Market Ethos

July 21, 2025

Know thyself

Sign up here to receive the Market Ethos by email.

The word ‘ethos’ is described as the underlying sentiment that shapes the beliefs of a group or society — much like the markets in our loose interpretation. On an individual level, it’s your character or disposition. (We’ll be focusing more on your character as an investor in this post, so no awkward questions about childhood or your relationship with your mother.)

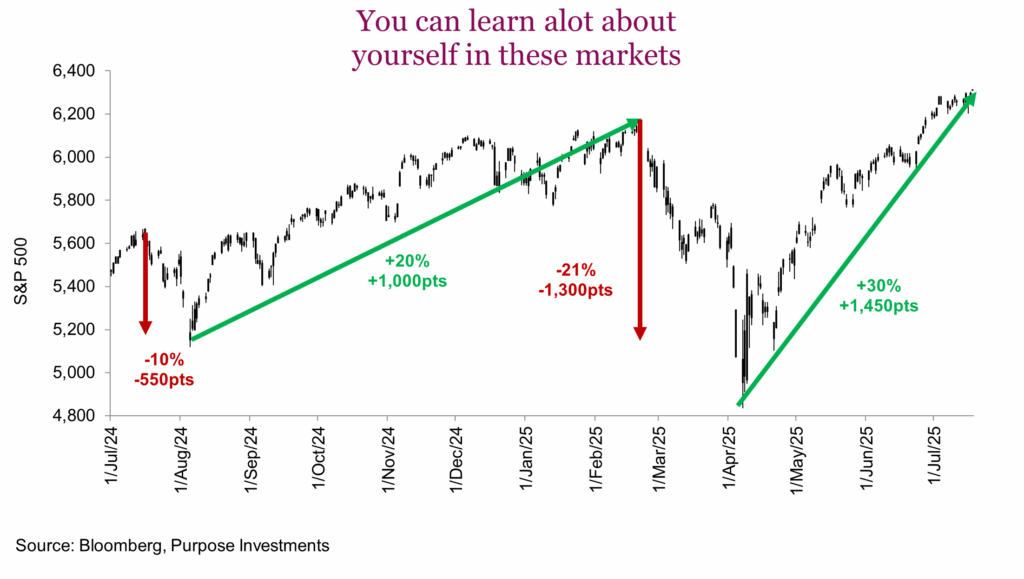

This year, and for the past five years, markets have performed very well, but a smooth ride it wasn’t. It’s during these kinds of market gyrations that, upon reflection, you can better understand your investor ethos.

In just the last 12-month period, the S&P 500 suffered a correction last summer (-10%), largely driven by a partial unwind of the yen carry trade combined with soft economic data. After taking five weeks to recover, markets remained flat until the U.S. election, after which markets gradually trended higher for a few months in February. Then the tariff news dropped, followed by a bounce all the way back to new highs.

It’s not just the market moves; the headline macro news has also been very volatile. This scenario of events and subsequent market reactions has created a great environment to understand yourself as an investor (or better understand your clients’ behaviours, if you are an advisor).

What was your anxiety level during these market drops, especially the tariff-induced episode? Did it make you want to de-risk (sell), opportunistically add given weaker markets (buy), or simply try your best to ignore the headlines and fluctuating portfolio market value? Or how about during the market upswings? Did you feel emboldened and want more – in other words, does your greed impulse overwhelm any fears? Seeing markets go back to highs does cloud your memory, but it’s worth honestly reflecting upon your feelings during these past moves to better understand your tendencies, whether you act on them or not.

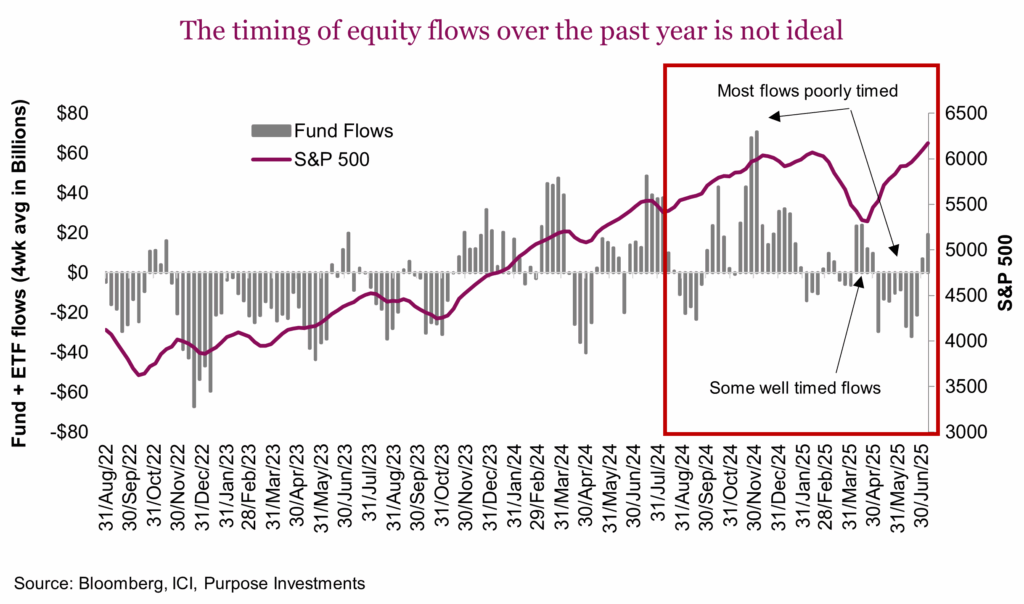

While everyone’s experience is different, the aggregate data does point to somewhat poor decision-making. The chart below is the four-week rolling average flows into equity funds & ETFs. Zeroing in on the past year, you can clearly see, in aggregate, some wealth-destroying behaviours. The vast majority of inflows came in late 2024, with the S&P 500 around 6,000, while outflows occurred, for the most part, below 6,000.

