Investor Strategy

April 2025

Facts vs feelings

Sign up here to receive the Market Ethos by email.

- March was not tariff-ic

- Hard or soft

- Will the soft data transmit to the hard data?

- Market cycle & portfolio positioning

- Final note

We believe an overreaction may occur in the coming months from economic data softness. This level of uncertainty is causing behaviours to change for consumers and companies. This may start manifesting in the data going forward. It is already evident in much of the soft data that is more sentiment driven. If this transitions to the hard economic and earnings data, that may create the best buying opportunity of 2025.

March was not tariff-ic

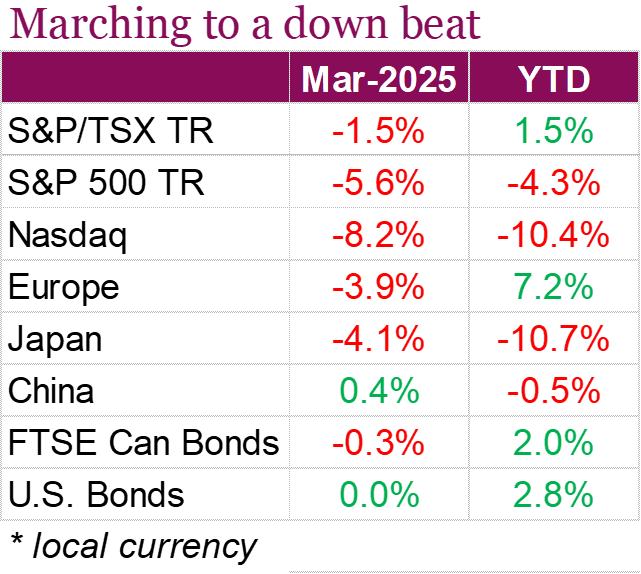

If the first quarter was to be defined by one word, it would be ‘tariffs’, or probably better put, ‘tariffs?’. Trump started his second term in office by threatening, then postponing, then threatening tariffs, leaving investors on edge about what the future of global trade will look like. Investors certainly didn’t appreciate all the flip flopping, which raised market volatility and pushed U.S. indexes into correction territory. Cracks in the U.S. exceptionalism theme which began to surface this year have pushed many investors to look elsewhere for returns. All told, the S&P 500 fell -5.6% on a total return basis in March, leaving the index now down -4.3% YTD. There has been a noticeable shift in sentiment, with the names that dominated headlines last year now among the largest detractors. The Nasdaq is down over -10% YTD, dragged down by the “Magnificent 7”, with an index that tracks those names down -16% for the year. The lacklustre performance from U.S. equities is especially surprising given how much euphoria there was surrounding Trump’s election win and what he would do to markets. Instead, investors have looked elsewhere, with Europe and Hong Kong remaining the standouts for the year. While the Euro Stoxx 50 index fell -3.8% in March, it is still up 7.7% YTD on a total return basis. The Hang Seng continued to climb in March, rising 1.1% and sitting 16.1% higher on a total return basis YTD.

While Canada has been in Trump’s crosshairs ever since taking office, Canadian equities haven’t suffered the same fate as U.S. equities. The TSX was down -1.5% in March, however, managed to stay in the green year-to-date and is- up 1.5% on a total return basis, helped by the materials sector which is up nearly 20% since the beginning of the year. Trade policy uncertainty caused the BoC to cut rates in March, with the central bank cutting its key interest rate by 25 bps to 2.75% on March 12. Officials noted that the Canadian economy looked strong heading into 2025, however, faced with deteriorating consumer and business sentiment, the central bank opted to cut. Following the decision, data showed that Canada’s economic growth stalled in February according to preliminary data, with GDP remaining flat after a strong 0.4% expansion in January. This slowdown would put first-quarter annualized growth at 2.1%, down from 2.6% in the previous quarter. Also, on the political front, Canada got a new leader in March, with Mark Carney taking the reins and being sworn in as Prime Minister, who then called an election for April 28, just nine days after taking office.

