Market Ethos

19 January 2026

Size matters

Sign up here to receive the Market Ethos by email.

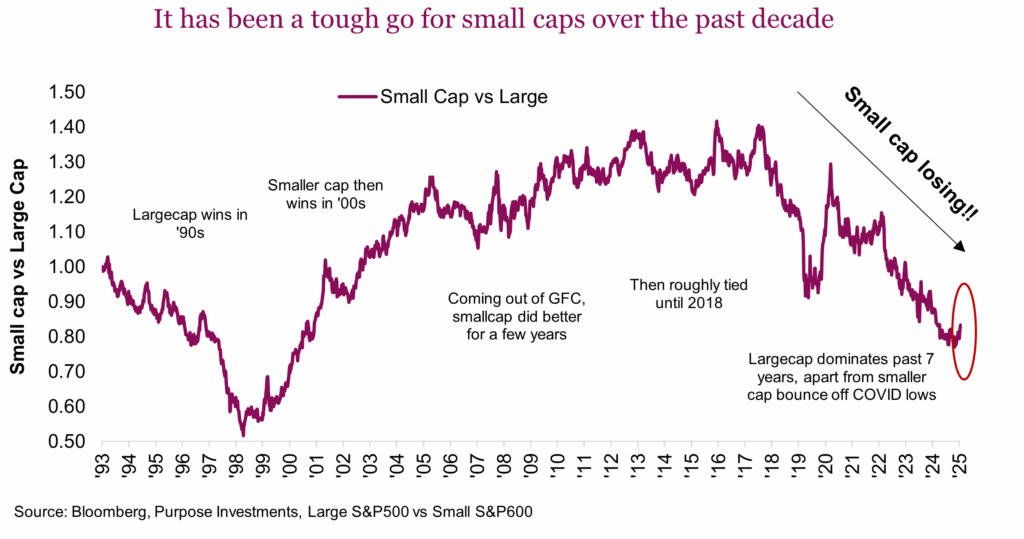

When it comes to large cap vs small cap it sure feels like big always wins. That certainly has been the trend for much of the past decade, with the exception of a few brief periods where relative performance flipped temporarily. It wasn’t always this way. In fact, there are many well- researched papers extolling the virtues of the size premium, meaning small caps should outperform over time. But you do have to look back pretty far to see or enjoy this premium.

But it’s January and the start of a new calendar year. The start of a new year typically has folks asking, “is this the year for small cap?” And January often sees a rally in lower quality, which is a factor more prevalent in small cap indices. So here we are mid-way through January and the S&P 500 is up +1.5% while the S&P 600 (small cap) is up +7.3%, encouraging more investors to ask the question.

We have not been fans of small cap for some time and currently have minimal exposure. And we certainly would not consider adding to small cap mid-January, given the early-year pop, which has often proved fleeting. Still, there are both encouraging and discouraging aspects to small cap today. Here is our take as we look at U.S. small caps:

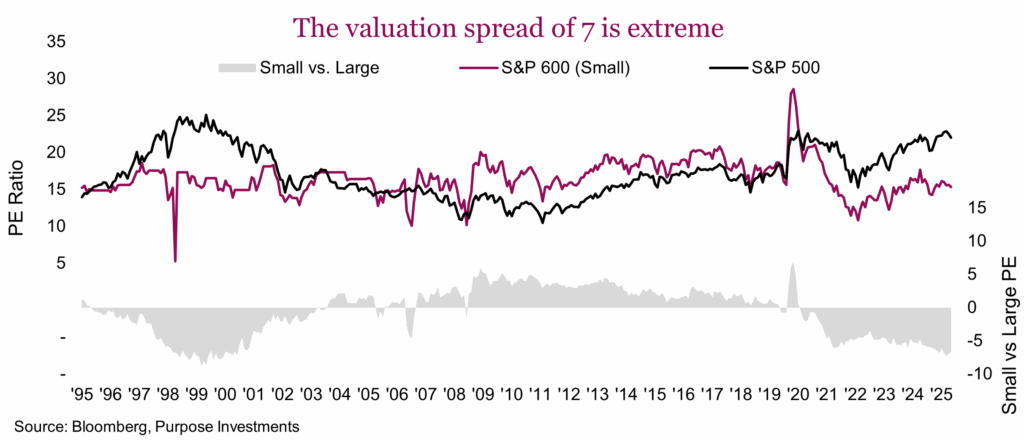

Fundamentals – Valuations are a strong vote for future small cap outperformance given the valuation spread. Based on consensus 12-month forward estimates, the large cap S&P 500 is trading 22x while the smaller cap S&P 600 is a more reasonable 15.3x. That spread is roughly at historical peak levels, so either large cap is too expensive, or small cap is too cheap. We also witnessed this valuation spread level at the end of the dotcom bubble which kicked off a multi-year run of small cap outperformance.

BUT, this valuation argument is not new. In fact, the valuations spread has proven persistent over the past few years and has clearly not led to small cap outperformance. This is because while valuation matters, so does earnings growth. If earnings are not growing, why would the market pay up with a higher multiple? And during the past few years, small cap earnings growth has lagged large cap.

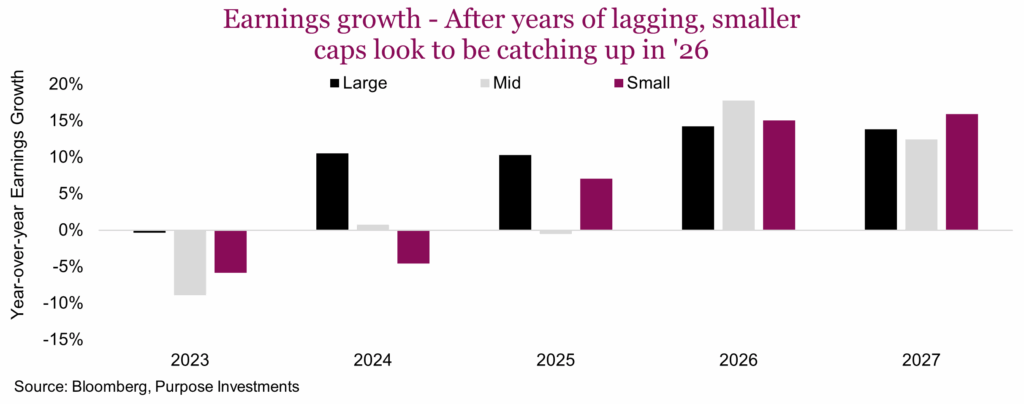

2026 does look more constructive for small and midcap from an earnings growth perspective, but don’t get too excited. Revisions often land hard for smaller cap companies, and the recent trend isn’t great. Over the past two months, the large cap S&P 500 consensus for 2026 has been revised higher by about +1.4%. A nice trend. Meanwhile, the S&P 600 small cap consensus earnings have declined by 2%.

Valuations certainly favour small cap and with earnings growth forecasts much improved, the fundamentals are encouraging — with the caveat that revisions are a bit troubling.

The economy – This is where our view turns a little more challenged, but we’ll start with the good news. The Fed is cutting interest rates, which has historically been positive for small cap companies. In fact, the relative performance of size correlates well with the steepness of the yield curve. When the curve steepens — whether due to central bank cuts at the short end or the longer end rising on improving economic growth prospects — small cap tends to outperform. Since mid 2023, the yield curve has been steadily steepening, yet small cap has not outperformed. A divergence like this can often be followed by a catchup. Financial conditions are certainly supportive of small cap.

U.S. economic growth composition is a challenge. The U.S. economy is growing well lately, but this growth is skewed toward corporate spending on data centers, trying to keep up with AI demand. Small cap index composition has a greater weight to the U.S. consumer, and less so to information technology names. So generally, small cap is not in the sweet spot for the U.S. economy as the consumer is under pressure. Adding to this are tariffs which are starting to show an incremental impact on financials. While small cap does enjoy a higher percentage of sales domestically, input costs may be an issue given tariffs.

