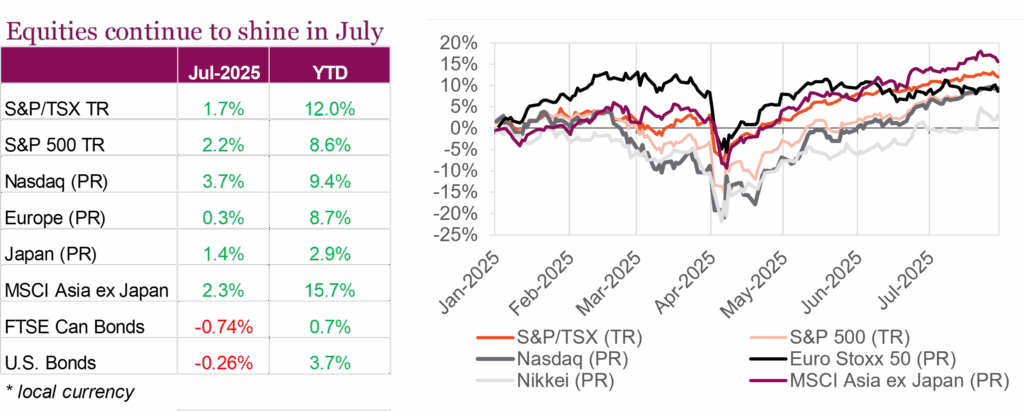

Record highs in July

Equity markets moved higher in July, with major indexes notching new all-time highs. On a total return basis, the TSX gained 1.7% while the S&P 500 advanced 2.2%, extending its recent rally that has seen U.S. markets rise over 28% since their April low. Tech companies, particularly those tied to AI, are once again fueling outperformance. Year-to-date, the S&P 500 and TSX are up 8.6% and 12.0%, respectively, as optimism over resilient growth overshadows macro headwinds.

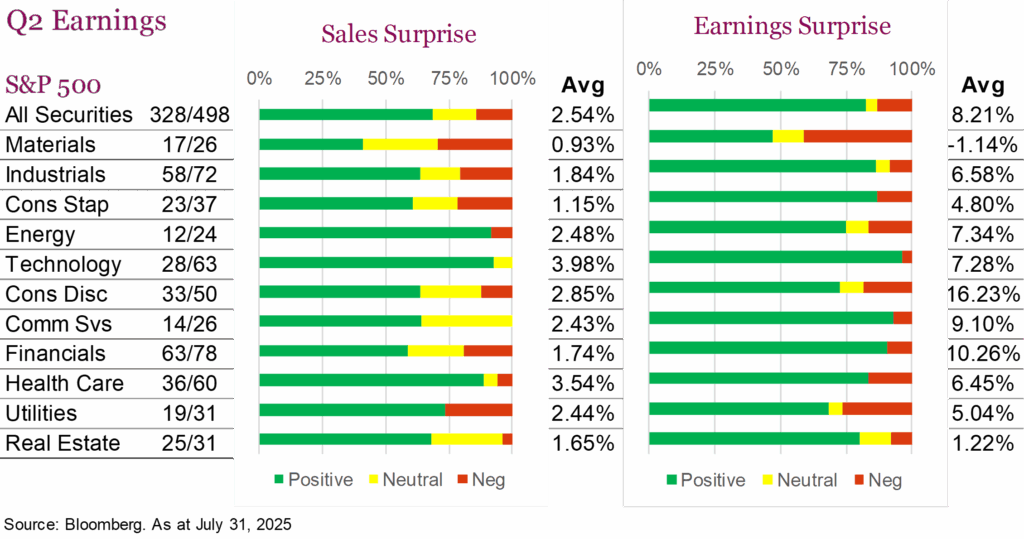

Q2 earnings season has been a key driver of recent market gains. With roughly two-thirds of S&P 500 companies having already reported, 80% have delivered positive EPS surprises, while 70% beat revenue estimates. Looking outside of equities, the U.S. dollar continued to weaken, hovering near a three-year low. Bonds struggled in July while FTSE Canada Universe Bond Index fell -0.74%, and the U.S. Aggregate Bond Index declined -0.26%. The weakness reflected a shift in rate expectations with investors scaling back hopes for near-term cuts as central banks reiterated their inflation vigilance.

