Investor Strategy

3 February 2026

Same themes to start the year

Sign up here to receive the Investor Strategy by email.

- A year of news in January

- The K is getting wider

- Gold: greedy or fearful

- Dollar doldrums

- Market cycle & portfolio positioning

- Final note

A year of news in January

Investors in January faced many of the same concerns that defined 2025, including geopolitical tensions, tariff threats, and changing interest rate expectations from the Fed. Add to that, a globally inspiring and courageous Davos speech by our PM, Iran protests and a violent government crackdown, increased U.S. tariff threats towards many from Europe to Canada, a reverse ICE operation in Venezuela (moving a Venezuelan national from their country to America), nationwide protests against ICE action across the U.S., a brief carry trade scare due to rising yields in Japan, the naming of a new Fed Chair, and a terrible winter storm. It’s been a dizzying start to the year.

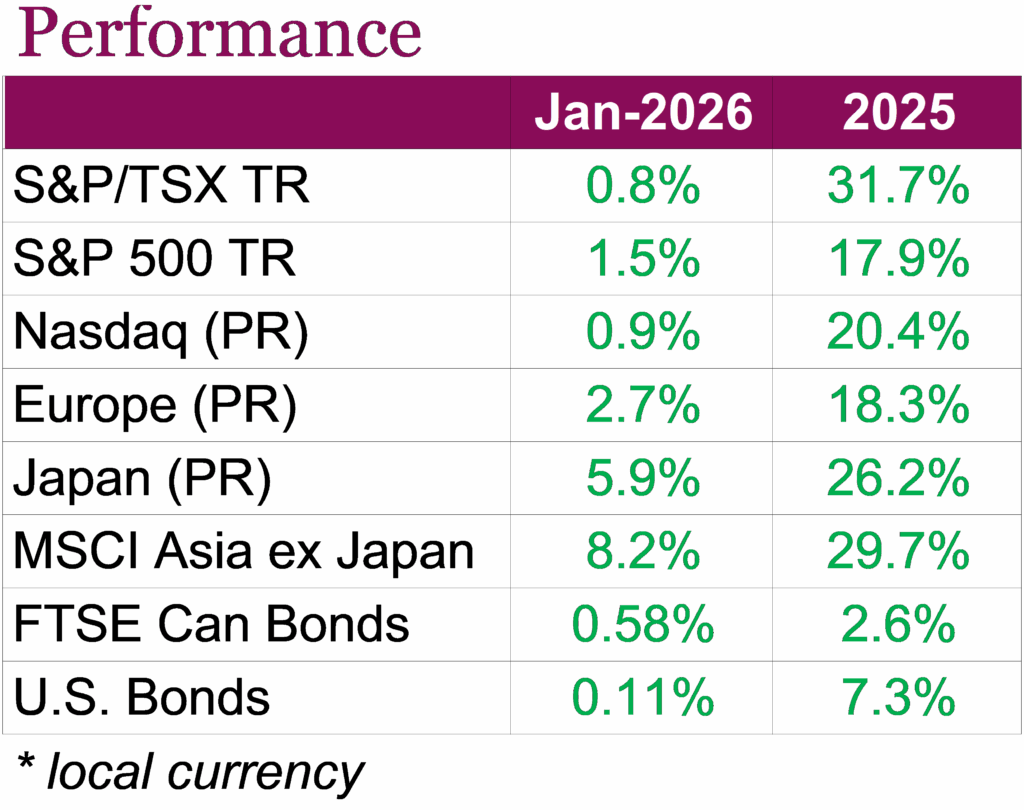

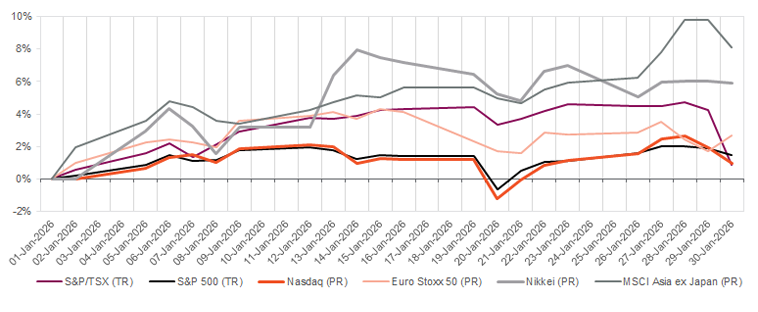

Despite the steady stream of headlines, markets proved resilient and most major asset classes finished the month higher. In Canada, the S&P/TSX Composite rose +0.8% on a total return basis, while U.S. markets continued to grind higher, with the S&P 500 gaining +1.5% and the Nasdaq up +0.9%. Bonds provided stability, with the FTSE TMX Universe Bond index up 0.58%, helped by stabilizing interest rate expectations, while U.S. aggregate bond indices posted a more modest 0.11%. Commodities stood out as well, particularly precious metals, with gold and silver delivering double-digit monthly returns. This came as investors sought safety amid uncertainty, although that proved not to be without its own volatility towards the end of the month.

