Sign up here to receive the Market Ethos by email.

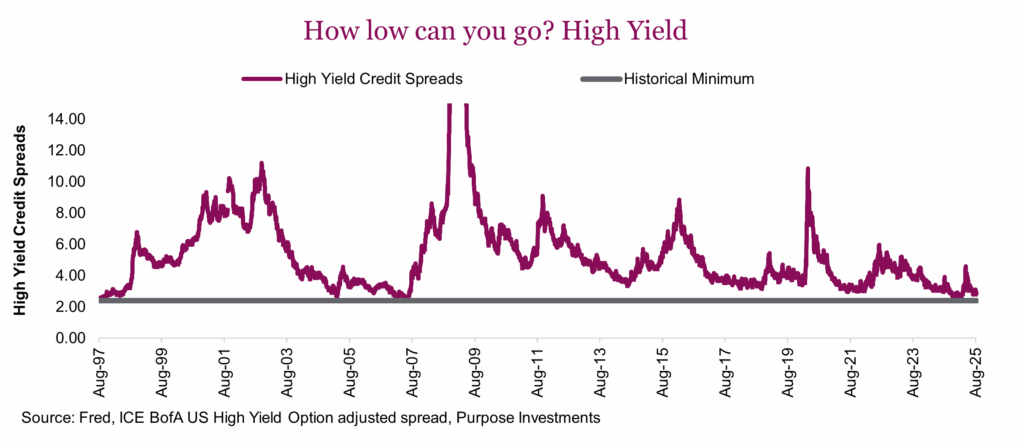

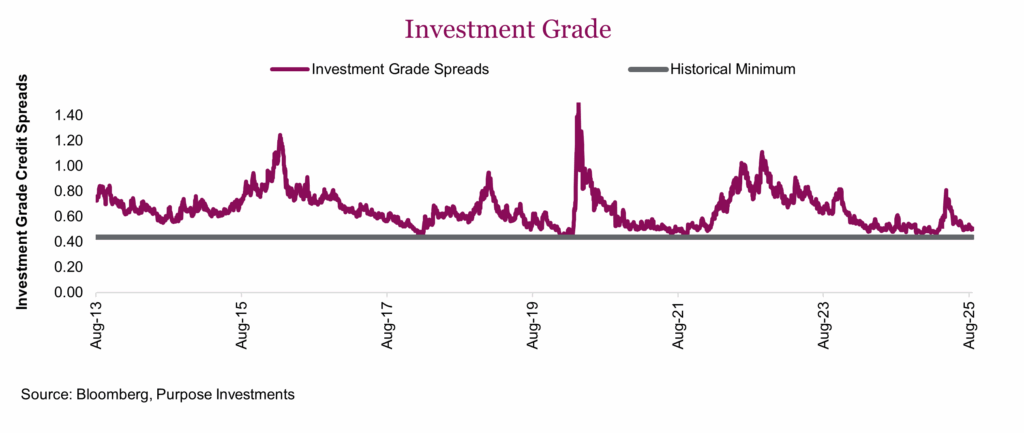

The risk-free rate, aptly named, is the nominal return you can earn without assuming any risk. Generally, government bonds or bills are used as a proxy for the risk-free rate to quantify it across different time periods. What got us thinking about the risk-free rate was credit spreads — the added yield above the risk-free rate provided by corporate bonds to compensate for such things as defaults. And these credit spreads are very low right now.

There are a few supporting factors that support such low credit spreads. Corporate debt, while high relative to assets, does enjoy coverage ratios (debt to EBITDA) that are very healthy. Perhaps the quality of issuers has improved over time. Or, with such healthy credit markets, companies just don’t go bankrupt like they used to. Just like equity investors tend to buy the dip on any sign of weakness, so do credit managers when spreads tick higher. There is clearly no shortage of buyers. That being said, do you think the world is so perfect to justify such euphorically low spreads?

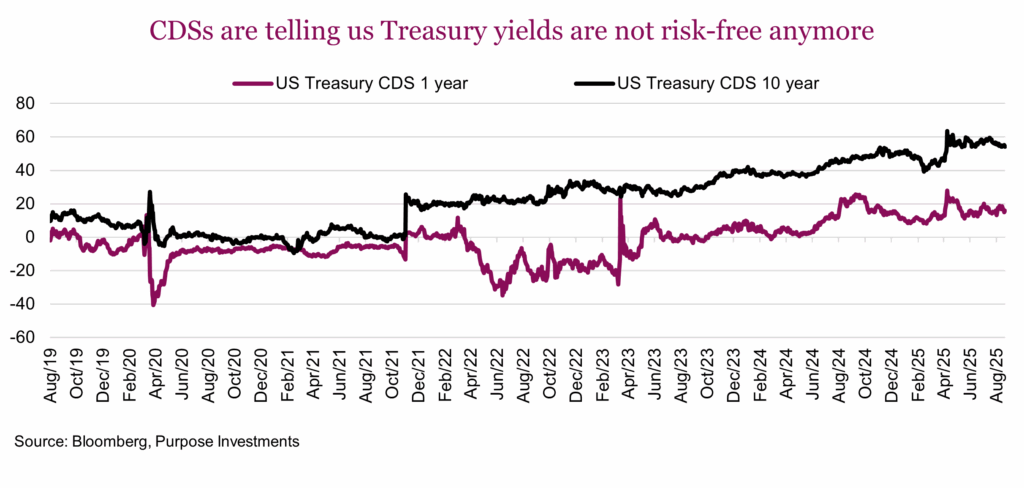

Then again, corporate spreads may be wider than they appear. As we highlighted, corporate spreads are measured off this ‘risk-free rate’ which is government bond yields. What if government bond yields aren’t risk-free anymore and now contain a bit of a risk premium? If so, that would suppress the stated corporate spread.

