Market Ethos

January 13, 2025

Things used to be easier

Sign up here to receive the Market Ethos by email.

Summary: In this Ethos, we explore a different lens for viewing yield solutions for a portfolio. Given most yield-providing allocations are also expected to provide some portfolio defense, we have shared a risk-adjusted yield framework to help consider different yield strategies for a portfolio.

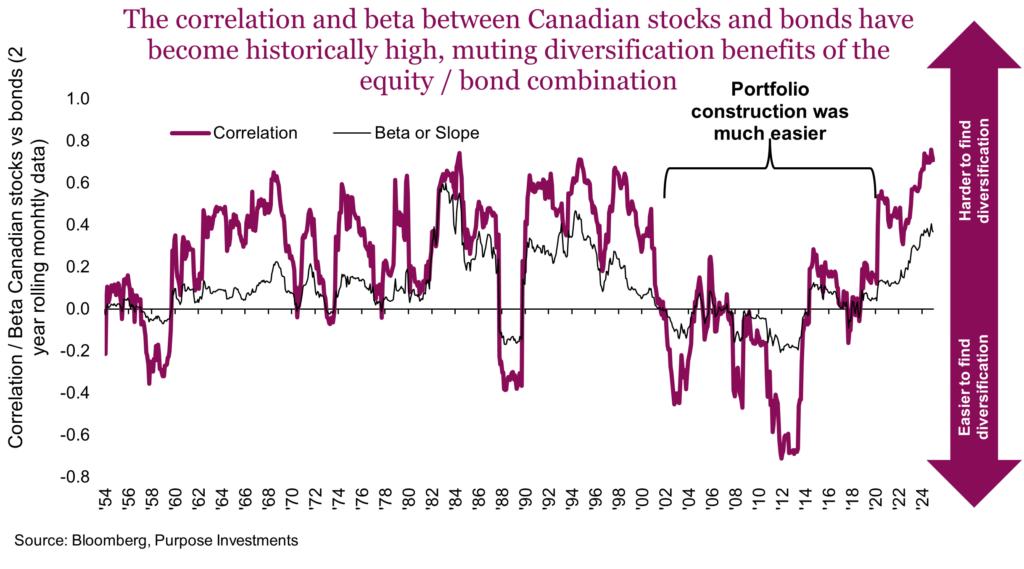

In simpler times, portfolios were constructed by combining equities and bonds. Equities provided much of the capital appreciation or growth for the portfolio, while bonds offered some income and acted as a ballast or portfolio stabilizer during those troubled times when the equity growth driver fell. As the markets evolved and the available investment strategies expanded, things become less simple.

We all lived through this evolution. In the 1990s, equities really enjoyed increased popularity as a driver of capital appreciation. Before this, individual equity ownership was much lower. In the 2000s, value and dividends became a dominant factor. In the 2010s, with yields continually moving lower, investors turned to a multitude of different yield producing strategies to compensate. Moving down the credit spectrum, getting more exotic in instruments or geographies, option/derivative income generators and of course dividend focused equity strategies.

This demand for higher yield source diversification for portfolios has only increased during the past few years given the heightened correlation between equities and bonds. Higher correlation means the defensive or stabilizing portfolio contribution from bonds has diminished. The silver lining being higher yields now make bonds a larger contributor to portfolio yield and potentially portfolio performance. As with everything, there always seems to be a tradeoff.

The same tradeoffs often apply to different sources of yields. For instance, today the broader Canadian bond universe (based on ETF) has a yield of about 3.4%. Meanwhile, shares of BCE Inc. have a dividend yield of 12%. Can you compare these two sources of yield? Let’s ignore the tax difference for a moment. Obviously, a single company carries more risk than the overall bond market. Remember the non-equity portion of the portfolio was designed to provide some income and some stability – a dual role. So let’s look at yield on a risk-adjusted or more specifically a downside risk-adjusted basis.

