Market Ethos

August 11, 2025

Earnings surprise again

Sign up here to receive the Market Ethos by email.

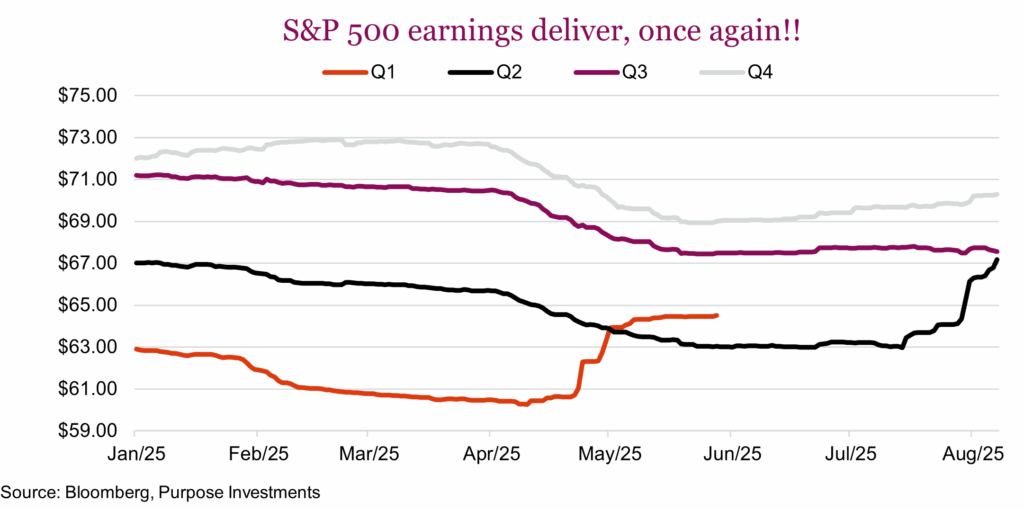

Second quarter earnings season is wrapping up and once again corporations delivered despite ongoing uncertainty. The S&P 500, with about 90% of companies having reported, had an 81% positive surprise rate which is a bit better than most quarters. Even more impressive, 70% experienced positive growth for an aggregate 11.4% growth rate. This was the 2nd quarter in a row that saw estimates reduced ahead of earnings season and a big spike when the results hit the tape. Q1 estimates started the year at $63, fell to $60 then jumped to $64.50 during the previous season. Q2 estimates started at $67, dropped to $63 then climbed back to $67 with the hard results.

The weak U.S. dollar certainly helped as did continued pricing power given inflation remained somewhat elevated. And while tariffs may put some upward pressure on costs, so far, the tailwinds have been more than enough to compensate. Perhaps the cherry on top of Q2 earnings has been some improvement for future quarterly estimates, that arrested their declines in June and have turned mildly positive.

It is safe to say, with hindsight, that the consensus analysts have gotten it wrong so far. Trimming estimates for Q1 and Q2 as the tariff fiasco gripped markets was premature. Corporations have clearly been able to navigate the uncertainty even with some stockpiling inventories and managed to protect profit margins and earnings. Will Q3 be a repeat? Perhaps, although it is worth noting tariff collection, and the impact, have only really just started in earnest.

We also must acknowledge that tariffs do not impact that many companies. Perhaps they have garnered more attention than they are due. And it really depends on other factors. For instance, most agree that tariffs are inflationary but it is not that simple. Yes, a tariff paid by a U.S. corporation as it imports either an input or finished product would lead to higher prices if simply passed through to pricing. But, some of this may be borne by the exporter. The tariff may be partially absorbed by a trimming to margins. Consumers may buy less, leading to lower volumes and cap price increases. Companies may stockpile ahead of tariffs, protecting margins for longer than one would expect. Or be more creative with sourcing goods to sidestep some of the tariff impact. A lot of moving parts and so far companies have been navigating well.

A similar trend of falling estimates then actual results beating was also evident in Canada for Q1 and Q2. Plus, estimates for Q3 and Q4 have started to trend higher. The rise of the TSX this year is pretty impressive, up 14.4% so far this year. So those estimates better get moving faster, as the TSX is now trading at 16.3x consensus earnings for the next 12 months. That is the highest valuation since early 2021 when earnings were still depressed coming out of the COVID recession.

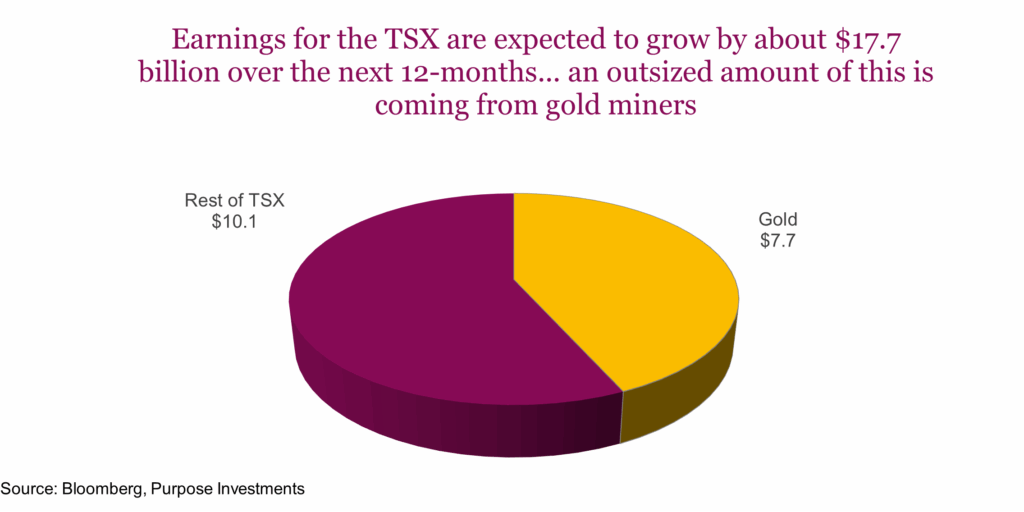

Is 16.3x a bit expensive for a market facing tariffs and a still sluggish housing market? Maybe. The bigger problem may be what brought the TSX to these new fresh highs. Banks have done well and are now historically expensive with only 4% earnings growth forecast over the next year. Shopify helped a good amount, about 2% for the TSX’s 14.4% gain. The other big piece is gold stocks. The Materials sector, which is now heavily gold weighted, contributed about 1/3 of the TSX’s gains this year. And for earnings growth, gold miners are forecast to grow earnings by $7.7B over the next year while the rest of the TSX contributes a mere $10B.

Don’t take this as us being negative on gold or gold miners, we are still positive on gold for a number of reasons. This is more about the TSX. Gold earnings, or really any kind of earnings that are very cyclical, usually carry a lower valuation multiple. Even when they are growing because those earnings can change course quickly and materially. The market will pay more for stability in earnings (consumer staples) or consistent growth (technology).

Final Thoughts

This has been a good earnings season for both America and Canada, which has helped moved markets higher. Let’s give credit where credit is due. And forward estimates are trending a bit higher, but given how consensus overreacted to the downside risks in previous quarters, is the collective now ignoring the risks after being burned in Q1 and Q2? Perhaps. The bigger issue may be for the TSX given so much of its gains and future expected earnings growth is coming from gold.

Maybe gold is Canada’s Nvidia. As it goes, so likely goes the index.