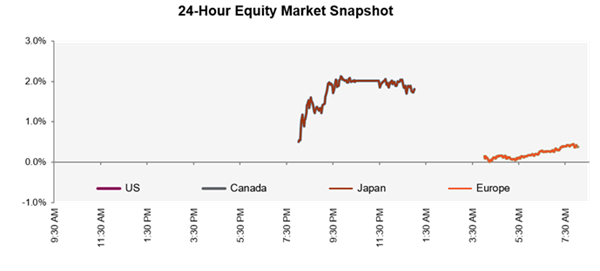

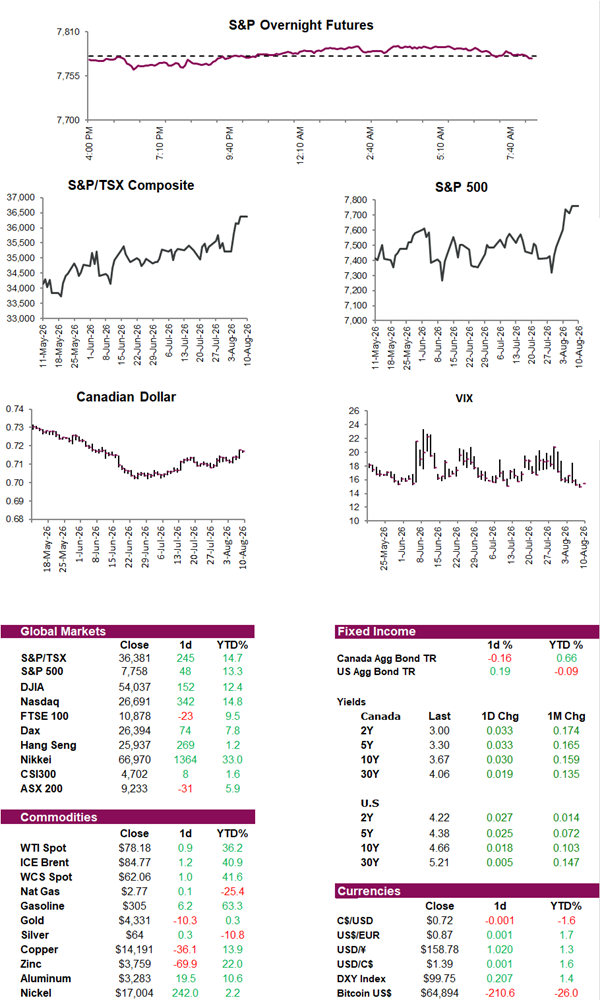

Equity futures are starting the week muted with the S&P 500 slightly lower while the TSX edges higher. Overseas, Asian markets finished mostly higher, led by Japan’s Nikkei, which rose 2.1%, while European markets are also mostly in the green. Oil prices are higher as investors await further updates on U.S.-Iran negotiations after Tehran laid out a sweeping list of demands for reopening the Strait of Hormuz. The conditions, including sanctions relief, the release of frozen assets, and a U.S. military withdrawal, are viewed as significant hurdles to reaching an agreement. This comes as earnings season enters its final stretch this week, with the S&P 500 on track for a seventh consecutive quarter of double-digit earnings growth. Looking ahead, investors are awaiting Wednesday’s U.S. CPI report, where inflation is expected to rise 3.4% year over year, which may provide investors with another clue of the Fed’s path for interest rates.

Stocks ended last week on a strong note, with both the S&P 500 and TSX reaching a record high and posting their best weekly performances since April, as weaker-than-expected employment data eased concerns about further Fed rate hikes. U.S. jobs data showed employers shed 23,000 jobs versus expectations for a big gain, while the unemployment rate fell to 4.1% largely because labour force participation declined, and the three-month average of job creation slowed to 20,000. Softer wage growth and weakening hiring pushed Treasury yields lower and reduced expectations for a Fed rate hike, which provided support for stocks despite concerns that further labour-market deterioration could weigh on consumer spending and economic growth. Tech stocks led the rally, with Nvidia, Microsoft, and Meta posting strong weekly gains.