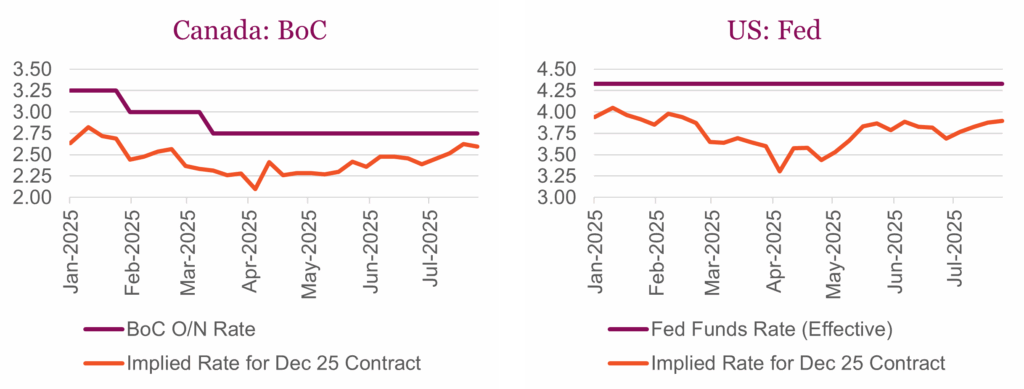

Central banks met over the month, with many, including the BoC, Fed, and ECB, deciding not to cut rates amid inflation concerns and persistent tariff threats. The Bank of Canada left its policy rate unchanged at 2.75% for a third consecutive meeting, citing uncertainty around U.S. tariffs and trade conditions. While headline inflation sits near 2.5%, core measures remain closer to 3%, keeping policymakers cautious despite a resilient economy and strong June job gains. In the U.S., the Fed also held rates steady at 4.25%-4.5% for a fifth straight meeting. Fed Chair Jerome Powell stressed patience as officials await further inflation and labour data. Notably, dissent emerged for the first time in decades, with two officials advocating for immediate cuts, along with calls from Trump to lower rates, underscoring the growing divide over how to balance persistent inflation against a cooling labour market. Rate markets are currently pricing in about one rate cut for both central banks by the end of 2025.

While recession fears have not completely disappeared, investors did see some positive data prints in July. The U.S. economy surprised with 3% annualized growth in Q2, a sharp rebound from Q1’s 0.5% decline. Strong consumer spending and exports drove the turnaround, with July’s ADP report showing job gains of 104,000. Wages continue to rise at a 4.4% annual pace, highlighting labour market resilience despite tariff-related uncertainties. Still, inflation progress remains limited with the Fed’s preferred gauge, core PCE, rising 0.3% in June and 2.8% year-over-year, suggesting lingering pressures. Canada’s economy also showed resilience. After fears of a contraction, Q2 is expected to show slight growth, helped by a 0.1% GDP gain in June, firm retail activity, and solid labour markets. While manufacturing softened under trade headwinds, confidence improved as tariff impacts proved smaller than expected.

Markets enter August with momentum but also elevated risks. Equity valuations are stretched, particularly in the U.S., while sticky inflation and tariff-driven volatility complicate central bank decision-making. The dollar’s weakness, alongside upgraded growth expectations, may support risk assets in the near term, but investors remain watchful of policy shifts and potential macro surprises. With stock markets hitting multiple record highs in July, it is likely a good time to take a deeper look into your portfolio positioning, particularly in equities.

The great rebalance

Perhaps one of the biggest challenges for investors is the noise, the constant loud onslaught of information about what is happening in the market and why. The noise is very short term in nature, dominated by the news of the day or week. Sometimes, underneath all this noise, there is a signal that something has changed in a more meaningful or longer-term nature. It is this signal that can make us more money or help sidestep danger. The rise of AI or digital assets are signals, as is the return of inflation, with no shortage of noise around them along the way. These are not new signals; they are already many years old.

One newer signal is potentially a shift to rebalance portfolios towards more international, and consequently less U.S. This has the potential to be a very long signal. Of course, the cautionary narrative is the many times over the past decade that investors got excited about international equity outperformance only to suffer as these past signals turned out to be more noise and the U.S. resumed its performance dominance.

So, should investors lean into more international at the expense of their beloved U.S. equity allocations? We believe so and will share our thoughts broken down into the near term and longer-term secular considerations. Signal or noise, you be the judge.