The fate of Canadian equities was largely tied to commodities throughout the month, largely due to the market’s heavier exposure to resources. Rising commodity prices lifted the TSX by more than 4.5% at one point during the month, but those gains did a quick U-turn on the final trading day as mining and materials shares sold off, leaving only a modest gain for January. Meanwhile, domestic economic data pointed to slowing momentum, with manufacturing and export-oriented sectors pressured by weaker global trade and ongoing tariff uncertainty. Estimates now suggest that Canada’s economy may have contracted modestly in the fourth quarter. Against this backdrop, the Bank of Canada held its policy rate steady at 2.25%, emphasizing patience and acknowledging that growth remains uneven and sensitive to trade uncertainty. That uncertainty once again took center stage after Canada penned a new trade deal with China and Mark Carney spoke of the need to reduce dependence on the U.S. ahead of a review of the CUSMA.

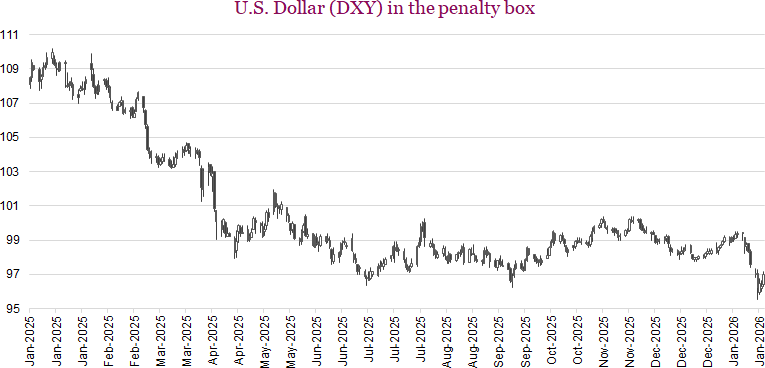

While the U.S. also experienced volatility, equities benefited from steady economic conditions and supportive corporate fundamentals. So far, Q4 earnings have been positive, with roughly three-quarters of companies beating profit expectations and blended earnings growth tracking near double digits, led by large tech companies. The Fed maintained its policy rate at 3.50%–3.75%, signaling a data-dependent, “wait-and-see” approach as inflation continues remain a concern. While discussions around future Fed leadership and policy direction added uncertainty, markets mostly focused on resilient growth and corporate profitability. Still, markets appear skeptical of the U.S., which we can see by the decline in the dollar. The dollar’s weakness comes amid rising fiscal deficits and increased policy uncertainty. The dollar did, however, get a boost towards the end of the month following the nomination of Kevin Warsh as the next Fed chair, a choice viewed as hawkish on inflation and supportive of tighter monetary policy. Expectations that rates could remain higher for longer briefly lifted Treasury yields and provided near-term support for the dollar, underscoring how sensitive currency markets remain to shifts in policy expectations.

