Market Ethos

July 14, 2025

Dividends are back, but exposure matters

Sign up here to receive the Market Ethos by email.

What’s not to love about dividend-focused investing? Over the past thirty years, the dividend factor has outperformed the broader index (DJ Canada Select Dividend index vs TSX), with less volatility — not as much up market capture, but much less down-market capture. Add steady cash flow in the form of dividends, which enjoy some preferential tax treatment (aka less tax) than many other income sources. Or, add in the fact that dividends, paid from nominal earnings, have a VERY long history of outpacing inflation, enabling dividend-focus investing to help financial plans reduce the risk of inflation on purchasing power.

Oh right, what’s not to love is that dividends underperformed the broader market by a decent amount in 2022 and 2023, just by a sliver in 2024 and roughly tied in 2025. The reason for this underperformance, even in the down market of 2022, was largely the result of rising yields. Higher yields of the past few years contrast with falling yields of the past three decades. Higher yields have created a market where you can find yield just about anywhere — cash, GICs, government bonds, credit, lots of yield enhancing strategies, etc. There is simply lots more on the yield menu than in years past, so dividends have not enjoyed the relentless inflows compared to the past decades.

There is good news though. Bond yields have become rangebound, which we believe will persist given the higher elasticity of yield demand. And perhaps the best news is that short term rates are falling which may start to entice the hordes of money that were diverted into cash vehicles back to other yield destinations such as the dividend factor.

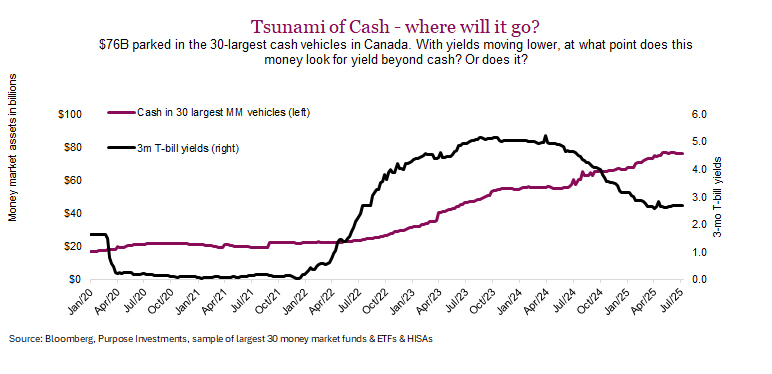

The chart above tracks assets in the 30-largest money market funds/ETFs in Canada, so it is not an all-encompassing number as it excludes so many other near cash options. However, it can provide insights into the trend, and since short term T-bill yields dropped below 3%, it seems the money has stopped flowing into cash (flat purple line in past few months). It is a leap of logic to imply cash is going to be reallocated to dividend-paying equities, as equities certainly have a much different risk profile. However, even if cash just stops hovering up new capital from peoples’ savings, that money may start to show up in dividend strategies again.

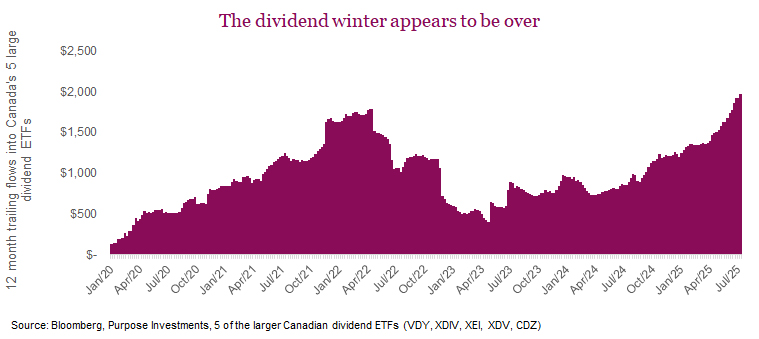

This trend appears to have started and accelerated in 2025; money is flowing into the dividend factor. Tracking five of the largest ETFs available in Canada, trailing 12-month flows dried to a trickle in 2023 as yields rose and cash was the go-to asset class. But inflows improved a bit in 2024 and then really accelerated in 2025. Dividends are back!!

Here comes the issue though, the dividend space has become more challenging. The inconvenient truth for anyone managing or investing in dividend- focused strategies is that all those years of falling yields and steady or relentless inflows were the golden age. It helped support dividend payers in times of trouble, making capital for these companies relatively cheap and easy to access. As a result, it lifted all boats. It didn’t matter how your portfolio was constructed or managed, just as long as you were capturing the dividend factor.

