Market Ethos

May 26, 2025

Let’s talk about yield

Sign up here to receive the Market Ethos by email.

In late 2009, Greece came to the market to sell some government bonds, and nobody showed up to buy them. Structural issues of the eurozone (namely a common currency, common central bank rates and divergent fiscal regimes), which had been exacerbated by the global financial crisis and falling economic growth, all culminated in the European debt crisis that lasted for years. For a while, investors did not have confidence they would get their money back from European government bonds.

More recently in October of 2022, the UK passed a budget that included too much spending and too many tax cuts, with the obvious implication of too much government borrowing ahead. Faith in the pound and gilts fell dramatically. 10-year Gilts, which had already experienced rising yields from 2% to 3.25% over the previous month, jumped to over 4.5% in a matter of a few days. Global inflation was running hot, which didn’t help. But the UK is not Greece — it enjoys its own currency, its own central bank and is financially much larger and developed. A number of levers were pulled and things calmed down. But it did indicate that faith in government bonds is not 100%, even for large, developed nations.

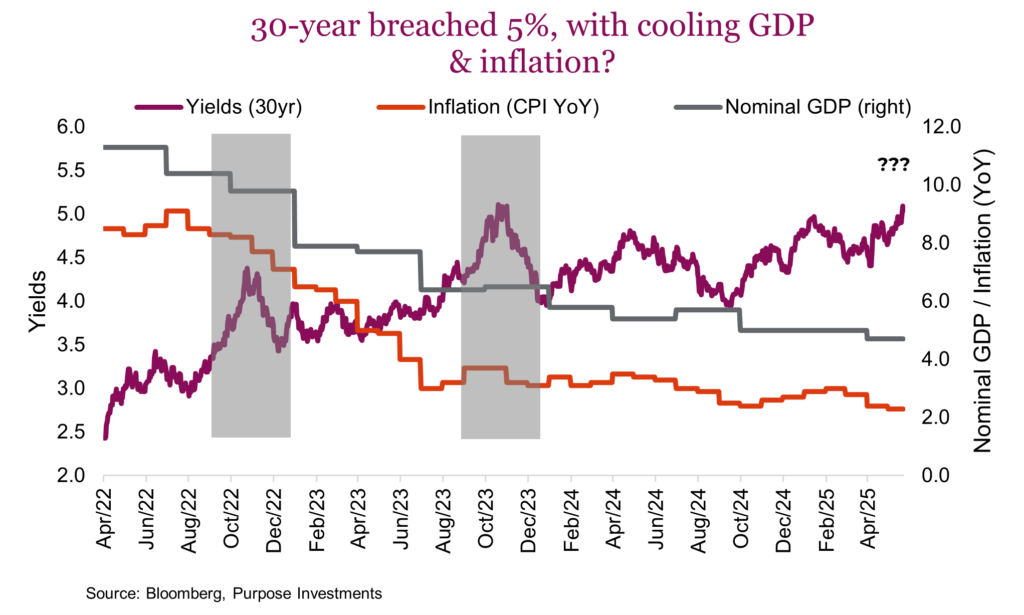

Last week, the U.S. 30-year Treasury yield broke through 5%. This level had been breached in 2023 (second grey box), but that was when nominal GDP was expanding at a robust 6%+ pace. Or the previous move up in 30-year yields occurred in 2022 (first grey box) when inflation was around 8% and economy growing over 10%. This recent increase in long yields is not driven by spiking inflation or an economy heating up, it appears to be driven by risk. Risk that the U.S. government may run into financial trouble, making a 30-year hold seem a bit too long, or require a bit extra yield to take the risk.

Concern over the budget making its way through the houses, combined with less enthusiastic international buyers following the tariff policy flip- floppery, are adding to the ‘narrative’. Some articles pointed to a drop in the bid-to-cover ratio for an auction of 20-year Treasuries. Really? The 20-year is an odd bond, and it dropped from 2.63x subscribed to 2.46x.