In the wake of market uncertainty in the first quarter, investors looked to diversify and flocked to safe haven assets. Gold has been the standout, rallying 9.6% in March and is now up 18.2% YTD, reaching new all-time highs along the way and blowing past $3000/oz. Bonds have also been a source of protection for investors, with the U.S. Aggregate Bond Index now up 2.8% year to date and the FTSE Canada Universe Bond Index up 2% for the year. One safe haven asset that’s looking a little less safe appears to be USD, with the U.S. Dollar Index (DXY) down -4.7% YTD as recession concerns rise.

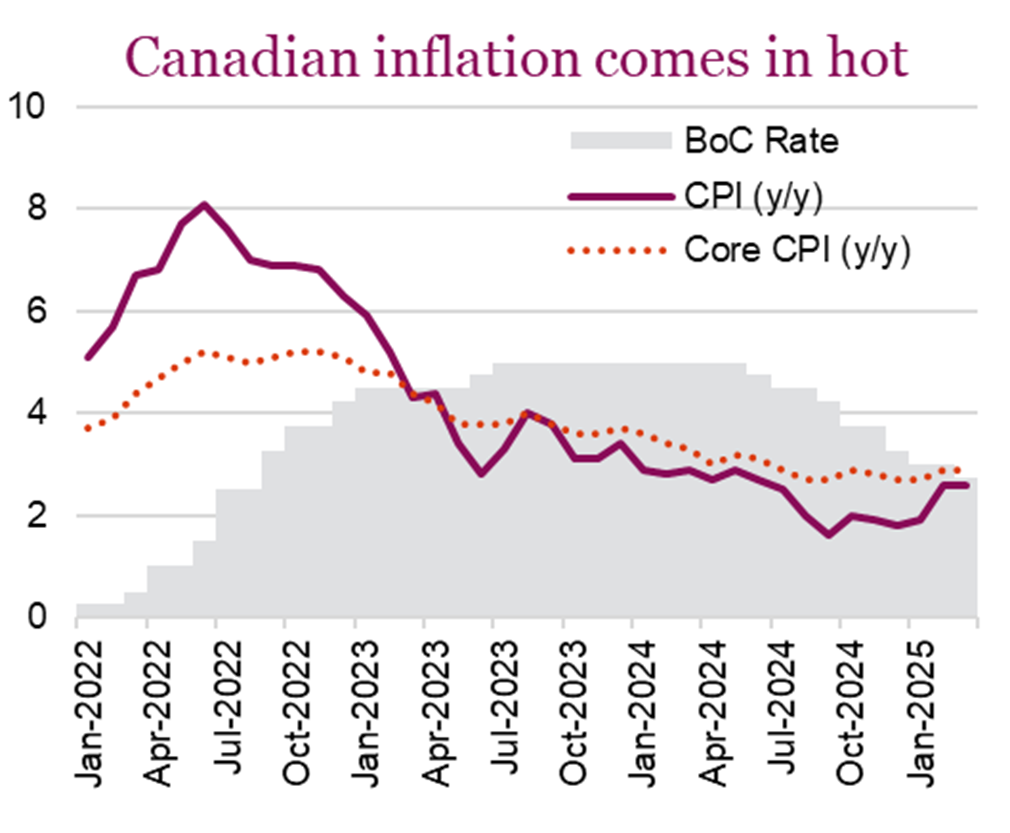

Both the Fed and BoC continue to work towards bringing inflation down to target levels in the face of trade uncertainty. While central banks were making progress at the end of last year, both countries are now contending with the threat of inflation creeping back up. These concerns intensified after Canada’s inflation rate jumped to 2.6% in February, the highest in eight months, as a federal sales tax holiday expired, pushing up food and grocery prices. Without the tax break, inflation would have hit 3%, right at the upper limit of the BoC’s target range. The Fed’s preferred inflation gauge, the core PCE index, rose 0.4% in February and 2.8% year-over-year, slightly above forecasts. Meanwhile, inflation-adjusted consumer spending edged up just 0.1%, reflecting cautious household demand. While the central bank held rates steady this month at 4.25%-4.5%, markets are pricing in potential rate cuts starting in July after the Fed signaled that they could cut rates two times this year. The Fed lowered its U.S. economic growth forecast for 2025 to 1.7% (from 2.1%) while raising its core inflation estimate to 2.8% (from 2.5%), signaling concerns about stagflation as Trump’s tariffs drive up prices and slow growth. Let’s dig a little deeper into the soft and hard data that has been presented and see what it’s trying to tell us.