Investors in 2025 have certainly taken note of the relative performance among different equity markets. Not that anyone should be complaining, they are all in the green, but the disparity is rather wide. In Canadian dollar terms the TSX is +11%, UK +14%, Germany +30%, Japan +5%, Hong Kong +19%, overall emerging markets +13% and the U.S. at the bottom at +4%. The vast majority of this divergence occurred before the Liberation Day tariff sell-off — since then markets have largely moved higher together. Is this noise or a signal?

Longer-term considerations

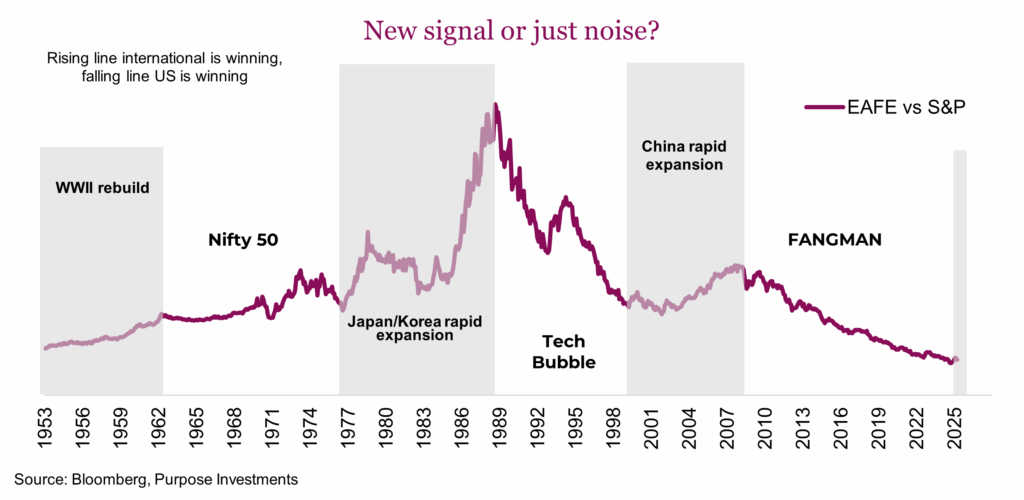

Long cycles – The history of markets and relative performance certainly points to very long-term cycles of relative outperformance (above chart). The duration of these cycles often surpasses even decades. And given the most recent long cycle strongly favoured U.S. equities does set the stage for a reversal, in favour of international. We’re not suggesting it is as simple as saying: in the 80s international won, the 90s U.S. won, the 00s international won, the 10s to mid-20s U.S. won, so now it is international’s turn. Or maybe it is that simple. Whether it has truly started or not, the long-term relative performance setup for international is certainly in place.

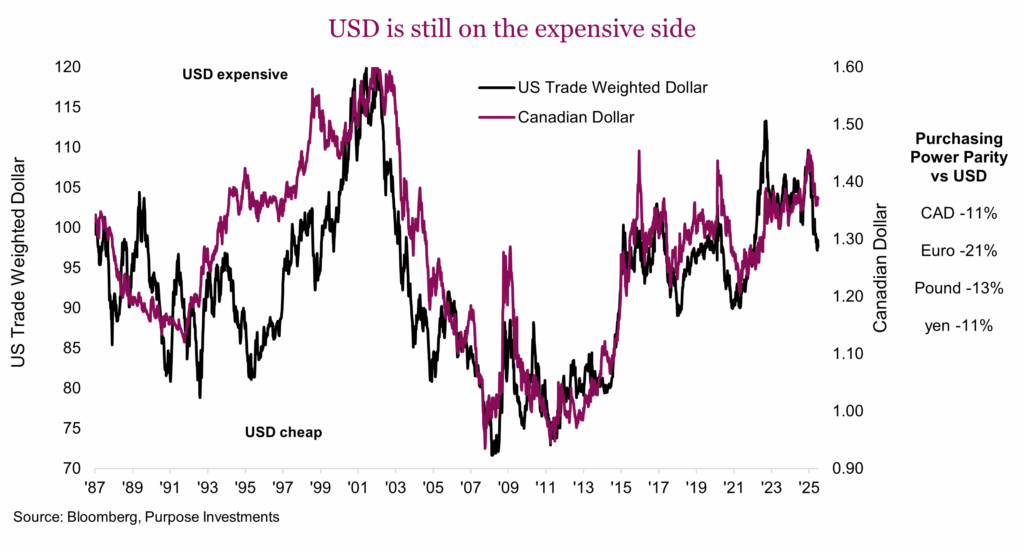

USD declining – You can’t talk international investing without having a view on currency. Predicting where a currency will go over the next few quarters is very challenging. But, among developed nations there is a strong long-term reversion to the mean. And while not crazy extreme, the USD is on the expensive side of the mean. It is also worth noting that the relative equity market outperformance of the U.S. or international, often kicks off from low relative value on the currency side. From current levels, that setup favours international over U.S.

