Sign up here to receive the Market Ethos by email.

The April correction was caused by policy, or rather changing policy. We had to look pretty far back to find other corrections that were policy-induced mainly because over the past 30ish years, policy has been ubiquitously supportive of markets. If Mr. Market got in too much trouble, policy came to the rescue. And if policy was implemented outside periods of market stress, they tended to be supportive or at least not disruptive.

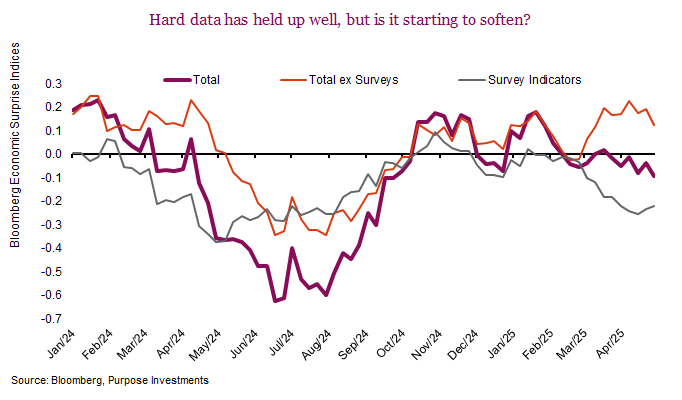

Looking at past policy-induced corrections, they tend to resolve quickly. Largely because the market adjusts to whatever the new rules are and then resumes what markets do. Another interesting characteristic of past policy corrections is that the economic data remains resilient for a longer period. In a normal correction induced by the economy, sentiment data erodes, fast economic data then slows and then this spreads to the slower hard economic data. The policy disruptions process takes longer which is what we are seeing today.

There is a high probability that the economic and earnings data year-to-date has been helped by the tariff uncertainty. Shipping volumes spiked higher ahead of the tariff risk as importers endeavoured to bring in goods to the U.S., ahead of the constantly moving tariff deadline. This also likely boosted industrial production, and it may also be evident in consumer spending.

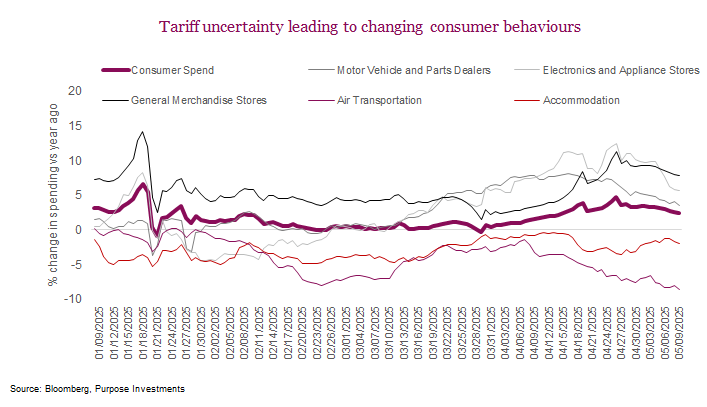

Based on daily credit and debit card transactions, the U.S. consumer appears in aggregate to be holding up nicely (thicker purple line), up about 2.4% year-over-year. But over the past month it has been really helped by goods spending in electronics, autos and general merchandise. The categories that could see tariff induced price increases. Meanwhile, spending on leisure has been very weak, including air transportation and accommodation.

Could the fear of tariffs have caused the consumer to try and pick up goods sooner rather than later? If so, that could spell a reversion down in the coming months that may be starting to take hold. This could be the case for containerships and industrial production.

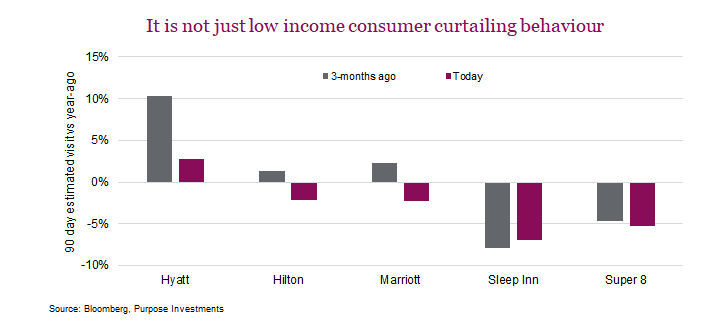

Accommodation is an interesting one. The norm over the past year has been that the higher income consumer was healthy and spending and the lower end was having troubles, given inflation. Breaking down several national hotel chains, it would appear the pain is now moving up the income spectrum. The chart below shows the change in estimated visits to various chains on a year-over-year basis, looking at the pace three months ago and today. The lower cost hotels have been suffering for a while. But even the higher-end hotels (Hyatt, Hilton, Marriott) are now seeing an erosion in visits.

