Market Ethos

July 22, 2024

Why it’s good to be Canadian

Sign up here to receive the Market Ethos by email.

Building on our July 8 Market Ethos – Bonds-equities: Diversification is harder to come by– this edition goes searching for diversification in a more correlated world. The stock-to-bond correlation is at the core of multi-asset portfolio construction, and from 2000 to 2020, it was negative. This makes the portfolio construction process much easier and allows you to enjoy decent returns with less risk or volatility. However, over the past few years, we have seen a dramatic rise in stock-bond correlations, which is a clear challenge for portfolios. 2022 was a tough year as both stocks and bonds fell simultaneously. And while nobody seems to be complaining about stocks going up and bonds doing okay, correlations have continued to climb.

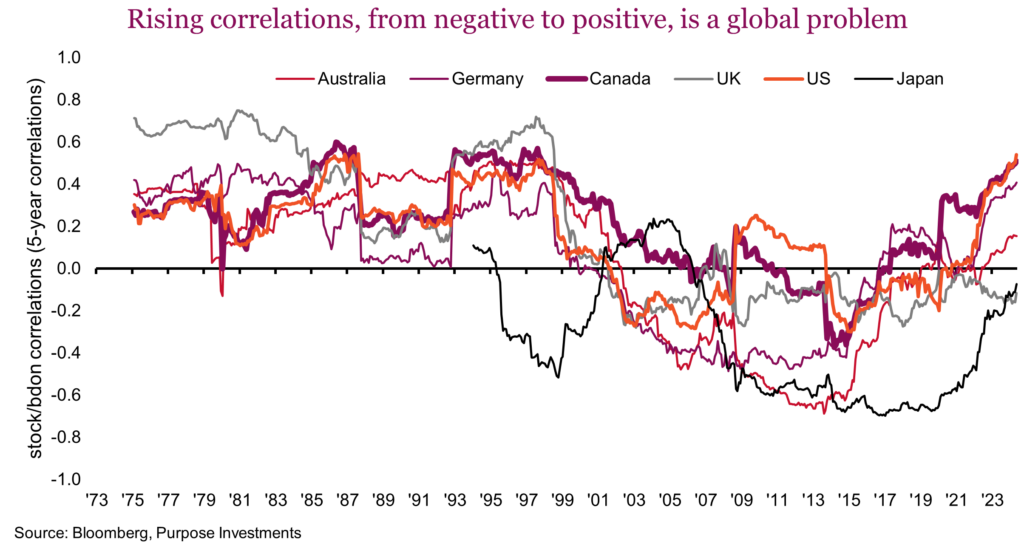

The vast majority of published content on this topic is very U.S.-centric, focusing mainly on the U.S. stock market and U.S. bond market. But we are Canadians, and proudly so. Being Canadian is actually a good thing, which we will explain shortly. But first, let’s look to see if this higher correlation problem is a global issue. The bad news is that it isn’t just the U.S. or Canada. Bond/equity correlations have risen substantially in most developed markets. The chart below includes a few other major markets; clearly, the trend is towards higher correlations. We would note this is a 5-year rolling correlation, so even though Japan may look like it still enjoys negative correlations, based on that upward trend, recent data is clearly positively correlated.

