Investor Strategy

March 3, 2025

Playing defence

Sign up here to receive the Market Ethos by email.

Executive summary

- February funk

- The Trump put

- Europe’s market resurgence

- Market cycle & portfolio positioning

- Final thoughts

While markets have remained resilient, the concern is that softening economic and earnings momentum may weaken its fortitude. Could a big enough market drop reverse the tariff risk (aka the Trump put)? Maybe, but that is not going to be a pleasant experiment. In the meantime, defence appears to be the prudent tilt.

February funk

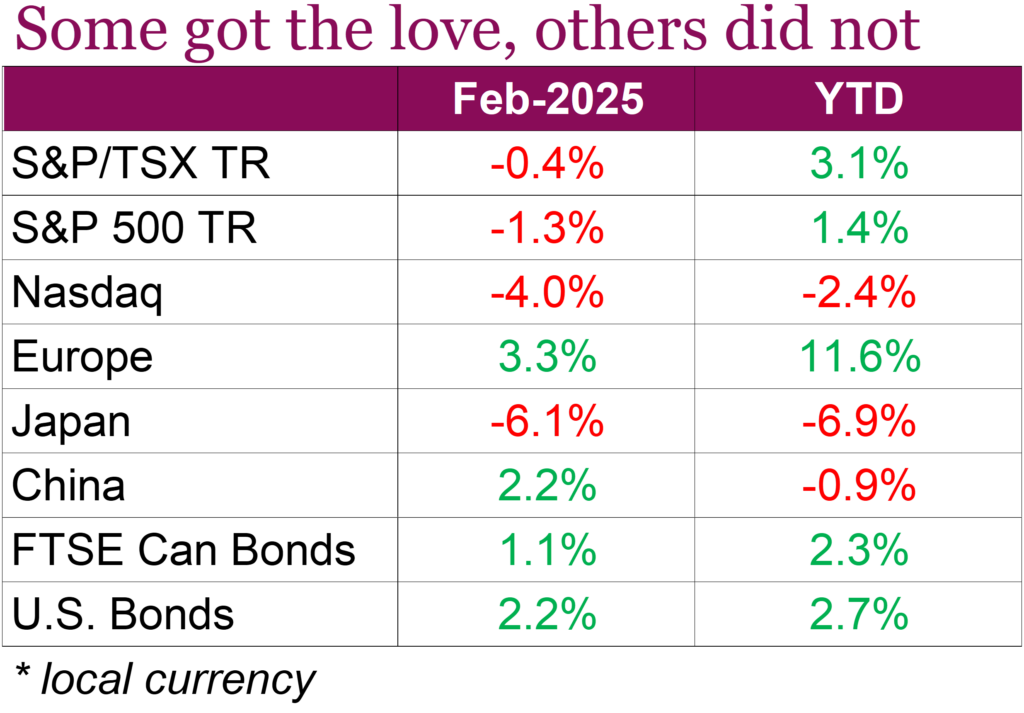

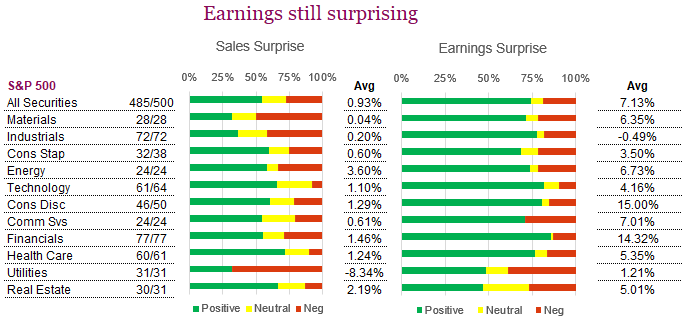

North American equity markets struggled in February as concerns of a global trade war sent investors fleeing to haven assets. The Nasdaq led losses with many of the Magnificent 7 names losing momentum amid slowing earnings growth and concerns over elevated valuations. On a total return basis, the index fell -3.9% in February and is down -2.3% YTD, with investors eyeing other opportunities after two years of stellar performance. Many of those Mag 7 names also dragged down the S&P 500 over the month, as the index finished with a total return of -1.3%, despite a relatively solid earnings season from the broader index. With 97% of S&P 500 companies having reported by the end of the month, 75% beat EPS expectations, and 63% exceeded revenue estimates. The blended (y/y) earnings growth rate stands at 18.2%, the highest since Q4 2021, significantly beating the initial 11.7% estimate from December.