Hard or soft

Most perceptions regarding investing are created by experiences. Anyone actively engaged in investing for the past ten years experienced a few corrections, two bear markets and higher than historical average market returns led by the U.S. The first bear market was Covid, which was very short and over for the markets long before it was over for our social calendars. This likely solidified the ‘buy the dip’ mentality. The second bear was inflation/yield driven, longer in duration yet not accompanied by a recession which made it more tenable. Meanwhile, U.S. exceptionalism encoded a strong preference for U.S. equities, especially megacaps.

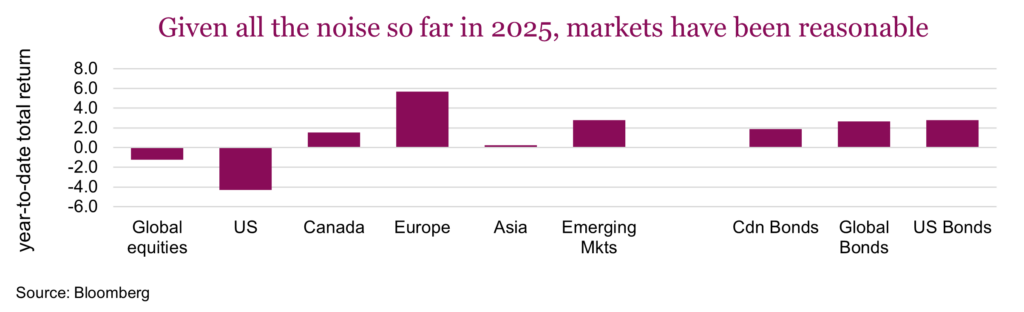

So what have investors learned in the first quarter of 2025? U.S. exceptionalism has certainly been called into question with the S&P 500 down -4.3% this year while international equities (MSCI EAFE) have crushed it, rising +7%. But perhaps the biggest lesson has been to not overreact to the headlines. Listening to the headlines, especially around tariffs, could have easily caused investors to believe in doomsday scenarios for Canada and other trade-sensitive economies. Meanwhile the TSX is up on the year and Germany, another export sensitive country, up +10.7%.

2025 remains a challenging year and not just because the previous two years’ markets enjoyed outsized returns. Policy risk is real and it has injected a higher level of uncertainty into the market, economy, consumers and corporations. Our strategy for this challenging year remains steadfast, listen to what people are saying but don’t overreact. There will likely be opportunities for those that can remain more even-keeled and muster the fortitude to take advantage if the market overreacts.

We believe an overreaction may occur in the coming months from economic data softness. This level of uncertainty is causing behaviours to change for consumers and companies. This may start manifesting in the data going forward. It is already evident in much of the soft data that is more sentiment driven. If this transitions to the hard economic and earnings data, that may create the best buying opportunity of 2025. In the meantime, decent economic and earnings appear to be mitigating the impact of higher uncertainty.

Will the soft data transmit to the hard data?

Gauging the direction of the economy is anything but simple, but it is critically important to politicians, central bankers, large corporations, small business owners and individual households. To accurately and timely assess the economy, stakeholders use a combination of hard and soft data.

What’s the difference?

Hard data is like a fitness tracker – it records just the facts, like how many steps you’ve taken, distance, speed, heart rate etc. These are measurable, objective numbers like GDP, unemployment, CPI, retail sales etc. Soft data on the other hand is more like a mood ring – it reflects feelings, expectations and sentiment such as consumer confidence, investor sentiment and business outlook surveys. Soft data aggregates consumer and business sentiment, providing a near-real time snapshot of confidence in the current and future strength of the economy. Both are useful. Hard data is accurate and reliable however, it lags, sometimes quite materially. Soft data is more immediate and has proven historically useful, but inherently flawed.