The U.S. dollar does enjoy the status of global reserve currency, and this comes with a bit of premium valuation. While we do not think the U.S. dollar will lose its reserve currency status anytime soon, it is certainly losing some of the status. Confiscating other central banks reserves for political reasons, whether you agree with the move or not, doesn’t help your status as global reserve currency. Nor does policy uncertainty of the current administration from chipping away at central bank independence to tariffs. Tariffs will slow global trade, and that means less buying of USD.

We are not U.S. dollar bears as potential slowing of global economic growth may bid up the dollar, but the longer-term trend in coming years is likely on the downside. And that means other currencies likely appreciate, again favouring international (unhedged obviously).

Everyone is overweight U.S. – Being a contrarian investor is often the better approach than simply chasing a trend, especially if that trend appears to be in its late innings or perhaps already over. Even if you have some hesitancy towards the view that international is poised to outperform U.S. equity markets, there is no denying after so many years of outperformance most portfolios have a healthy overweight America. Chalk it up to recency bias or performance chasing, it would seem most portfolios are heavy America and light everywhere else. When most investors are on one side of the boat, it is usually best to move to the other side or at least back to a more neutral positioning.

This trend of arguably oversized U.S. weights relative to international is also evident when looking at funds/ETFs in the global equity category. Based on global equity managers, their non-U.S. equity weight went from 60% in 2010, to 50% in 2015 to 40% more recently.

No denying this has been the right call over recent years through the end of 2024. But given the setup and current exposures, a more international mix may be prudent. And if you think you missed the boat, we would remind readers that if this signal is true, it may have years to run.

Near-term considerations

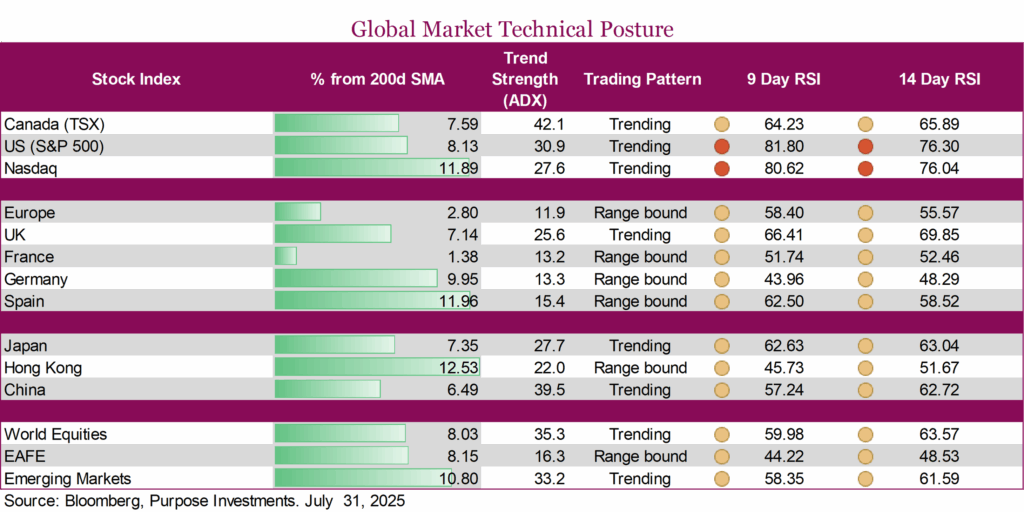

Technically stretched in the U.S. – As we enter the back half of the summer, U.S equity markets find themselves in a precarious position. Technically (at the time of writing), U.S. equities, specifically the S&P 500 and NASDAQ are two of the most overbought indices globally. The relative strength index (RSI) is flashing warning signs and well into overbought territory. While this doesn’t mean an imminent correction, it does suggest a high level of short-term froth in the market. Prices are rising, the trend strength remains strong, and the bulls remain in control for now. While the bullish momentum continues, the mathematical reality of mean reversion suggests current levels may prove unsustainable without extraordinary fundamental support.