Clearly, this somewhat fearless market does not seem bothered in the least by headline news. That will likely change soon but in the meantime we enjoy a very confident market. January is often a peculiar month for markets, from a performance perspective. There are often large systematic inflows following the calendar year end, which is a positive. Redeploying tax-loss harvesting proceeds back into the market, often helps fuel a rally in lower-quality names. Large portfolio rebalancing also takes place.

Despite a rather painful last day of the month, 2026 is off to a good start.

The K is getting wider

The U.S. economy, in aggregate, is doing pretty well. Once the delayed Q4 data is reported, their economy will have likely grown a bit over 2% in real terms for 2025. Forecasts for 2026 have been trending higher to 2.6%. Sure, job growth has slowed to a crawl and housing activity remains dormant. But corporate investment in AI infrastructure, improving PMI manufacturing surveys and a positive fiscal impulse from the big beautiful bill all help temper those concerns. Add it up, and you have an economy that is growing with barely a whisper of recession risk.

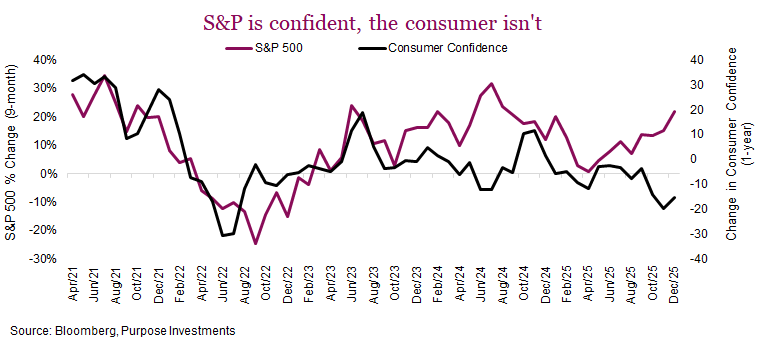

We highlighted the term ‘in aggregate’ because one of the building imbalances is this “K-shaped economy”. The K term denotes how part of the economy, namely corporations, better off consumers and asset owners, are doing very well. That is the upper arm of the K. But the lower arm is not doing well. This is comprised of lower-income consumers, those that don’t own assets or those who don’t feel the wealth effect of an S&P hitting all-time highs. The lower arm of the K also feels the impact of inflation harder, as cost of living is rising faster than wages. This disparity helps explain why the S&P 500 reaching new highs is taking place with consumer confidence going in the other direction. Historically, changes in the market correlate strongly with consumer confidence (+0.5 over past 25 years). But with the K widening, this is not the case given confidence is an equal voting survey, not weighted by wealth.

This may not be a big issue today. For starters, the U.S. economy, and most economies for that matter, have always been somewhat K shaped. This isn’t new but it appears to have become a wider K. The risk is that the lower income cohort of consumer spending weakens enough to drag down the aggregate. This has not occurred yet, looking at consumer spending, but cracks are increasingly showing up.

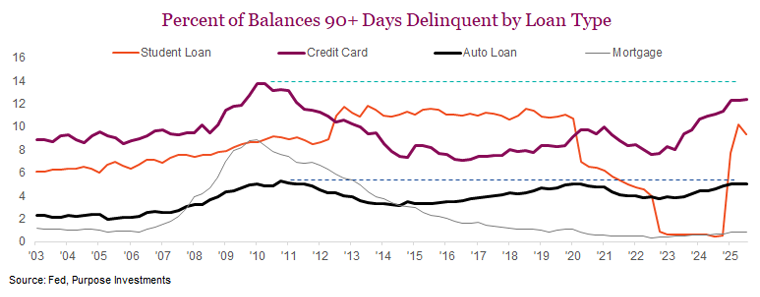

Total outstanding credit card debt has remained flat for two years now. That may sound encouraging but not adding on credit debt is a sign of weakness for a consumer, especially the U.S. consumer. Aggregate payrolls, which measures total employment times wages, has softened slightly. In normal economic times, this grows at about 5% but it has dipped down to 4.2% over the past few months. This tends to soften heading into recessions. Perhaps most concerning for the lower-income consumer is delinquencies.

