Investor Strategy

8 December 2025

Finish line in sight

Sign up here to receive the Investor Strategy by email.

- Did Santa come early?

- Canada’s banks: Value is abroad

- Japan-Land-of-the-rising-governance

- Market cycle & portfolio positioning

- Final note

Did Santa come early?

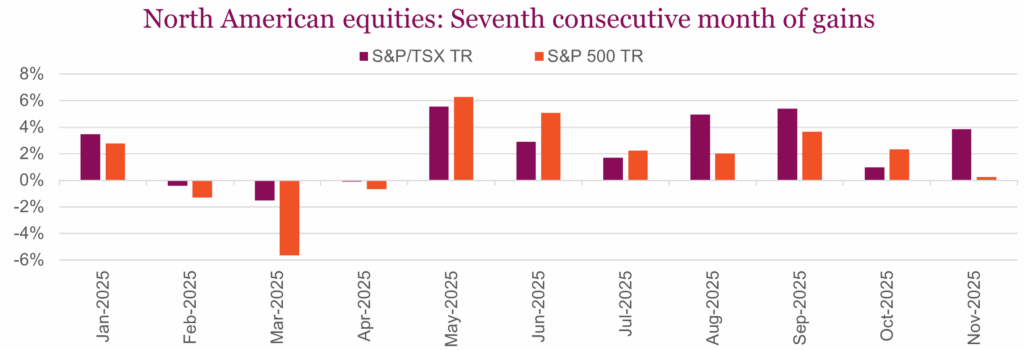

November delivered a different tone compared to the last few months, with markets grappling with renewed volatility, concerns over stretched valuations, and uncertainty around the path of monetary policy. Still, North American equities managed to claw back from mid-month losses to finish in the green for the seventh consecutive month of gains, supported by solid earnings and expectations for continued policy easing by the Fed.

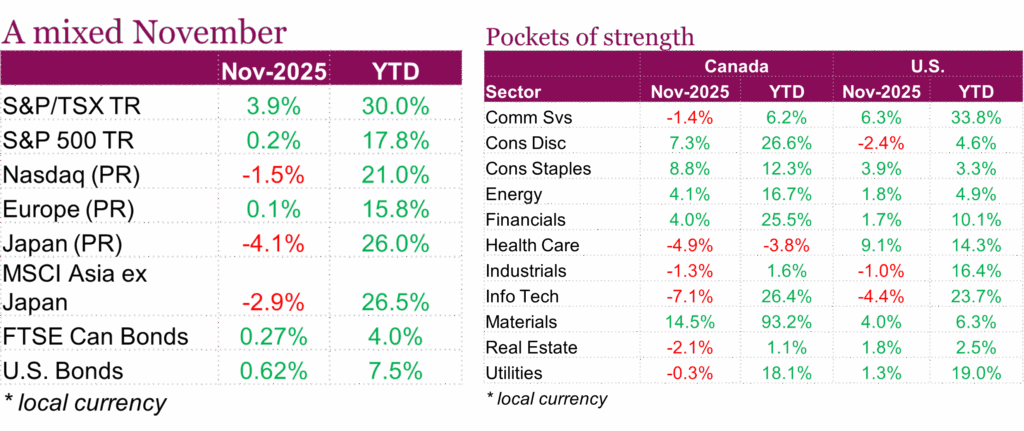

The S&P 500 eked out a 0.25% gain on a total return basis in November, its worst performance since April, after spending most of the month in the red. Investors digested mixed economic data, the lingering effects of the U.S. government shutdown, and rising questions around the sustainability of AI-driven capital spending. Profit-taking hit the tech sector particularly hard, leading to a -4.4% sector decline despite another quarter of blockbuster earnings. Overall, growth stocks underperformed value significantly, reversing the trend that had dominated most of the year. Still, the U.S. earnings picture remained impressive, with S&P 500 operating earnings and revenues surprising to the upside. Sentiment remains mixed, as the U.S. economy contends with a K-shaped economy although optimism is growing by the prospect of further Fed easing at the December meeting. Luckily the story was a bit different in Canada, with equities delivering stronger returns. The TSX Composite Total Return Index gained 3.9%, with Materials once again leading the way. Global markets outside North America were mixed, with Europe’s major indices flat to slightly lower, while Asian equities struggled, led by losses in Japan, Korea, and Taiwan.

