Market Ethos

June 9, 2025

Risky business

Sign up here to receive the Market Ethos by email.

Last week was yet another example cementing the need for investors to navigate the noise by ignoring it. One would think a playground fight (on X) between the president and the world’s richest man would have negative implications. But the market has gotten over it and moved on, buoyed by a labour report that wasn’t bad. It was kind of a neutral report, but since many were expecting a weak one, neutral is good, and it lifted the S&P 500 back over 6,000. The S&P 500 has seen some wild swings so far this year, starting around 6,000, then up a bit, then down a lot to under 5,000 and then back to 6,000. Anyone reacting to the headlines or policy announcements during the journey has probably caused a bit of damage to their portfolio.

Remember when Canada was doomed to a recession, the loonie at 68 cents, politicians resigning, etc? Well, Q1 GDP was up over 2%, the CAD is now over 73 cents and the TSX has been making new all-time highs for a few weeks now. Of course, the future is always uncertain. The key lessons for 2025 are 1) listen to the news, largely because it is almost impossible not to and 2) don’t react to it, as you will likely end up just chasing your tail (dog reference but it applies to portfolios too) and 3) price matters.

Do you feel the market is riskier today or riskier in the early days of April as President Trump announced tariffs on everyone rocking global markets? Trick question, an S&P at 4,900 in the early days of April is less risky than an S&P 6,000, whether in February or in June. A lower price carries less risk. This is a crazy year from a news and headline perspective, and it is likely best to use price as a useful input tool.

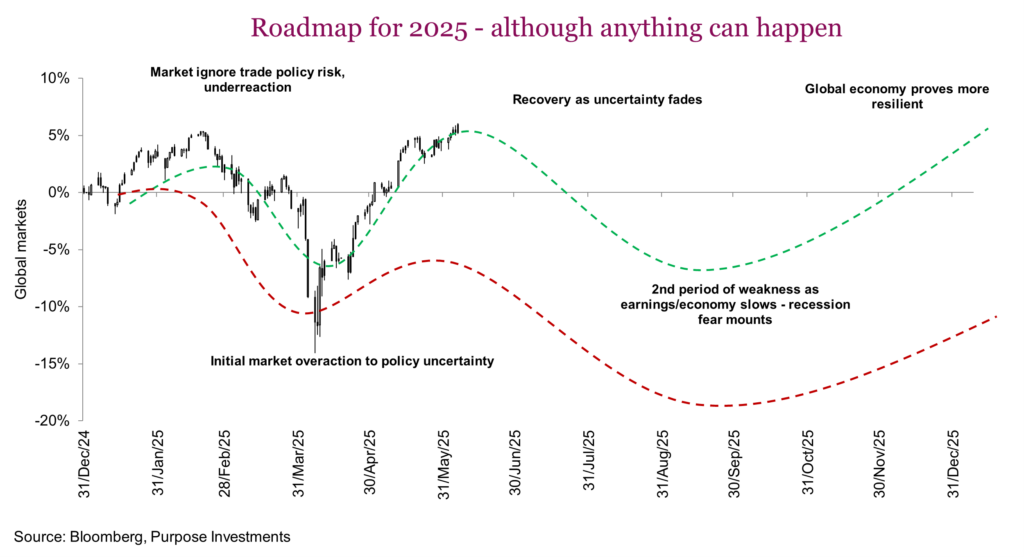

It is fair to say the equity markets were ignoring the trade uncertainty or policy risk in the early days of 2025. Even with announcements of tariff intentions, the narrative was an offramp or solution would be found. Then the market took the tariff policy risk seriously, in retrospect too seriously given the market recovery over the past couple months. Underreaction, overreaction, underreaction?

So, now it does look like an opportune time to reduce market exposure, especially if you were fortuitous enough to have added during the period of weakness. Over 6,000 for the S&P 500, this market is risky again.

There are encouraging factors for the markets at the moment. The trade tensions have certainly cooled and this may continue. The weaker U.S. dollar is positive for global markets and the price level of the S&P 500. Oil down in the $60s certainly helps the global consumer. And with many of the policy announcements from the U.S. being, let’s say market unfriendly, there are likely more market-friendly components in the coming months such as less regulation, etc.

BUT, the bearish case is also pretty strong. Rising long-term yields are causing a bit of angst among investors. Earnings revisions continue to soften. Last week’s U.S. labour report was ok, but labour is always a very slow and lagging indicator. Overall, the economic data does appear to be slowing. Throw on a U.S. tax bill that has raised many eyebrows on the level of spending and potential taxation changes for foreign capital. And let’s not forget the recent trend of global investors moving money elsewhere (in case you were wondering WHY the TSX was making new highs, this global trend has helped).

