Market Insights

October 30, 2025

“Debasement” is trending: What is driving the conversation

Sign up here to receive the Market Ethos by email.

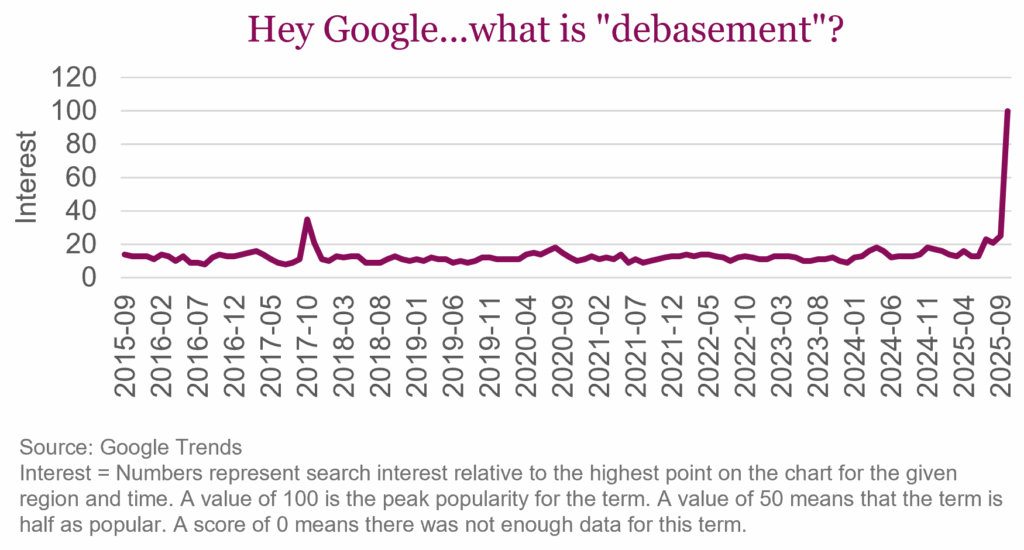

If Google search data offers any signal of investor sentiment, “debasement” may have officially gone mainstream. Searches for the term surged in October 2025, reflecting broader questions about the value of money. Historically, “debasement” referred to the process of reducing the intrinsic value of currency, most often by decreasing the precious metal content of coins. Today, it captures a broader anxiety about the erosion of purchasing power of fiat money and the view that policy decisions, debt burdens, and persistent inflation are quietly contributing to it.

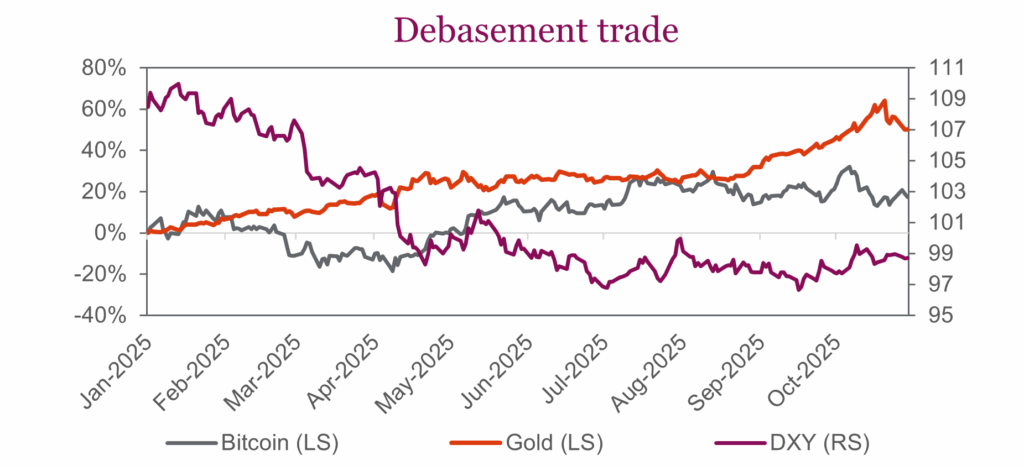

This sentiment has underpinned the modern “debasement trade,” where investors shift away from government issued currencies like the U.S. dollar and into assets viewed as stores of value like gold and other commodities, and, for some, cryptocurrencies.