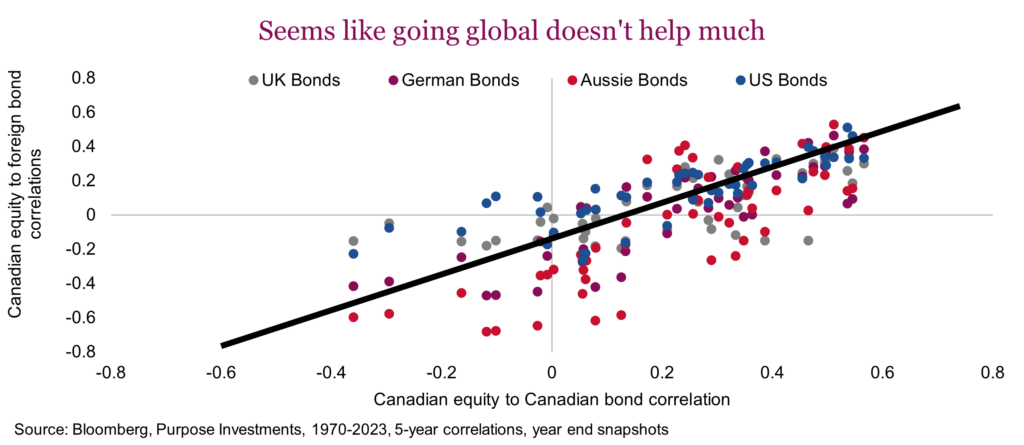

These are all domestic paired correlations of a country’s stock and bond market. But can we, as Canadians, lean on foreign bond markets to find some diversification? Unfortunately, since most developed market correlations move together, this does not seem to be a great source of diversification when you can’t get much from your domestic market. The following scatter chart shows year-end points of 5-year correlations. Across the x-axis is the Canadian equity to bond correlation, and the dots are correlations of Canadian equities to foreign bonds.

While there may be some benefits to going global when equity/bond correlations are closer to zero in Canada, during periods of strong positive or negative correlations, everyone appears to be in the same boat. Given that we live in a more strongly positively correlated world today, going global probably doesn’t help too much.

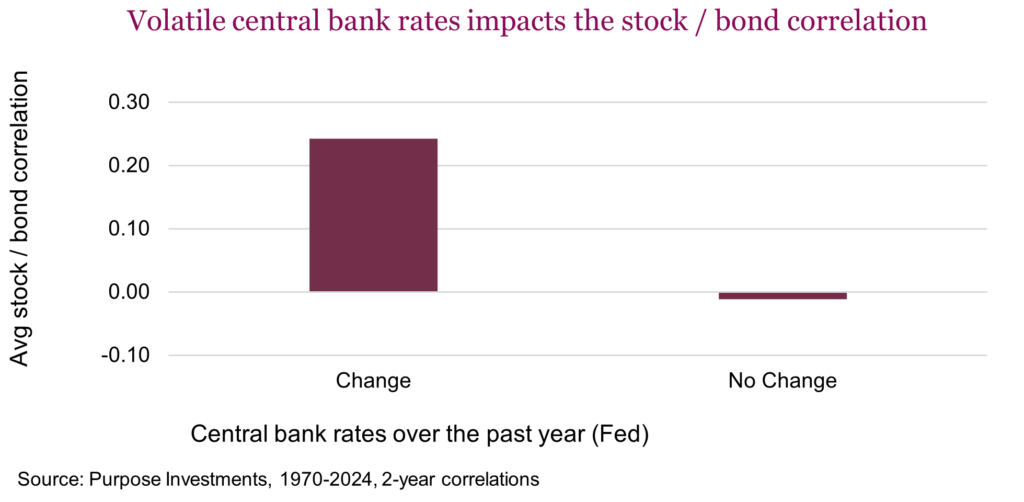

With most developed market bond/equity correlations moving higher together, it does provide evidence that this change is likely driven by global factors instead of country-specific factors. Inflation, specifically inflation volatility, appears to be a large contributor to correlations. Central banks tend to become much more active in changing overnight lending rates when inflation is on the move. Just in case you have missed the last couple of years, the latest bout of inflation saw the Fed Funds rate go from 0.25% to 5.5% in a mere 18 months.

Even in the longer term, a strong relationship exists between central banks’ changing rates and the equity/bond correlation. We are not implying causation. We’re simply highlighting that central bank rate changes occur when inflation is volatile. Regardless of who is to blame or if anyone is to blame, over the past 50 years, during periods when central banks have been more active with policy, equity/bond correlations tend to be higher. Given inflation is now fading, we are likely entering another bout of more active central bank rate changes. This would continue to support equity/bond correlations to remain elevated.