Why soft data gets so much attention

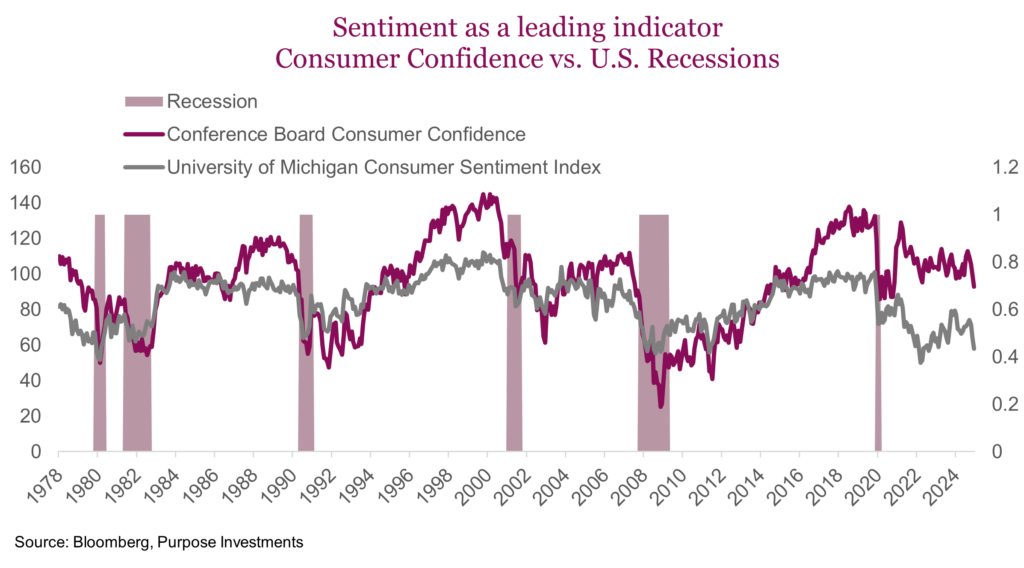

One of the more prominent soft data releases is consumer confidence. Popular measures come from the University of Michigan, Conference board, Bloomberg Nanos. Each are survey based, where consumers are asked to assess their personal financial situation. After the surveys are completed, the results are compiled and aggregated into an “index” of consumer confidence.

As you can see in the chart below, consumer confidence is correlated with the strength of the economy at the time of the survey. Particularly when the economy goes into a recession, consumer confidence generally falls sharply, and when the economy is in an expansion, it is generally at a high level. The soft data does appear to show that these types of surveys provide good forecasts of future economic activity. Empirical studies have also shown that these confidence numbers do provide some useful information for predicting the direction of the economy, but consumer confidence is far from a super forecaster.

Declining predictive power

In a perfect world, we would just have hard data in near real-time manner. Real-time retail sales, durable goods spending, hiring and inflation numbers would be amazing. Unfortunately, that’s just a distant dream. Household and business confidence numbers do offer clues to future spending patterns, but the relationship is far from perfect. One of the issues is that sentiment itself may be more skewed now. Sentiment is very much driven by what we see on TV every night, or maybe more likely what we see on our phones while “doomscrolling” in bed. The very definition of doomscrolling refers to the habit of repeatedly consuming negative news and social media content, often leading to feelings of anxiety, dread and helplessness. Social media might be to blame, but it’s an easy scapegoat. The general population’s behaviour and attitudes can become more erratic due to external factors like economic uncertainty, political instability and media influence. This can make it harder for surveys to capture consistent sentiment.