Fixed income markets were generally strong in November, helped by falling U.S. Treasury yields and expectations for additional rate cuts. U.S. aggregate bonds gained 0.6%, while Canadian aggregate bonds rose 0.3%. This came after the Fed cut rates to 4.0% in late October, and markets began to price in an additional 25 bps cut at its December meeting. The impact of the government shutdown on economic data releases left policymakers leaning on private-sector indicators, which painted a mixed picture. Still, the consensus remains that the labour market is weakening and inflation appears controlled, giving the Fed the ability to ease further. In Canada, markets expect rates to remain unchanged for the foreseeable future as the BoC weighs stronger-than-expected Q3 GDP growth, surprise labour resilience, and controlled inflation against weakening domestic demand, stagnant business investment, and softening consumer spending.

Looking ahead, December tends to be favourable for equities, but this year has been anything but normal. Elevated valuations, questions around the stability of AI-related investment, and deteriorating forward growth indicators could limit the upside. At the same time, strong earnings fundamentals, seasonal tailwinds, and a supportive policy backdrop continue to boost optimism. This has left investors entering the final month of the year balancing familiar year-end optimism against a growing list of macro, market, and geopolitcal uncertainties.

Apart from a volatile spat in March/April and a few smaller wobbles, 2025 has been a solid year with the most recurring theme: joy with a high level of nervousness. In our Outlook 2025: Three in a row?”, we questioned if either the KC Chiefs or the markets could achieve three in a row victories. We now know the Eagles prevailed last February, but it seems the markets pulled it off.

And while the headline noise remains challenging and does inject brief spats of volatility, it is the underlying fundamental trends that really delivered. The economy remained decent, not great but just good enough. Inflation remained somewhat contained, moving a bit higher in a few pockets, but generally a mildly lower trend. This was good enough to keep bond yields rangebound, currently near the lower end of that range. Meanwhile, earnings delivered. S&P posted decent earnings growth as did most other jurisdictions. This was in contrast to the previous few years where S&P earnings growth was materially higher than most other major indices.

We could argue a Santa Claus rally seems unlikely, considering it appears Santa came really early this year and already dropped presents into investment accounts. But who knows, this could just push till the end. December often does see larger market moves, more up than down, in part due to investor unwillingness to realize gains late in the year, as lighter volumes tend to exacerbate market moves.

Canada’s banks: Value is abroad

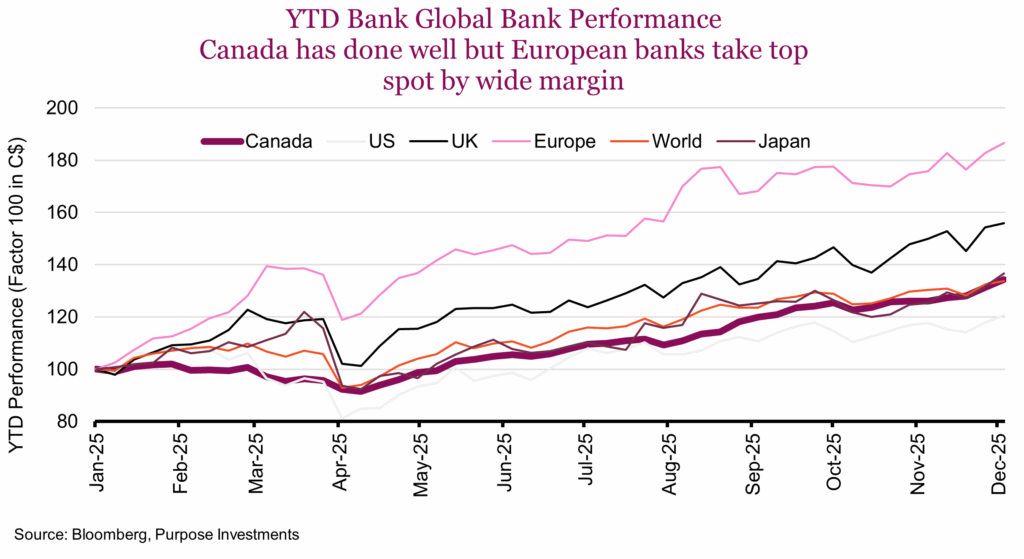

As mentioned in our market ethos last week (Laggards need to join the party), banks are doing very well. The Canadian banks are integral to the performance of the TSX. However, reliance on banks is not just a Canadian market characteristic. While we are quick to point fingers at our neighbors down south and cry afoul of the concentration issues of the big tech names, Canada and many other countries rely heavily on the health of their banks to drive equity market returns.