So far, markets have reflected that mood. Gold is up roughly 50% year-to-date (Oct 28, 2025), reaching record highs above US$4,000 per ounce before easing slightly, while Bitcoin has climbed nearly 20%, buoyed by a mix of expectations of easier policy and unease over long-term currency stability. The U.S. dollar, meanwhile, has weakened by about -9%, weighed down by narrower rate differentials, slowing U.S. growth, and mounting fiscal concerns. Together, these moves suggest the “debasement” trade is not just a niche narrative but a visible market theme.

Why it’s gaining momentum

The momentum behind the debasement trade stems from various interconnected pressures such as government debt, economic fragmentation, inflation, and policy credibility.

1. Unsustainable debt level

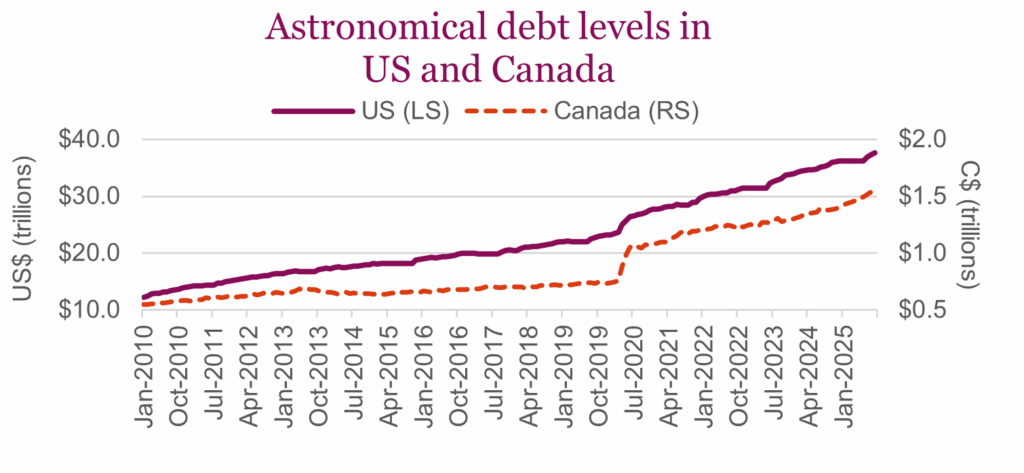

Public debt has ballooned to levels that test the limits of fiscal credibility. The U.S. government’s obligations now exceed $37 trillion, with interest costs rivaling defense spending. In past cycles, robust growth could help offset heavy debt, but that’s harder today given aging demographics, weaker productivity (whilst AI adoption can counter), and slower global trade. These structural headwinds make it hard to “grow out” of debt. Meanwhile, persistent post-pandemic spending on defense and healthcare has kept deficits high even during periods of growth. With deglobalization and re-industrialization raising costs, higher inflation risks and subsequently costlier borrowing, are making debt management increasingly difficult.

In Canada, borrowing needs are likely to stay elevated as Ottawa plans to finance long-term investments in housing, infrastructure, defence, and supply-chain resilience, amid growing pressure to diversify export markets and reduce reliance on the U.S. The trade-off is higher headline debt in the near term to strengthen resiliency and support long-run growth capacity.

2. Economic and geopolitical fragmentation

The weaponization of trade and finance through sanctions, tariffs, and export controls, has accelerated efforts to diversify away from the U.S. dollar. Countries such as China, India, and Russia have expanded trade settlements in local currencies and increased gold reserves as a hedge against financial coercion. Gold’s appeal lies in its neutrality and lack of counterparty risk, qualities that stand out in a world of political and economic divides.