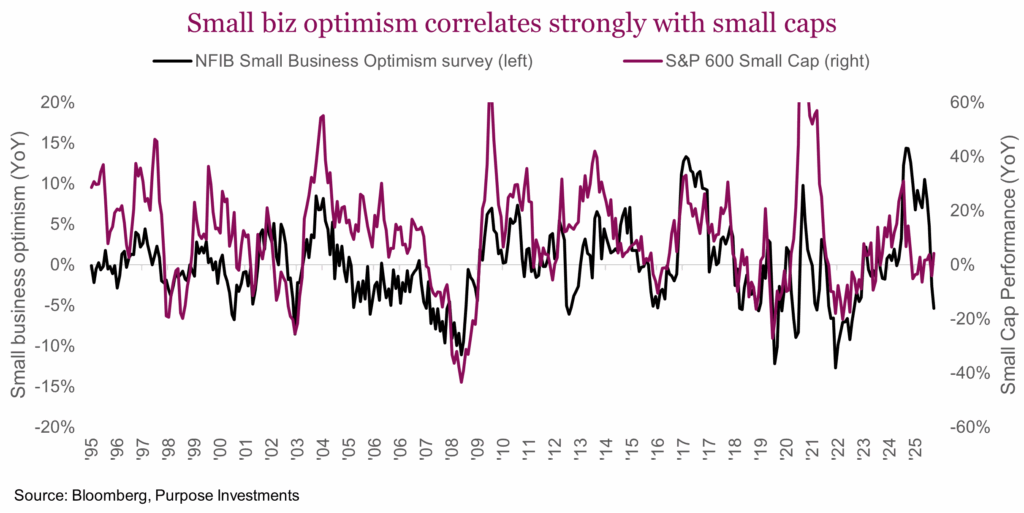

This is encapsulated in the National Federation of Independent Businesses (NFIB) small business optimism survey. This survey correlates well with small cap index performance, and results have turned negative.

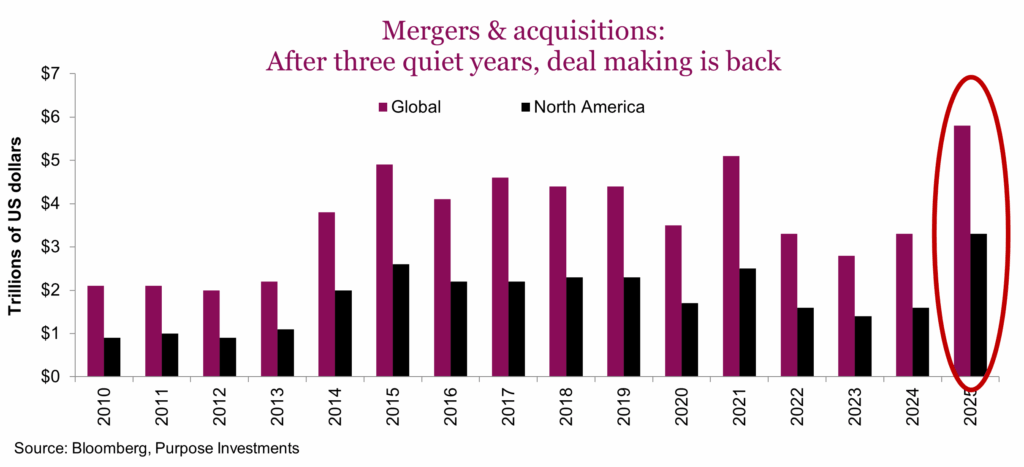

Mergers & Acquisitions – This is another good news story; M&A activity has been picking up. There are few things that help the performance of a small cap name more than being purchased. Deal making was suppressed globally for three years (2022-24) but began to reaccelerate in 2025. We believe this momentum will continue, which is good news for smaller caps.

Final thoughts

On balance, we are a bit more constructive on smaller caps compared to past years. For now, we still prefer some equal weight large cap exposure in the U.S. to partially mitigate the high concentration risk. We’re just not going down the size spectrum at this point. And we are not alone. 2025 saw record ETF inflows with large cap equities absorbing $659 billion, while small cap ETFs suffered about $1 billion of outflows. That does entice the contrarian in us, perhaps if there were a pullback.