Conversely, European, Asian and emerging markets present a very different technical picture. These international markets remain largely range bound and sit comfortably below overbought levels, suggesting there is room to run should sentiment shift once again from the dominant AI trade. This divergence creates an opportunity where international diversification may offer both defensive characteristics and upside potential.

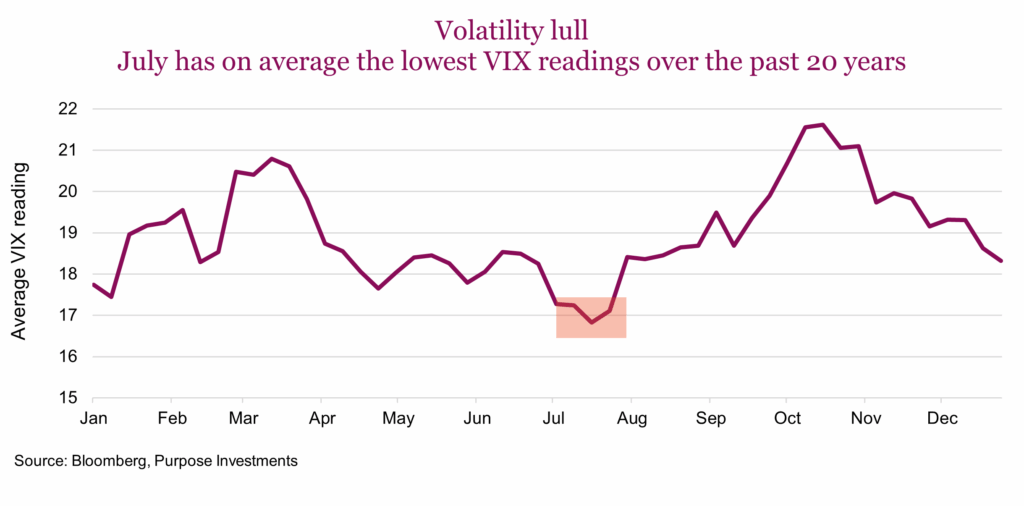

Volatility lull – One of the more interesting patterns in market seasonality is the well-known summer lull. As the chart below depicts, over the past twenty years, the last three weeks of July have the lowest average VIX readings. This year is no exception. Over the past two months there have been precisely 3 days when the S&P 500 has moved more than one percent in either direction. It’s been an unusually calm market backdrop despite the seemingly high level of geopolitical uncertainty.

This calm in the summer doldrums presents an ideal time to reconfigure portfolios. There is less noise to obscure the decision-making process, and emotions are calmer. This all makes it easier to focus on the long-term and make shifts to strategic portfolio asset allocations.

AI is the difference maker – This year’s international outperformance predominantly took place in the first few months. Over that time, there were two significant catalysts. The first was the fiscal policy pivot from Germany, marked by big spending plans on defence and other infrastructure projects. This shift away from a more austere fiscal policy stance sparked market optimism on future European growth prospects. The second, and more substantial reason was the DeepSeek moment that temporarily disrupted the AI investment narrative. The mini panic across AI-related stocks impacted both directly and indirectly related companies. It also showed how broad the narrative is across U.S. markets. This mini correction wasn’t driven by fundamentals or earning misses, but by cracks in the sentiment. For a few days it felt like the scaffolding holding up the AI trade might falter.