Canadian equites fared better than their American counterparts in February, falling just -0.4% in total return. Despite tariff concerns, equities were helped by solid economic data which showed Canada’s economy growing at an annualized 2.6% in Q4, exceeding expectations due to strong household spending, exports, and business investment. The Bank of Canada’s (BoC) rate cuts boosted consumption, and the job market remains solid with inflation seemingly under control. Canadian inflation data showed consumer prices rising 1.9% YoY in January from 1.8% in December, in line with estimates. The increase was driven primarily by higher energy prices, while core inflation measures also increased to an average annual pace of 2.7%, though three-month averages declined. Economists remain divided on whether the BoC will cut rates or pause at its March 12 meeting, as the uncertainties of tariffs weigh on the economic outlook, pushing yields lower and leading the FTSE/TMX Bond Index to finish 1.1% higher for the month.

The notable exceptions to sluggish equity market returns in February came from Europe and Hong Kong. The Euro Stoxx 50 index rose 3.5% in February and is now up 11.9% YTD on a total return basis. European equities have outperformed the S&P 500 by over 14% on a total return basis since the beginning of December, as investors rotate away from U.S. equities. While the strong start to the year has been broad-based, the European banking sector has been one notable standout helped by upgraded consensus expectations for banks earnings. European equities have also been given a boost from defence stocks following increased military spending commitments from EU leaders. The Hang Seng was up 13.4% in February despite fears of U.S.-China economic decoupling, spurred by Trump’s new tariffs. The boost came after further stimulus measures were introduced and as optimism grows around the Chinese tech sector, particularly the new kid on the block, DeepSeek.

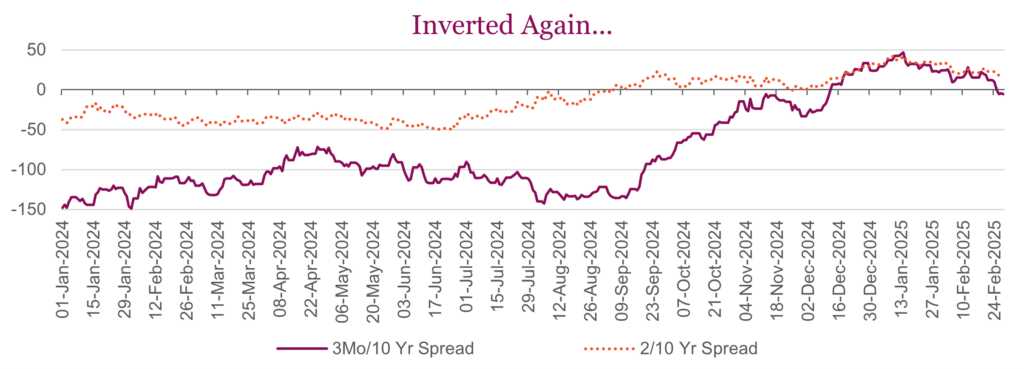

Still, investors remain on edge with both tariff and inflation concerns remaining front of mind. The U.S. Consumer Confidence Index dropped to 98.3 from 105.3 in January, marking the steepest decline since August 2021. The sudden drop came as a surprise given the strong job market and 2.3% GDP growth in Q4 2024, highlighting just how much the new administration’s policy changes have weighed on investors. These concerns pushed yields lower throughout the month, helping the US Aggregate bond index rise 2.2% in February and bringing its YTD gain to 2.74%. With the dramatic move in yields, we saw the re-emergence of one of the better recession indicators used by the Federal Reserve – and that is a negative spread between the 3-month and 10-year yield. However, the classic 2/10-year yield has remained positive.