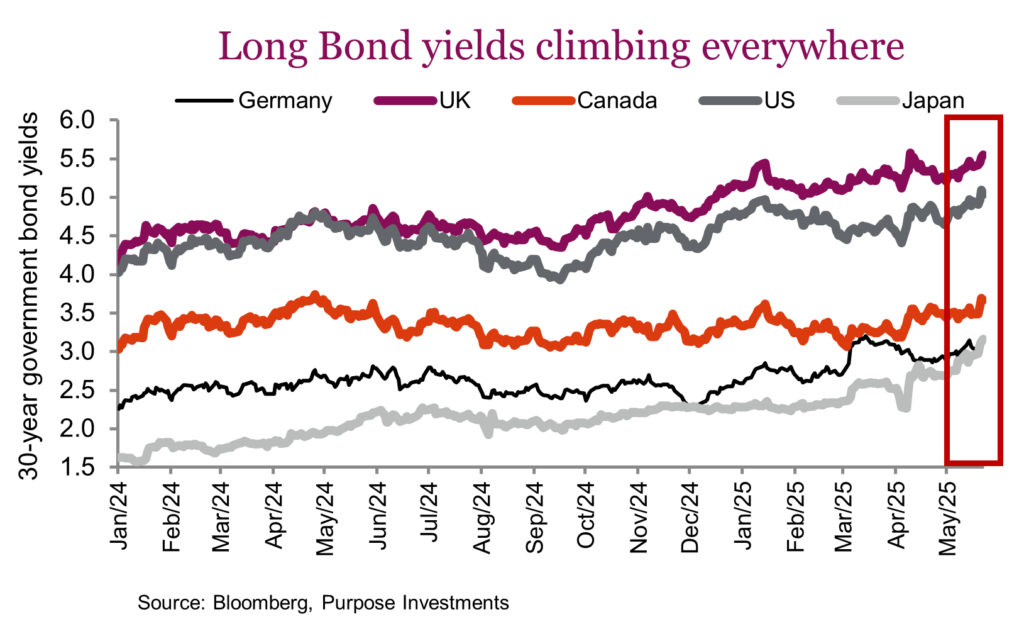

But these rising long yields are not just an American story. The long-dated bonds for many nations have been rising of late, including Canada, UK and Japan. Japan, once the land of no yield, is now getting some yield. Is this evidence that debt sustainability has become an issue around the world due to high deficits and high debt levels? Not so fast.

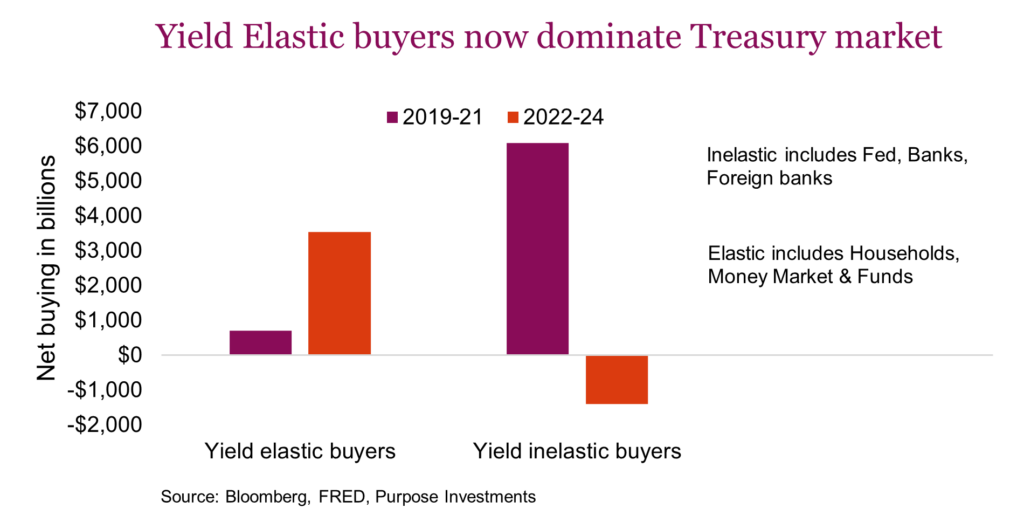

As we discussed last summer in our Ethos titled ‘Bond buyers can be so sensitive’, the composition of bond buyers has changed over the past decade or so. In the 2010s, most bond buyers were what we would call ‘yield insensitive’ or inelastic. In the U.S. the Fed was implementing quantitative easing, buying bonds and never caring what the yield was. Foreign banks saddled with U.S. dollars from net exports to the U.S. had to convert or park it in Treasuries. Domestic banks with too much capital given so much money in the system and not enough loan demand, would park money in Treasuries to improve capital ratios. These are inelastic bond buyers, they just don’t care if it yields 1% or 5%.

