Market Ethos

9 March 2026

Diversification gone awry

Sign up here to receive the Market Ethos by email.

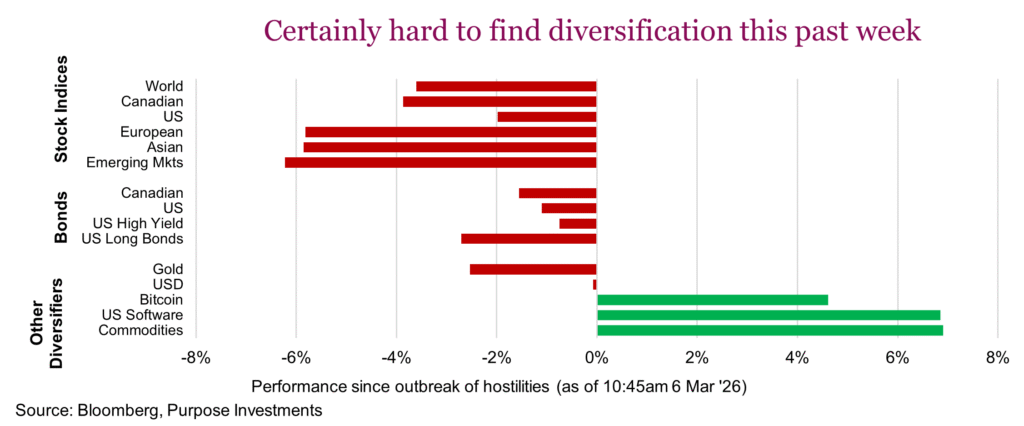

One would think that if markets sell off due to a material rise in geopolitical risk (outbreak of war between U.S./Israel and Iran), gold should be a good diversifier. That was clearly not the case this past week. Bonds weren’t so great either. But riding to the rescue of portfolios is bitcoin and software stocks — that certainly is not following the traditional script. And of course, commodities thanks to a huge rise in oil prices.

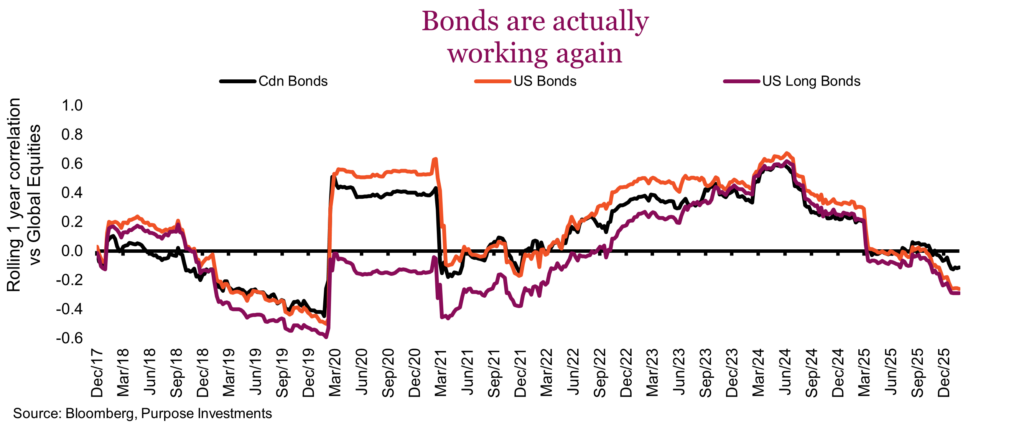

It isn’t just this past week that portfolio diversification has been more challenging. Everyone remembers 2022/23 when the bond/equity correlation became much more positive than previous years. Making the market drop of 2022 much more painful. Bond / equity correlations remained strong positive into 2024, but nobody minded as both equities and bonds were moving higher in price. Funny that.

While bonds have not helped much this past week, we would point out their correlation to equities has been falling. That is good news, and certainly a vast improvement from 2022/23. International equities, while strongly correlated, given they are part of global equities, have seen their correlations fall a bit too.

