Today

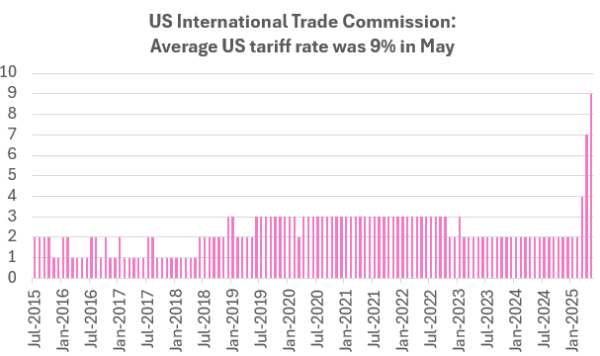

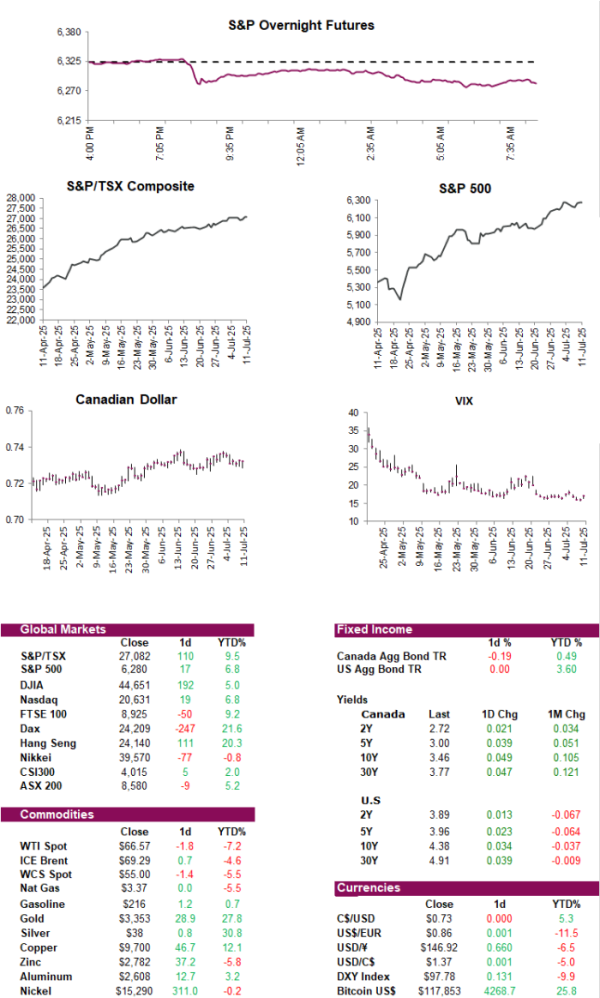

Stock futures are lower this morning following Trump’s latest tariff threats, including a hike to 35% on Canadian goods, up from 25%, announced last night (more on that below). In response, Carney took to social media, stating that throughout the negotiations, the government’s focus has been on defending Canadian workers and businesses, and remains committed to doing so ahead of the revised August 1 deadline. Separately, Trump also said he will impose a blanket 15-20% tariff on most trading partners, up from the current baseline minimum for nearly all trading partners of 10%. On a positive note, June Canadian job numbers were just released, and there were surprises to the upside. Data showed Canada added 83.1k jobs in June, far exceeding the forecasts for no growth, and the prior reading of 8.8k. While part-time work accounted for 84% of the growth, this still marks the largest jobs number in the past 6 months. Meanwhile Canada’s unemployment rate dropped 0.1% to 6.9%.

So much for “negotiations.” In a letter posted to social media and addressed to “Mr. Prime Minister” (we know him as Mark Carney), Trump announced a sweeping 35% tariff on Canadian goods, separate from existing sector-specific tariffs, set to take effect August 1. According to a U.S. official however, CUSMA (or USMCA) compliant goods will continue to be exempt. Trump offered to waive the tariffs if Canadian companies shifted manufacturing to the U.S. and warned that any retaliatory tariffs would be met with an increase equal to the Canadian hike, added on top of the original 35%. Trump cited fentanyl trafficking again as justification, despite data that contradicts the claim. He also took aim at Canada’s protected dairy industry and what he described as unfair non-tariff barriers. All in all, not exactly the tone you’d expect when both countries were supposedly working toward a new trade deal. For what it’s worth, we’ve been here before, so we should know the playbook by now. Stay tuned for more changes details.