Look harder

So, if bonds will be harder pressed to deliver that sweet diversification-smoothing factor for portfolios, what does it all mean? First off, bonds will work again if economic growth falters; we are very confident of this. So they are not broken, they are just not as ‘diversifying’ as they used to be. And given higher yields, there is the silver lining of higher expected returns from bonds. Perhaps investors could just suck it up and accept we are in a world where portfolio volatility will be higher than in the previous couple of decades. That is one option.

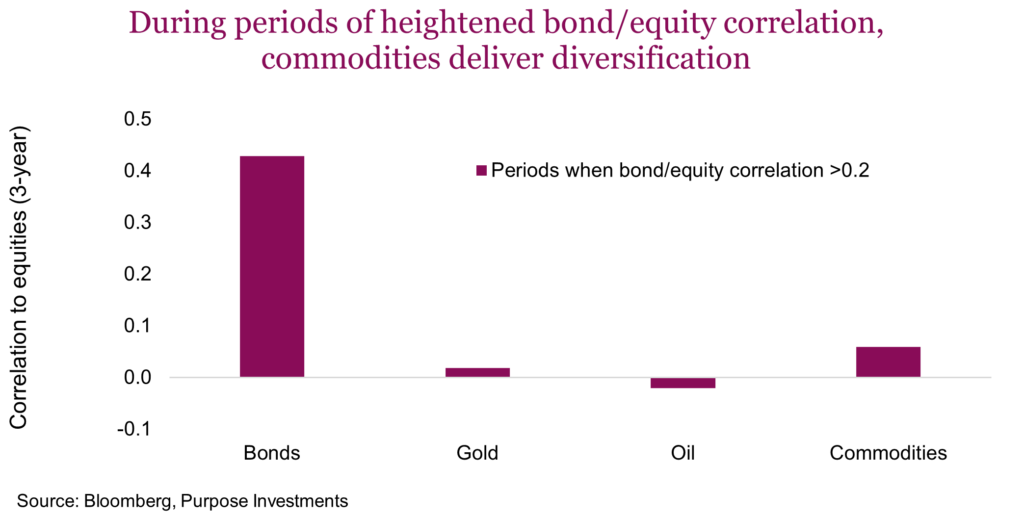

But could we find some diversification from other sources? This is where it gets good to be Canadian. Switching back to U.S. bond/equity correlations for a moment, we looked at what provided diversification during historical periods of elevated correlations. Emerging market debt and equities provided a little, but it wasn’t great. But what really helped was commodities, specifically oil, gold, or even the broader commodities index.

Looking at periods when the equity/bond correlation was elevated, over 0.2, bonds are not providing much diversification. During those periods, though, gold, oil, and commodities generally do. While encouraging, this does come with added costs and much higher absolute volatility. Bonds have a historic volatility (annualized standard deviation based on monthly performance) of around 5-6%. The broader commodities index is around 17%, gold 19% and oil 36%. If you decide to lean into these ‘diversifiers,’ don’t get carried away, as you are adding absolute risk at the same time.

This is where it’s nice to be Canadian. The TSX has a good amount of energy, gold, and broader commodities built into its composition. And while we do not like to focus on one year, it is worth noting that in 2022 when stocks and bonds were falling together, the TSX was one of the best equity markets globally.

Final thoughts

The bad news is that equity/bond correlations across developed markets often move in tandem, so it is harder to lean on international diversification to help out. And with central banks changing rates globally, this time in the downward direction, this higher-correlated world may persist. Commodities continue to offer a good source of diversification but with a much higher risk profile. That being said, a small addition may provide a larger portfolio impact. Clearly, they’re best used sparingly.

The silver lining may be Canada, as the TSX is a commodity-tilted equity market. So, this does provide some built-in commodity-like diversification.