Soft data not painting a very rosy picture

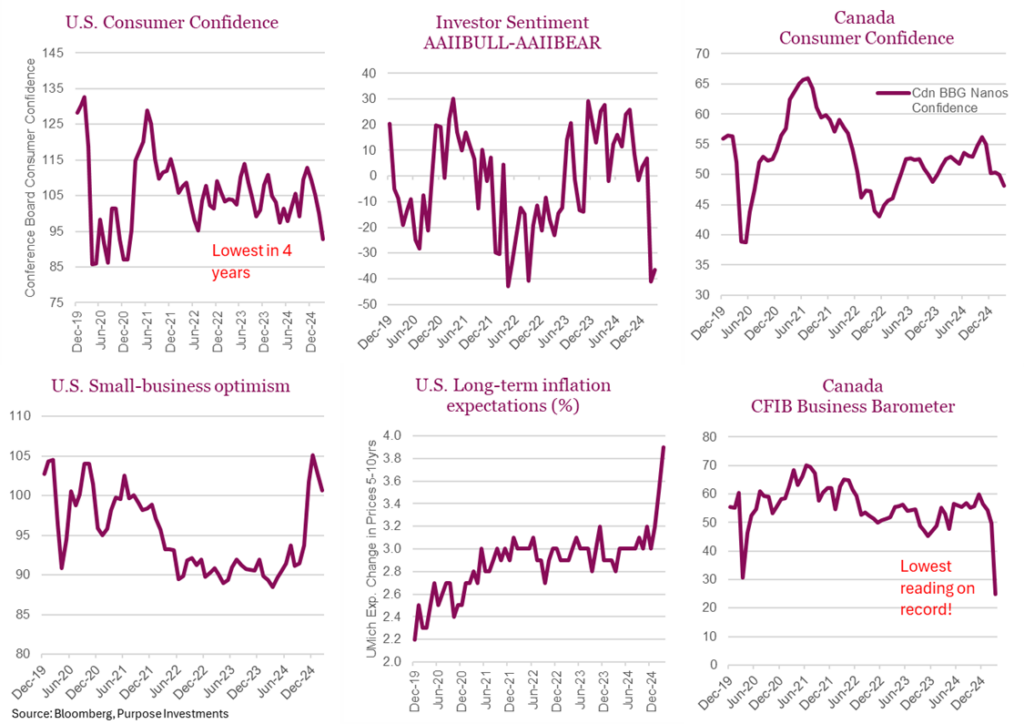

U.S. consumer confidence hit the lowest level in four years as higher prices and Trump’s trade policy uncertainty has dampened business and consumer sentiment. Inflation expectations are high and rising, consumers are miserable and even small business owners which were jubilant after the election are beginning to turn more negative. Overall, the dour mood points to growing anxiety in the U.S. It appears trade wars are great at stirring price pressures and brewing insecurity.

Canada has not done much better, with Canadian consumers feeling very downbeat these days. Consumer confidence is falling as seen in the BBG Nanos confidence index and the Conference Board’s consumer confidence index plunged to a record low in March. Consumers are likely to stay cautious for some time. Businesses are so worried that the CFIB Business Barometer Index recently registered an all-time low reading! To put this into context, this is below the depths of the financial crisis and even peak-COVID mania. Canadian businesses have never been more scared.

While recession fears are rising, we’re a far way off of two consecutive quarters of negative GDP growth. What the soft data is pointing to is more or less a “vibecession”. This refers to a period where consumer and business confidence is deeply pessimistic. Whether or not this precipitates an actual recession is too soon to tell. We saw a similar situation back in 2022. Rising inflation caused a dark cloud of negative sentiment that never materialized into a technical recession. Soft data is not a reflection of the actual economy. The economy is complex apparatus, a system of interconnected entities and interactions. It’s these micro-level interactions that all add up to the grand macro-level outcomes of the economy. Within this complexity, individual decision making is based on expectations and gut feel. For this reason, economists and investors who discount the soft data are taking a big risk.