Trying to keep yields in check. U.S. Treasury Secretary Scott Bessent appears focused on preventing a further rise in long-term Treasury yields after borrowing costs reached their highest levels in nearly two decades. His coordinated intervention with Japan to support the yen, encouraging greater use of a Federal Reserve dollar-liquidity facility, and changing Treasury guidance to leave open the possibility of reducing long-term bond issuance, have been viewed as efforts to ease pressure on the bond market. The 10-year Treasury yield has climbed to around 4.65% as inflation, large federal deficits, the Iran war’s energy shock, and concerns over Fed independence have weighed on bonds. While these measures could help contain yields, strategists warn that the Treasury Department has limited influence over the larger forces driving rates, with long term improvement ultimately dependent on weaker inflation, fiscal restraint, and confidence that the Fed can restore price stability.

Let’s make a deal. Officials in Canada are trying to secure an interim trade agreement with the U.S. before Trump’s threatened 50% tariffs on nearly $20 billion of Canadian goods take effect on Aug. 19, with recent high-level talks offering some optimism that a deal is possible. Canada is looking for relief from existing U.S. tariffs on steel, aluminum, autos, and lumber, while signalling it could address American concerns over auto counter tariffs, dairy restrictions, and provincial bans on U.S. alcohol in return. Canadian negotiators have warned that imposing the new tariffs would damage relations and likely force Mark Carney to retaliate amid domestic pressure, which could trigger another round of escalation. While officials see a potential path to an interim agreement, any deal ultimately requires Trump’s approval which may be difficult as Carney has emphasized that Canada wants broad tariff relief rather than a narrow agreement covering only a few industries.

Export engine. China’s export sector continues to outperform its domestic economy, with exports rising 24% y/y July and the trade surplus reaching $113 billion, even as weak consumption and slower economic growth continue at home. Beijing’s push to dominate manufacturing in EVs, batteries, and solar technology has contributed to what policymakers in the west are calling a second China shock, prompting tariffs and other trade barriers in the U.S. and Europe. In response, leading Chinese companies are expanding manufacturing abroad to bypass trade restrictions and protect international revenues, potentially benefiting globally established firms in EVs, batteries, consumer electronics and AI-related hardware. A stronger yuan could create another group of winners by reducing the local-currency value of foreign-denominated debt, especially for state-owned energy companies and airlines. However, strategists warn that protectionism and domestic price competition, along with geopolitical risks mean China’s export strength may not translate directly into stronger corporate profits or equity returns.

While we’re on the subject, China’s inflation pressures eased more than expected in July as lower global oil prices and weak domestic demand offset some of the earlier price increases caused by the Iran war and disruption to energy supplies. Producer prices rose 3.5% YoY, down from 4.1% in June and below expectations, while core consumer inflation was 0.9% and headline CPI slipped 0.1% from the previous month. The data reinforce the uneven picture of China’s economy, where strong exports and parts of the industrial sector contrast with sluggish household spending, a weak property market, and softer factory orders. With this in mind, officials in China have pledged to accelerate fiscal spending and infrastructure investment while continuing efforts to curb price competition among manufacturers, although economists expect these measures to take time to feed through to demand.

What if you could get all the joy of online shopping with none of the post payment regrets? Turns out there’s now a whole genre of websites built on that exact feeling. South Korea’s latest internet trend, “dopamine sites” lets users shop and order food without spending a cent, because nothing is real. Apps like FoodNeverComes simulate the entire process, from browsing the site to even tracking the package that never arrives. The creator dreamed it up after catching himself opening delivery apps late at night with no intention of eating, and young Koreans have since embraced these sites as part of boredom cure, part spending hack. But psychologists caution that skipping the checkout doesn’t answer why we use these apps in the first place, suggesting the trend is somewhere between a fix for impulse spending and a snapshot into just how deep our consumer wiring runs.

Diversion: The importance of clear and concise prompts