Now other things appear to be driving performance more and more. With higher costs of capital, debt or financial leverage has become a factor of greater importance. Operational leverage too, geographic exposure, economic cyclicality of the business and of course, interest rate sensitivity. These factors have always mattered, but their influence on performance appears to be rising in importance.

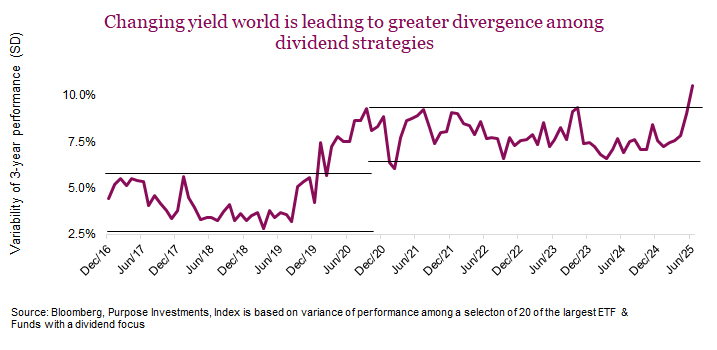

One way this is showing up is in the divergence among dividend strategies. In the 2010s, the performance difference between top quartile and bottom quartile was not that wide. Again, it didn’t matter how you were getting exposure to dividends, you just wanted some exposure. But in the 2020s, the divergence in performance among dividend strategies has been increasing. We believe this is because other factors are having an increasing impact on performance, and this reveals the differences across strategies.

The chart below is the standard deviation of 3-year rolling performance among 20 of the largest dividend-focused ETFs and funds available in Canada. An important consideration is the Covid market volatility of 2020, as we had a bit less conviction of this trend as long as that year was still in the 3-year rolling number. However, it has rolled off the back of the 3-year variance among dividend strategies, and it is still rising. It now matters more how you get exposure to dividends.

The challenge is: If you agree that other factors are increasingly important among dividend strategies, which factors are good or bad going forward? Do you want higher or lower beta, dividend yield, valuations, dividend growers, those with higher dividend health, or interest rate sensitivity? The list goes on and these tend to be more volatility factors. For instance, beta as a factor was very bad in March and April when markets were falling, but very good in the last few months as markets moved higher. A strategy that leans into simply higher dividend-paying companies, which are typically more interest-rate sensitive, will do better if bond yields come back down somewhat. But they would suffer if yields moved higher. It’s not just about picking the factor you want more of, it is getting the timing right.

Here are the considerations we believe investors should look at when selecting new or assessing existing dividend strategies in this more complicated environment for dividend managers:

Diversification – While it sounds pretty basic, many dividend strategies are not well diversified. Chasing yield at the cost of diversification can lead to very high single sector weights, while many other sectors have no exposure. Some have as much as 50% financials or no health care or consumer exposure. Better diversification helps in an environment that has different factors working at different times.

Balanced cyclical yield / interest rate sensitivity – When bond yields were on their previous secular trend down, it was easy just to have exposure to more interest rate-sensitive dividend payers. But now with higher yields and more volatility around inflation and yields, a more balanced approach is needed. Economically sensitive dividend-paying companies can help balance the impact of interest rate sensitivity in this higher yield environment.

Financial leverage – Many higher dividend-paying companies operate in industries that are more stable which enables a more optimal capital structure to carry more debt or financial leverage. However, given a higher cost of debt capital in this yield environment, financial leverage has become a rising risk. When the cost of capital is high, financial leverage is a negative.

Flexibility – With other factors in addition to change in bond yields increasingly driving performance, and these additional factors being more volatile, dividend strategies that can adapt should have an advantage. Potentially taking advantage of valuation extremes in different parts of the market, adjusting the split between cyclical yield and interest rate sensitivity depends is on the trend in economic and yields, or other factors. A more flexible or active approach compared to a static allocation may be more ideal. Look for higher active share or turnover or active shifting exposures as evidence of greater flexibility. Of course, any shifts won’t always be the right shifts, but it should be better than a static approach given a changing landscape for dividend companies.

Final thoughts

The dividend factor appears to have weathered the adjustment in yields and is now back in vogue, from a flow perspective. The challenge is that a higher yield environment makes manager or strategy selection in the dividend space more important as divergence in performance is widening. Gaining exposure to the dividend space is certainly not as easy as it used to be.