Market Ethos

April 21, 2025

On again, off again

Sign up here to receive the Market Ethos by email.

It’s pretty easy to characterize U.S. policy announcements over the past month as a bit of a Jekyll-and-Hyde scenario. Some days, the good Dr. Jekyll shows up, but on any given day, Mr. Hyde may show up. Markets don’t like Mr. Hyde. This policy uncertainty or flip-flopping has led to some very large daily swings.

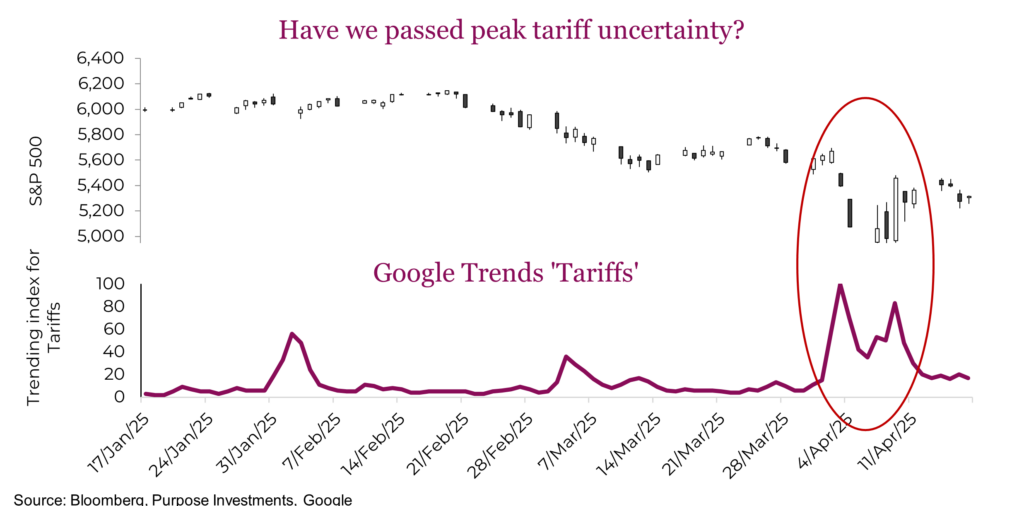

Good news #1: The potentially good news is that we believe we are past peak tariff uncertainty from a market reaction perspective. The billboard of tariff rates, followed by reciprocal tariffs from many countries, followed by more from the U.S., feels like the peak. Or at least it’s really hard to conjure up a more market-unfriendly scenario of events. And now negotiations are ongoing, so a level of optimism has crept back into the market. Mr. Hyde may show up again (and likely will), but the market may not react with the same magnitude.

Good news #2: Policy, whether central bank, tax, regulation or trade, is really challenging. Mainly because the feedback loop on whether you made a good or bad decision often takes years. Sometimes, the person who made the decision isn’t even in the decision-making seat when it becomes known whether they made a good or bad policy adjustment. Now we disagree with the approach the U.S. is taking towards trying to reconfigure trade and do believe in more free trade. But there are solid reasons to change their policy, and we won’t know for years if it really worked.

That wasn’t the good news. The good news is that this market weakness is 100% policy-inflicted. It isn’t some strange airborne virus, it isn’t surging inflation, it isn’t the financial plumbing breaking, and it isn’t a recession. It’s policy with Jekyll-and-Hyde uncertainty. This is good news because there is always an option to pivot policy, to reverse or mitigate market damage, as we saw with the 90-day pause pivot.

Contagion?

As we have highlighted, the soft data is very poor. Soft data is typically sentiment derived from surveys, and not surprisingly with so much uncertainty, sentiment has soured. Investor sentiment, consumer confidence, and manufacturing surveys are all in the dumps. Typically, this soft data is viewed as a leading indicator for the more delayed or lagging hard economic and earnings data (read more about this in Investor Strategy: Facts vs feelings).

But sentiment or soft data can often exaggerate. For example, investor sentiment is more negative this month than during COVID. That doesn’t match with price action or money flows. People often say one thing and behave very differently. Sentiment can provide insights into future direction, but not magnitude.

After all, this tariff uncertainty pales in comparison to a global pandemic. The BIG question is whether or not this negative sentiment data will spread to the hard data. So far, the hard data has held up well despite the uncertainty. Retail sales, economic forecasts, earnings forecasts, and labour gains have shown only minor losses of momentum or have not softened at all.

