Market Ethos

November 24, 2025

AI’s wild ride

Sign up here to receive the Market Ethos by email.

Great innovations have pretty much always led to bubbles. The standard historical list includes railways, electricity, the automobile, radio, TVs, computers, wireless and of course that internet bubble of the late 1990s. But you don’t need to go that far back as smaller bubbles have occurred in shale oil production, housing, and even Mary Jane (hint, became legal in Canada in October 2018). Artificial intelligence (AI) certainly fits the mold, and it may be a BIG one because it is a BIG innovation.

Narrowing the historical field to innovation bubbles, there is a generalized path. The new technology creates a large amount of displacement, ushering in a ‘new paradigm’ that will change the world. This is followed by a boom then euphoria as fear of missing out (FOMO) increasingly dominates investor behaviour. Some cracks in the extent of the new paradigm arise, leading to big up and down swings. Then it all unravels, and the bubble pops.

It is kind of rubbish though. The duration of bubbles can range from months to more than a decade, and the speed and height of the rise vary widely. Some bubbles lift up the entire economy, then let it down in the end triggering some sort of recession. Others don’t, and really have no broader economic impact.

Here are some questions and thoughts on bubbles and AI:

Q: Is AI a bubble?

A:Yes

The narrative is certainly strong enough. Price gains are an interesting one which actually is very different than in the late 90s. The dotcom bubble had tons of pure plays and IPOs, that would jump 50, 100, 150%. One argument that AI isn’t a bubble or near its peak is the lack of pure play companies. That will change with OpenAI’s IPO. But this bubble may have grown within already very large tech companies, masking its rise.

There is no lack of grandiose projections – such as OpenAI committing to $300B of cloud services from Oracle, who is estimated to have $25 billon in cloud revenue in 2025 (that would be a 12x). This is partially financed by a $100B investment by Nvidia in OpenAI, some solid circular financing. One argument this isn’t a bubble is that the capex spending had been largely driven by existing cashflow from companies. But that is changing quickly as debt and other financing is becoming more common. Morgan Stanley projects $2.9 trillion of capex on data centers over the next four years, with half coming from tech company spending and the other half from private credit, bond issuance, asset back securitization and private equity.

Here are some fun numbers. Estimates from Morgan Stanley have AI infrastructure spending of $2.9 trillion over the next four years. According to ChatGPT (ironically), hyperscale data centers enjoy operating margins in the high teens. If we say 20% operating margin and 20% tax, to generate a 20% ROI in four years’ time on a $2.9 trillion spend, you would need about an extra $3.6 trillion in revenue by 2028. That is $440/year from every person on earth.

There is already a high level of retail participation as just about everybody is already very long this bubble. We see a lot of advisor models, and one of the more common themes is a high U.S. equity weight. And this weight is certainly highly tilted to names or strategies that are geared to the AI spend.

Q: Are we in the boom or euphoric phase?

A: This is the question that matters most and nobody knows.

Our current view is we are past the initial boom phase and likely in the euphoric period given many of the points above. However, this phase can last a long time and there are certainly more tailwinds today than headwinds. As users of various AI-enabled tools, we continue to increasingly find use cases that enhance our workflow. In fact, we are already paying more than the $440/year. This trend will continue even if/when the bubble deflates.

Q: What does this phase potentially look like?

A: It will be exciting.