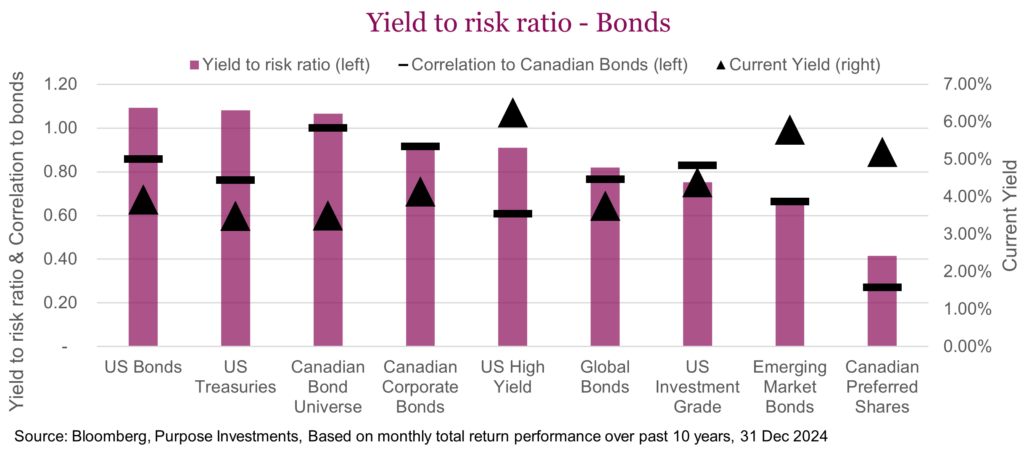

Yield to risk ratio – The Sortino ratio is a common metric that measures return relative to downside deviation – a measure of downside risk below a certain level. Often this level is set at zero, so only being penalized for negative monthly returns. The more common standard deviation penalizes for both up and down side volatility, but who doesn’t like upside volatility. The yield to risk ratio is similar to Sortino, measuring the current yield of an investment relative to its historical downside risk. As a result, it provides a downside risk adjusted yield ratio. The higher the yield, the higher the score. The higher the risk, the lower the score.

Given that the role in a portfolio of most yield providing strategies is both income and portfolio stability, this offers a combined lens for this dual objective. The chart below shows a number of different bond strategies, based on available ETFs, with their respective yield to risk ratio and the current yield.

While emerging market bonds and Canadian preferred shares have some of the highest yields, they do not stack up well on a risk adjusted basis. For investors in these asset classes, that may bring back some painful memories. Plain old bonds, both Canada and U.S., both stack up pretty well on a risk-adjusted yield basis.

Another factor to consider when using multiple sources of yield in a portfolio is how they are correlated. Given traditional bonds may have muted defense in a more correlated world, ideally we would want a lower correlation to bonds. Preferred shares may not stack up well from a yield to risk ratio but they do provide a very different performance than the bond market. So does high yield.

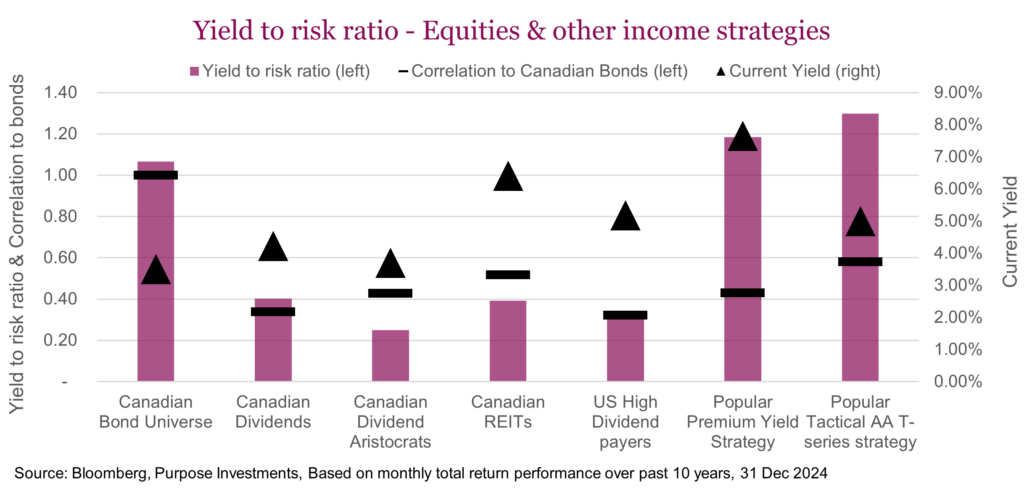

But yield is now being sourced from many areas outside the bond universe. The following provides the same metrics for a number of dividend focused ETFs and other income oriented strategies. The benefit of going outside the normal bond arena, strategies can be found that provide yield and different styles of defense.

Clearly there are attractive yields available in the equity dividend space, however the defensive characteristics are lacking. They may often be called ‘bond proxies’, but that is a loose proxy. On a positive note, the proliferation of differentiated yield-generating strategies has created many other options to better diversify a portfolio’s yield sources.

Two important notes – tax and growth. It is somewhat unfair to compare yields on a pre-tax basis and some allowance should be considered for after tax yields. Of course tax-sheltered accounts don’t care. And then there is growth. The equities likely have a growth component and the ability to grow dividends. Those are very positive characteristics that must be considered separately.

Final thoughts

Today, a portfolio’s yield is generated from many different sources and types of investments, well beyond bonds. Having a well-diversified yield has become even more important in a higher correlated world, as relying on one or two sources may prove risky. The good news is there are many sources of yield in the market, thanks to higher rates and the industry’s ability to innovate. When adding these different sources, give consideration to a risk-adjusted yield framework – this is often a key component of the portfolio that should perform well in terms of defense.

It may not be a simpler time, but it sure is more interesting.