Market Ethos

October 20, 2025

Stick to the math

Sign up here to receive the Market Ethos by email.

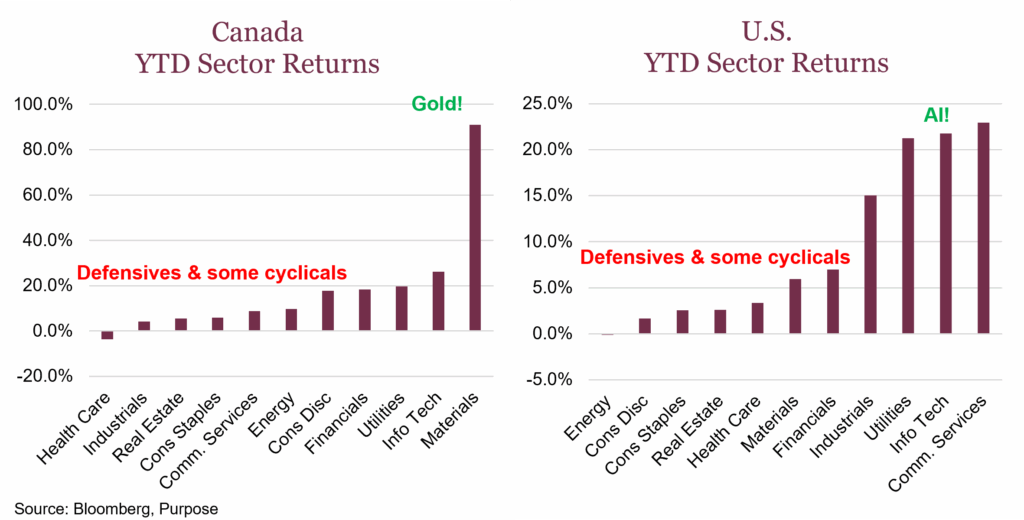

For the first time in what feels like forever, the mighty S&P 500 stalled out last week, failing to hit a new all-time high. Luckily for us north of the border, the S&P/TSX Composite still managed to clear a new precipice, thanks largely to the incredible run in gold prices. The market is increasingly driven by narrative, with returns clustering tightly around a few dominant, easy-to-digest themes. For bull markets, this isn’t necessarily a bad thing — there is, after all, immense strength in a good story.

Right now, in both Canada and the U.S., two market-moving narratives dominate, while many other parts of the market are being ignored, as the chart below illustrates. The two dominant narratives are:

- The AI narrative: Think anything to do with AI and the never-ending data centre buildout. It increasingly resembles a 2025 version of the vendor-financed, infinite-money-printing machine. If AI really does everything that’s promised, many jobs will be lost. Conversely, if the overbuild is a bubble and collapses, lots of people will also lose their jobs. OK, this outlook is probably too pessimistic, but the risk/reward in most of the AI-related names is both binary and extreme.

- Gold: The surge in gold prices is being framed as a dollar debasement trade. However, this isn’t really what the macroeconomic evidence shows. Not all “hard” assets are rising as the debasement theory would suggest, and the narrative implies that developed countries are losing control of their long-term debt, making bonds a terrible investment. With 10-year yields near their lowest level in a year, the debasement narrative loses its grip on reality — but the perception remains strong, so here we are. Gold is now up ~30% over the past two months and over 60% YTD. Debasement or not, anything gold-related is caught up in a strong momentum push.

Narrative-driven markets have one distinct problem: strong stories inherently compromise sound decision-making. We see this dynamic play out for several key reasons.

First, stories simplify complexity. Markets are elaborate systems, but narratives offer straightforward cause-and-effect explanations, such as “AI will transform everything,” or “rates are staying higher for longer.” These simplifications feel coherent and digestible, yet they often gloss over uncertainty and crucial nuance.

Second, feelings become more important than facts. Compelling narratives trigger strong emotions like fear of missing out (FOMO) or regret. Investing becomes much more about how a decision feels, which allows investors to rationalize valuation extremes or contradictory data. Just look at any of the stocks you’re watching right now. It’s the same pattern over and over: stocks sold too early, or those once contemplated, have moved substantially higher. Regret is common, and it drives investors to chase, which is typically not the optimal strategy.

Third, social reinforcement ensures these stories spread easily. They provide great soundbites for the media and are simple to remember. When enough capital chases a good story, prices rise, creating a reflexive loop that seemingly validates the initial story.

Ultimately, investors begin substituting a simple story for rigorous analysis. In investing, all you can really, truly control is your process. Part of a fundamentally sound, repeatable process means diving into the numbers to see what areas of the market are currently pricing in a great story, as well as those whose stories might have been forgotten.

Valuation dispersion

Every valuation is just a number from today multiplied by a story about tomorrow.

Morgan Housel

This quote is simple yet profound. Valuations are just two numbers: prices and earnings. The more optimistic the story about tomorrow, the more investors drive prices higher, increasing valuations to lofty levels. Conversely, the more dire or depressing the story, the more investors sell, depressing valuations.

