Investor Strategy

September 2025

Playing “D” (diversification, that is)

Sign up here to receive the Investor Strategy by email.

- Summer ending on a high note

- Searching for diversification

- In search of portfolio diversifiers

- The great Canadian disconnect

- Market cycle & portfolio positioning

- Final note

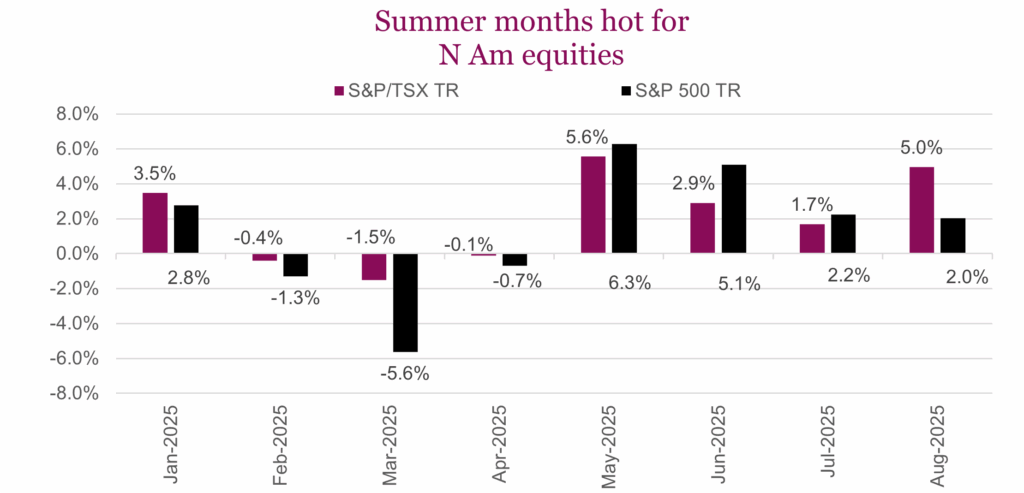

Summer ending on a high note

Equities extended their rally in August, powered by a strong corporate earnings season and steady economic momentum. Both the S&P 500 and the TSX notched new record highs over the month, securing a fourth consecutive month of gains. The S&P 500 advanced 2% on a total return basis, while the TSX outperformed with a 5% monthly gain, led by strength in Materials and Financials. Investor optimism was further buoyed by expectations that the Fed will deliver its first rate cut of 2025 at the September meeting. These policy hopes helped push U.S. Treasury yields lower, lifting U.S. aggregate bonds 1.20% higher on the month. Canadian bonds also posted modest gains, with the FTSE Canada Universe Bond Index rising 0.37% in August as markets assessed weakening domestic growth and the BoC’s more dovish tone.

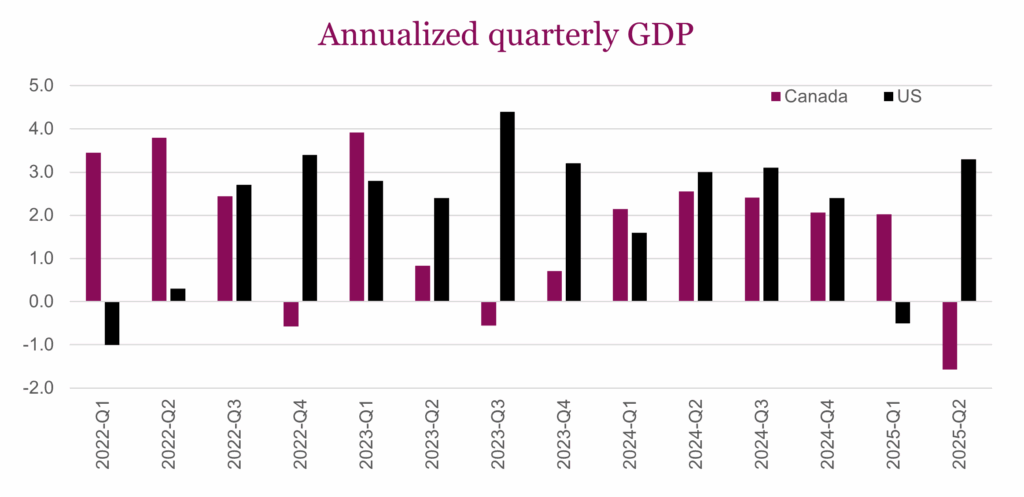

In the U.S., annualized GDP (q/q) moved higher to 3.3% from the prior reading of 3.0%, bolstered by stronger business investment and an unprecedented contribution from net exports. Gross domestic income rose 4.8%, while corporate profits rebounded 1.7% following their steepest contraction since 2020. Household spending remained resilient, with personal consumption rising 0.3% in July, its strongest increase in four months. Inflation, however, remains a persistent challenge with headline PCE prices rising 2.9% year-over-year in July, the highest since February. Core PCE also climbed 0.3% on the month. This sticky inflation print leaves the Fed balancing the need to support growth through easing while ensuring policy credibility is not undermined.