Hard data has slowed but holding up

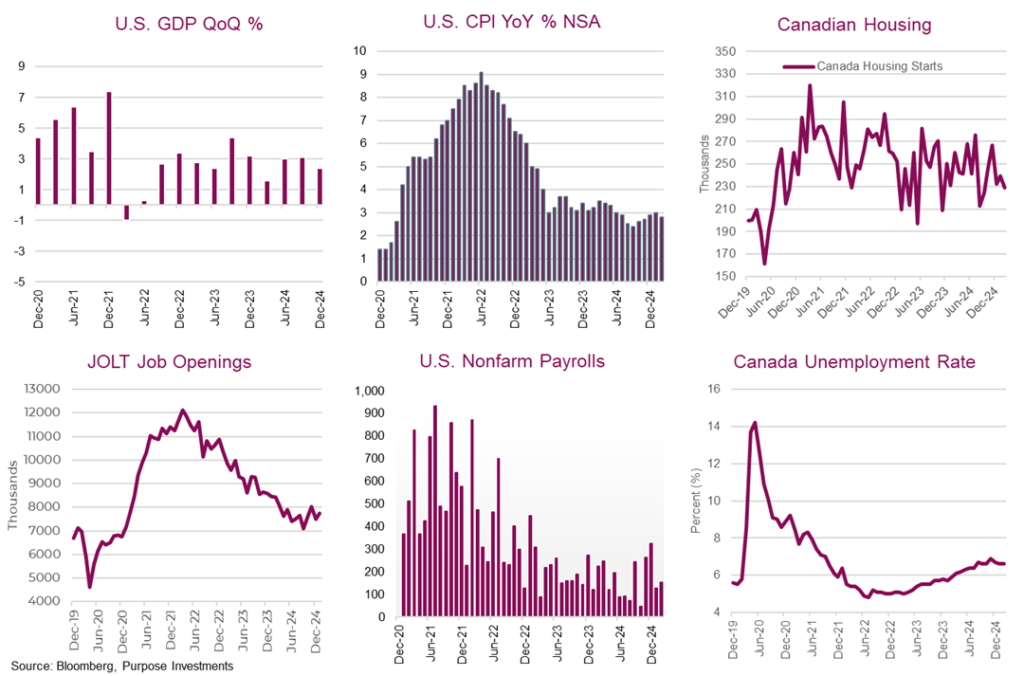

Then there’s the hard data, which in aggregate shows that the economy is cooling but hardly dropping off a cliff. Job gains in the U.S. remain steady, unemployment has ticked up in both Canada and the U.S, and job openings have fallen, but are off the lows. Factory output shows no real concern, it even came in higher than expected in February. Inflation data in both Canada and the U.S. is rising, which is concerning, but the pace and level are not at alarming levels. It even eased in February, notching the slowest pace of price growth in four months. The Canadian housing market has steadied, aided by falling rates however there is no real pickup in activity. Our unemployment rate is higher, at 6.6% but has come off slightly from the recent high set in November.

Current market signals – it’s complicated

Depending on whether you’re glancing at the mood ring or the fitness tracker, they are both giving off mixed signals. The soft data is showing real concern over the economy. Unfortunately, the hard data lags but isn’t setting off alarm bells. We’ll have to wait and see over the next few months to see if the economy is slowing faster than expected. As of yet, we don’t see much evidence. It’s this waiting, and uncertainty that becomes very tiresome for investors. My mother always said “patience is a virtue” however this virtue appears lost to both Wall Street and Main Street. Uncertainty breeds anxiety, which is exactly what we’re seeing in the markets.

When markets are anxious, discount rates go up, risk premiums go up, and valuations come down. Hence the market correction. The first leg was more or less an off-gassing of an overheated market. Looking back, it’s easy to see we were due. Markets will likely have a brief reprieve, followed by the second leg – a growth scare if the soft-data is correct.