This past week, Canadian banks reported their year-end earnings. They were generally well received with all but Bank of Montreal positive month to date. A common theme was robust capital markets activity and wealth inflows offsetting some increase in provisions for credit losses. Net Interest Margin and a continued focus on expense management helped drive the earnings beats. Overall, the TSX Bank index is up 2.2% so far in December with nearly all of the banks except BMO trading at all-time highs. Despite a challenged Canadian housing market, and broader economic uncertainty, the banks have delivered.

While Canadian banks have posted a solid ~40% return so far this year, the true outperformance story belongs to European financials, which have led the pack on the back of a rising rate environments and restructuring efforts. European banks are up over +90% YTD, followed by their U.K. counterparts which are up over 60%. U.S. banks have still posted decent returns but at ‘just’ +23% YTD, the S&P 500 Bank index is trailing the pack. Regional bank volatility and commercial real estate concerns remain a drag for the group. What’s clear is that despite growth challenges around the globe, the market is rewarding regional cyclical recovery winners and valuations DO MATTER. The low valuation starting points for international banks presented significantly higher upside potential.

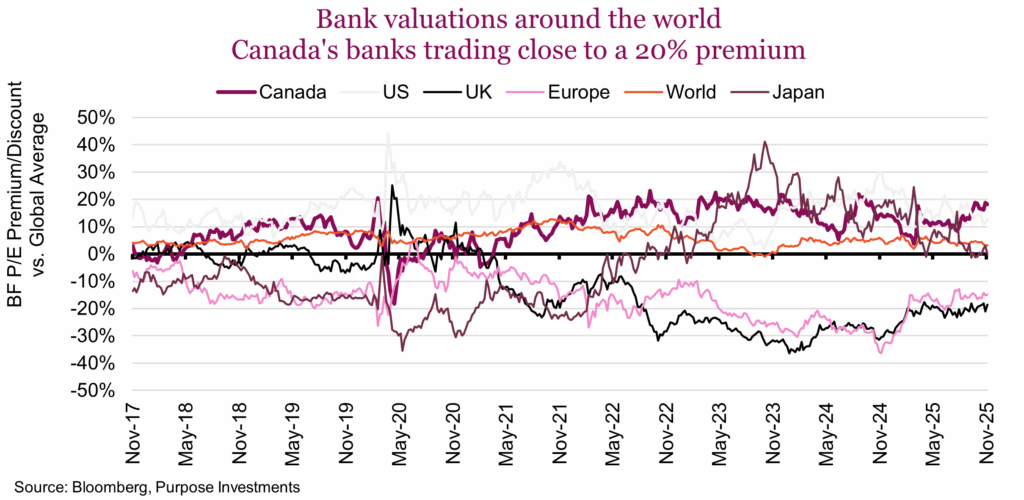

This is where it becomes somewhat concerning from a Canadian perspective. The Canadian banks currently trade a blended forward valuation (P/E) that are now over two standard deviations from their long-term historical average. They are historically expensive, which is why the recent performance is even more remarkable. A common rationalization is that they are simply keeping pace with global banks. A rising tide lifts all banks as they say. Fair, however when you dig into it, Canadian bank valuations are currently trading near a 20% premium over the global bank peer average. In the chart below, we plot the historical bank valuations compared to the global average. Canada is typically at a premium, but at current levels Canadian banks are trading richer than American peers. European and UK banks are still well below the global average, even after this year’s incredible performance. This leads us to think that there could still be further upside potential for international banks, but likely less for Canadian banks. Simply put, the risk/reward proposition for Canadian banks is less attractive on a relative valuation basis.

