Sign up here to receive the Market Ethos by email.

Summary: Earnings are all that matter for markets in the long run. As we head into Q3 earnings season, attention should be focused on margins given cooling inflation (a negative for sales growth) and cooling cost inflation (a positive for margins). More importantly, global earnings estimates have been cooling – an unsustainable trend given most index prices keep rising. Corporate hints at the future will drive the next move in earnings revisions. Listen closely.

Over time, equity markets go up because earnings go up, and earnings go up because the economy expands. Sure, the market moves up and down more than earnings as the market multiple (PE ratio or valuations) fluctuates given investor mindset, risk, outside factors, interest rates, etc. The economic relationship to earnings is loose too as operating and financial leverage influences the equation. Yet all these other ‘noise’ factors tend to mean revert over multi-year time periods, leaving a direct relationship between markets and earnings. So clearly today’s earnings matter as we head into Q3 earnings season, but tomorrow’s earnings do too.

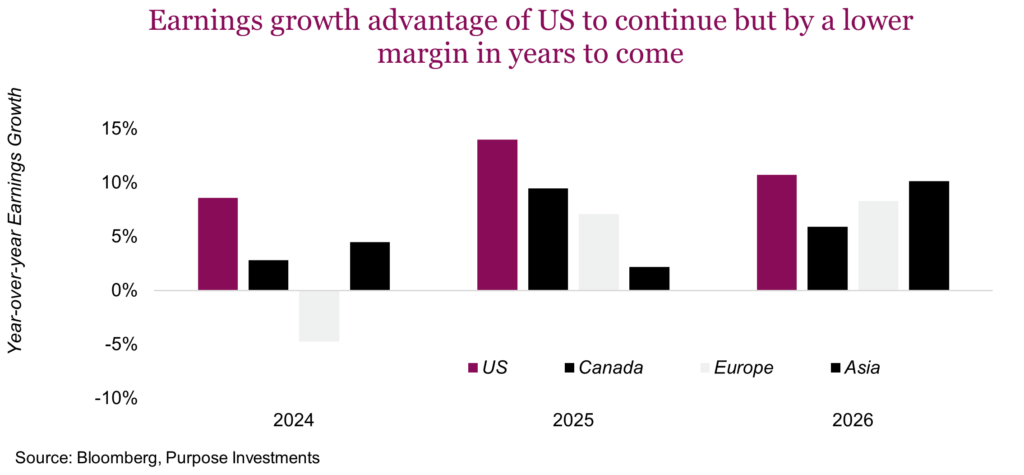

Is the S&P expensive at 21.8x estimated earnings for the next 12-months? And is Canada actually cheap at 15.3x? It is not just what you are paying for current earnings but how those earnings will grow over time. The S&P has been more expensive for years and has outperformed, mainly because it has enjoyed strong earnings growth. In 2024, U.S. headline earnings were just under 10%, this rises next year. Canada has seen pretty low growth in 2024 with some better growth expected for next year. Europe and Asia are cheaper than the U.S. and even a bit cheaper than Canada, with less earnings growth over the coming years.

Markets tend to move on new information, so this coming earnings season and future seasons contain a ton of information from companies on how their businesses are running. The big question will be whether the U.S. will be able to attain that lofty 14% earnings growth into 2025 … or exceed it.