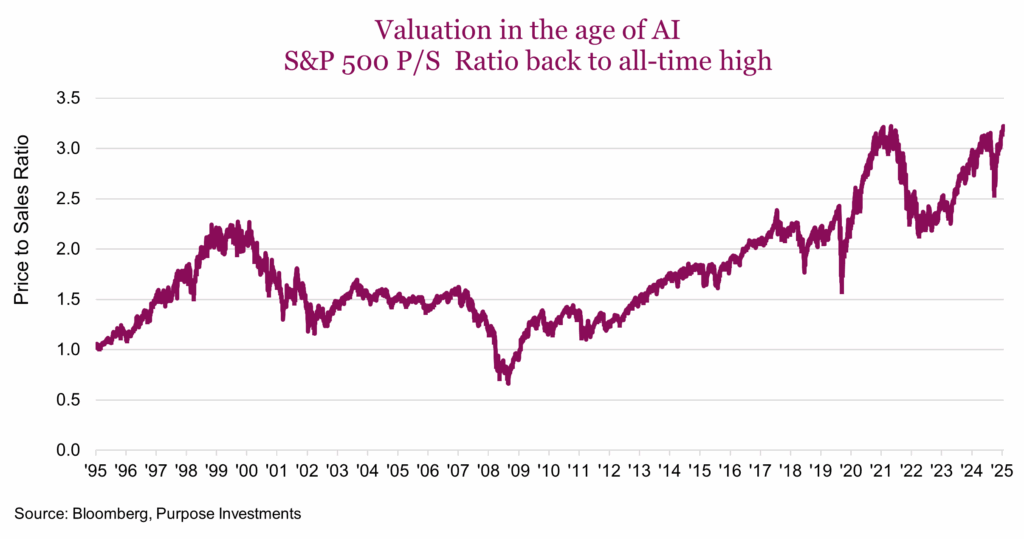

The moment passed, and the rally has resumed. There are now two companies – Nvidia and Microsoft – that have surpassed $4 trillion in market cap. Valuations based on the price to sales ratio are now at all-time highs matching levels last seen in 2021, as seen in the chart below. The core reason for the high price to sales ratio is that investors are now willing to pay massive premiums for companies that they believe will have explosive revenue growth in the future.

The AI party continues – though it may now be late evening, no one knows how long it will last. It could be lights out at 11 pm, or carry on until sunrise. What we do know is that enthusiasm is rampant, and there are legitimate reasons to be excited. But no matter how good the party is, it can always be spoiled. There is no guarantee that those who spend the most and throw hundreds of millions of dollars to recruit AI all-stars will win this race. For all we know, there isn’t just one winner. China could very well end up an AI winner. In investing, you want to cover your bets so having some exposure to China can help ensure a more balanced approach, especially by including emerging market positions that may also benefit from parallel AI developments.

The current valuations and technical divergence suggest now is a good time to rebalance and tilt towards a healthy overweight international exposure. Not only does this shift diversify away from U.S. centric risks but it also offers a broader range of potential winners in evolving global themes. Rebalancing doesn’t require a bearish outlook; it simply reflects the discipline to manage risk and recognize that no rally lasts forever. With volatility low and U.S. sentiment increasingly euphoric, it’s worth pausing to ask: is your portfolio as diversified and future proof as it could be?

International is a fixer upper – There is no denying America has a lot going for it. Strong entrepreneurial populace, amazing access to capital and generally corporate-friendly regulations. Meanwhile many international markets suffer from a more challenging regulatory environment, or challenging demographics or slower economic growth. This is plain to see if you compare the earnings growth for the S&P vs EAFE over the past 10 years. $1 of earnings for the S&P grew to $2.65 over the past ten years. For international developed markets, that same $1 only grew to $1.66 – clearly explaining the relative outperformance over the past decade for the U.S. equity market.

But just like in real estate, sometimes the biggest gains come from the fixer-upper opportunities compared to the new modern home. Replacing the windows and a new coat of paint can go a long way in creating value. This may be the case for international in different ways in different regions.

Fiscal spending to spur economic growth appears to be accelerating. Keep in mind coming out of Covid, the U.S. continued to run large spending deficits (aka fiscal spending) while other regions from Europe to Japan brought their deficits down much more. This does partially explain the economic growth gap over the past few years, with U.S. leading. But now Germany has increased fiscal spending plans – the DAX is one of the best markets so far this year. Others appear to be following Germany’s lead.

Japan has continued its long journey of improving corporate governance and making companies more shareholder friendly. Meanwhile, thanks in part to retirement saving structures, individual investors are increasingly becoming equity holders within retirement plans, instead of simply parking cash at the post office. Equity ownership in Japan is still low 10-15% compared to 40-50% in the U.S. But they are catching up.

Add in the policy uncertainty coming out of the U.S., from tariffs to defense, and this has become a bit of a kick in the butt for other nations to start pulling levers to increase their own growth prospects or attract capital. Cutting red tape, fiscal spending on economic growth, re-distributing trade, are all positive moves in the right direction.

Rate of change matters in markets and it would appear international markets, generally speaking, are becoming a bit more investor friendly. America is still the gold standard but if the gap narrows, so could the valuation gap.