Which is why building economic resilience at home is now a priority. Big moves are underway at the Port of Vancouver with the Vancouver Fraser Port Authority launching its search for a team to design and build a new wharf for the Roberts Bank Terminal 2 Project. This marks a major step toward delivering 70% more container capacity, which could see $100 billion in new trade capacity and contribute $3 billion to Canada’s GDP each year. The project is expected to create thousands of jobs, strengthen supply chains, and improve access to essential goods across the country. The port authority is using a progressive design build model with environmental priorities woven into the contract, including habitat enhancements and fish passage projects identified by First Nations. Victor Pang, CFO at the port authority, said the port does not have a policy that excludes bidders based on country of origin, noting that all qualified teams are welcome. He added that Canadian material providers may have a natural edge due to proximity and logistics.

Creative outsourcing. Since China banned exports of critical minerals like antimony, gallium, and germanium to the U.S. in December, American importers have continued to receive these materials via third countries (mainly Thailand and Mexico), despite both lacking significant mining or processing capabilities. Trade data and shipping records suggest Chinese-origin materials are being rerouted and relabeled to bypass restrictions, with companies like Thai Unipet Industries, a subsidiary of China’s Youngsun Chemicals, sharply increasing shipments to the U.S. This highlights the challenge China faces in enforcing its export bans, as profits and supply pressures drive creative workarounds. Meanwhile, U.S. law does not prohibit such imports, and prices for these minerals have risen amid tightening global supply and rising geopolitical tensions.

A brief dip in interest rates in the U.S. led to a notable 9.4% jump in overall mortgage applications last week, with both refinance and purchase applications rising 9%. The average 30-year fixed rate dropped slightly to 6.77%, the lowest in three months, fueling the increase in demand. Refinance activity rallied 56% compared to a year ago, and purchase applications rose 25% year over year, helped by increasing housing inventory and slower home-price growth. This matters because mortgage activity often acts as a leading indicator for the broader housing market and consumer confidence. However, despite the pick-up, actual home sales remain uncertain due to shaky consumer sentiment and high contract cancellation rates. Mortgage rates have edged up again post-July 4th, though they remain near recent lows.

Party outside the USA. According to the latest StatsCan data, Canadians are continuing to skip the drive south, taking the fewest number of trips to the U.S. in the first half of the year since 2017, excluding the pandemic years. Canadians returned from 8 million trips, well below the 11 million recorded over the same period last year. In June alone, return trips by car dropped 33 percent compared to a year ago. It marked the sixth straight monthly decline and points to a broader shift away from U.S. travel. It is not just one-sided either. U.S. car trips into Canada also declined for the fifth consecutive month, as a weaker Canadian dollar and rising trade tensions weigh on cross-border enthusiasm. Still, rising domestic tourism and international visitors are expected to pick up the slack. For now, it seems the party continues to stay local.

AI does what now?? For the first time ever, an AI-trained robot has performed a realistic surgery WITHOUT human support. At John Hopkins University, a robot recently successfully executed a gall bladder removal on a pig, after being trained on videos of human surgeons. According to researchers, the robot’s performance was comparable to that of an ‘expert surgeon’, as it had a 100% success rate in all eight surgeries it conducted. Even more impressive was the robot’s ability to adapt to unpredictable events and respond to voice commands from the human team. Humans still have the advantage of speed for now however, as the robot took an average of 5 min 17 seconds to complete a task, compared to 4 minutes for a human surgeon. The experiment only scratches the surface of autonomous surgery, where robots could be used in regular hospital procedures to improve quality healthcare access, reduce costs, and limit waiting times.

Diversion: This ones knows this old trick