The Trump put

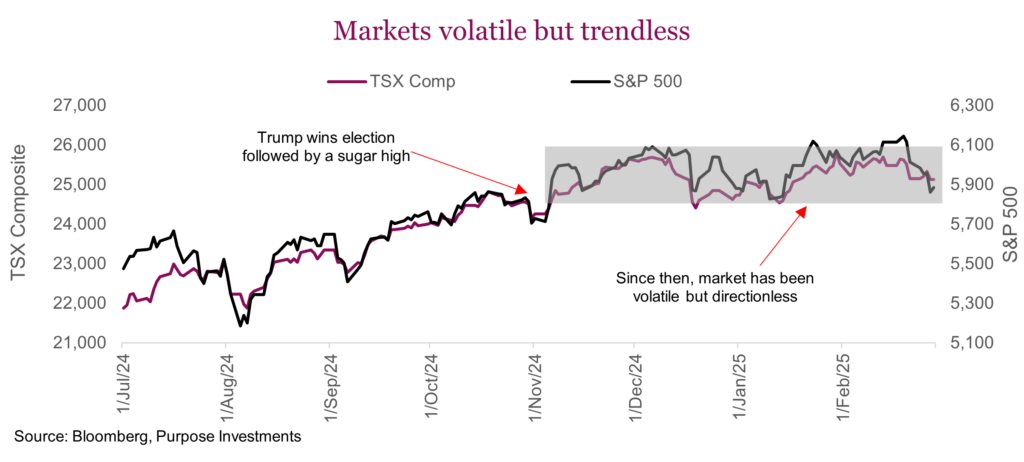

Following Trump’s election win, the markets rejoiced, partly fueled by the unwinding of market hedges and in anticipation of more market- friendly policies from the new administration. Unfortunately, like any “sugar high” it just doesn’t last and since cooling in December, the S&P 500 has been stuck in in a range around 6,000-6,100. This is an impressive feat in our opinion, given the avalanche of policy announcements or talk. Sure, it has caused markets to bounce around much more, but still within this range. Even the TSX clearly more at risk of an escalating tariff conflict — is within one good trading session of its all-time high. The word “resilient” is fitting.

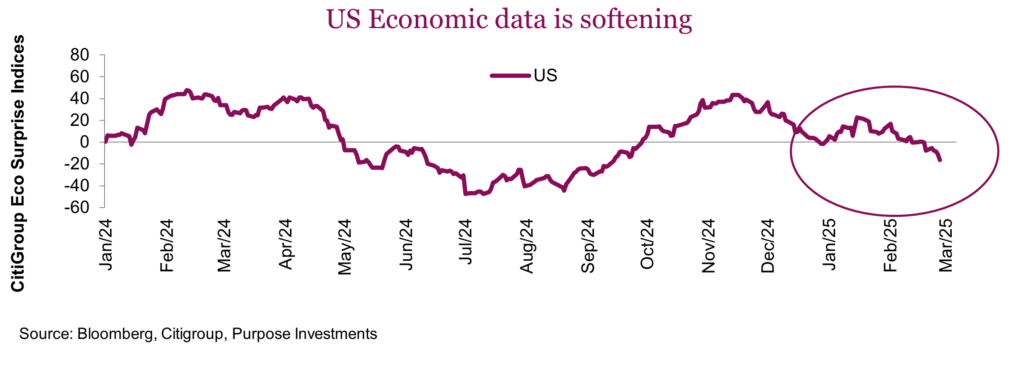

Helping the markets absorb all this headline noise without throwing a tantrum have been the economy and earnings. Economic momentum was decent as 2024 finished off — and it wasn’t just America, as the data picked up in many jurisdictions. This improving economic backdrop seemed to more than offset concerns over U.S. inflation, which has been reaccelerating for the past four months. A little more inflation is not hard to stomach when the economy is surprising to the upside, perhaps even justified. Meanwhile the fourth quarter earnings were decent, with the S&P posting about 10% earnings growth and 5% sales growth. Unfortunately, this support backdrop may be waning. Economic data has started to soften, notably for the U.S. that had been so impressive over the past couple quarters. Just look at 10-year Treasury yields that have fallen from a high of 4.8% in early January to 4.27%, even with inflation still ticking higher. Additional evidence of a softening U.S. economy is showing up in multiple areas, encapsulated in the CitiGroup Economic Surprise index. This captures how the economic data is coming out relative to consensus economist expectations. That descending line, well, it means negative surprises.