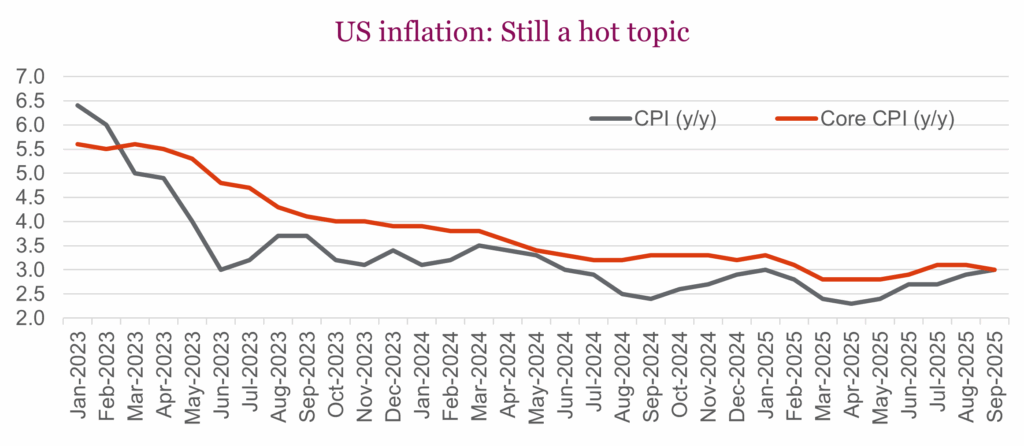

3. Inflation as a persistent tailwind

While headline inflation has cooled, underlying pressures remain. Reshoring and local-content rules, defense spending, and energy transition projects will structurally raise input costs. Even if inflation only runs a bit above target, that mix keeps real returns uncertain and pushes investors toward assets that help preserve purchasing power. Even moderate inflation above central bank targets could keep investors searching for protection in hard assets.

4. Central bank independence

Years of extraordinary monetary accommodation have blurred the lines between fiscal and monetary policy. Central banks, once viewed as apolitical guardians of price stability now face growing political pressure to support growth. The pandemic-era bond-buying programs reinforced that dependence, as governments came to rely on cheap financing for large deficits. This dynamic has weakened one of the traditional anchors of currency stability.

What it means for markets

Some would argue that the usual anchors of currency stability such as moderate debt, global cooperation, and central bank independence are less secure today. With aging populations, heavy debt loads, and rising geopolitical strain, the policy toolkit may be more limited than it used to be. Against this backdrop, the debasement trade can be seen as both a hedge and a signal. As a hedge, assets like gold help preserve purchasing power when inflation risks, fiscal stress, or currency weakness rise. As a signal, flows into these assets can point to waning confidence in policy credibility and growing concern about debt, inflation, and geopolitics.

Gold and other precious metals have drawn interest for their neutrality, scarcity, and relative liquidity. Cryptocurrencies, despite volatility, a short track record, and uneven regulation, are also attracting attention as digital stand-ins for stores of value. Even so, none of this removes the risk of sharp reversals or valuations outrunning fundamentals. As with any investment, exposure should align with objectives, time horizon, liquidity needs, and risk tolerance, with sizing and entry points guided by valuation rather than headlines. This helps explain recent strength in gold and cryptocurrencies, but it also reflects a simple reality: the U.S. dollar remains the cornerstone of global finance even as the conversation about what gives money its value continues to evolve, and markets and policymakers take notice.

Source: Charts are sourced to Bloomberg L.P., and Richardson Wealth unless otherwise noted.

Authors: An Nguyen, VP Investment Services; Phil Kwon, Head of Portfolio Analytics; Andrew Innis, Analyst

Disclaimers

Richardson Wealth Limited

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson Wealth Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by the author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Richardson Wealth does not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise.

Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice.

The particulars contained herein were obtained from sources which we believe are reliable, but are not guaranteed by us and may be incomplete. This is not an official publication or research report from Richardson Wealth, and is not to be used as a solicitation in any jurisdiction.

This document is for informational purposes only, and is not being delivered to you in the context of an offering of any securities, nor is it a recommendation or solicitation to buy, hold or sell any security.

Richardson Wealth Limited, Member Canadian Investor Protection Fund.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.