North of the border, Canada’s economy faltered, contracting at a -1.6% annualized rate in Q2, the sharpest decline since the pandemic. The downturn reflected a tariff-driven 27% decline in exports and a 10.1% drop in business investment. Domestic demand, however, provided a cushion, rising 3.5% on the back of stronger consumer spending, government outlays, and a rebound in housing activity. Preliminary July GDP data suggested a return to modest growth, implying that the weakness may be largely trade-related rather than systemic. Still, subdued income growth and labour market softness pose risks ahead, keeping the BoC on alert and open to further policy easing should conditions deteriorate.

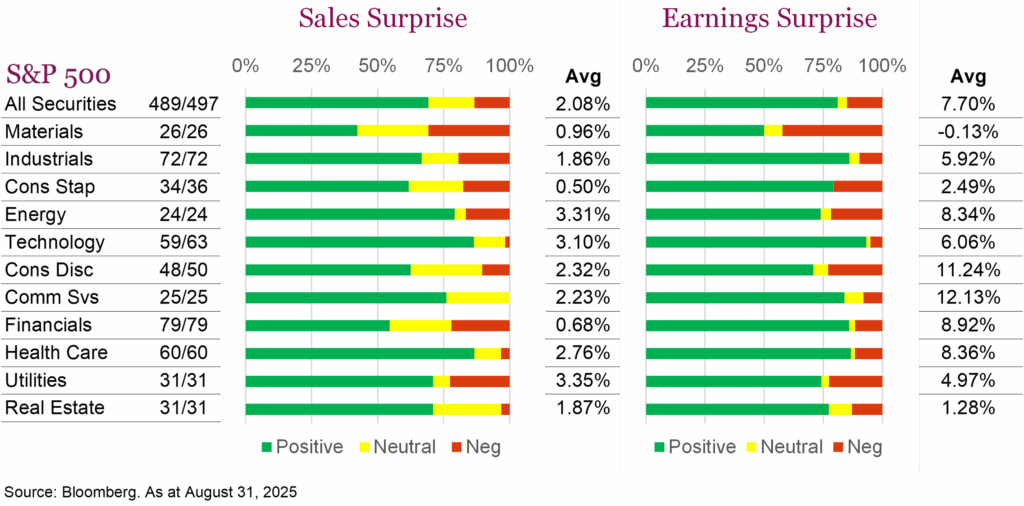

Earnings provided key support for equity markets in August. With nearly all S&P 500 companies reporting, 81% delivered positive surprises on both earnings and revenue. Fewer companies are flagging recession risks, with mentions in earnings calls falling sharply from 124 in Q1 to just 16 in Q2, a sign that corporate leaders see the slowdown as less threatening than earlier in the year. That said, risks remain, particularly from market concentration. The so-called Magnificent Seven now account for 34% of the S&P 500, rising to almost 40% when including Broadcom, Berkshire Hathaway, and JPMorgan, a level well above the dot-com era. With the forward 12-month P/E ratio at 23.9, well above historical averages, valuations appear stretched, underscoring the importance of continued earnings strength and economic resilience to sustain equity market momentum.

Searching for diversification

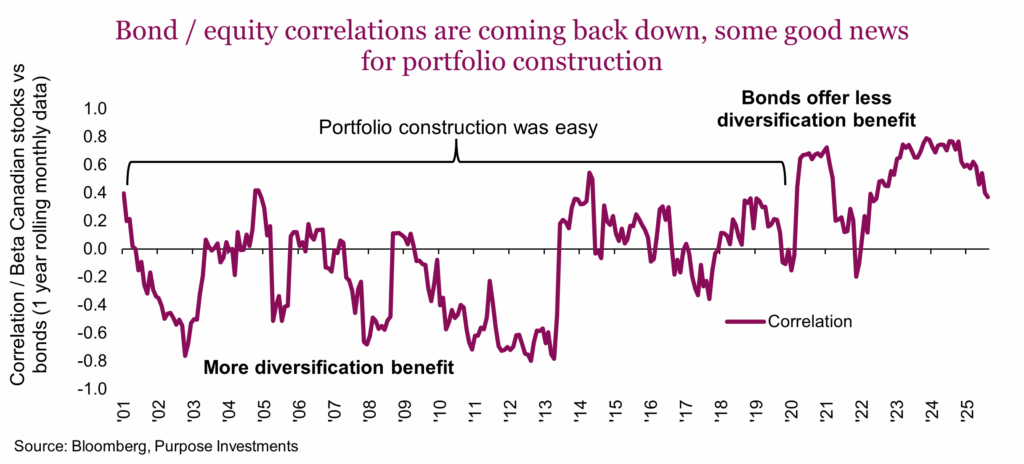

Diversification across different investment asset classes sits as the foundation of portfolio construction. Combining different asset classes that behave differently in various market regimes provides greater portfolio stability — reducing overall risk and the risk of making a behavioural mistake. We can all remember the 2000-2020 period that saw reliable negative correlations between equities and bonds, the cornerstone of most portfolios. And we can all remember the past few years when those correlations moved higher, causing greater portfolio volatility and making diversification harder to find.

