Market Ethos

November 17, 2025

Faster isn’t always better

Sign up here to receive the Market Ethos by email.

We think most would agree the world seems to be moving at an increasingly faster pace, as immediacy has become the norm. Have a question? You can usually get an answer right away from Google or ChatGPT. If you have the munchies, Uber will get it to you pretty quickly. Want to order a few books for an upcoming beach vacation? Amazon, for a bit extra, can get them to you later today. Faster is better. There may be a biproduct of this increased immediacy: patience appears to be diminishing. We are sure traffic is worse, or perhaps with less patience being stuck in traffic is less tolerable. Or the subway, are there more delays now or is it us? Both, it’s them too. Toronto subway delays are up 53% from 2019 levels according to all-knowing Gemini. Maybe a bad example. Nonetheless, immediacy is the norm, delays are not acceptable and everyone is less patient as this is the NOW world.

This greater sense of immediacy also creates challenges in the investment world. A headline or event can move markets immediately, as participants rush to incorporate the news into where they are willing to buy or sell. It is a crowd-sourced giant guessing machine, and it moves fast. The challenge is that the impact on the economy or earnings is not immediate; it often unfolds gradually with long delays.

The Fed cuts interest rates and markets react in real time. However, the impact on the economy is gradual, with some saying it takes 1-2 years. This of course doesn’t jive with our general impatience bias. Or take tariffs. The market reacted very negatively earlier this year, but as the economy continued to endure and corporate profits remained resilient over the last couple quarters, concerns subsequently dissipated. The challenge that is tariffs have a gradual and delayed impact on the economy and earnings. Initial overreaction may have morphed into underreaction today.

Tariff announcements are sudden events, but the actual impact is gradual and delayed. The cost of tariffs is borne by three parties. The exporter may reduce their prices, especially if there are other providers or substitutes. If demand is inelastic, they won’t absorb much of the impact. The importer can absorb a portion of tariffs, often driven by the willingness of their clients to pay higher prices. This impacts margins. Alternatively, a portion of tariffs can be pushed through to the end client. This sharing of the impact is not equal nor constant as it changes over time.

This is where patience comes in. Companies didn’t raise prices at the onset of tariffs. Instead, they likely pull levers or run down older inventory to keep prices stable and maintain margins. But as that and other levers are used up, the impact of tariffs may gradually become more apparent. Not all of a sudden and not equally. But it may be starting to impact corporate margins.

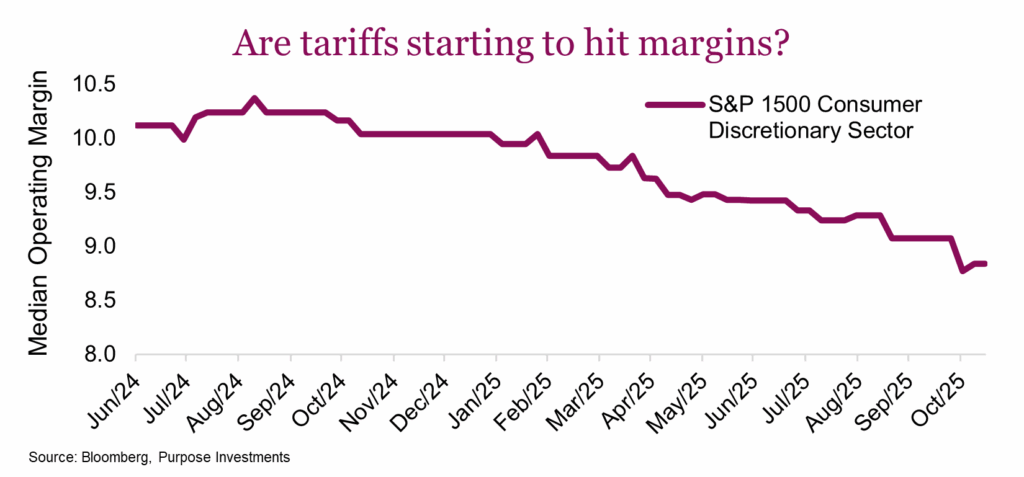

Arguably the most at-risk sector is Consumer Discretionary as this sector includes retailers, household products, apparels and auto companies. As a sector, it brings in a lot of stuff from markets outside the U.S. and sells to the hungry U.S. consumer. The above chart is the median operating margin for S&P 1500 consumer discretionary companies. It clearly shows a downward trend that is starting to accelerate.