Earnings too are looking a bit squishy. 2025 and 2026 earnings estimates for the S&P 500 dipped lower during earnings season. That is the period where most companies are giving some level of guidance or comfort about the coming quarters. So, softening isn’t great. On a positive, the market is pricing in 10% earnings growth for 2025 and 12% for 2026. So perhaps some minor downward revisions are tolerable, as long as they stay minor.

If the supportive fundamental backdrop continues to falter, will the market remain so sanguine about the non-stop policy announcements and uncertainty? Policy risk (more every day it seems), economic growth momentum risk and some earnings risk, and it’s unlikely this market will stay in its 3-month trading range much longer.

But if the market weakens there could be some good news, enter the “Trump Put”. Many readers have likely heard of the “Fed Put”, or the more personalized versions depending on the Chair, such as the “Greenspan Put” or “Powell Put”. It is the widespread belief by market participants that if the economy or market falls too much, they (the Fed) will come to the rescue with more and more stimulus. The “put” part comes from the options market, as a put option can be structured to create portfolio insurance to limit the downside. Hence “Fed Put”.

President Trump appears to measure his success, or the success of policies, based on what the S&P or market is doing. In fact, during his first term at times when markets reacted negatively in response to policy, the policy was often adjusted or even reversed. We experienced a micro episode of this on the morning of February 3 after the Mexico and Canadian tariffs were signed into law over the weekend. This includes the Friday afternoon market slide when it appeared the executive order was certainly going to be signed on the weekend, and the market open on Monday when the S&P 500 dropped over 3% from 6,115 to 5,925 over a combined four hours of trading. And what happened next? Trump deferred the tariffs for a month and the market bounced back to over 6,000, recovering fully a few sessions later.

The question then becomes how much market weakness is required to see a pivot from the flow of policy announcements from the administration? Or for those options-savvy folks, where is the put strike price? Clearly an unknown, but the crux is that a drop in the market may well trigger a cooling of policy risk. Some policy reversals, no new market-unfriendly policy announcements, could well help market recover from weakness. Following the same line of logic, perhaps the rapid-fire onslaught of policy announcements was partially emboldened by a market that had proven resilient.

To be clear, we are not saying policy announcements or Trump can save or control the market. Earnings, the economy, confidence, rates, yields and policy all have an impact it’s cumulative. But if there is enough market weakness, for whatever reason, policy reversals or softening would likely be welcomed by the market. Even a holiday of new policy announcements would be nice.

If you are wondering what guardrails there are for the new U.S. administration, it may well be the market. One month done, 47 to go.