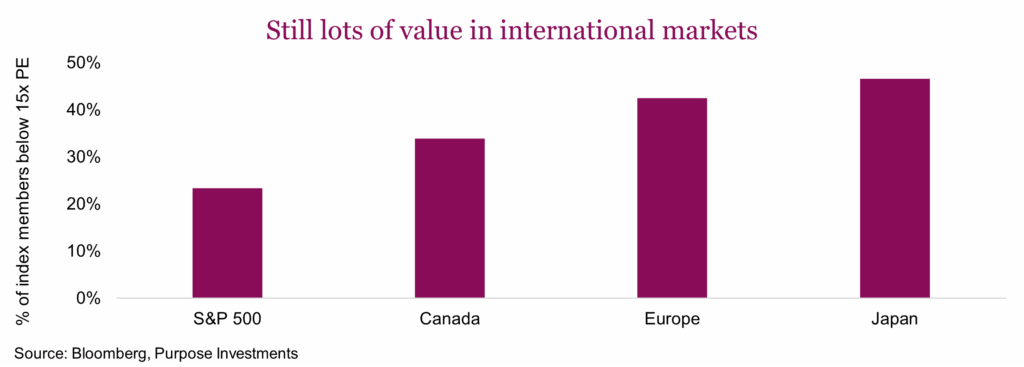

Valuations – No need to beat this repetitive drum on valuations, the world knows the valuation spread is historically wide between the U.S. and international markets, and that has been the case for many years. S&P 500 at 22.5x forward earnings estimates, which has proven peak valuations over the past decade, is still expensive vs Asia at 16.5x and Europe at 14.5x. International valuations are actually a bit higher now than a year ago, mostly due to some price appreciation.

Headline valuations are often skewed by a few names for market cap weighted indices. Another lens is simply looking for the number of index members trading above or below a certain threshold, in this case 15x price-to-earnings. The S&P only has 23% of its index constituents trading below 15x, Canada is not far behind at 33% while Europe and Japan have almost half index members below 15x.

Valuations are how much you are paying for earnings, but they don’t capture earnings growth. The U.S. is still enjoying stronger earnings growth than international developed markets in 2025, albeit a lower spread than in previous years. But 2025 is now half over and expectations for international have been brought down a large amount due to tariff fears and uncertainty. Again, this lowers the bar for future growth. Estimates for 2026 are roughly equal across developed markets, and given the valuations spread international is certainly favoured.

Touching on emerging markets (EM), we are getting optimistic. EM has performed well this year even given certain well-known headwinds. In past years, one would have thought rising tariffs and higher global interest rates would really hurt EM, but the markets and economies have proven resilient. In aggregate, they have been cutting interest rates ahead of developed markets, which has helped their economies. Plus, if US dollar general weakness is of concern, many EM nations are commodity heavy, providing a potential valuable diversifier for portfolios.