One of the reasons correlations moved higher in recent years was the return of a higher inflationary environment. Inflation hasn’t gone away but it has cooled enough for most central banks to gradually reduce short-term rates. The good news is the strongly positive correlation between equities and bonds is starting to come back down. Just look at Canadian bonds (measured by the Bloomberg Canada Aggregate Bond Index), which have declined for six months in a row; precisely what they are supposed to do when equity markets are moving higher during this period. As a result, the one-year trailing correlation between Canadian equities and Canadian bonds has started to come back down.

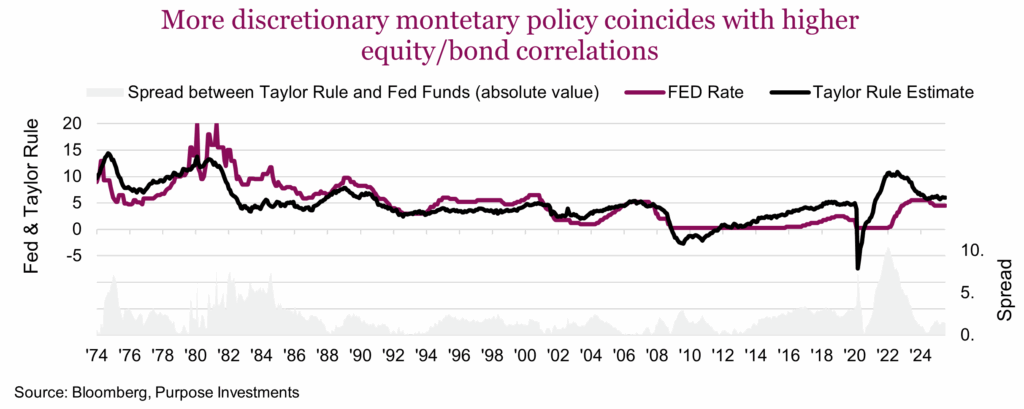

We could celebrate this improving correlation trend, but it may be way too soon to pop the cork. Historically, when monetary policy (short-term rates) have been more driven by economic data, mainly focused on price stability, bond/equity correlations have been lower. And when monetary policy has been set more by other factors, correlations have been higher. For the U.S., over the past year the spread between actual Fed Funds rates and the Taylor rule has been much higher than normal. The Taylor rule is a guideline for short-term rates based on inflation and economic growth. Even today, the Taylor rule suggests a Fed Funds rate of 6%, a full 1.5% above the current rate. And there is mounting pressure to cut short-term rates, despite the U.S. economy growing by over 3% and with inflation still elevated.

The conclusion is that central bank policy is being driven by other factors outside the economic data. This is not an environment that we should expect bond/equity correlations to move back into negative territory, even though they are improving of late. This also highlights the need to find diversification for portfolios from other sources. On this, there is good and bad news.

In search of portfolio diversifiers

The tools for constructing well-balanced portfolios have always evolved over time as different strategies with different performance characteristics continue to increase in availability. At the same time, correlations are not stable over time and some investments that were great diversifiers can change to become less so. And if you wait long enough, they may become great diversifiers once again.

Because of this evolving availability and shifting market correlations, diversifying across different diversifiers remains prudent. Bonds were great diversifiers, then not at all, and are now showing some signs of improvement. The good news is there are other asset classes that have started to become better diversifiers than years past, and some that have gone the other way. Here are a few examples:

International equities

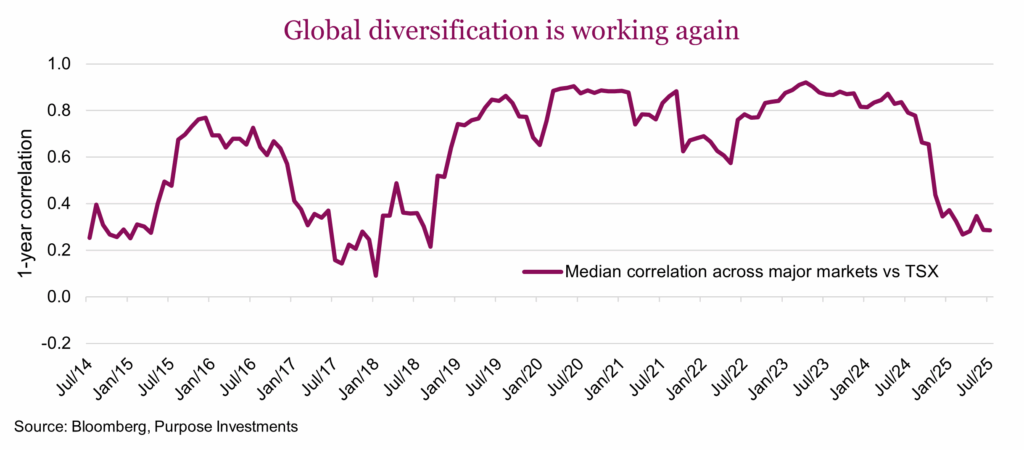

The benefits of international equity diversification were extremely strong from the 1980s to 2000 as individual equity markets moved to their own beat. However, as markets became more intertwined, this diversification benefit softened and then in 2019, correlations between markets were very strong again. This greatly reduced the benefits of going more global in portfolios, at least from a diversification perspective.