Europe’s market resurgence

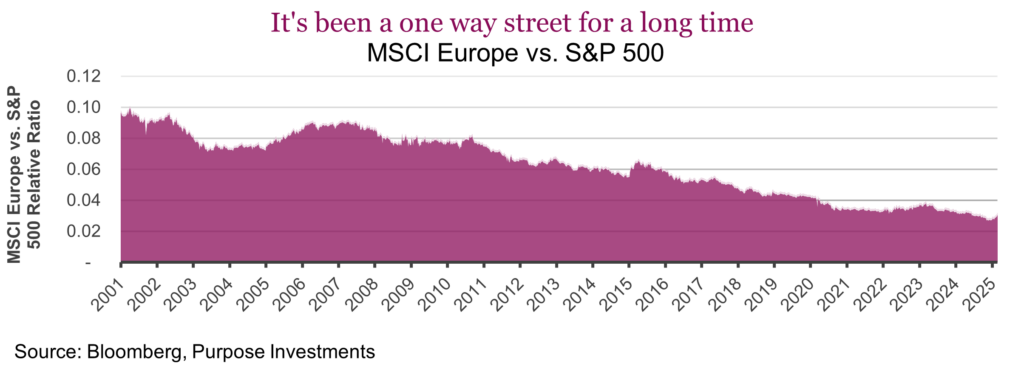

Two months into 2025, international equities are off to an impressive start. Leading the charge across developed markets is Germany (+13% YTD), with the rest of the European market not far behind. The MSCI Europe index is up 11% year-to-date in Canadian dollar terms. From our perspective, we can let out a relieved “it’s about time!” Throughout last year, we advocated for an overweight position in international equities. The thinking wasn’t wrong — just early. Investors are increasingly reassessing the “U.S. exceptionalism” thesis, with cracks forming along the AI-defined edges. As a result, there is growing interest in international diversification and the potential for higher returns outside of the U.S.

This renewed interest has been a long time coming, but two or three months do not make a trend. Above is a sobering chart showing the relative performance of the MSCI Europe versus the S&P 500 over the past 25 years. The recent outperformance barely registers after 18 years of underperformance. Being overweight in international equities is still a contrarian trade — it is far from crowded and one we believe has the potential to continue.

On a near-term basis, you could see some pullback. Weekly momentum of the relative trade is becoming slightly overbought, and a reversal is normal after such an extreme oversold level in Q4. The speed of Europe’s rebound has been remarkable. Since early December, the European advance has quickly narrowed the gap in trailing

one-year returns.

Developed markets, led by Europe, are showing renewed momentum. Several key factors contribute to this shift. Monetary policy in the Eurozone has become significantly more relaxed. The ECB has now cut its target rate 125 bps and is expected to continue to cut another three times this year. There is also a distinct possibility of peace or at least a ceasefire in Ukraine, which could pave the way for rebuilding efforts and an economic boost to the region. Additionally, Germany’s recent elections have resulted in a more pro-business government promising to revitalize economic growth, lower energy prices, and increase infrastructure spending. All in all, the economic news in the region has become more favourable.