It is ok to ignore student loans as policy has flip-flopped on this one. But credit card balances over 90 days delinquent, and auto loans, are nearing levels not seen since the financial crisis. Auto loans too. Clearly the lower-end consumer is having trouble making ends meet. However, there are some positives as we head into 2026. The big, beautiful bill does have a number of provisions for lower-income consumers, while gasoline prices have dipped below $3/gallon for the first time since 2021.

This isn’t a crisis today as the wealthier consumer is still in great shape. But if the K continues to widen, the lower end may start to drag down the aggregate. And as goes the U.S. consumer, so goes the economy.

Gold: greedy or fearful

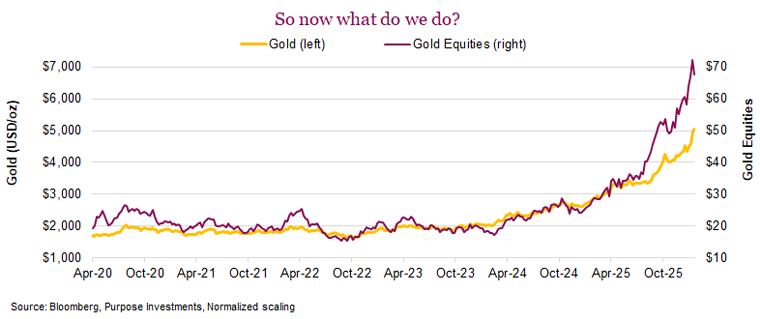

Who doesn’t love gold? As the yellow metal breached $5,000/oz, up 160% over the past two years with miners up almost 300%, the only folks who don’t love gold are those that don’t own any. For those that own some, either bullion or miners, they simply wish they had owned more. But what do you do with an investment that has gone up this much? It does come down to how greedy or fearful you are.

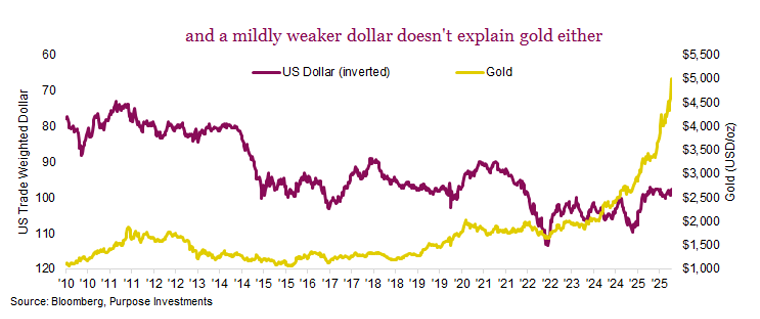

The positive gold narrative is widely known and often parroted as a rationale for an allocation. U.S dollar debasement, central banks allocating more to gold, elevated inflation risk, concern over sustainability of fiat currencies with rising debt levels, eroding trust in the system given policy uncertainty, etc. All legit reasons, but then there is price: How much are you paying? You can’t value gold, there is no discounted cashflow, there is no PE ratio. It is simply 1 / T where T is trust in the system. Trust has gone down over the past couple years, so gold goes up.