There’s no denying there was some aggregate equity market buying around the trough of the sell-off in April, but this appears to be the exception, not the rule. Tallying it all up, the dollar-weighted buying was at a 5,820 index level for the S&P, while the dollar-weighted selling was at 5,737. Buying higher, selling lower.

Now you may think, “Hey, the S&P is at 6,300, so buying at 5,820 isn’t bad.” True, a rising equity market can really help mask poor decision-making. The fact is, the average S&P level for this period was 5,793, a better entry point for a systematic approach.

Understand your behavioral biases

These market moves create an opportunity to better understand yourself, learn what kind of investor you are, and implement efforts to control or minimize the risk of making a mistake. Based on investor and advisor conversations, we have highlighted a number of key biases that appear prevalent during periods over the past year.

Ostrich effect

Everyone likes good news, being optimistic and making money. The ostrich effect occurs when investors place more emphasis on good news and ignore or downplay bad news (glass half full). This was likely evident in July 2024, as the economic data had been weakening but markets didn’t seem to care. We believe it was certainly evident in January and February of this year as markets ignored trade policy risk. And this could be occurring today as market optimism certainly isn’t fazed by slowing economic or earnings data.

This effect drives our attention away from bad news, almost as a defense mechanism. Investors most at risk of this bias are those who have become attached to a view, opinion or position for an extended period of time.

Strategies to counter the ostrich effect:

- Actively search out negative or contrary opinions. This can help open your mind to alternative scenarios.

- Get a second opinion. Other subject experts may not be as attached to your view or opinion, enabling a more balanced approach to weighing the pros and cons.

- Pre-mortems on an existing position can really help uncover what could go wrong. And if contrary evidence surfaces, you will be in a better position to assess and incorporate it into your overall view.

Availability bias

This has become one of the biggest biases for investors. It has people believing the most convenient reason something is happening, often drawing a linear causation. Given that macro headlines are exceptionally loud these days, it’s very easy to connect the headlines with markets.

Unfortunately, since markets are very dynamic and have so many moving parts, there’s almost never a simple cause and effect. Falling prey to this bias runs the risk of not being aware of other factors that don’t receive the same degree of coverage.

Strategies to counter availability bias:

- Stop watching the news (kidding). Media is often focused on sharing more vivid images or information in an effort to maintain viewers’ attention. Less exciting information is often not reported on.

- Track the sources of your investment information and attempt to diversify across many different sources.

Anchoring bias

We very often become anchored based on what we paid for an investment or by the fact that an investment traded at a certain level. This anchor price can have an outsized impact on subsequent decision-making. This is the case even if that anchor price is no longer appropriate given the market environment, or if the anchor itself was inappropriate.

At the moment, many investors are anchored to the lows of April, saying, “How can I buy today given it was so much cheaper a few months ago?” The TSX was around 23,000 versus over 27,000 today. However, the April lows may not even be appropriate because they were exacerbated by an abrupt tariff escalation. What we know today is very different: tariff risk isn’t gone, but it’s not nearly as dire as portrayed in April.

Strategies to counter the anchoring bias:

- Remove all original costs when reviewing a portfolio. The decision to buy/hold/sell a position or fund should be based on future prospects relative to its current price. It’s ok to consider cost for tax reasons, but this should be secondary.

- When researching, avoid numerical forecasts, especially early in the process, as this may impact how additional information is incorporated.

- Associate the market environment or company news with a certain price level. If the news changes materially or the market environment changes, the anchored price should no longer be applicable, so throw it out.

Fear of missing out (FOMO)

FOMO actually isn’t a behaviour bias, but the result of a few biases: loss aversion, herd behaviour, and status quo bias. Not surprisingly, it impacts investors when markets or specific industries have a great amount of volatility.

This appears to be evident today in the broad market as equity fund/ETF flows are starting to turn positive, even after so much positive performance has already been experienced. FOMO is also common in subcategories, from crypto to AI.

Strategies to counter FOMO

- Being more systematic. FOMO is often caused by inaction due to fear or regret. Having a more systematic approach that reduces emotions can certainly help.

- Move in smaller steps. We would all love to simply buy at the bottom and sell at the top. Since that is unrealistic, moving in smaller incremental steps can have you doing more selling when prices are elevated and more buying when they’re cheaper. This also helps diversify timing risks when markets are volatile.

- Have a long-term plan. It really helps you think in longer time horizons and fret less about near-term market volatility.

Final thoughts

Take the time to reflect. If you can better understand your emotions and behavioural biases, you have a better chance of avoiding bad decisions when those biases flare up again. If you believe you’re at risk of capitulating during weakness, tilt more defensively or rely more on professional advice. If you’re a performance chaser, remaining diversified is crucial; incorporating a risk mitigation strategy and a more systematic approach can really help.

Take stock of your behaviours and feelings about investing over the past few years. Understanding your personal tendencies with an objective lens can really help your own decision-making process during periods of market volatility. And understanding can help avoid or mitigate damaging performance behaviours.

To know thyself is the beginning of wisdom.

Socrates