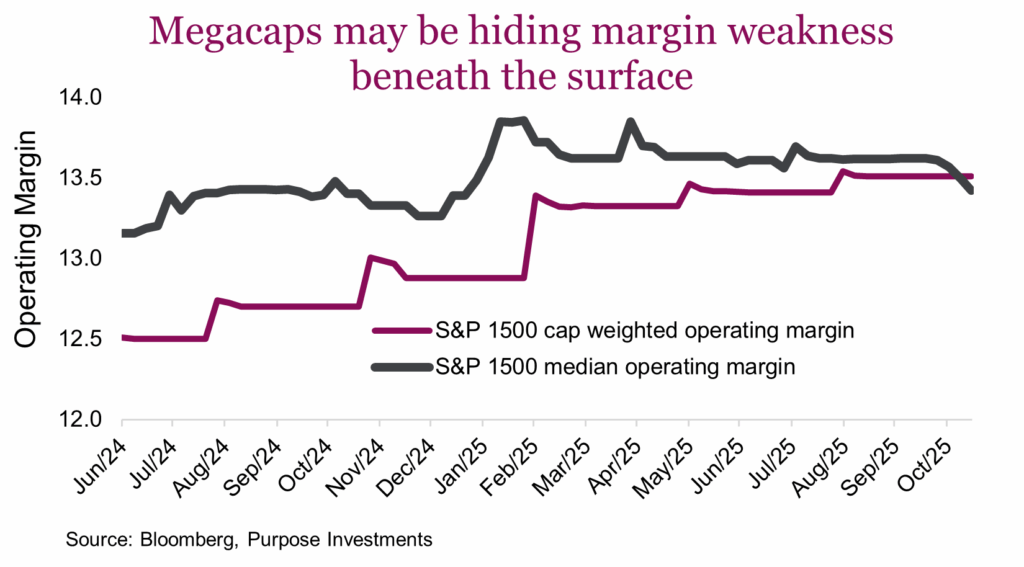

Many market participants may be missing signs of margin deterioration because it isn’t happening as much among the megacaps. Larger companies generally have more levers to pull to help protect margins as compared to smaller companies. Plus, market capitalization-based indices naturally put more weight on those megacap tech names that are benefiting from a lot of this data center-related spending. As an example, the operating margins for the S&P 1500, which is market cap weighted, is steadily rising while the median margin among index constituents has started to fall.

Tariffs will likely put pressure on margins — not as soon as they are implemented, but over time as offsetting efforts run out of steam. This process will likely be gradual and may go unnoticed initially, but will slowly become a larger issue. Also, companies may start to raise prices to protect margins, feeding inflation pressures. These risks are building beneath the surface.

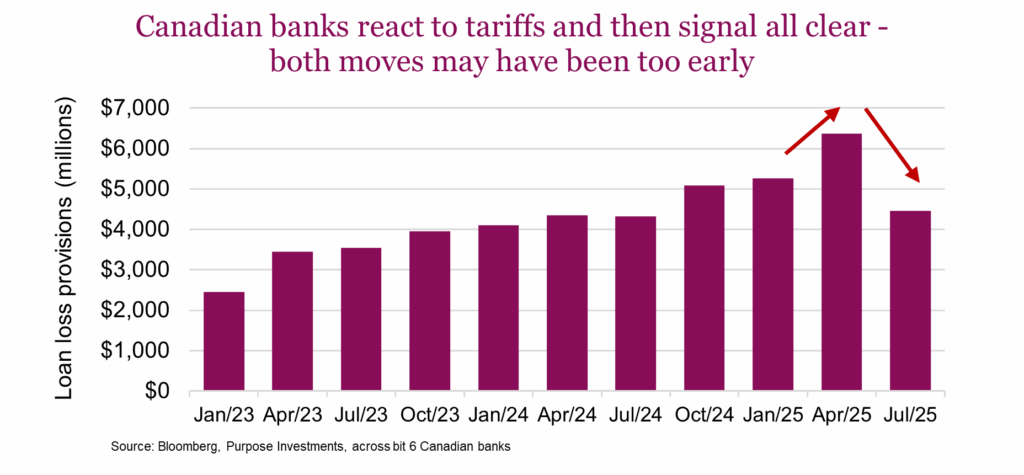

Are banks impatient?

The Canadian banks have enjoyed the strong year, up 33% year-to-date. While there are many moving parts in their earnings, loan loss provisions may be evidence of impatience. As tariffs were thrust upon Canada and became a clear risk to our economy and the banks’ clients, banks reacted quickly by raising loan loss provisions in Q2 (period ending 30 April). That seems logical but as loans continued to perform, all the banks reduced provisions in Q3, providing a boost to earnings.

Now the banks have much better line of sight into their clients. But they may have been too quick to react to tariff risks, and subsequently too quick to unwind those previous reactions. We don’t believe a company that gets hit by tariffs is going to stop paying its loans immediately. No, they will try to adjust operations, maybe reduce headcount, or attempt to find other markets. Defaulting on loans is an option but it is likely further down the list of potential actions.

Jobless claims and unemployment have been trending higher in Canada, perhaps signs of other levers being pulled. Defaulting on loans may be moving its way up the list and now banks have brought down loan loss provisions. The next few quarters will be insightful.

Final thoughts

Markets react very quickly to news and often overreact. As time ticks by, markets often begin to forget about it or underreact. But over time, the impact of events such as rates, tariffs and uncertainty slowly make their way into the economy and company earnings. Sometimes you have to be patient. Just because it hasn’t shown up yet doesn’t mean it isn’t coming. And given it’s usually a gradual process, these things can easily sneak up on us and the market in general.

Impatience bias isn’t a behaviour bias as far as we can tell, but maybe it should be.