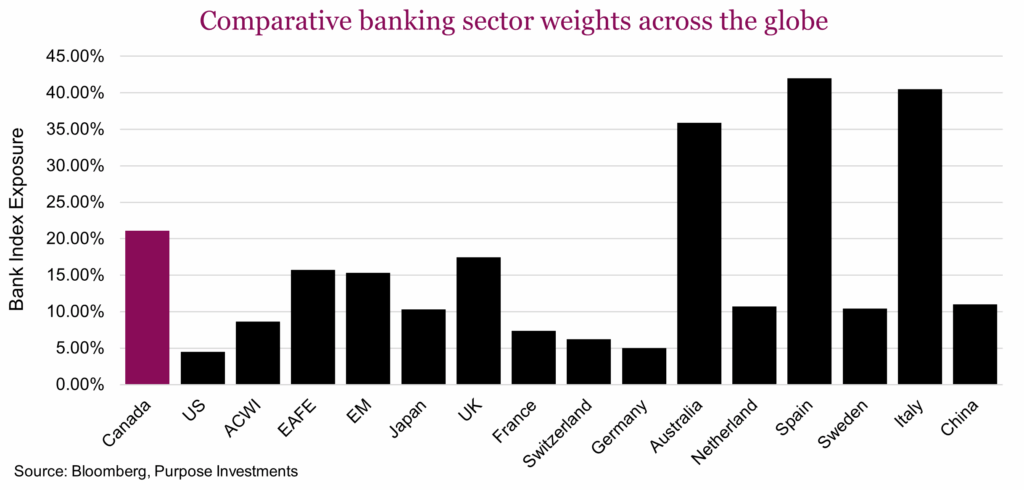

From a portfolio construction perspective, bank outlooks should play an important role in asset allocation decisions. The outsized 21% weight of banks in the S&P/TSX Composite means that equity performance is heavily correlated to the fate of the big 6. Widening our lens, the chart below shows the bank exposure across major indices as well as some of the largest individual country exposures within the MSCI EAFE index. Banks are a lower weight in the All Country World Index (ACWI) at 8.65% and especially the S&P 500 (4.55%); however they play a big part in EAFE (15.7%) and EM (15.3%) indices. From a concentration risk standpoint, Canada is nowhere near Australia, Spain and Italy whose markets all have significant bank exposure.

From our perspective it’s hard to deny the recent strength and stability of the Canadian banks. They are a key part of most Canadians portfolio. Valuations are lofty and yields are increasingly skinny. For instance, Royal Bank now yields just 2.9%, less than Canadian 10-year bonds and the lowest yields since 2007. While they typically trade at a premium to global peers, the spread is historically wider which may present a difficult setup for relative outperformance vs global peers. From our perspective, this only reinforces our conviction in maintaining an international overweight. While not the sole reason, this is a good way to gain exposure to the cheaper global bank value thesis.

Japan: Land of the rising governance

One of the most humbling aspects of investing is when you are right, but it doesn’t work out — or vice versa. Two of the reasons we became more positive on Japan in June of 2022 didn’t play out, but the position worked out very well. In other words, we were kind of wrong, but it still worked out.

The first, China reopening, didn’t actually work. Our thinking in June of 2022 was that China, which left their economy shut much longer than the rest of the world with their COVID response, would come roaring back. But at that time, we didn’t want emerging market exposure, so we went with Japan due to their trade exposure. China didn’t come roaring back as confidence was hurt, and housing remained a problem.

The second was with the yen at 140. It was crazy cheap, making anything denominated in yen very cheap. Certainly encouraging going there on vacation, as our mighty loonie goes a long way. Guess what? The yen weakened to over 160 by mid-2024 and is now sitting around 155 (quoted yen per US dollar, so higher is a weaker yen). And yet the Nikkei has annualized about 22% since then in Canadian dollar terms, so something must be working out.