Market cycle & portfolio positioning

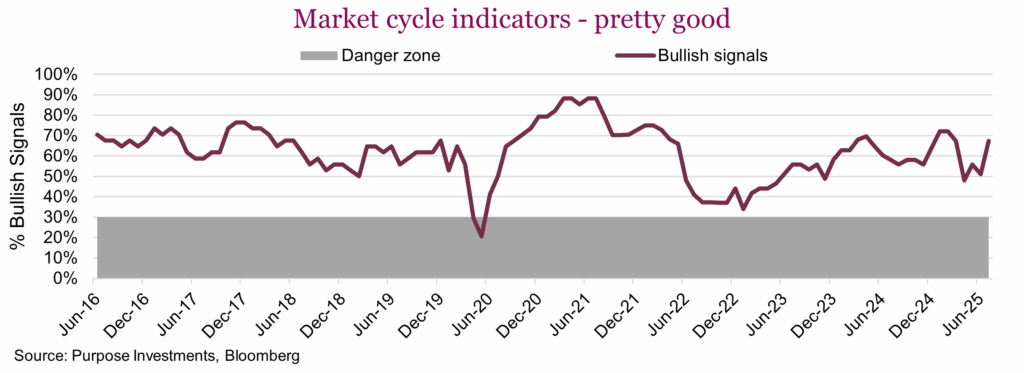

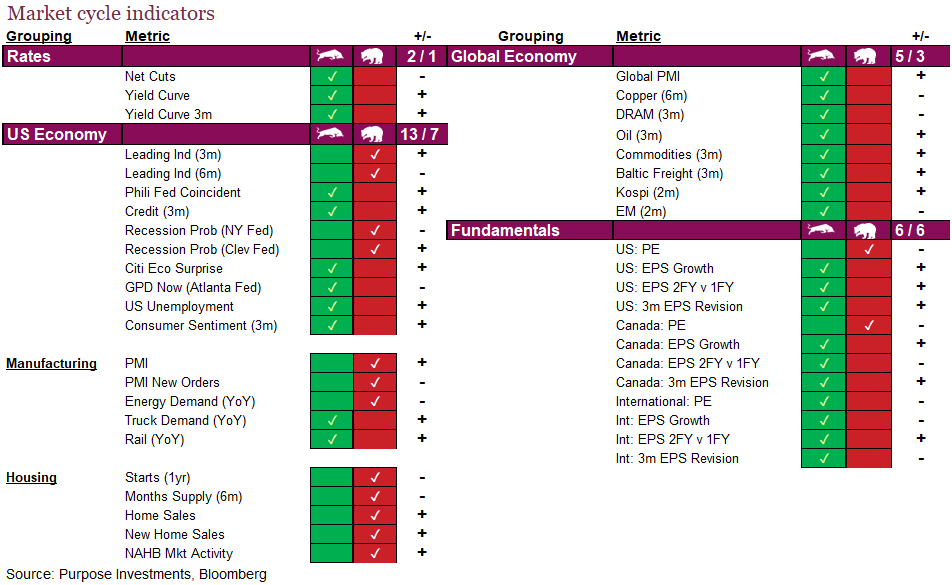

Our market cycle indicators have improved over the past month, with a notable uptick in global economic signals. In fact, all eight are bullish, providing additional support for a reasonably stable global economy. The U.S. economy improved a little bit but remains rather mixed. All five U.S. housing signals are bearish, with higher mortgage rates continuing to weigh on this cyclical and important part of the U.S. economy. Employment and consumer sentiment remain supportive as leading indicators and recession probabilities are bearish.

Overall, we remain a bit on the defensive side with a healthy cash level. Valuations have become even more challenging, and we continue to see a reasonable risk of slowing economic data in the coming months.

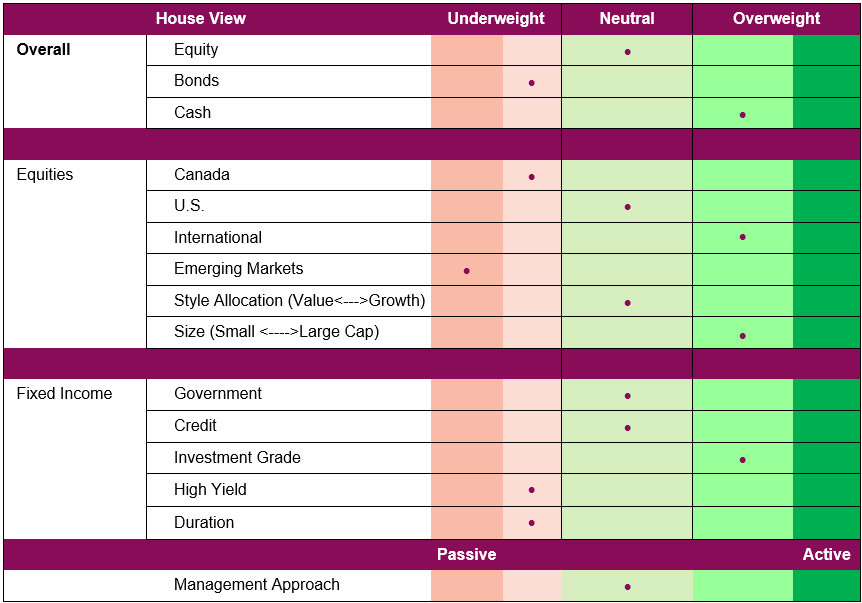

Portfolio Positioning

Final note

Is the relative outperformance of international equity markets vs the U.S. a signal of a changing long-term trend or just noise? Nothing is ever certain, but the supporting evidence certainly has us believing the signal has a higher probability. This coupled with the pre-existing prevalence of overweight U.S. and limited international equity exposure, at the very least encourages a more balanced allocation. No denying the AI theme could continue to drive U.S. equity outperformance, but themes rarely play out as market participants expect. And with the S&P in overbought territory, this could prove to be a good time for some rebalancing.