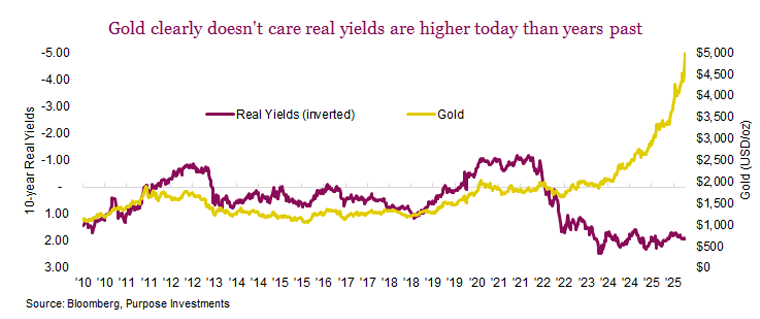

This is both good news and bad news for gold. It means it can go much higher, but it also can go much lower. Two factors that historically moved inversely with gold are real yields and the U.S. dollar. Lower real yields mean the opportunity cost of holding gold (with no yield) is less. But guess what, real yields are higher today than they have been over the past few decades, which should be negative for gold. A higher U.S. dollar, given gold is a real asset that is quoted in USD, should have a lower gold price and a weaker USD implies a higher gold price. No argument here and the USD has softened, but nowhere near enough to translate to $5k bullion prices.

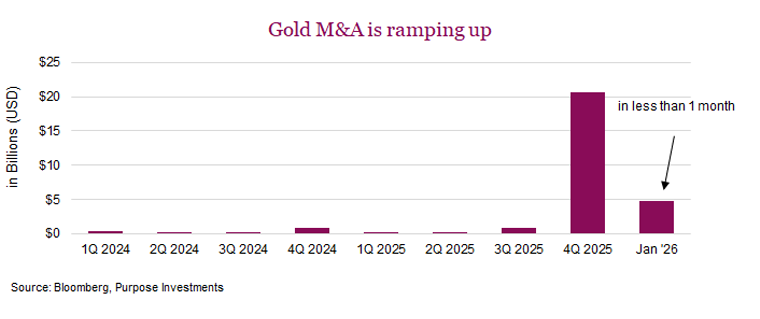

So where does that leave us? This gold parabolic run is now likely 100% a momentum trade, fundamentals have been long left behind. That doesn’t mean the run is over, but it does make any gold allocation increasingly volatile (for the record, this was written before gold fell nearly -10% in the last couple days of January). This enthusiasm has also spread to other metals from silver to palladium and even to copper. M&A is picking up too. So far in 2026, less than a month into the new year, $4.7 billion of deals have been announced globally. The total for all of 2025 was $22 billion, which was extremely back-end loaded. Gold companies are generating a lot of free cash flow and have been raising money like crazy. Historically, once flush with cash, gold companies either poke holes in the earth or buy one another. It is their nature.

For us, fear has become larger than greed. This certainly appears to be a good time to right size positions or even harvest some gains. Additionally, the price action last week, with gold up +$171 on Tuesday, +$237 on Wednesday, then opening Thursday to rally up $200 to $5,596/oz, then dropping down to $5,100/oz to finish roughly flat at $5,396, was dizzying. This was followed by a $481 drop on Friday down to below $5,000/oz, highlighting the volatility of a pure momentum-driven market.

Dollar doldrums

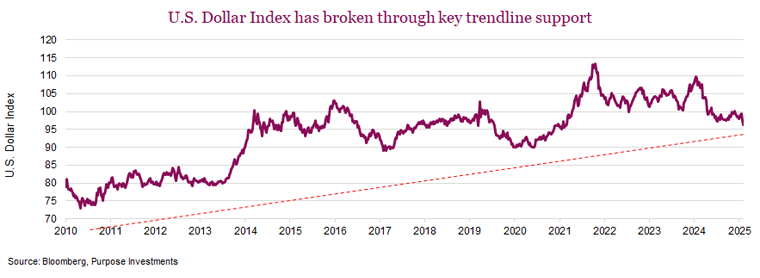

In January, the U.S. dollar broke through a 15-year trendline, the last precipice of support in what has been a record run. After declining 10% last year, the U.S. dollar is off to a rocky start to the year so far. It is becoming clear that the long uptrend has ended. Through a technical lens, the 200-month simple moving average at 92.25 for the DXY Index is now in play and the medium-term bias remains lower. Despite higher rates and a stronger economy than most, the world is past peak dollar appetite. This move marks a potential sea change for global capital allocators. From DIY stock portfolios to the all-in-one ETFs that are very popular, dollar-denominated assets play an important part in most Canadian portfolios.