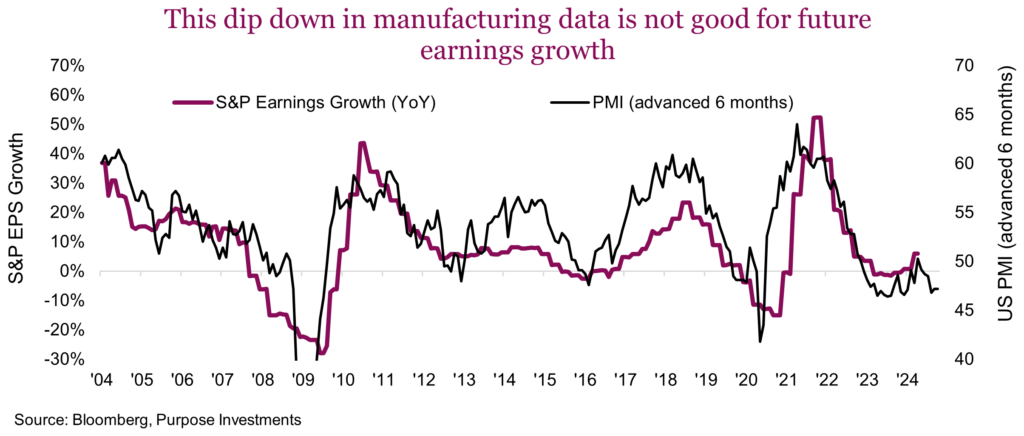

While the overall economy may drive earnings growth, manufacturing economic activity does have an outsized weighting for S&P 500 earnings. This may pose a problem. There is a strong relationship between the monthly survey of manufacturing activity (PMI) and earnings growth six months into the future, showing a 0.7 correlation. During the past couple of months we have seen a drop in the PMI manufacturing survey, which may imply a softening pace for earnings growth. Directionally, this is a pretty strong relationship so it may be a challenge for the S&P to post increasing earnings growth into 2025 as current consensus estimates imply manufacturing activity is slowing.

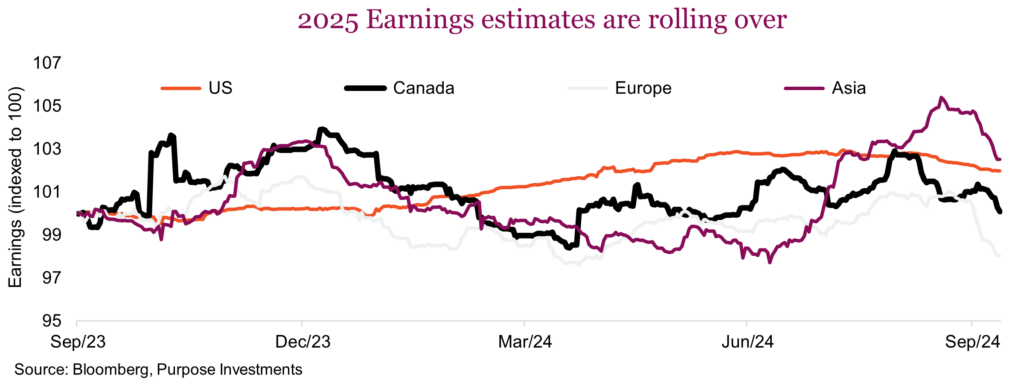

On an equally sobering note, the positive earnings revision trend of previous months appears to have reversed, even for the mighty U.S. equity market. The optimism for 2025 earnings appears to be cooling across the board.

There are some good news factors however. Even though inflation is cooling, measured via CPI, producer prices are cooling faster. That may help keep profit margins at healthy levels. Wage pressures appear to be softening as well – good news on the cost side for many corporations. Perhaps the biggest piece of good news is falling overnight rates as central banks gradually move back to whatever normal rates will be. This helps keep some upward pressure on the market multiple, or what the market will pay for a $1 of earnings.

Final thoughts

It is challenging to bet against corporations – they are very good at managing expectations, managing rising costs and delivering. However, much of the markets’ rise over the past few years lines up really well with whichever market was enjoying the best earnings growth. Given that current estimates for 2025 favour the U.S. market for growth over others, perhaps U.S. exceptionalism will continue. However, the U.S. is priced for near perfection, which raises the risk of reality falling short of estimates.

This earnings season will be critical to see if companies are still largely able to manage their way through variations in inflation, costs, wages, interest rates and all the other moving parts.

Source: Charts are sourced to Bloomberg L.P., Purpose Investments Inc., and Richardson Wealth unless otherwise noted.

The contents of this publication were researched, written and produced by Purpose Investments Inc. and are used by Richardson Wealth Limited for information purposes only.

*This report is authored by Craig Basinger, Chief Market Strategist at Purpose Investments Inc. Effective September 1, 2021, Craig Basinger has transitioned to Purpose Investments Inc.

Disclaimers

Richardson Wealth Limited

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson Wealth Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.

Purpose Investments Inc.

Purpose Investments Inc. is a registered securities entity. Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Neither Purpose Investments nor Richardson Wealth warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise.

Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice.

The particulars contained herein were obtained from sources which we believe are reliable but are not guaranteed by us and may be incomplete. This is not an official publication or research report of either Richardson Wealth or Purpose Investments, and this is not to be used as a solicitation in any jurisdiction.

This document is not for public distribution, is for informational purposes only, and is not being delivered to you in the context of an offering of any securities, nor is it a recommendation or solicitation to buy, hold or sell any security.

Richardson Wealth Limited, Member Canadian Investor Protection Fund.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.

Related articles

Investor Strategy

Navigating the fog

October 8, 2024. Investor Strategy. Though markets wobbled at the start of the month, risk appetite and optimism came back. The path ahead remains uncertain;…

September 30, 2024. Market Ethos. Following a global market rally spurred by a recent Fed rate cut, China introduced a significant stimulus package to counter…