Market Ethos

December 1, 2025

Laggards need to join the party

Sign up here to receive the Market Ethos by email.

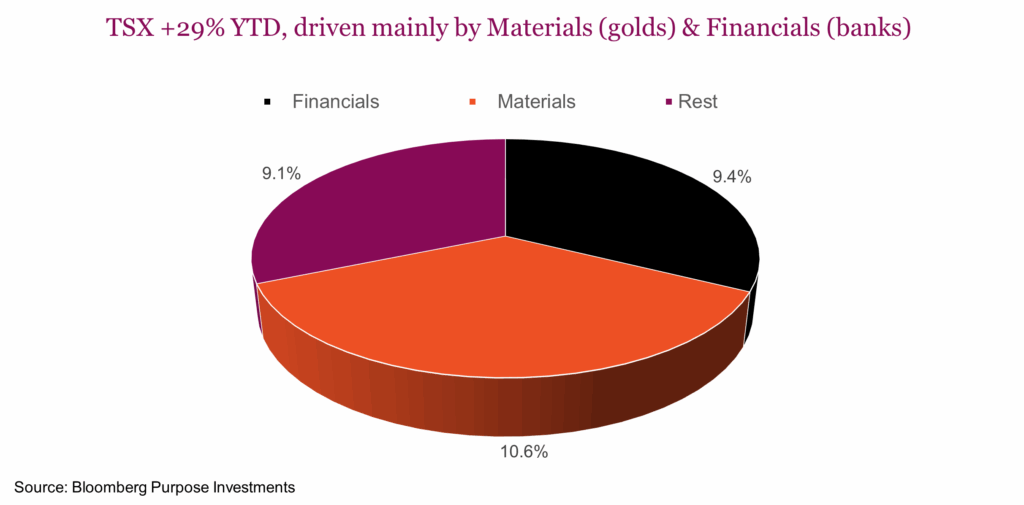

The TSX, up 29.2% (as of Nov 26) has enjoyed an amazing year. In fact, this is shaping up to be the third consecutive year of strong double-digit gains (not trying to jinx it). What makes 2025 even more impressive than previous years is that it comes amid a clearly negative tariff environment, a lackluster housing industry and oil down over $10/bbl. Most investors are aware of where this performance came from: banks and gold. Materials and Financials provided 20% of the 29% gain, but we don’t want to downplay the contribution from Shopify and Celestica (3.5%). Beyond these groups, however, gains were certainly hard to come by.

Perhaps the more challenging issue is that within Materials, it was mainly the gold names, and within Financials, mainly the banks. There are 32 gold companies and 7 banks in the TSX Composite’s 234 members, which means 17% of the TSX names drove more than half the gains. If you didn’t own enough of these so far in 2025, it has likely not been nearly as enjoyable.

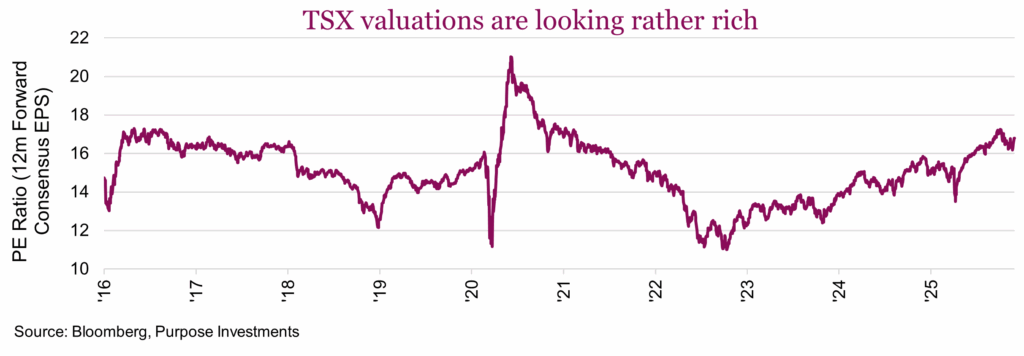

A 29% year-to-date gain is awesome, but this has pushed valuations for the TSX from 13.1x two years ago to 16.8x today. Which raises the question – with elevated valuations should we expect strong gains to continue into 2026? One of the challenges with aggregate market valuations is the composition of the market. The TSX has some pretty big sectors that drive the overall market and valuation. Let’s dig in to see if it is really expensive looking at individual sectors or companies for better clarity. We’ll also see if there are other areas that could keep these strong returns flowing into ’26.