You would think a government that has long held a strong dollar policy would have some concern. The reaction, at least publicly, is conflicting. President Trump has no issue and thinks the value of the dollar is great. Conversely, Treasury Secretary Scott Bessent attempted to restore some semblance of stability, noting that the U.S. still has a strong dollar policy. All this is just talk. We would rather listen to the markets, and what they are telling us. At this moment in time of profound uncertainty, especially on the geopolitical front, it is clear that the market is removing some of the safe haven status of the U.S. dollar.

Less of a haven – There is an interesting devaluation at play. You have legitimate concerns over Fed independence and the potential for further easing from a monetary policy standpoint is a surge in precious metals. This reduced safe-haven Treasury demand is an evolving, but growing risk. Other forces at play include dollar appetite destruction from foreign investors, increased hedging activity, and a general rotation away from U.S. assets.

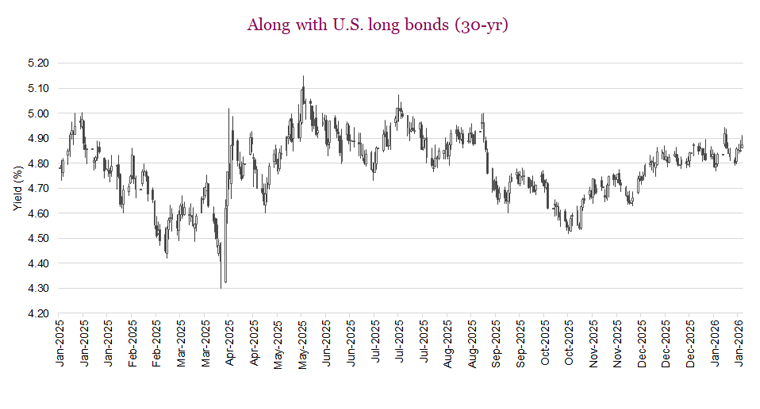

Rates – Interest rate differentials are a primary factor for currency valuation. While U.S. rates are still the highest out of most global peers, the anticipated direction is for a narrowing of the interest rate premium for U.S. Treasuries. U.S. rates are likely to come down, making them less attractive compared to other option. The Treasury market remains immensely important given the size and liquidity, however demand at the margin may not be as strong.

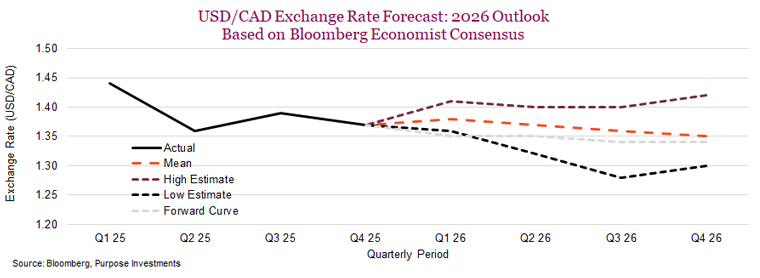

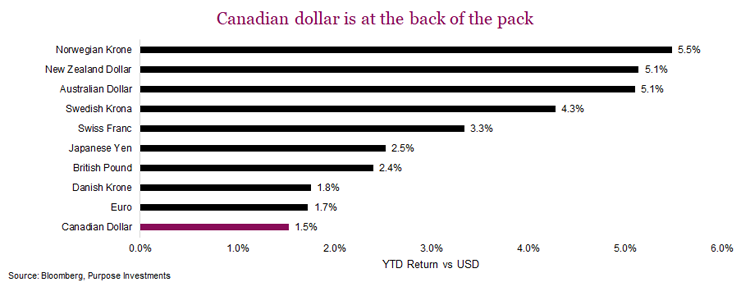

Canadian dollar – The Canadian dollar has strengthened, up over one and half percent versus the U.S. dollar YTD. The Loonie, now at $0.0.7404 (as at January 29), has recovered modestly from November lows of near $0.7072 CAD/USD. Consensus forecasts anticipated a gradual CAD appreciation over 2026 as shown in the chart below. Interestingly, at current levels the Canadian dollar is already trading roughly in line with year-end targets. The upside from here is possible but not widely anticipated.