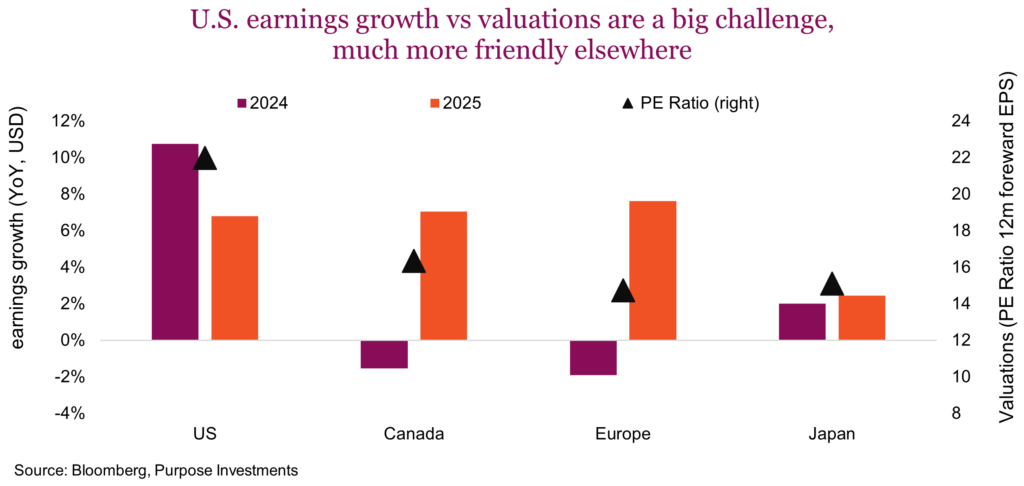

There is nothing that is doom and gloom, however at 6,000 is the U.S. market underreacting to the risks? Especially for the U.S. market. Even with the relative trailing performance year-to-date, the S&P 500 is still trading over 22x and is now expected to only enjoy 6% earnings growth — far below the 10%+ pace of last year. Earnings growth for 2025 has moderated everywhere, but other markets are not trading over 20x. Hence, S&P 6,000 is looking risky.

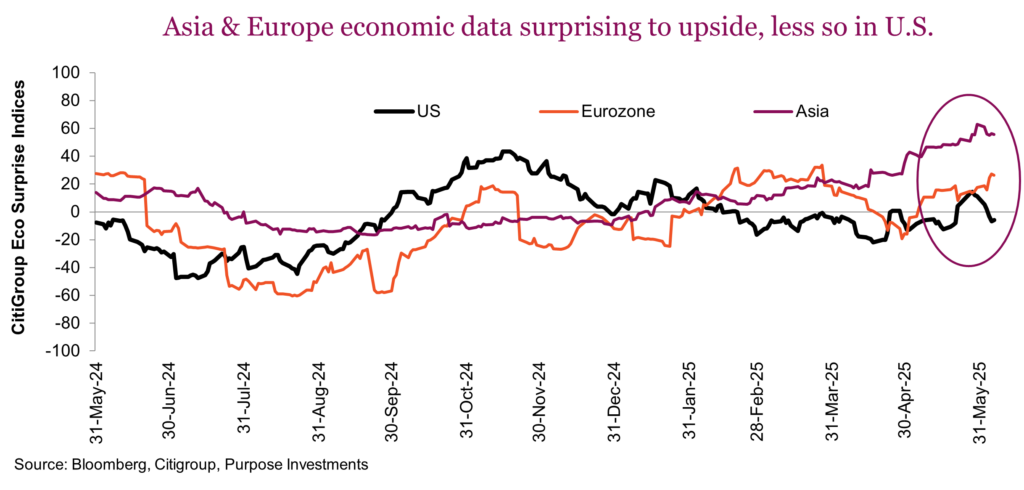

Add on top of this, a trend in the economic data that has Europe and Asia seeing more upside surprises while the U.S. data is the laggard.

Final thoughts

Only in hindsight can you see if the market was overreacting or underreacting to a risk or opportunity. It’s easy to say it overreacted to trade policy risk, but harder to say it is now underreacting to risks or properly reacting to upside potential. With the S&P 500 over 6,000, 22x multiple with slowing economic data and a negative earnings revision trend, the S&P 500 is getting risky again and we are monitoring. Take a good look at your asset allocation, as mentioned in the latest Investor Strategy, you may be overweight U.S. equities if you take a deeper look under the hood. If you are overweight, it seems like a good time to trim some.