Valuations remain key

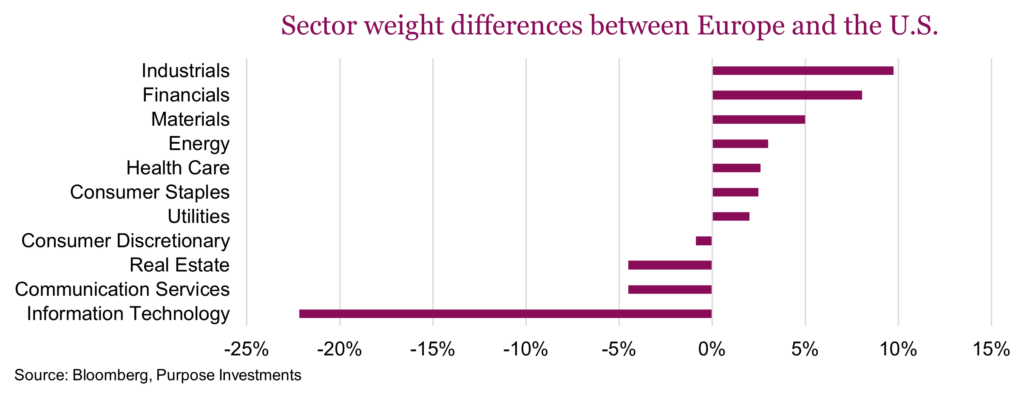

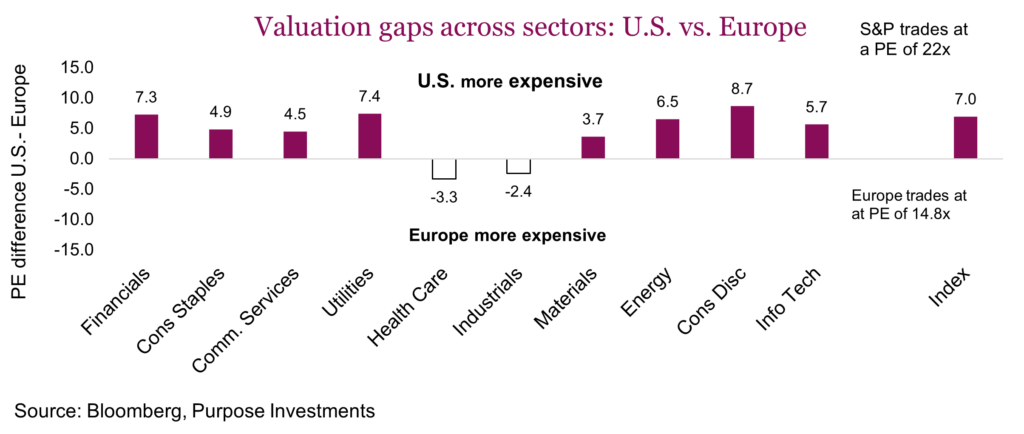

At just 14.8x estimated earnings, European valuations remain attractive compared to the S&P 500, which trades at 22.1x earnings — a 7.2-point premium. However, this is not an apples-to-apples comparison. Structural differences justify some of the valuation disparity. Europe has significantly less large-cap tech exposure (-20%) and more exposure to Financials (+8%), Industrials (+10%), and Materials (+5%). These are historically lower valuation multiple sectors and this relative sector tilt makes European markets more cyclical. More cyclical and trade implies closer ties to China and the global economy.

The chart below outlines the relative forward price-to-earnings ratios of the MSCI Europe Index and the S&P 500 across all sectors. The U.S. is more expensive in nearly every sector. The largest valuation gaps are in Financials (the largest sector in Europe), as well as Utilities and Energy. However, not all sectors follow this trend — Health Care and Industrials trade at a premium in Europe. Different industry dynamics are at play here. For instance, within the Industrial sector transportation stocks, which trade at a low P/E, are a much smaller weight compared to the U.S. Relative to the U.S. Europe is cheap, and relative to its own history Europe is still attractively valued, trading roughly in line with its 10-year median valuation, while the U.S. is trading at a substantial premium to its historical valuations. While lower growth expectations, investor sentiment, and structural economic factors do explain some of the gap, the magnitude of the valuation gap across most sectors remains extreme.

Earnings growth improving

Relative earnings growth expectations play a critical role in valuations. The U.S. already has decent earnings growth priced in, which helps justify its higher valuations. Meanwhile, international equities, led by Europe, are seeing earnings estimates improve. European earnings growth expectations have risen substantially, shifting from negative in 2024 to solid projected growth over the next few years. This narrowing earnings gap should drive further inflows into international equities.

Outlook

A weak start to 2025 for the U.S. bodes poorly for its full-year prospects, relative to global markets. Historically, the U.S. has outperformed the rest of the world in 24 of the last 35 years (70% of the time). However, in the six instances when the U.S. underperformed by this magnitude by the end of February, it never managed to reclaim the lead position by year-end.

The ongoing market rotation reflects growing interest in international equities, supported by attractive valuations, improving earnings estimates, and a clear sentiment shift. Risks remain, particularly potential trade tensions and tariff threats between the U.S. and Europe. However, we continue to believe in the positive outlook for international equities and the benefits of diversification.

Market cycle & portfolio positioning

We are living in a conditional world at the moment that is full of ‘ifs’. As of today, the global economy is doing rather well. There has been an uptick in global manufacturing activity with 10 of the 16 more important country PMI data surveys above 50, representing rising activity. This is roughly the highest reading since early 2022. The Canadian economy just posted a 2.6% growth rate for Q4, that brings the quarterly average to a respectable 2.4% for 2024.

The giant ‘IF’ of course is tariffs, timing, magnitude and breadth. If as draconian as the headlines imply, likely a Canadian recession and big blow to global growth/trade. If tempered, less of a negative impact. If delayed or softened more, then even less an impact. Many twists and turns lie ahead.