While strong in isolation this year, compared to the other G10 currencies, the loonie is lagging, reflecting a uniquely Canadian paradox. It is uniquely vulnerable among major currencies thanks to a number of key risks. Chief among them are questions around the critical trade relationship with the U.S. and the upcoming USMCA review in July. Canada currently benefits from exemptions on USMCA-compatible exports, however there will be difficult months ahead as both sides puff up their chests during negotiations.

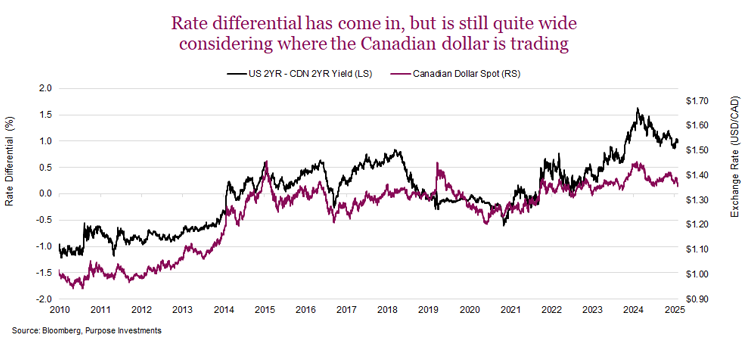

Besides trade uncertainty, there is also the possibility of a Venezuelan oil resurgence in coming years that could threaten to at least partially displace Canadian exports to the U.S. Domestically, the Bank of Canada is holding rates steady, noting that US policy uncertainty is making it very difficult to predict the direction and timing of the next change in the policy rate. This uncertainty, coupled with a stable but limping economy, leaves Canada very much at risk to the whims of U.S. policy in the near future. This is despite Carney’s recent attempts to diversify and open further trade relationships focused on fiscal stimulus. Rates in Canada are steady, and differentials have fallen from recent peaks, but remain historically elevated. U.S. 2-year rates are nearly 1.0% higher than Canada’s.

Currency positioning

Hedges – Within our multi-asset portfolios, we remain partially hedged. Specifically, we have hedged roughly half of the U.S. equity and fixed income exposure. Should we see a sharp move in the loonie, we would reassess our conviction on whether maintaining the hedge makes sense, specifically from a cost standpoint as hedging can be expensive and detract from returns.

Seek outperformance driven by currency tailwinds – Certain asset classes benefit from a weaker U.S. dollar. We continue to believe that maintaining gold exposure is beneficial, however volatility has been picking up and sentiment is somewhat stretched. Another asset class that benefits is emerging markets. The MSCI Emerging Markets index rose 28% in 2025 and is marking the best start for EM equites since 2012, up 9.7% YTD. There are a number of factors behind emerging market strength, and a weaker dollar is one of them.

The path forward will not be a straight line. Policy pivots from the ECB or interventions from Japan will create “switchbacks” in volatility, but the broader trajectory is clear. The dollar is historically expensive, and its dominance is being tested. The dollar’s decline won’t be a straight line, and the volatility creates both risk and opportunity. Success will belong to those who adapt and don’t treat currency as just an afterthought.