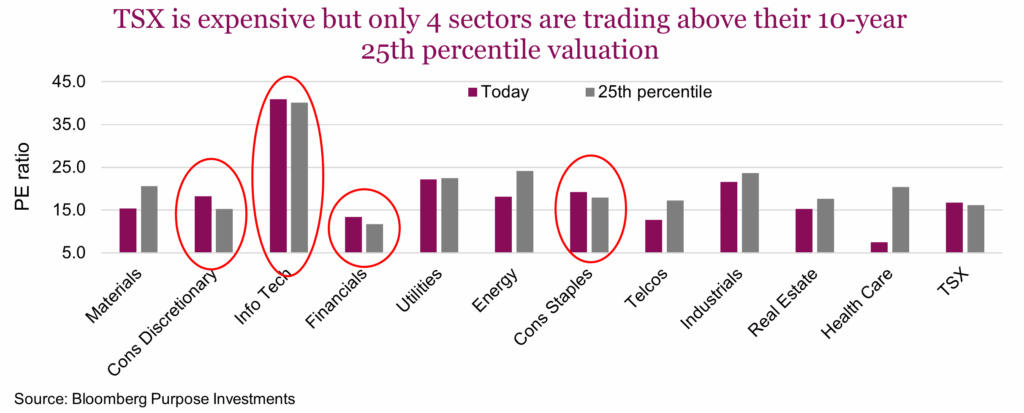

The valuation story of the TSX does look a bit better underneath the hood. Looking at the past 10 years of valuations, the TSX is in to the top quartile valuation bracket (16.8 vs 16.2x). Unlike with fund performance, top quartile is not good in this case as it’s the top 25% of valuation instances over the past decade. So, the market in aggregate is expensive but this is driven by four sectors. Consumer Discretionary, Information Technology, Financials and Consumer Staples are the only sectors in their respective highest valuation quartiles. That leaves seven below, including the high flying Materials sector. Folks won’t pay up too much for the elevated earnings of gold companies because they can disappear as quickly as they appeared.

Herein lies the challenge for 2026. While many sectors are still offering attractive valuations, which may be encouraging for future returns, most of these sectors are largely inconsequential for the TSX. For example, Health Care, Real Estate and Telcos are cheap but in total they present a mere 4.3% of the TSX. Health Care is a paltry 0.3%, Real Estate 1.8% and even those Telcos are down to 2.3%. They simply are not big enough to move the TSX in either direction at this point.

The big weights of course include Financials (32%), Energy (16%), Materials (14%), Industrials (12%) and Technology (10%). As go these sectors, so goes the TSX. Financials are a risk for the TSX given elevated valuations. They may not look overly high in the above table but the variance in valuations for this sector has historically been pretty narrow. Maybe the better economic data will help – we saw decent Canada GDP last week. But we do believe it will be hard for financials to do much heavy lifting in 2026. Materials are a wildcard as to where gold goes from here. Maybe it will keep driving the TSX but those gains have already been pretty monumental. Maybe technology, aka Shopify.

If the TSX is going to keep pushing higher, it would likely need a lift from Industrials and Energy. Industrials are cheap as the risk of tariffs has hit this sector especially hard. Given USMCA goes into review in 2026, that is a big wildcard. We think Energy could be a positive driver in 2026. Yes, there is a glut of oil on the market with surplus by many forecasters expected to rise to 1m barrels per day. But there has also been a lack of big projects financed over the past few years, which could bring the market into better balance. The stocks would likely move well ahead of this and they are attractive. More on this in our upcoming 2026 outlook.

Final thoughts

Putting it all together, the TSX may enjoy solid returns in 2026, but it is going to be tough given valuations. International fund flows may do the trick as money is increasingly looking for markets outside the U.S. as the great rebalance continues. That could keep pushing valuations higher but it’s going to be harder. We are a bit more cautious on Canada; it was easier to be bullish when valuations were in the 11-13x range. To keep the party going, some of the laggards, namely Energy and Industrials will likely have to start contributing.