Market Ethos

November 10, 2025

Headlines versus reality

Sign up here to receive the Market Ethos by email.

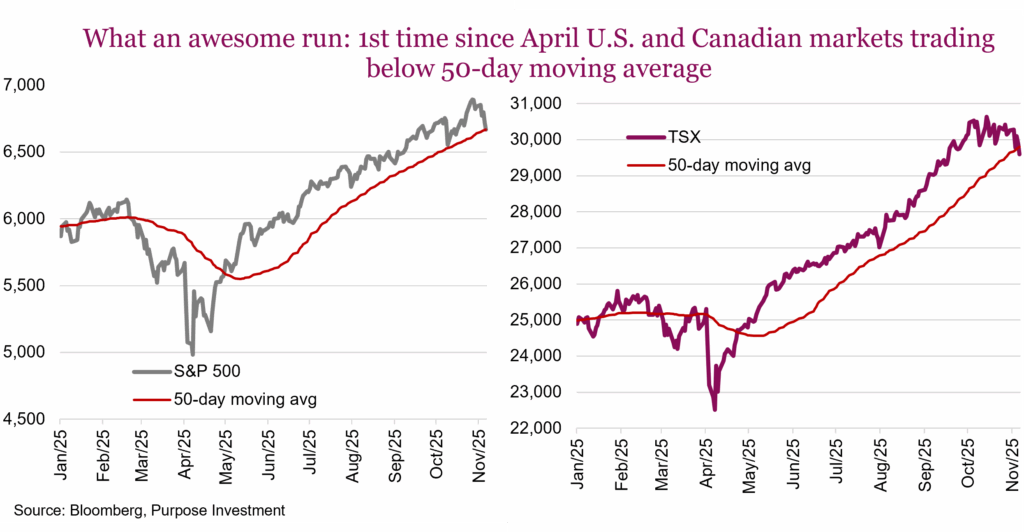

The market advance in 2025, or alternatively since the ‘Liberation Day’ tariff-induced bottom, has been very impressive. Not just in the magnitude of the market advance but in its lack of breaks or pauses during the journey. Any previous periods of weakness were quickly bid back up as the ‘buy the dippers’ took advantage of a slight discount. So now with the S&P and TSX trading below their respective 50-day moving averages for the first time since April, is this just a bigger dip or is it the early days of the correction that so many have been waiting for?

Naturally, as soon as the market wobbled a bit, the headlines were somewhat filled with bearish commentaries. A report that two large U.S. banks called for a 10-20% correction certainly attracted a lot of eyeballs. Worth pointing out that the timeline was over the next 12-24 months and given the S&P 500 has had about 25 corrections over the past 50 years, that outlook is actually the long-term average. Also worth noting that Warren Buffett’s Berkshire is sitting on $700B in cash. That isn’t really news as Berkshire has held a mountain of cash for a long time, up a bit from $643B a year ago but not like it’s a new market timing call. Or a famous hedge fund manager that has piled on puts in a few AI-related names. It’s a bearish positioned fund, and they have been bearish pretty much all the time.

We’re trying to highlight the dangers of headline scrolling. The world is trying to grab your attention, but headlines often lack enough context. It’s even harder now that many are relying on large language models to summarize. A headline yesterday read ‘US companies announce most October job cuts in over 20 years’, sounds really bad, eh? Why should we only look at October data? Attention grabbing yes, insightful less so. There was an uptick in job cuts, somewhat concerning but not as alarmist as the headline reads.

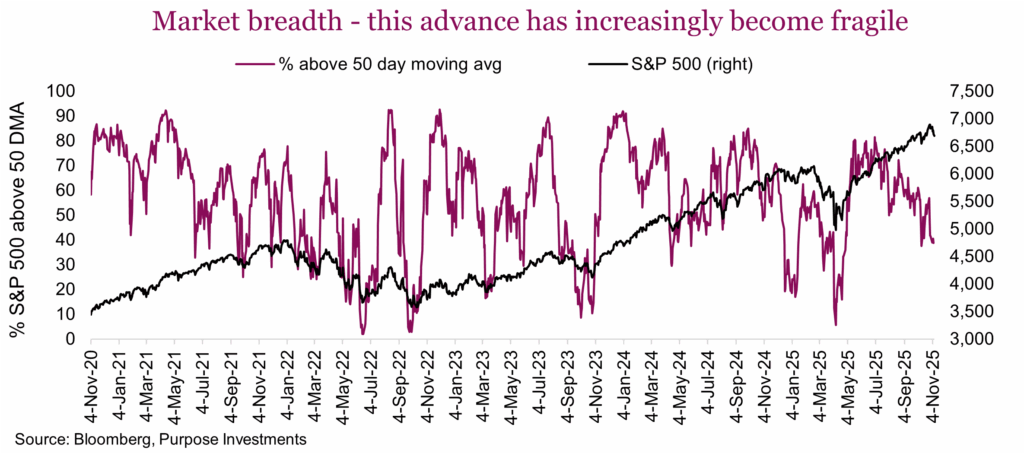

That being said, there is some decent evidence supporting that this could be the start of an actual correction. The market has run pretty far and very smoothly, so we could just say it’s due. But that is a pretty lame argument. Of greater concern has been breadth — in other words, the measure of how many members of an index are participating in its advance or in its decline.