The U.S. market, for one, is clearly telling a much grander story than it did in the past. Trading at 22.6x blended forward earnings, the market is expensive relative to history. Institutional surveys also suggest U.S. equity valuations remain far too high for comfort. By contrast, the TSX is trading at 17x blended forward earnings, which is cheaper than the U.S. but much more expensive than it was a few years ago. This is where digging into the data becomes critical.

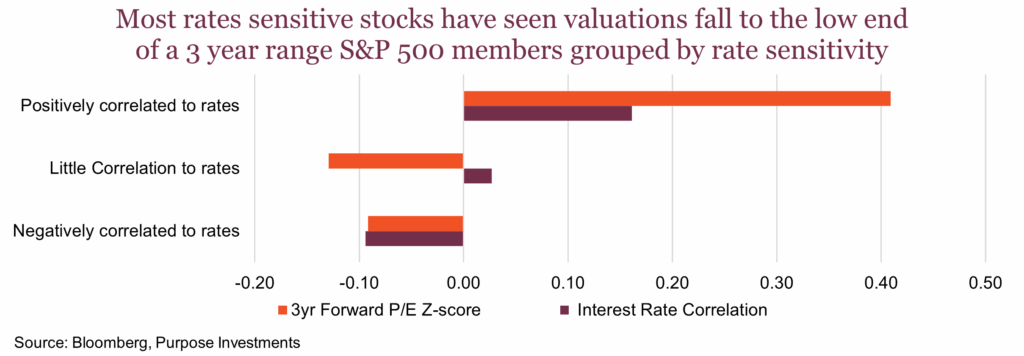

Current valuations show a clear premium on perceived momentum and growth names that often carry low or negative sensitivity to interest rates. Most lower-risk/defensive sectors fundamentally tied to interest rates, however, have been systematically punished, as seen in the chart below.

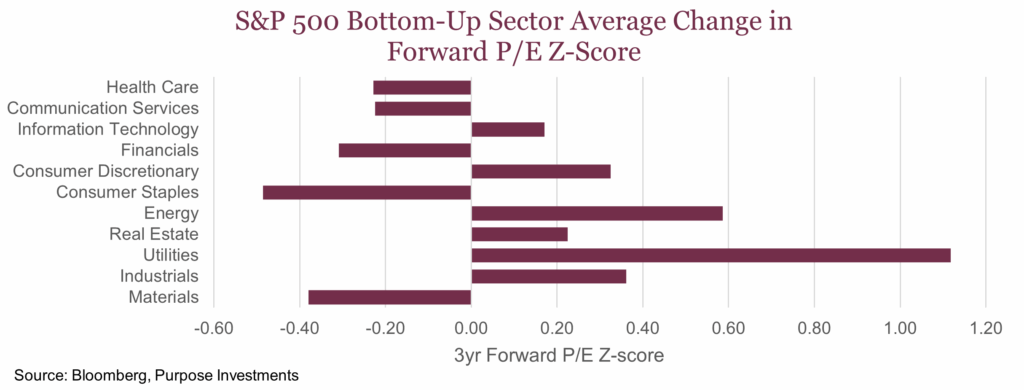

When we analyze sectors based on their valuations, z-scores are useful — they measure how rich or cheap a company or sector is relative to its own historical average. Digging into current valuations, a certain trend emerges. The market is not rewarding sectors based on interest rate sensitivity, despite both the Bank of Canada and Federal Reserve cutting rates and longer-term bond yields falling steeply over the past few months. Most rate-sensitive sectors have underperformed by a wide margin this year.

The exception is Utilities, which have divorced their rate-sensitive brethren (Staples, REITs, Telcos) and are now actively part of the dominant AI narrative. Trading at a z-score of 1.12, the sector is full of stocks trading at an excessive premium due to the incessant power demand from the AI data centre buildout. In fact, based on its own history, the Utilities sector is now more expensive than the broader growth engine.

The real deep value lies in sectors that are boring, cyclical, or simply overlooked, irrespective of their rate sensitivity. The truly “cheap” assets, those trading at a historical discount (negative z-score), are Consumer Staples, Financials, Health Care, Materials, and Telecom stocks. For the most part, this all makes intuitive sense. It’s been a risk-on market, and most defensive stocks have gone out of favour.

We believe U.S. Financials are interesting. They’ve been on a good run, but valuations are actually not as stretched as you would assume. In fact, U.S. insurance names rank among the cheapest industries relative to their own history.

Focusing on the cheapest names reveals a core thesis: the last pockets of value are primarily tied to rate sensitives (e.g., Utilities), which the market has written off in favour of pure growth plays. We believe these historically defensive sectors have been so out of fashion that their current positioning makes them a strong contrarian option against pervasive bullish, momentum-fuelled sentiment in a well-diversified portfolio.

Final thoughts

In an environment where narrative commands an absurd premium, the only reliable way to find value is to skip the compelling story and just stick to the math. This is the market’s last safe bargain, hidden almost entirely in sectors directly impacted by interest rates (which have been falling) or those simply deemed “safe or boring.”

Sometimes, the best opportunities come not from chasing a story, but from stepping back and recognizing the value in what’s been overlooked. The market and media might adore narratives, but for disciplined investors, sometimes boring is the best strategy.