Let’s start with the good news: earnings revisions and growth have moved higher for international equities. We have written on the improving earnings growth for international equity markets a number of times over the past few months. While earnings growth still is slower than the U.S., international equities, notably in Europe, certainly are getting the most improved scorecard so far in 2025. Add in the low valuations and it is compelling, and that is helping drive international markets higher so far this year. In case you hadn’t noticed, the Euro Stoxx 50 is up 11% year-to-date compared to a paltry 1% for the TSX and 0% for S&P.

Offsetting this good news for market cyclical indicators is softness in the U.S. economic data. Momentum in housing appears to be waning, one of the more cyclical components of the economy. The other cyclical component, manufacturing, has improved. Although we are not celebrating this as it would appear many companies have been getting in orders ahead of potential tariffs. This may have front-loaded manufacturing activity in Q4 and so far in Q1. The broad Citigroup economic surprise index has turned negative and consumer sentiment too.

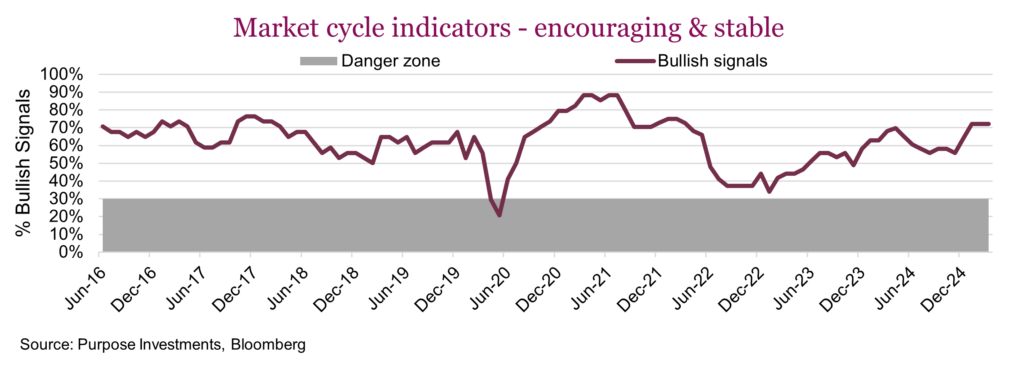

Sentiment is always hard to capture and often this ‘soft’ data from surveys does not follow into the hard data. Sometimes people say one thing but do another, in case you hadn’t noticed. This is most evident this week in the American Association of Individual Investors (AAII). This survey, dating back to 1986, asks investors about their expected direction of the S&P over the next six months. This week, 60.6% were bearish, an extreme reading. Only 6 times (out of 1,960 weekly surveys or 0.3%) have investors been this bearish.

Normally, this is a contrarian indicator. In other words, when everyone is bearish it has historically been a buying opportunity. The problem is all those past extreme bearish readings came with markets already down 10, 20, 30 or even 40%. When this past week’s survey was conducted, the S&P 500 was down a mere -2% from its all-time high. Everyone is unhappy and bearish but nobody’s selling. This is one weird market.