However, this inter-market correlation has fallen dramatically in the past year. Across major equity indices, the median correlation with the TSX has fallen to about 0.3, roughly the lowest correlation in the past 15 years. That certainly adds one more solid reason investors may benefit from increasing international diversification. And while a broad market sell-off certainly drags down all markets, even during the turmoil earlier this year there were material differences in the pain felt across different markets. Year-to-date performance at the global equity market bottom on April 8 had global equities down -12%, S&P -15%, TSX -9%, UK -3%, Germany +2% and Hong Kong flat.

In a more polarized world, markets do appear to be diverging, providing support for international diversification.

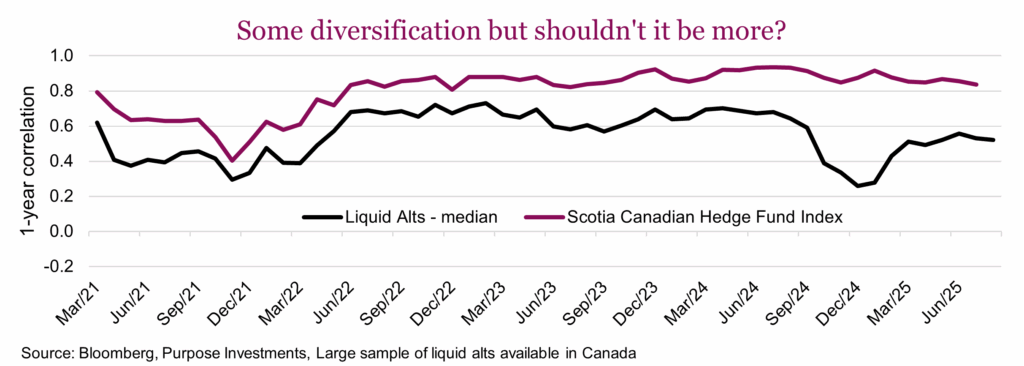

Alternatives

We are just going to scratch the surface here, and we have our own disclaimer. Given the diversity of strategies in this space, any sort of aggregation insights have their limits. That being said, it should be better. Scotia’s index is an equal weight among hedge funds managed by Canadian domiciled managers. The Liquid Alt below is a large selection of liquid alts available in Canada (48) with very different strategies. This is the rolling median correlation among them versus the TSX.

The variance among different strategies is large. There are many that are great diversifiers against market risks, and there are many that are really just equity exposure with a few twists. A higher level of due diligence is required and understanding a position’s purpose for the portfolio is critical.

Alternatives are certainly a source of diversification for portfolios, but require extra research and due diligence.

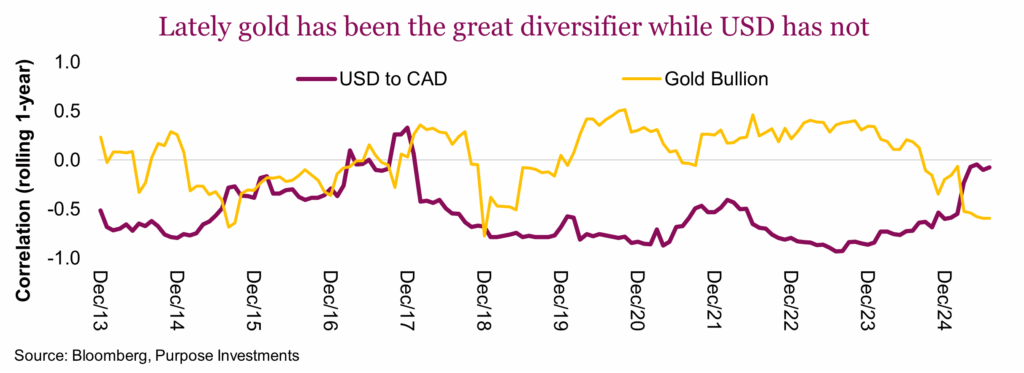

Currency and gold

There is a general rule for Canadian portfolios: the U.S. dollar is great. History has shown when there are periods of market weakness, the U.S. dollar often rises in value, providing a very valuable source of portfolio diversification. This happens for a few reasons. Most periods of market weakness can be traced back to concerns over economic growth. Given the U.S. is less sensitive to global trade than other nations (including Canada), and is the global reserve currency, combined with the fact that many investors bring their money back home to America when trouble comes, the U.S. dollar tends to rise during times of uncertainty.