Market cycle & portfolio positioning

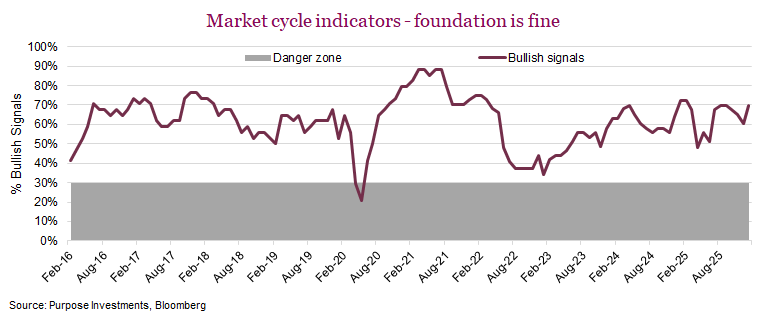

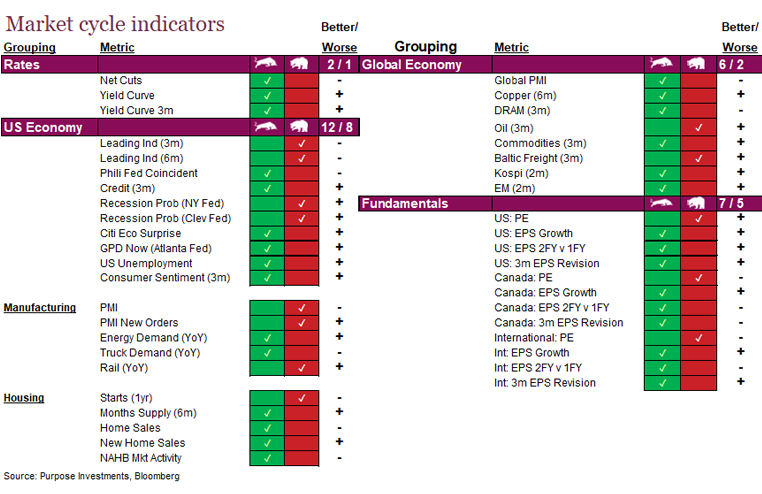

The theme so far in 2026 is a continuation of the trends in late 2025. The economic data has continued to improve a bit, inflation remains decent and markets seem fearless. The foundation remains relatively stable with some improvement more on the U.S. economic front. Economist surveys asking if they expect a recession in the next year have continued to see a lower and lower probability across major global economies.

Market cycle indicators ticked a bit higher over the past month. This was driven by a steepening of the yield curve over the past three months. On the U.S. economic front, consumer sentiment moved higher over the past three months, still low but moving in the positive direction. Energy demand improved, a sign of transport demand improving. Global economic signals were stable as were fundamentals.

No changes to positioning. There have been some good debates and a number of ideas analyzed, but we continue to come back to liking our current positioning. Paraphrasing Jesse Livermore – profit comes from patience, sitting tight with profitable positions rather than constantly trading or overthinking.

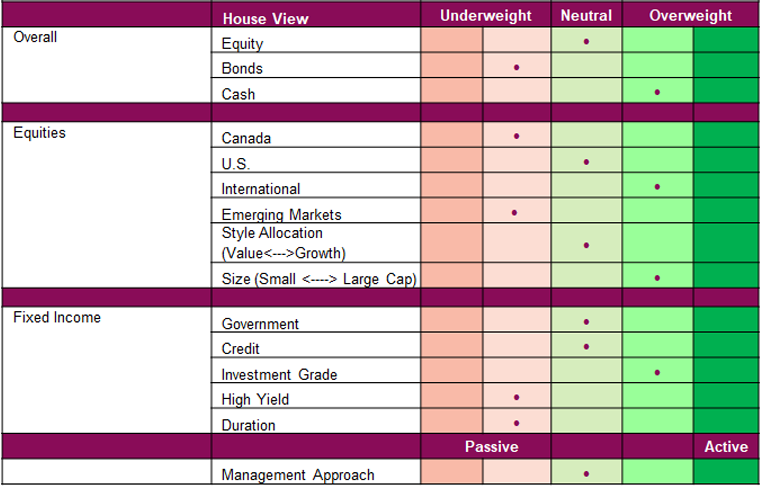

Portfolio positioning

Final note

The drop in gold on Friday, leading to a big drop for the TSX, is certainly a biggie and highlights the risk of a purely momentum-driven market for gold. Could this rattle the confidence of the markets? Perhaps. More likely it is a consolidation after such a strong climb. On the positive, the underlying foundation remains healthy and if the market pulls back enough could create an opportunity. For now, we remain tilted defensively.