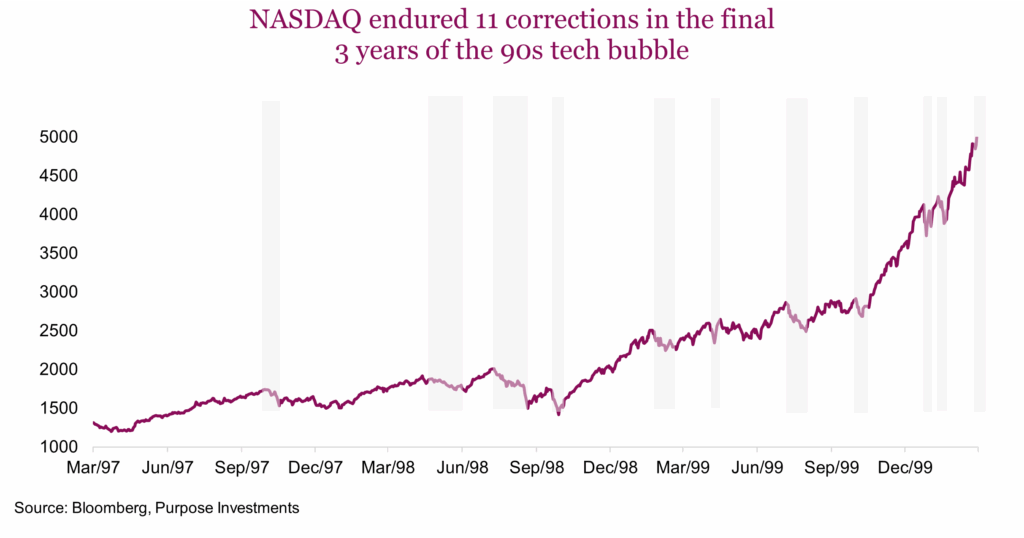

During the last three years of the 1990s tech bubble, the NASDAQ rose over 300%. But it also endured 11 corrections measured by drops of greater than 10%. That is almost four corrections per year. This AI bubble is different, perhaps with fewer pure plays it will be less volatile. Or perhaps it’s bigger so the swings will be bigger. But we would expect to see big swings, up and down, as enthusiasm rises and wanes. There is simply not enough clarity on the path forward, to provide much stability.

We are positive on this space, and we love the tools. That said, $2.9 trillion in data centers gives us pause. If that much compute is truly required, we believe they will find more efficient models as that lift may prove too much. For now, though, the capex boom is real.

One fear we do have is a learned response from large cap technology companies. If a large tech company missed the smart phone revolution, they were punished by the market (like Microsoft, or BlackBerry). If they missed the technology innovation moving towards the cloud (Cisco), they were punished by the market. The end result is with AI, large cap tech companies will view not going ‘all-in’ as a greater risk than spending billions.

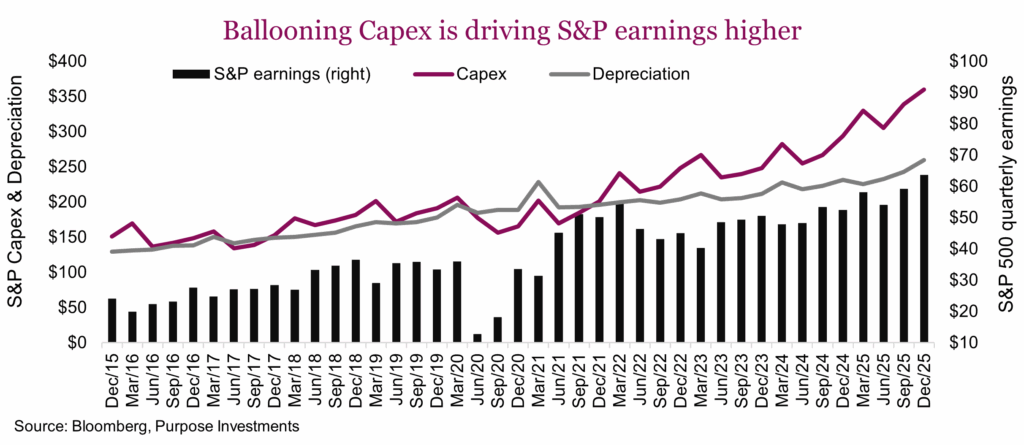

Nobody knows if the spend will have the ROI, but we do know the spending is happening now. And this kind of spending is great for markets and the economy. The following chart is S&P 500 constituent company capex (corporate spending) and depreciation, plotted alongside overall S&P 500 earnings. That capex line is going to keep rising faster and given depreciation is trailing, earnings will continue to enjoy an AI super charge. This is even more amplified if just looking at earnings from Information Technology and Industrials.

Capex spendings is great for corporate earnings as it carries a strong multiplier effect. Given what looks like limitless capital for AI-related spending, this really bodes well for overall market earnings growth and for the economy — even if other areas like labour or trade soften.

Adoption of AI across corporations also continues to ramp up, with many exploring how to use the evolving tools to improve workflow and enhance productivity. Simply put, more and more companies and people are using the services. This certainly puts us in the camp that, while the euphoric phase may have begun, it likely will have legs.

Q: What could pop the bubble?

A: Any number of things.

Recessions can quickly alter risk appetites and capex budgets, but we don’t see that as a near-term risk. Lower availability of capital would prove problematic, although there’s not much sign of that today. If capex doesn’t generate enough of a return, valuations in these tech giants that carry very high weights in the market would be crushed. Is a cutting age data center today destined to be legacy in five years? Or if you try and charge to make an economic profit, will a competitor undercut with ever lower price points to take market share?

Final thoughts

The euphoric phase is akin to a bucking bronco, just to bring back a rodeo reference. Given there are just so many unknowns, the bucking will be driven by oscillating levels of enthusiasm. Fortunately, we believe the potential bubble-ending scenarios or risks are far enough out, meaning this phase could have legs. So, in the meantime, this bubble will likely continue to inflate. But we would not be surprised to see increasing frequency of market corrections.