Part 2: Tools to manage your investing biases

Behavioural finance is the study of how we make decisions when it comes to our money and investments. To refresh your knowledge of behavioural finance fundamentals, please read Part 1: The foundation.

Typically, all decisions involve biases or mental shortcuts, which are based on our life experiences and accumulated knowledge. Most of the time these biases enable us to get to the “best” decision quickly without expending too much mental effort; but sometimes they can lead us to making sub-optimal choices. When it comes to investing, these biases can hurt us much more than help us.

First, we’ll outline several common biases and how they can negatively impact our financial decision making. We’ll then share some strategies to help mitigate or counter these biases, with the goal of making better decisions and becoming more successful investors.

Loss aversion

In the world of behavioural finance, loss aversion is a major motivation for many investors. This is also known as prospect theory which argues that investors feel the pain of a loss to be far greater than the pleasure of an equal-sized gain. This may sound slightly abstract, but loss aversion impacts just about every investor’s decision making.

Have you ever held onto a losing investment way too long or refused to sell a loser hoping it will turn around and recover (“Get even-itis”)? Loss aversion can also lead investors to sell their winners too early, attempting to avoid the pain caused in case the share price falls back down.

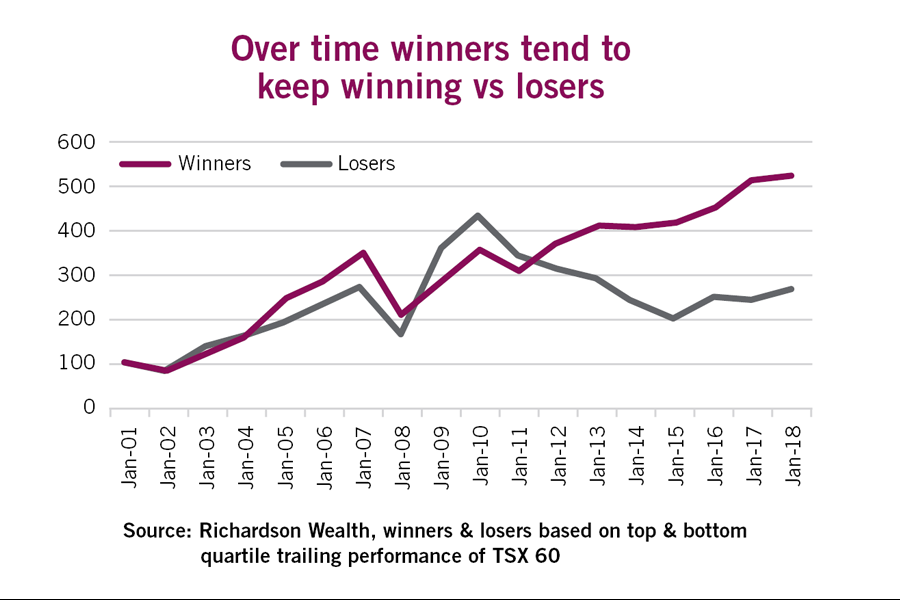

Unfortunately, this thought process can significantly hurt returns over time. The winners tend to keep winning while the losers don’t seem to recover all that much. This is evidence that should help encourage investors to cut their losses and let their winners run longer.

How to defend against loss aversion

- Ignoring the original cost can help offset this bias. After all, it is the current market value and prospects of an investment that truly matter; the stock or fund doesn’t know or remember what you paid for it

- Obtaining a second opinion on an investment also helps. While the person you ask has biases too, they won’t be emotionally vested or anchored by what you paid and they’re likely to have different biases.

- Another tool that can help is documenting the original thesis or rationale for an investment. If it still holds, even if the price has dropped, this investment is typically fine to hold. If the situation has changed, and the thesis is no longer valid, it’s usually best to cut and run.

Performance chasing

Performance chasing isn’t a behavioural bias but the result of a number of biases including overconfidence and herd behaviour.

Overconfidence

Overconfidence is the tendency to believe past performance is evidence of a superior manager. While this may be the case, more often it is the manager’s style being well rewarded in the existing market environment.

Herd behaviour

The financial industry encourages this behaviour and does little to limit its impact on investment results. You may have noticed the popularity of those charts showing how much $10K would have grown over several years invested in a fund. This is attempting to lure you in by implying the herd is doing so well, you just need to join.

The problem is that the investment styles rewarded in the market tend to change from year-to-year and chasing the best trailing performance can have a negative impact on returns as market dynamics change.

How to defend against performance chasing

Past performance is important but needs to be analyzed in the context of the wider market environment, as well as which styles or assets are being rewarded and which are not.

- Don’t confuse “right place, right time” for skill. Growth has dominated the U.S. market in the past few years; however, selling all your value and dividend-focused managers to pile into all growth is a recipe for some very poor results when the style leadership changes.

- When reviewing past fund performance, analyze it with the filter of the market environment during that time. And remember how it all fits together within the portfolio – don’t just look at one investment in isolation.

Status quo

Status quo is based on our desire to simply leave things the way they are and is related to regret aversion or conservatism. Many investors, even when faced with a solid reason to make a change, will opt to do nothing – a body at rest, stays at rest. This is caused by worrying you’re making the wrong decision and you’ll regret the choice afterwards.

A noteworthy example of this is Nortel. Many of the shareholders of this once darling tech company didn’t sell after receiving shares spun out from BCE, even though Nortel had very different risk/reward characteristics compared to its major holding Bell Canada.

How to defend against status quo bias

- Having a clear thesis or rationale for your investments, current asset allocation weights and geographic mix can help substantially. These notes don’t have to be detailed — even a few bullet points can help. This way, if a change is being proposed, it can be in the context of why you originally owned or made a decision

- If you’re holding cash to be opportunistic on a correction, write a personal contract that you’ll invest if the market drops by a certain percent.

Familiarity

Familiarity bias causes many investors to buy things they’re familiar with and leads to less diversification.

For Canadian investors, this is often evident in terms of a home country bias. This diminishes diversification as Canada’s equity market isn’t well balanced. The S&P/TSX Composite Index consists of 34% financials sector stocks, 20% energy stocks and 11% materials and little in the way of health care or technology. A good tip to identify familiarity bias is to compare a local company with a foreign peer. For example, ask yourself which you would feel more comfortable owning: CIBC or BB&T, a U.S. bank of equal size. Chances are it would be CIBC since you see their branches everywhere.

Interestingly, the direct non-Canadian equity holdings that are most often seen in portfolios are the mega-cap U.S. names. While this can help address the home country bias, it also introduces another aspect of familiarity bias in more famous large-cap names. Again, this can limit diversification.

How to defend against familiarity bias

One easy solution to gain exposure internationally, including outside the U.S., is to use either funds or ETFs. The benefit is that you won’t be staring at companies you have never heard of before in your portfolio. Moreover, with funds, there should be some local expertise on the ground where they are investing.

Behavioural checklist

Complete before making an investment decision.

Have you actively searched out and considered contrary opinions on this investment decision?

Why do you believe the market is wrong and you’re right about the investment being underpriced?

Are you being unduly influenced by the media?

Is your original cost base influencing your decision?

Are you buying this because you are afraid of missing out on a popular trend?

Can you clearly articulate the thesis on why you’re making this investment decision, and what your exit strategy is?

Becoming a wise behavioural investor

Part 1: The foundation

Learn about common systemic decisions investors make that hinder long term returns, along with basic tools to mitigate the financial impact.