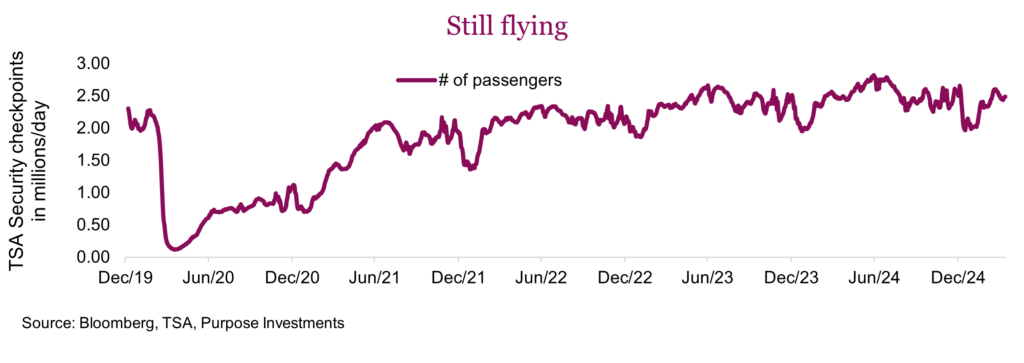

Even looking at more timely economic activity data, things look alright. Let’s call these fast-hard data, given their increased timeliness. Initial jobless claims, for instance, are a weekly reading on the number of new people applying for unemployment insurance. So far, no sign of an uptick. Or take TSA security checkpoint volumes. If the economy is slowing, usually the number of people flying begins to slow down. So far, people are still flying.

The list goes on, including OpenTable – people are still eating out. Or credit card point of sale activity – people are still spending. Gasoline demand is stable – people are still driving.

What happens next?

We’re going to talk mainly about the S&P 500, but the idea applies elsewhere. The S&P went from 6,000 at the end of January to around 5,000 in early April, with a partial recovery to 5,300 at the time of writing. A bullish argument from here can be made. Perhaps our first chart is accurate, and peak trade uncertainty is behind us.

The market is down -12%, which means it’s less risky compared to its previous level, which some may disagree with. There are market-friendly policy movements, including deregulation and tax cuts, percolating in the background. Oil prices have come down, a positive for consumer sentiment that will also help with inflation pressures. If we can string together a few days of stable prices, the dip buyers will likely gain confidence. This could help markets recover more in the near term.

The bearish argument can also be made even if you believe we are through peak trade uncertainty, which is still unknowable. Earnings estimates have been somewhat resilient, but this may change quickly. All this uncertainty is having an impact on company decision-making and financials. But analysts won’t revise down estimates materially, as it remains a coin flip.

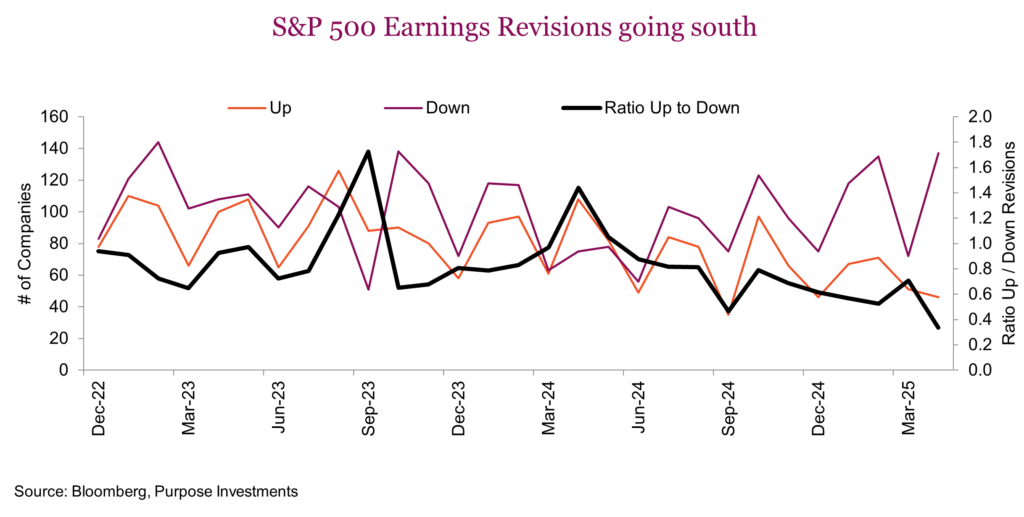

That is, until or if companies start providing more tepid guidance. The aggregate numbers have not moved much, but the trend is bad. The following chart tracks monthly changes to revisions, and at just about the halfway point in April, we are already seeing a large number of downward revisions with very few upward revisions.

And if that soft sentiment data spreads to the fast and normal hard data, that will certainly have more folks talking recession. The challenge is that if either earnings or economic data turns weak, it isn’t something that can be fixed with a tweet or a Truth Social post, as it would no longer be self-induced.

We are not in the recession camp, but we could see markets creating a deeper buying opportunity if those fears ramp up in the coming months. We’re keeping some dry powder on hand if there’s a market opportunity.