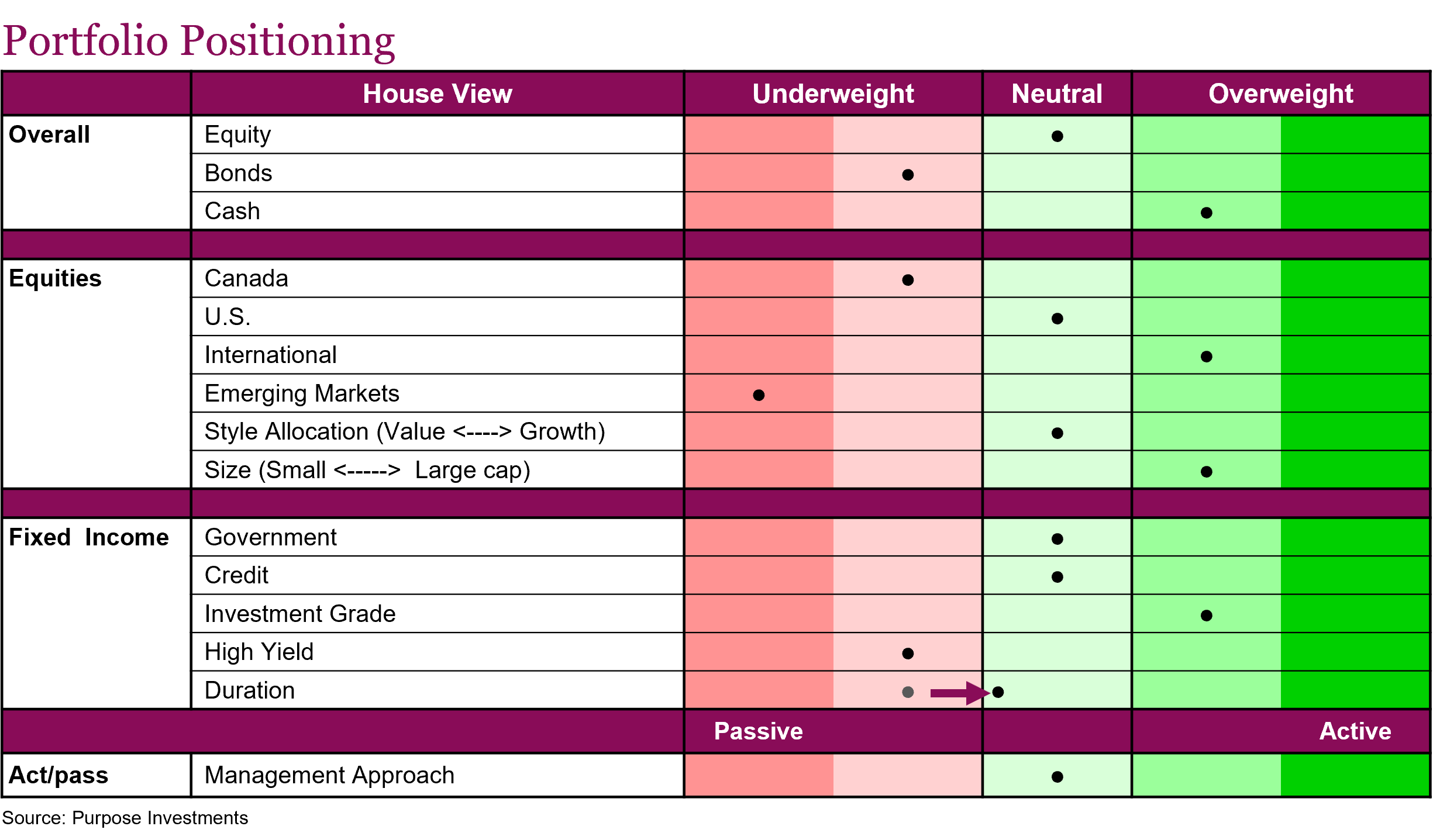

At the overall portfolio level, there were recent changes, as we increased our bond position and decreased the portfolio’s sensitivity to broad market movements by trimming exposure to long-only equity securities. This does tilt us a little bit more defensive. While equities are neutral, our positioning among equities has a defensive tilt. This includes more equal weight for U.S. exposure. Bit more on the value side and mild overweight international.

On the bond side, we remain a bit underweight (despite adding) with a tilt towards higher credit quality. Duration is at the higher end of our historical range, as we believe yields will come down further on softening economic momentum. Additional defence comes from our diversifiers that includes volatility management, alternative yield and gold exposure.

Higher cash is earmarked to be opportunistic should some market weakness develop.

Final note

2025 is a noisy year, which will likely have many twists and turns. The next big one has occurred as tariff implementation returns for a second attempt. While markets have remained resilient, the concern is that softening economic and earnings momentum may weaken its fortitude. Could a big enough market drop reverse the tariff risk (aka the Trump put)? Maybe, but that is not going to be a pleasant experiment. In the meantime, defence appears to be the prudent tilt. Perhaps the Eagles defence winning the championship over the Chiefs high-powered offense is applicable to markets in 2025. We will see.