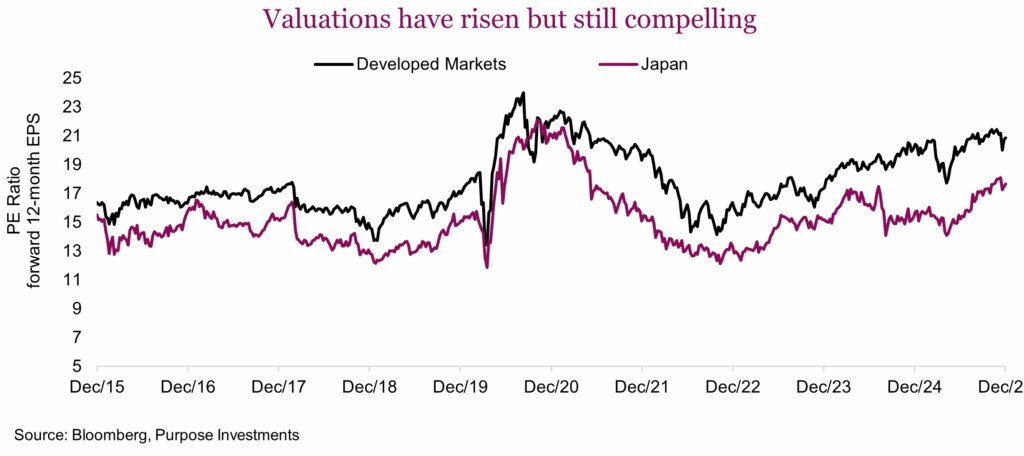

One aspect that has worked is valuations. Three years ago, Japan was trading at rather depressed levels, of around 12.7x forward consensus estimated earnings. That was cheap on an historical basis and also cheaper than valuations across developed markets globally. Fast forward to today and valuations have risen to about 17x. Not as cheap but still rather compelling compared to developed markets. The other good news is even with the strong price gains, this valuation is elevated especially if you also consider strong earnings growth which sits at just under 10% based on forward estimates for the next 12 months.

Perhaps the most compelling rationale for being more positive Japan is a gradual secular change for Japanese companies. Here’s a little trip down history lane. Japan enjoyed and then suffered from one of the greatest bubbles in history, which peaked at the end of 1989. This bubble had many drivers with real estate at its core. Near the peak it was estimated the Imperial Palace was valued at more than all of Manhattan. Unfortunately, what prolonged the pain of the bust was the desire to avoid layoffs and keep companies alive. This led to many zombie companies that muddled along operationally but eroded shareholder value. Employment and stability were put above shareholders, prolonging the cleansing phase. While not the only reason, this contributed to a 34-year-long period before the Nikkei reached its peak from December of 1989.

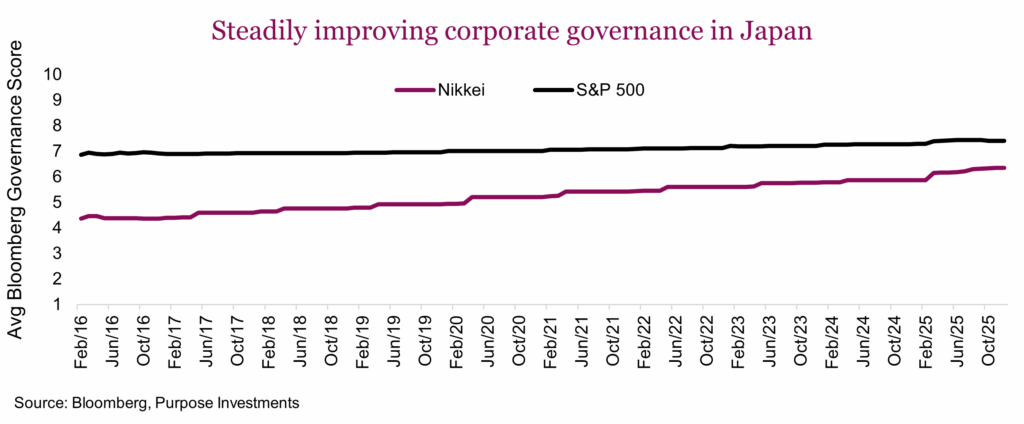

Now for the good news. A number of years ago this philosophy began to change, helped by some legislation requiring companies to not sit on as much cash and focus more on creating shareholder value. Evidence of this changing philosophy can be seen in the average ‘governance score’ for Nikkie member companies. Bloomberg Governance scores focus on board composition, executive compensation, shareholder rights and audit. From a shareholders’ perspective, a higher score out of 10 is better.

The trend has been gradual but certainly noteworthy. After many years with a very low score on governance, it has been steadily rising. Not quite as shareholder friendly as the S&P 500 but the gap is much smaller than it used to be. It is hard to draw causation between governance and share prices as there are many more factors at play. However, better governance is a positive. And this is likely a long-term secular trend that we expect to continue to provide a tailwind for Japanese equities.

Japan does fit nicely into our more positive view for international equities, but not without risks. Tariffs are obviously an ongoing risk variable especially given Japan sends a lot more goods to the U.S. each month than it imports. However, they trade much more globally. And don’t forget, that yen is still really cheap which continues to provide an advantage.

With investing, things rarely work out as expected. Nonetheless, Japan continues to perform and with a cheap yen, improving governance and earnings growth, it still stacks up really nicely.