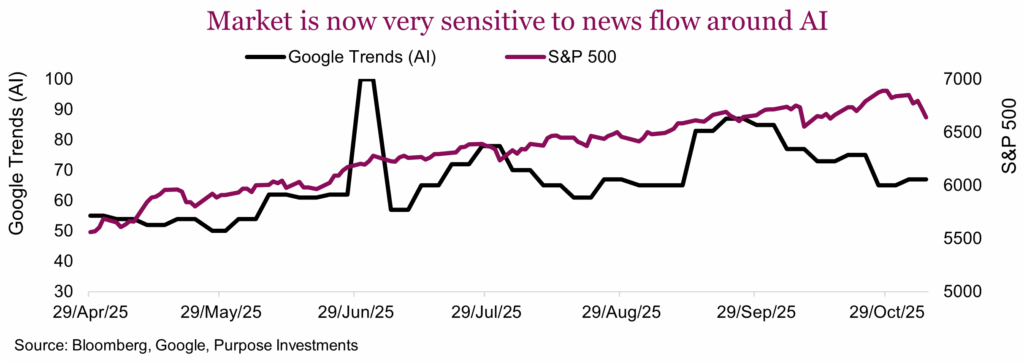

The breadth has continued to narrow driven by leadership concentrated in megacap tech names. That makes this market advance very sensitive to variations in excitement around AI. Opinions vary widely — how transformative will AI be, its actual return on investment, etc. Regardless of the debate, the news flow on AI appears to be a large determinant of market advance or decline. Based on Google Trends, the topic of AI appears to be softening a bit. Perhaps this is contributing to market softness. This market attention could shift to the economy, inflation, or even the government shutdown. But for now, it appears this is an AI-driven market.

It is also hard to tell if the buy-the-dippers are alive and well. Based on ICI data, the biggest equity fund + ETF inflow this year occurred during the week of April 9. That was the week when markets really got hit with tariff uncertainty — so great job investors for buying that dip!! Briefer and shallower periods of weakness since then appear to have elicited selling, not buying. Late May, early August, and mid-October are the three previous blips that either saw selling or certainly not inflow buying. Maybe the drops were not big or long enough to motivate this investor cohort; we may find out shortly as the current weakness is a bit more substantial.

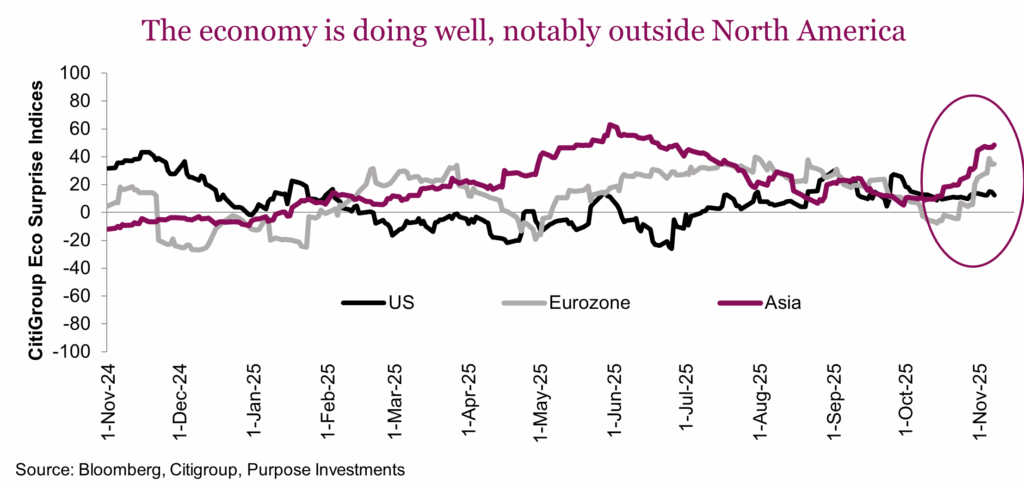

So here we have a market breaking below its 50-day moving average, all the bearish folks garnering the headlines, a market with poor breadth that is dependent on AI excitement and a less enthusiastic dip-buying investor. The good news is we have a global economy that is decent, perhaps even improving. The Citigroup Economic surprise indices have been moving higher, implying the economic data is better than expected. Less risk of recession means if this does turn into a correction, there’s less chance it becomes a grinding bear. It would be nice to have some more U.S. economic data, which is spotty given the ongoing government shutdown.

Final thoughts

Try and avoid doomscrolling financial headlines. It does feel that when markets are down, they tend to be more negative and when markets are up, more positive. It is a type of confirmation bias that helps attract more eyeballs. When it comes to investing, there are well researched or educated views, but the future is unknown. Have a view but also have a few different plans.

It would not be much of a surprise if this became a correction. We would look for investor sentiment to turn bearish, relative performance of defensives such as consumer staples and health care to show outperformance divergence from broader market, perhaps bond yields decline, put/call ratio to spike, US dollar strength to mention a few of our correction monitor signals. If enough provide a signal, and the market is down a more meaningful amount, and our economic view remains at low near-term recession risk, we may have that 2nd buying opportunity of 2025.

We are not there yet. Global equity markets are down 3-4% — this is mildly interesting but not interesting enough. It could very easily snap back positively this week on some AI news or perhaps government shutdown news. For now, we sit patiently with a mild defensive tilt in positioning and a well diversified defense. If a correction develops, we’re ready to act. But we’re equally happy if it doesn’t and we all enjoy a Santa Claus rally. Although we do think Santa already came really early this year.