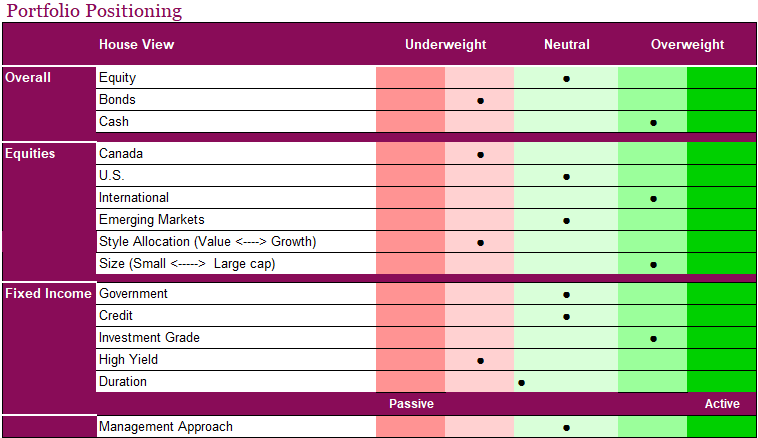

Market cycle & portfolio positioning

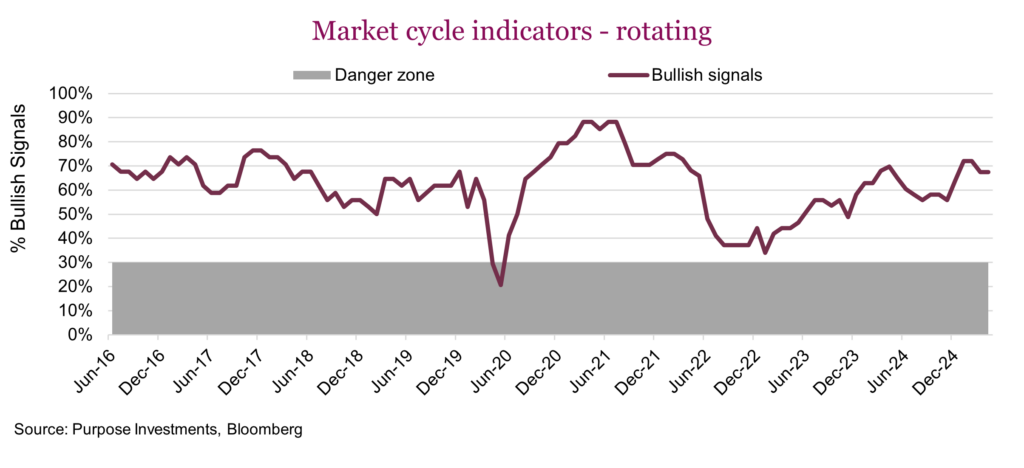

The market cycle indicators have ticked slightly lower but remain relatively healthy. This doesn’t capture the bigger story which is a rotation beneath the aggregate headline number. Over the past month, there has been a steady erosion of indicators for the U.S. economy. General indicators including Leading Indicators (3m change) and GDP Now (a faster data indicator for GDP) both flipped bearish. PMI new orders and Energy Demand turned bearish for the U.S. manufacturing grouping. Additionally, the trend is 6 signals improving with 13 eroding, compared to 12 improving and only 8 eroding last month.

Some data has been a bit squirrelly of late due to the risk of tariffs. It has caused many companies to increase inventories beforehand, likely pulling forward some economic activity. This may result in a dip in the data over the coming months, whether tariffs are implemented or not. Another factor to consider is DOGE. While the number of layoffs is hard to quantify, this will likely start showing up in the labour reports in coming months as well. We could very well see a further drop in economic data. On the positive, international keeps gaining momentum from a market cycle perspective. Emerging Markets (EM) and Baltic Freight both turned bullish compared to last month. This helped partially offset the bearish switches for the U.S.

Over the past month we have not made any material allocation changes. The defensive tilt with extra cash and diversifiers certainly helped during the recent period of market weakness. Having an overweight international and a bit of an equal weight tilt within U.S. equities also helped. The market weakness was really focused on those megacap technology names, highlighting just how concentrated the U.S. market has become.

The narrow market sell-off focused mainly on the mega cap technology names was starting to look interesting, but now with a partial bounce back we are less enamored. The partial market recovery could be the “Trump put” in action. Over the past couple weeks, it feels like there has been a decline in attention-grabbing antagonistic policy statements. From oversold levels, we believe the market can bounce on even a slight drop in uncertainty.

This could change at any moment and is likely to change as tariffs become clearer (if they do, who knows). Markets usually prefer to know, even if it’s bad news, compared to continued uncertainty. So this bounce may have some legs. Unfortunately, after months of uncertainty, it is starting to have an impact on economic data and corporations. Some early reporting companies have not filled us with much confidence for Q1 earnings season. Add to this the impact of DOGE which should start showing up in labour data in April.

This may cause a period of market weakness in the coming months with talk of recession risk. This could be the better buying opportunity for 2025.

Final note

Markets continue to wrestle with tariff concerns and some cooling expectations around AI. We do believe if markets decline, it is likely that the policy talk out of the U.S. could soften. This is the “Trump put” we have written about — of course we don’t know what level of weakness is required to cause policy talk to pivot. Perhaps the silver lining is that this period of uncertainty is almost 100% self-induced by U.S. policy, which can be easily adjusted. Time will tell as this volatility will likely continue.

Of greater interest will be if all this uncertainty starts to meaningfully show up in the hard data — either the hard economic data, or earnings. Q1 earnings season kicks off in mid-April and we would bet many companies will be cooling their guidance given the uncertainty. Corporate uncertainty will also start to show up in the data. And in the coming months, all those DOGE-related layoffs may also start having an impact. ‘Recession’ talk may be on the horizon.

If this does occur, it may create one of the better buying opportunities in 2025. Hopefully we don’t get there but if we do, it is best to have some dry powder to potentially take advantage.