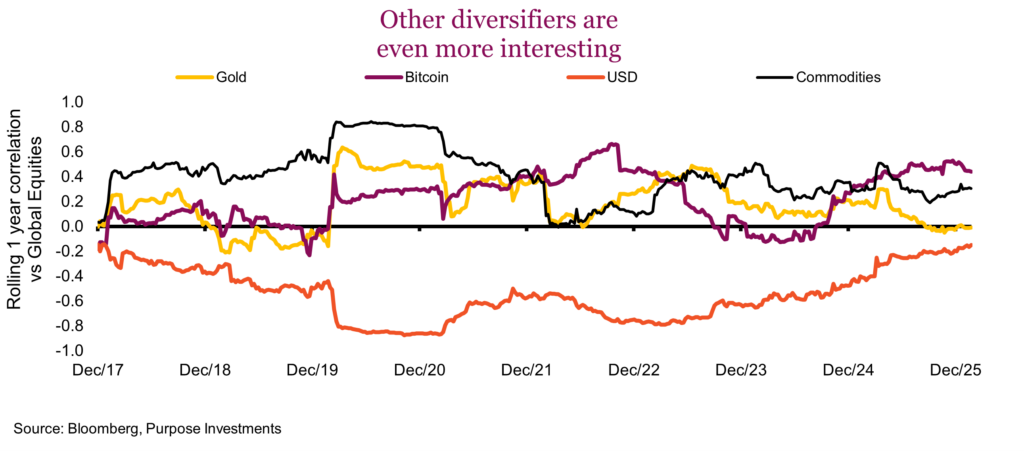

The other unique diversifiers are perhaps even more interesting. For many years U.S. dollar exposure has been a good diversifier for Canadian investors. From a correlation perspective this has been diminishing lately. Bitcoin, gold and commodities all generally have positive correlations to global equities, but are certainly on the lower side.

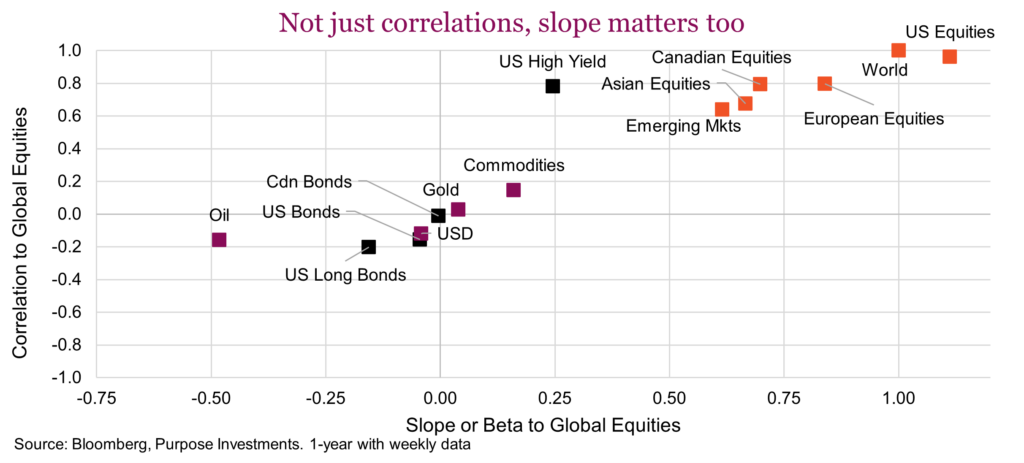

Correlations just tell one part of the story, the average relative direction. The other part is the degree of the move. The following scatter chart is a basket of asset class categories plotted with correlation to global equities on the y-axis and slope on the x-axis. For example, U.S. high yield is strongly correlated to equities, but the slope is much lower. That means the direction will often be the same but high yield will move much less. This helps diversification.

This is just one week of market weakness that once again highlights the need to really think about portfolios construction, namely diversified defense. With the COVID correction in 2020, bonds worked well after liquidity was restored, as did the U.S. dollar. Then came the inflation correction of 2022 — bonds sucked, gold did well, as well as more exotic income strategies that were less interest rate-sensitive. The Liberation Day tariff-induced correction saw different defensive strategies work best. Simple fact, these markets require multiple types of defense as corrections have become less atypical.

We were joking in the opening highlighting bitcoin and software as diversifiers this past week. The math adds up, given during this week that most things went down they went up. But don’t read too much into this, they went up because they had already fallen SO MUCH. Bitcoin was over $120k in October and had fallen down to low $60ks. U.S. software based on one of the more popular ETFs had fallen from over $115 to below $80.

Final thoughts

This market is fragile and the sudden ramp of geopolitical risk is clearly being felt. Bombing campaigns can end as quickly as they begin, but risks are now high. While markets have fallen, we’re still not anywhere near correction territory. We do wonder though if markets fall more, does the TACO playbook apply to armed conflicts or is it just tariffs? For now, we’re staying a bit defensive and most importantly we have a diversified defense within portfolios. We combine our core bond positions with gold, and higher cash. This allows options to act should parts of the market become too oversold. Never a dull moment.