However, as central bank independence and policy uncertainty are home grown in America, this diversification benefit is offset. So, it’s not too surprising that with the volatility of the past year, the U.S. dollar has not been a good diversifier — the opposite in fact. Taking its place is gold, which does really well as a diversifier during periods of policy uncertainty.

Conclusion

We would say that bonds may not be as good a diversifier as during the previous decade, but they still do provide a reasonable amount. And given yields are now higher, bonds also have more of a potential contribution to overall performance. The good news is there are other sources of diversification from greater international allocations, alternatives, commodities and even the US dollar. It will really depend on what the next period of weakness looks like. If it is a period of economic weakness, bonds and USD may work best, while gold and international less so. Or if it is another flare up policy uncertainty, it could be the exact opposite.

Best to find diversification from a few key sources to best diversify your diversification.

The great Canadian disconnect

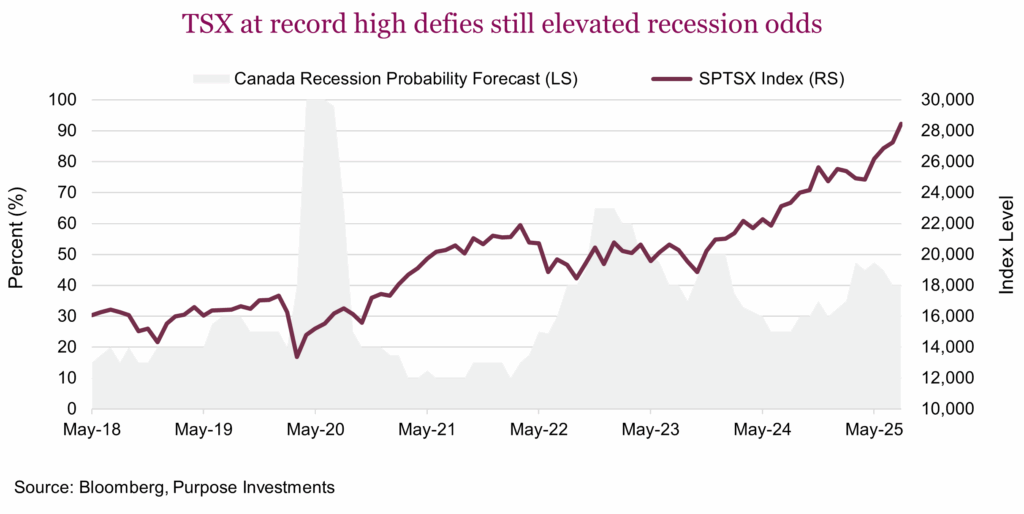

From an investment perspective, Canada presents a puzzling picture so far this year. On one hand, the stock market is enjoying significant gains, but on the other, the country’s economic health remains weak. The S&P/TSX Composite Index has risen approximately 17% year-to-date, better than many global markets; meanwhile the Canadian economy continues to limp along. This disconnect highlights that the market’s performance is less a reflection of a strong Canadian recovery and more a function of global commodity trends and data that has bested overly pessimistic expectations. The market is not the economy is a common saying, but the experience this year in Canada is especially true.

Canada’s economy contracted -1.6% annualized in Q2, the sharpest decline in GDP since the pandemic and worse than the -0.7% decline expected. This slowdown was primarily driven by weaker exports due to trade tariffs, slower local spending and ongoing issues with low productivity and lack of business investment. June marked the third straight monthly decline in GDP. None of these drivers appear to be turning the corner very quickly, which puts Q3 on a knife’s edge. The median forecast currently stands at just 0.2% with 8 of 19 economists expecting a negative Q3, underscoring the very real risk of a technical recession. The chart below illustrates the dramatic disconnect quite neatly. Recession risk currently stands at around 40% over the next twelve months, meanwhile the TSX is flying high. Typically, when recession risks are this elevated, the market shows some sense of caution or elevated risk aversion. Not so this year.

It’s not all gloom and doom — the story for consumers and the job market is somewhat mixed. Real time data from credit card transactions and service sector activity points towards some stabilization, but this is still a far cry from a robust reacceleration. StatsCan’s latest retail survey shows spending on essential consumer categories is holding up, but consumer spending is somewhat uneven across discretionary segments. The unemployment rate has climbed to 6.9%, the highest since the post-COVID recovery. While high, the unemployment rate has leveled off around the average levels seen between 2013 and 2016. July’s weak employment print (-40k jobs), while subject to Canada’s typical monthly volatility, does point continued signs of softening. The growth in average weekly earnings has also cooled, which reduces the pressure for inflation caused by higher wages but also signals a tightening pocketbook.