This risk premium in government debt isn’t about inflation or where yields are going next, it is more about default risk. This concern isn’t anything new. In the early 1990s, Ross Perot warned the U.S. government was on an unsustainable fiscal path when the total debt was a mere $4 trillion; three decades later and debt is over $37 trillion. Clearly his warnings were premature in the 1990s, but today there are increased rumblings on the sustainability, or path forward.

Without going down the rabbit hole of how government debt works, we will jump to the current state for the U.S. Their debt is very large, interest costs are rising and demographics are a challenge. So too is the current deficit level and expected increases based on current programs and policies. The global reserve currency is a huge plus though, as is the depth of the U.S. financial system — there are many levers to pull. Today, there is no shortage of buyers of U.S. debt, despite some of the headlines. So, this isn’t a today problem.

But it is a rising future risk without question. As a proxy for this risk, we will listen to the markets. Credit default swaps (CDS) are available on U.S. Treasuries, providing further evidence government yields are not risk-free, because if they were you wouldn’t need insurance, now would ya? CDS pricing is influenced by a number of factors that can push pricing around. There are two key takeaways: 1) Treasury yields are now incorporating some degree of risk and 2) that degree of risk rises the farther out you look.

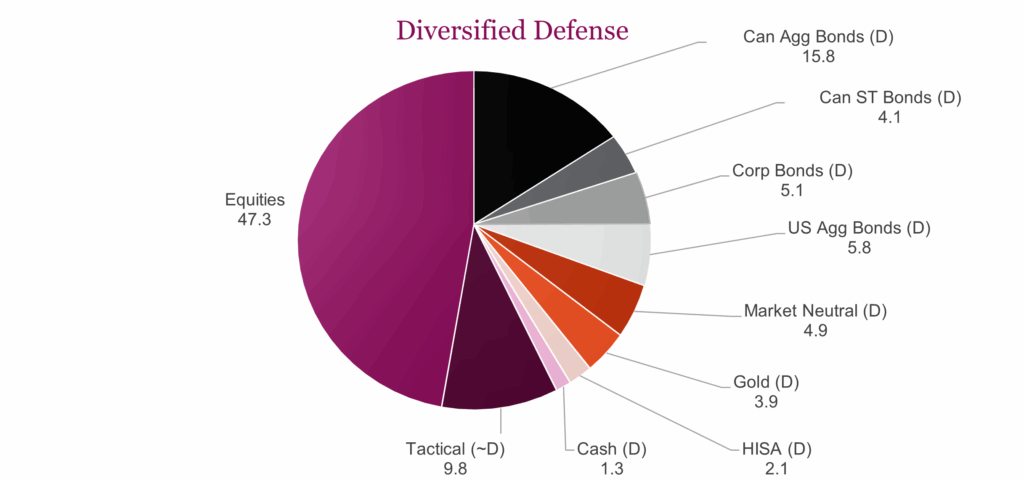

We are not alarmists on government debt or sustainability at this time, but we do believe this subject is on the rise. There are vast implications on how and/or when policy evolves in an attempt to address this rising risk, with potential knock-on effects. Today we are not losing any sleep, but we do believe portfolios should increasingly diversify their defensive positioning to include bonds, credit, hard assets, options strategies, momentum and alternatives. As an example, below are our defensive bucket allocations.

Final thoughts

The crux is that a Microsoft 10-year bond trading with a credit spread of 10 bps to the 10-year Treasury yield is actually closer to 70 bps above the true risk-free rate. Maybe credit spreads are not as tight as they appear given the benchmark they are measured against has moved. For those with exposure to credit, including ourselves, this may provide some solace that the posted historically low credit spreads to Treasury yields is not a reason to be overly nervous.

Source: Charts are sourced to Bloomberg L.P., Purpose Investments Inc., and Richardson Wealth unless otherwise noted.

The contents of this publication were researched, written and produced by Purpose Investments Inc. and are used by Richardson Wealth Limited for information purposes only.

*This report is authored by Craig Basinger, Chief Market Strategist at Purpose Investments Inc. Effective September 1, 2021, Craig Basinger has transitioned to Purpose Investments Inc.

Disclaimers

Richardson Wealth Limited

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson Wealth Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.

Purpose Investments Inc.

Purpose Investments Inc. is a registered securities entity. Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Neither Purpose Investments nor Richardson Wealth warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise.

Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice.

The particulars contained herein were obtained from sources which we believe are reliable but are not guaranteed by us and may be incomplete. This is not an official publication or research report of either Richardson Wealth or Purpose Investments, and this is not to be used as a solicitation in any jurisdiction.

This document is not for public distribution, is for informational purposes only, and is not being delivered to you in the context of an offering of any securities, nor is it a recommendation or solicitation to buy, hold or sell any security.

Richardson Wealth Limited, Member Canadian Investor Protection Fund.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.

Related articles

Market Ethos

Waiting at the train station

23 March 2026. Market Ethos. As hostilities broke out in the Middle East, markets were initially rather resilient. But after three weeks, that resilience is…

12 March 2026. Market Ethos. Over the past three decades banks have delivered standout returns. But with valuations pushed higher, the question now is: How…