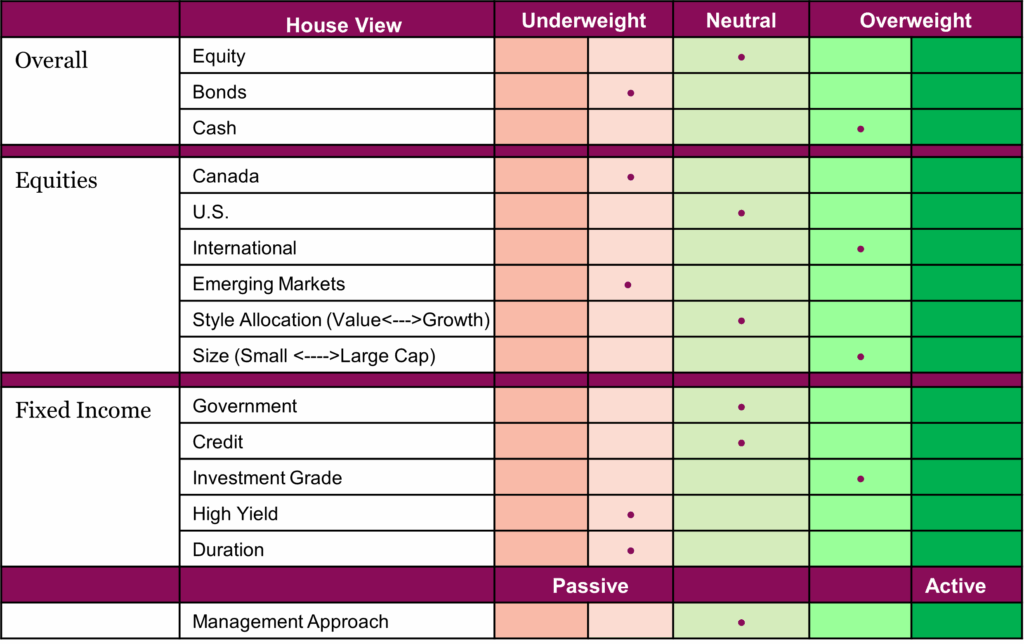

Market cycle & portfolio positioning

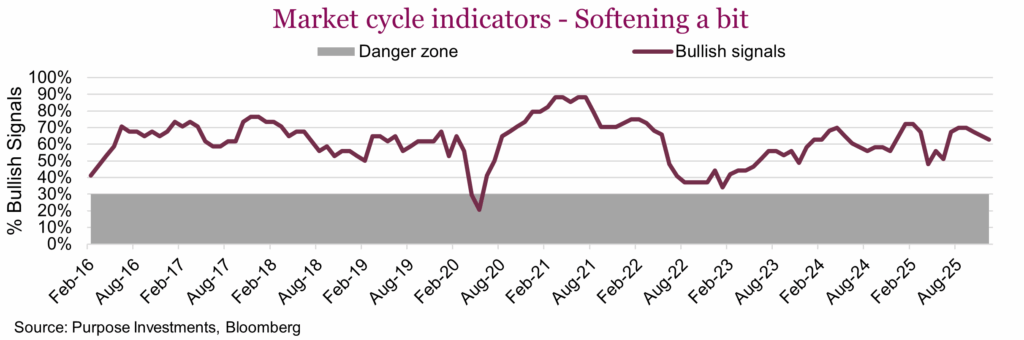

Good news, with the U.S. government shutdown over that data compilers are catching up from their little break. And so far, there has not been anything noteworthy. When it comes to economic data, generally nothing noteworthy is a good thing. Still the total market cycle indicators that are bullish ticked a little lower. Two signals flipped from last month, US Energy Demand which is bucked in U.S. manufacturing and international earnings growth slowed a little. Forward estimates are still strong and revisions positive, so not a huge deal. Of note, TSX earnings growth is now outpacing the S&P. Banks and gold, powerful combo.

Overall, still decently supportive.

No changes to positioning, that seems to be the trend this year. Markets have been great; nobody wants to trigger any more capital gains or upset the apple cart. Hopefully a quiet December to put a cap on an awesome year.

Portfolio positioning

Final note

There is no denying such a great year has pushed valuations into a higher bracket than a year ago, which already was a bit expensive. We should also remember that valuations don’t mark tops or bottoms but a higher valuation does increase market risks if there is a misstep. Fortunately, at the moment, lots of market-friendly AI capex spending, decent economic data and somewhat lower rates/yields is providing a pretty good foundation. Can’t wait to raise a glass to 2025 once we get through the home stretch for the year.