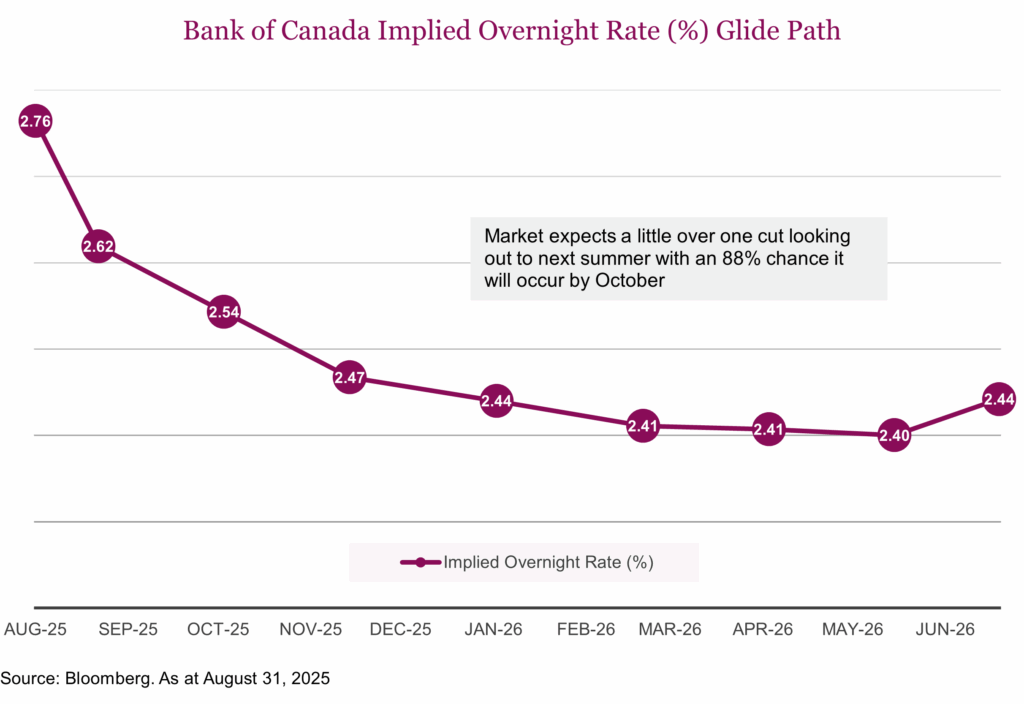

When it comes to monetary policy, inflation is really the only key variable. Overall, headline inflation is now below the Bank of Canada’s 2% target, but core inflation measures are still elevated around 2.5%. The good news is that the disinflationary trend should continue. The Bank of Canada has already cut the overnight lending rate 225 bps since last June. It’s been on hold since March, however the market has recently increased expectations that the Bank of Canada may cut rates again this year. The market is pricing in a little over one cut looking out to next summer, with the most likely timing coming this year. Despite this, business sentiment remains depressed, with the Business Outlook Survey revealing a lack of confidence impacting capital expenditures and hiring plans. There are some green shoots, but efforts to improve interprovincial trade, while positive, are not a complete fix for the problems facing the economy.

Perhaps the biggest problem remains the housing market, which used to be a key driver of growth. New home prices have been flat since early 2022 and are now starting to drift lower. Developers are struggling with a reality of overpriced units sitting and a reluctance to reprice. While lower interest rates should eventually help with affordability, the full impact of higher debt on households will make housing recovery slow and bumpy well into 2026. This sensitivity to household debt and a fragile housing market continues to be a key risk for the Canadian economy but the worst-case expectations have thus far failed to materialize.