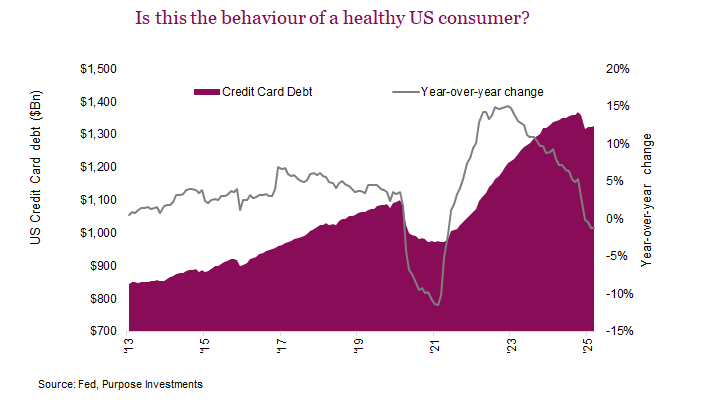

As further evidence the U.S. consumer may be running low, we turn to credit card data. Now this has been an interesting trend because COVID caused many to migrate to a more cashless world. As a result, the aggregate credit card debt rose substantially. But this was more a behaviour change in the choice of payment options. The challenge of late is that spending on cards is starting to contract. Just a bit so far, however this could be a sign the consumer is more tapped out.

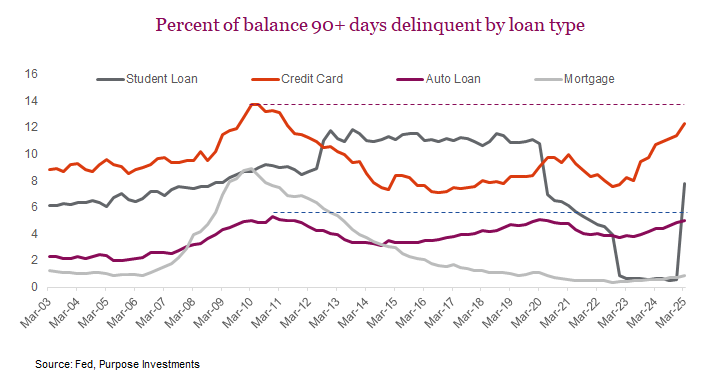

More disturbing is delinquencies. This is the percentage of balances that are 90+ days delinquent by category. We will ignore student loans as those have been odd given changing legislation in the U.S. Mortgage delinquencies are very low, however, credit card delinquencies are getting close to the peak levels following the great financial crisis. And this has happened with a supportive labour market and no recession. Auto loans are also seeing rising delinquencies. Inflation and high rates are clearly taking a toll on the consumer, and it is starting to show up more and more.

Final thoughts

The U.S. consumer has a long history of finding ways to keep spending. We believe the saying goes if they earn $1, they spend $1.20. Still, they do appear to be waning or at least losing momentum at a time when wage growth is good and the labour markets are decent. Neither policy uncertainty nor DOGE efforts have helped. This does appear to be further evidence supporting a potential economic growth scare in the coming months or quarters. Or at the very least a very selective approach in the consumer discretionary space.

Source: Charts are sourced to Bloomberg L.P., Purpose Investments Inc., and Richardson Wealth unless otherwise noted.

The contents of this publication were researched, written and produced by Purpose Investments Inc. and are used by Richardson Wealth Limited for information purposes only.

*This report is authored by Craig Basinger, Chief Market Strategist at Purpose Investments Inc. Effective September 1, 2021, Craig Basinger has transitioned to Purpose Investments Inc.

Disclaimers

Richardson Wealth Limited

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson Wealth Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.

Purpose Investments Inc.

Purpose Investments Inc. is a registered securities entity. Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Neither Purpose Investments nor Richardson Wealth warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise.

Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice.

The particulars contained herein were obtained from sources which we believe are reliable but are not guaranteed by us and may be incomplete. This is not an official publication or research report of either Richardson Wealth or Purpose Investments, and this is not to be used as a solicitation in any jurisdiction.

This document is not for public distribution, is for informational purposes only, and is not being delivered to you in the context of an offering of any securities, nor is it a recommendation or solicitation to buy, hold or sell any security.

Richardson Wealth Limited, Member Canadian Investor Protection Fund.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.

Related articles

Market Ethos

Buy the dip … anyone?

30 March 2026. Market Ethos. As the Middle East conflict continues to evolve, this market is starting to become increasingly fragile, and continues to adjust…

23 March 2026. Market Ethos. As hostilities broke out in the Middle East, markets were initially rather resilient. But after three weeks, that resilience is…

12 March 2026. Market Ethos. Over the past three decades banks have delivered standout returns. But with valuations pushed higher, the question now is: How…