Market Ethos

October 27, 2025

China’s FOMO moment

Sign up here to receive the Market Ethos by email.

A few years ago, headlines abounded calling China ‘uninvestable’. It wasn’t just headlines — many famous market prognosticators and portfolio managers echoed the sentiment. The popularity of strategies ‘ex China’ increased in demand. There were many sound factors that contributed to this consensus view. Deflationary pressures due to overcapacity, regulatory crackdowns and a collapse in the property sector topped the list. Along with fear over an increasingly polarized world.

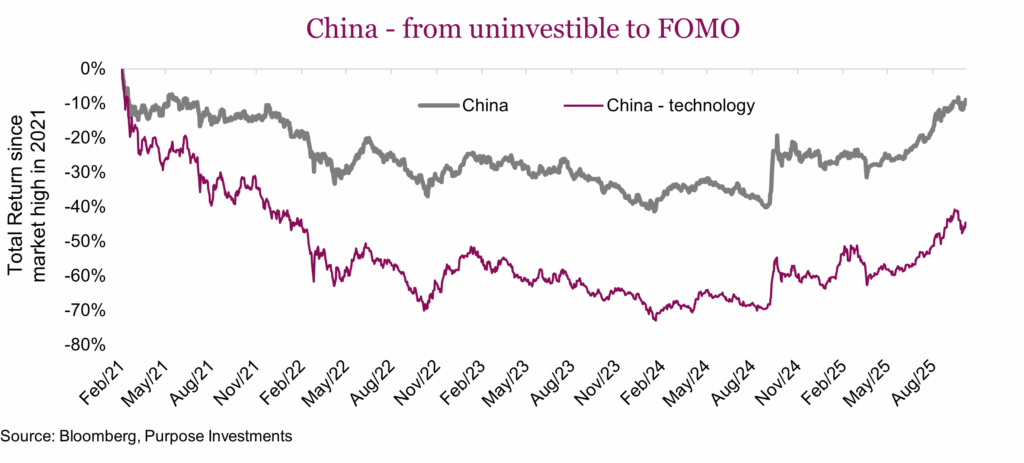

The pain in China’s equity market was apparent. After outsized positive returns in 2020, peaking in early 2021, China’s equity market tumbled over the next three years, bottoming in early 2024 — the drop was -47%. China tech sector, based on a popular China technology ETF, fell 74% during this period. This cumulated in bringing the valuation of the Chinese equity market, based on the Bloomberg China equity index, down to below 10x earnings while global equities traded at 17x. A hefty discount for any emerging market.

But since bottoming in early 2024, the Chinese equity market has been on a tear, up +47%. And those calling it ‘uninvestible’ have largely gone silent as investors have been coming back to this $19 trillion dollar equity market (including Hong Kong) that sits atop the world’s second-largest economy. So, is it all smooth sailing ahead? Hardly, but it’s certainly more constructive.

The Chinese equity market has historically been very volatile, not just because of the underlying companies but also thanks to varying investor interest from both domestic investors and foreign investment. This is a bit of a generalization but a number of years ago, Chinese investors flocked to equities which drove their market higher. Stats on the number of brokerage accounts opened each month was a metric of this rising risk appetite for equities. But when it collapsed into a bear market in 2015, capital went elsewhere, namely to real estate. When that collapsed after phenomenal gains in 2021-23, investors went elsewhere, including gold. But now it seems equities are back, with the caveat that change in investor appetite certainly adds to volatility.

Demographics and debt are certainly still sizeable risks. No question that due to previous policies and immigration, China has a rapidly aging population and pretty high debt levels. The property crisis, caused by speculation, overbuilding and debt accumulation, which started a few years ago, isn’t over. However, is a crisis that is over three years old still a crisis? Certainly, companies that were going to fail have already done so which reduces the risk of new market moving events.

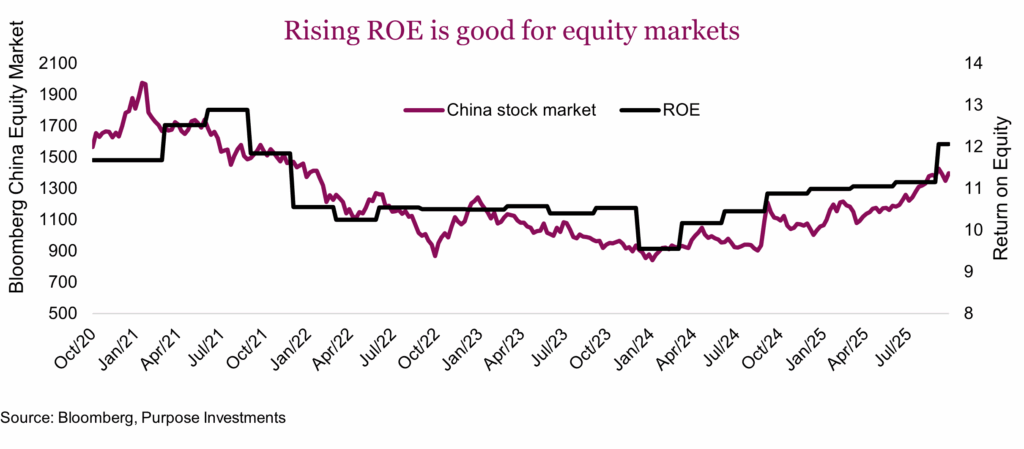

Despite these headwinds, there are some very material tailwinds of late helping this recovery rally in China’s equity market. Perhaps one of the most positive has been recent policies labeled ‘Anti-involution’ which requires some understanding of how China’s economy operates. It is more influenced by centralized initiatives. One of the more interesting analogies came from a research provider that focuses on China, referring it to a ‘hunger games’ approach. Leadership determines an industry they would like to develop, and directives are given to provinces to foster said industry. As a result, companies in the industry pop up all over the country, often too many of them. This leads to overcapacity but as time progresses, clear winners rise up. The industry consolidates as many can’t compete, and the best model(s) become the last one(s) standing, often global leaders.

EVs is a good example. In 2018 there were an estimated 500+ EV companies registered in China (Source: ChatGPT). This was whittled down to less than 50 by 2024 as the survival of the fittest process continued. The upside is it fosters the creation of globally competitive companies. The downside is it creates too much capacity during the process and likely destroys a lot of investment capital along the journey. This process has been evident in many other industries in China.

Anti-involution, which is a new direction started in 2024, is attempting to tackle overcapacity to better balance growth, innovation and sustainability. By reducing excessive competition, the policy is attempting to help promote pricing power through consolidation. For equity markets this is more friendly and has already started to lift return on equity.

Then there is artificial intelligence. Safe to say the U.S. is currently the leader in AI, however China is clearly in second place. And if it really comes down to electricity generation to drive data centers, China certainly knows how to build capacity in things rather quickly. The 3 Gorges dam, largest in the world, required resettlement of 1.2 million people. In North America we have trouble building pipelines. Hard to say which is the better way, though it probably depends on whether you are one of the 1.2 million who had to move. Preference aside, China has the lead in faster building, sometimes to their detriment with overcapacity.

Final thoughts

Based on the TD weekly fund flow report, China has attracted about $38B in flows during the past 3-months. To put that into context, that was 15% of global equity flows, with the U.S. attracting $105B. 15% of global flows is certainly evidence that China has shed the ‘uninvestible’ label. And perhaps investors are instead starting to feel a little FOMO (fear of missing out).