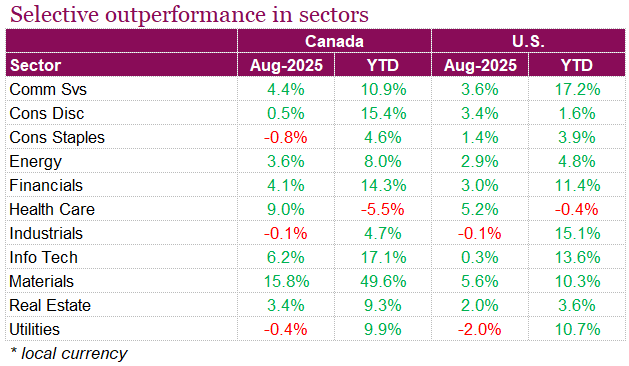

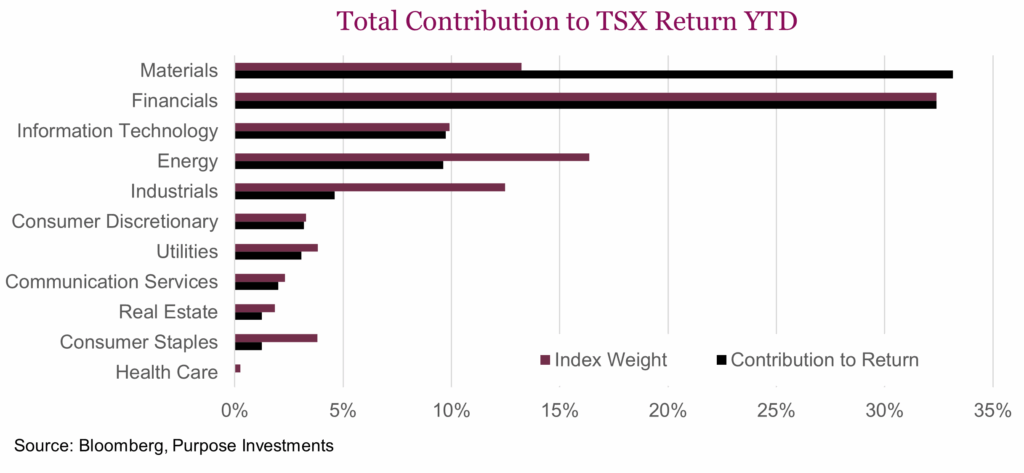

The outsized performance of the TSX this year, therefore, cannot be viewed as a sign of broad-based economic health. Its 17% gain is highly concentrated, with a significant portion attributed to the Materials (33%) and Financial (32%) sectors. Given the high index weight and strong returns across a number of banks this past week, Financials are contributing exactly what would be expected given their 32% weigh in the TSX. Miners are punching well above their weight, which has more than offset weaker contributions from Energy and Industrial sectors. In terms of what’s driving earnings, the majority of earning growth comes from the materials, energy, and financial sectors. Roughly 45% of the TSX’s Q3 earnings growth is expected to come from gold producers. Banks rallied on better than feared results: lower credit provisions, resilient capital markets revenue, and strong capital ratios. Loan growth is subdued, reflecting soft domestic demand, but the risk of serious credit losses is clearly receding and gradually easing, supporting household and business resilience. These sectors are either tied to global commodity prices or are benefiting from a “soft-landing” narrative rather than robust domestic activity. This reality underscores the key takeaway: while the Canadian stock market has been strong, it is not a good indicator for the domestic economy, which remains soft.

Looking ahead, a close eye must be kept on GDP prints to see if the negative Q2 and near-flat Q3 forecasts are confirmed, which would keep recession talk alive. This includes labour market trends, particularly the unemployment rate and wage growth, with an eye to lagging indicators which are important for gauging consumer health. Currently, we are underweight Canadian equities with the TSX now trading at 16.5x; still cheap compared to the U.S. but now somewhat expensive compared to the 10year average PE of 15x.

Ultimately, while Canada has surprised positively in the near term, the economy is not yet out of the woods. Structural imbalances, elevated household leverage, and external headwinds mean that a cautious outlook remains warranted especially for areas of the market that are domestically exposed.