However, over the past few years, the above cohort has shrunk in size. Limited growth in global trade has led to less buying by foreign banks plus a bit of reluctance to hold as much bank reserves in Treasuries. The Fed is no longer a big bond buyer. Domestic banks are not as active as net buyers either. Filling the void has been accomplished by households and money market funds, both driven by a typical investor. Investors, like you and me, are yield elastic.

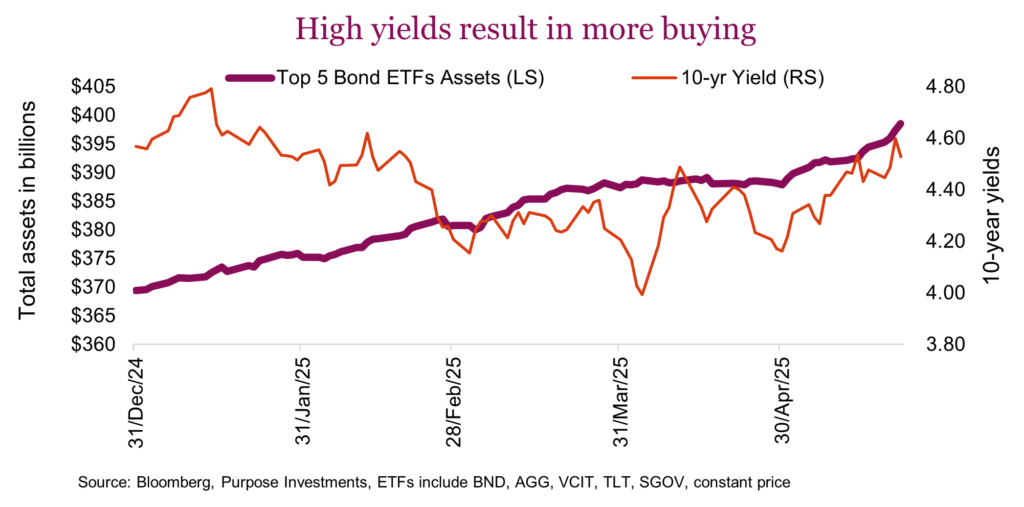

With yield elastic buyers in the driver’s seat, this should help keep yields more rangebound and higher than the 2010s, which were dominated by inelastic yield buyers. If yields fall, fewer buyers should limit how low yields move. And if yields rise, more buyers may be enticed to do some buying. Overall, this should keep yields more rangebound. And this recent increase in yields has enticed more buying. For a more timely reading, the chart below shows the net assets in the five biggest U.S. bond ETFs. You may notice the increase over the past few weeks (slope of purple line) as yields moved higher — yields are starting to cool a bit.

In the short term, we are not discounting the impact on bond yields. But should inflation or economic growth change direction, that would certainly impact yields. We are also aware the U.S. has enjoyed lower issuance levels over the past few months thanks to tax receipts, with issuance (aka supply) increasing in coming months. Or if the market goes risk-off for any other reason. However, the impact on yields of any changes in these dynamics will be somewhat muted given the elasticity of yield demand by investors.

Longer term there is a debt sustainability risk, but this is likely a muted risk today. A high debt to GDP does not beget a crisis. More important is the yield environment relative to economic growth. If yields remain higher than growth for an extended period, there is greater risk of a crisis. Today, U.S. nominal GDP is growing at 5-6%, still decently higher than overall yields.

Final thoughts

We are not saying bond yields can’t move up from here but if they do, more buyers will likely show up including ourselves. This should limit how high yields can climb in the near term and keep them somewhat rangebound. We do believe the pace of U.S. deficits is high given the low unemployment and economic growth. But we’re not convinced this will lead to runaway yields anytime soon. And should the economy start to cool, yields will likely come down.