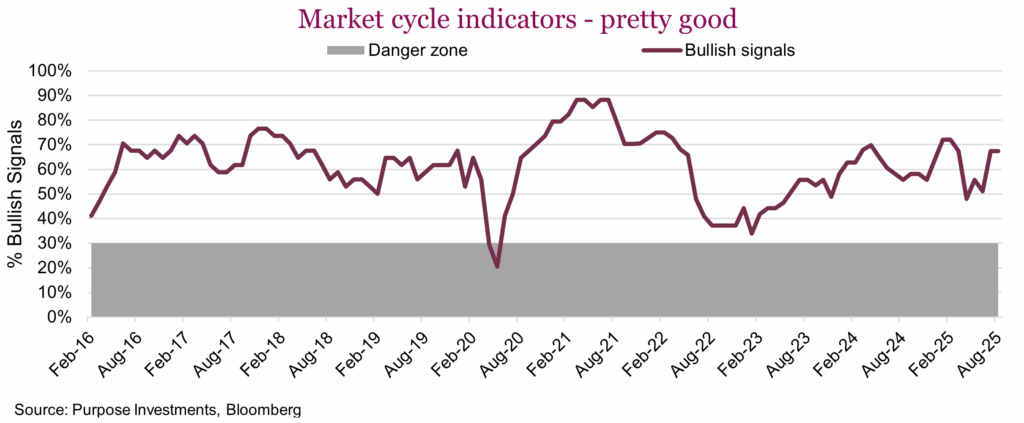

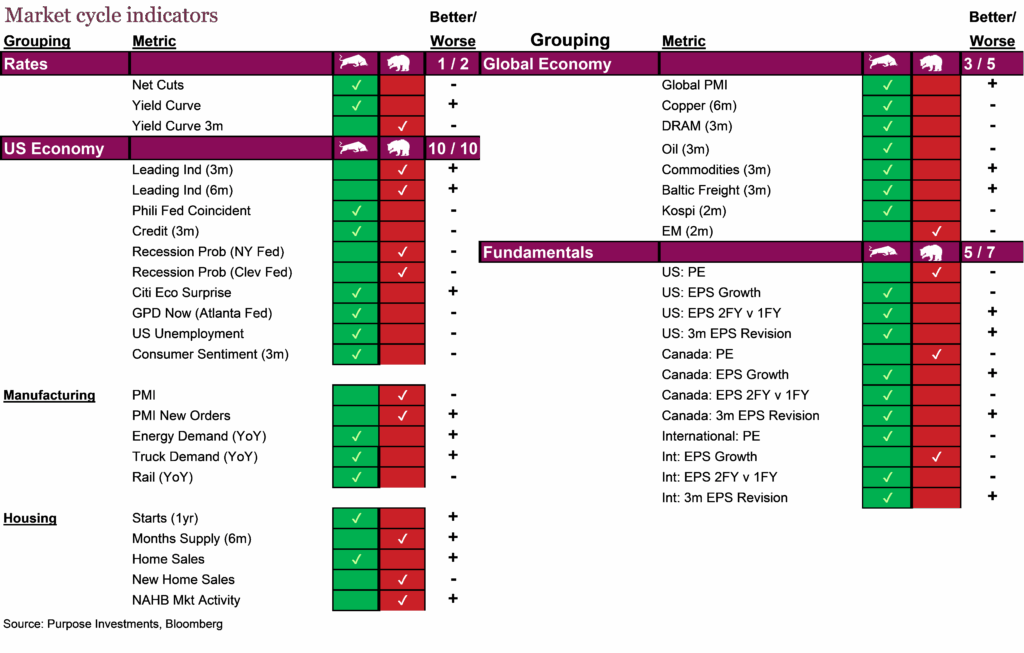

Market cycle and portfolio positioning

Market cycle indicators were flat at this time last month, but with a few moving pieces beneath the surface. The yield curve signals are rather flip floppy at the moment with short- and longer-term yields in the U.S. just about the same. The yield curve may be positively sloped, but it’s hard to notice with 3-month yields at 4.17 and 10-year at 4.22. On a positive note for the U.S. economy, housing saw some signs of improvement, as did overall energy demand. It does look like that slowdown we had been expecting later this year is gradually becoming a less probable event.

With the U.S. net up two signals, there were negatives elsewhere to get the total back to flat on the month. Emerging markets rolled over a bit after strong gains this year, which gave a bearish signal for global growth. We would not be too concerned given all the other global growth indicators are healthy. International EPS growth also slowed a bit but remains relatively stable overall.

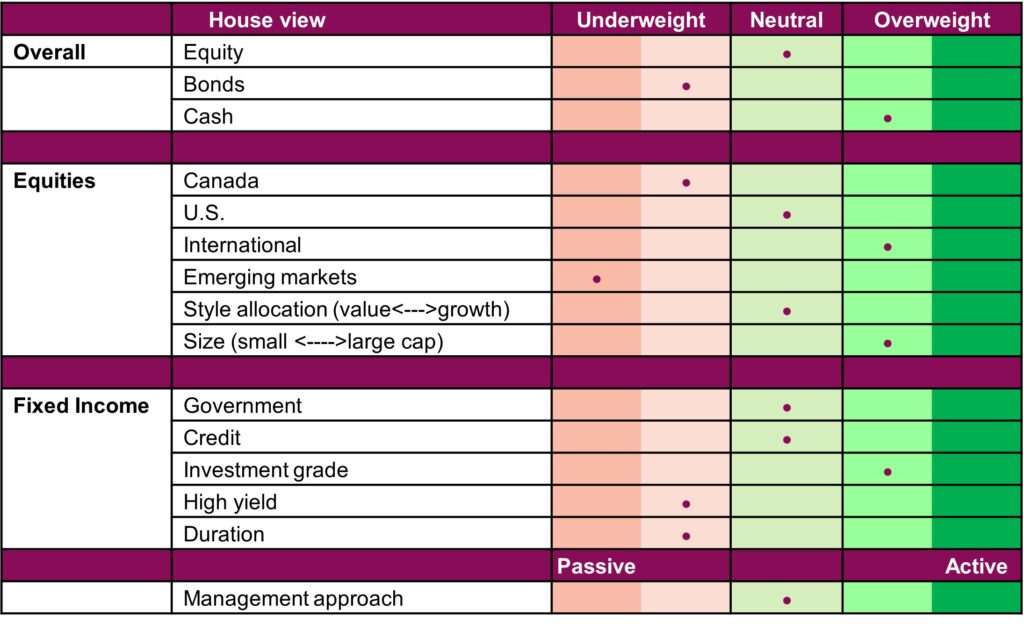

No changes to portfolio allocations over the past month — we believe profit is most often made in the sitting. More cash and diversifiers have us in a position where if a seasonal period of market weakness does arise, we have many options to be active. While this does have us slightly defensive in a market that keeps going up, better bond tilts, gold and international have compensated to make up the cash/defensive drag. It’s certainly been an interesting year so far, and more to go.

Portfolio positioning

Final note

2025 is far from a plain vanilla investment year. Policy uncertainty, erosion of central bank independence, fiscal spending going global, markets reaching highs, rising concerns over deficits, struggling housing markets, persistent inflation and decent earnings growth are a few of the highlights with one third of the year still to go. We are coming into a seasonal challenging period. Finding diverse sources of diversification remains prudent for portfolios with so many moving parts in the markets.