Market Ethos

July 28, 2025

Focus on fundamentals, not fads

Sign up here to receive the Market Ethos by email.

Everyone loves a great story. But a proper tale – especially one with sage advice – takes time to tell, and time is money. This is why investing stories often come packaged as age-old quips, mantras, shorthand acronyms, and even memes. These shorthands are all narrative devices that reduce complexity through simplicity. While acronyms remain popular in traditional media, memes are far more viral, taking hold and spreading like wildfire through social media. Unlike sayings or acronyms, memes don’t describe market trends, they shape them through coordinated sentiment and bandwagon trading to push heavily shorted stocks around. Acronyms and memes are both catchy, spreading as momentum builds. But blindly following either comes with risks.

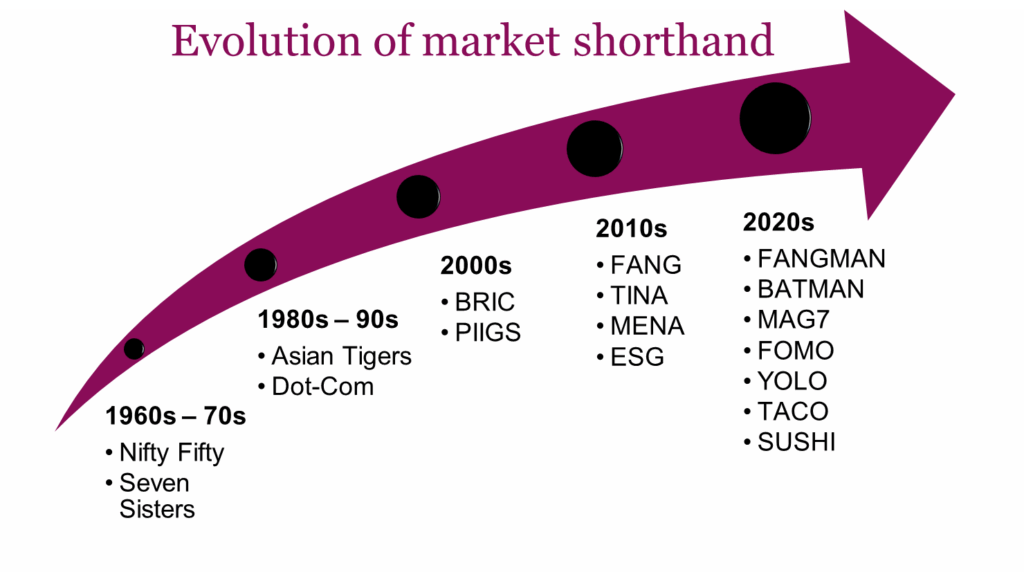

Simplifying investment narratives isn’t new. In the 1960s you had the Nifty Fifty, a quick shorthand that described the top stocks of the day that were very popular despite excessive valuations. Skip forward a few decades, and we saw the rise of the BRICs driven by globalization narratives. FANG and all the subsequent variations have been around for over a decade, reflecting big tech dominance and growing concentration risk. The chart below shows the evolution and expansion of popular market shorthand. We might be missing some, but it’s enough to see that while these shorthands have been around for a long time, they are becoming increasingly popular. Just this year, we have TACO (Trump Always Chickens Out) and SUSHI (Stocks Usually Stop Having Interest) added to the list. Sure, most of this is just fun and games on equity sales desks or financial news outlets, but the risk is that these generalizations get slavishly followed, preventing investors from looking at fundamentals. These mental shortcuts risk morphing into mental shortcomings, without diligent critical thinking.

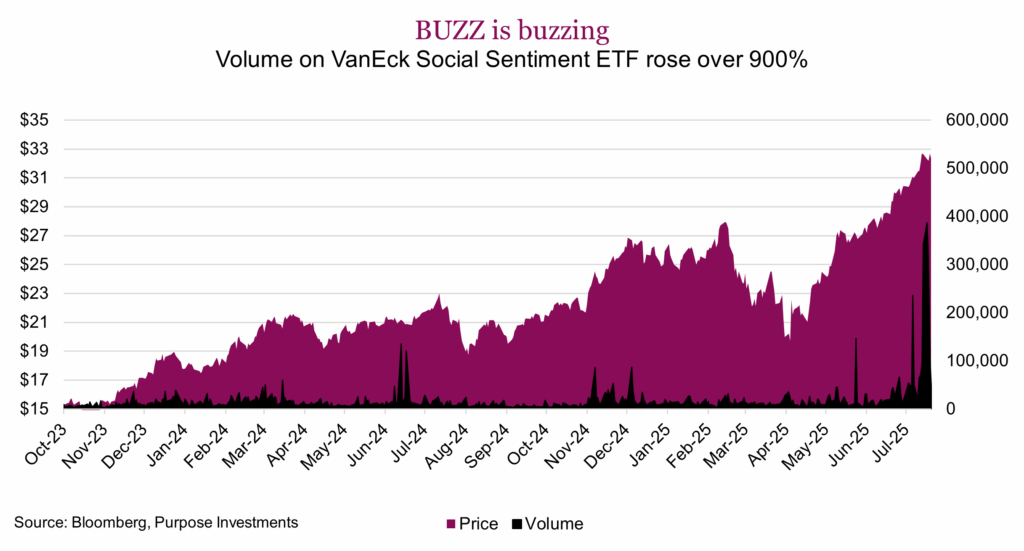

Meme-mania came back in a big way this week. The setup echoes 2021, but old-time favourites like GameStop and AMC didn’t get the invite this go around. Heavily shorted stocks saw a surge in volume, sending prices higher. Some of the popular names this week were OpenDoor, GoPro, Khol’s and Krispy Kreme. These companies saw some eye-popping returns, all up more than 100% just this week. Combining new tools like AI sentiment scraping, options leverage and mass coordination and retail traders can really push a stock around, even if these meme trades are not based on macro or company fundamentals. The chart below highlights another popular ETF from 2021, BUZZ, launched to much fanfare by the likes of Dave Portnoy during the r/wallstreetbets (Reddit) heyday. It had it’s time in the sun, at one point reaching $500 million in AUM, then dwindled for years and saw AUM fall to around $40 million in April. Just last week, volume spiked over 900% compared to typical levels showing that along with individual stocks, funds connected to the meme craze are back in the game. Meme stocks sit at the extreme end of narrative-based investing. We use the term ‘investing’ very loosely here. The returns are ephemeral, viral and sentiment fueled. Transitory does not do them justice. For meme stocks, sentiment is the strategy and nothing else.

If narrative investing were a spectrum, acronyms and memes would be at opposite ends. Both are fueled by memorable and catchy slogans, and both thrive in environments of high liquidity and easy access to information. However, acronyms are typically slower moving, encapsulating actual trends that have already been in place, and will continue to be for some time. The benefits to investors in acronym-rich communication are simple. They spread fast, are memorable, and have strong viral appeal. Most of the great acronyms or generalizations that have coincided with portions of the market have had strong returns. Often, they imply thematic exposure and spread through financial media or creative product departments. Meme stocks are simply bandwagon trading spread though social media sites like Reddit and TikTok.

Narrative investing has several pitfalls investors should be weary of:

- Oversimplification: Reducing complex themes into a simple label can cause investors to overlook potential risks

- Herd behaviour: Once certain acronyms gain popularity they can drive market moves and group think-inflating bubbles

- Obsolescence: Markets can change quickly, and acronyms can become irrelevant. TINA lost relevance once bond yields rose.

- Jargon barrier: Overuse creates insider language that can exclude those not familiar with their use. They favour tribalism, creating an ‘in crowd’

Nothing lasts forever

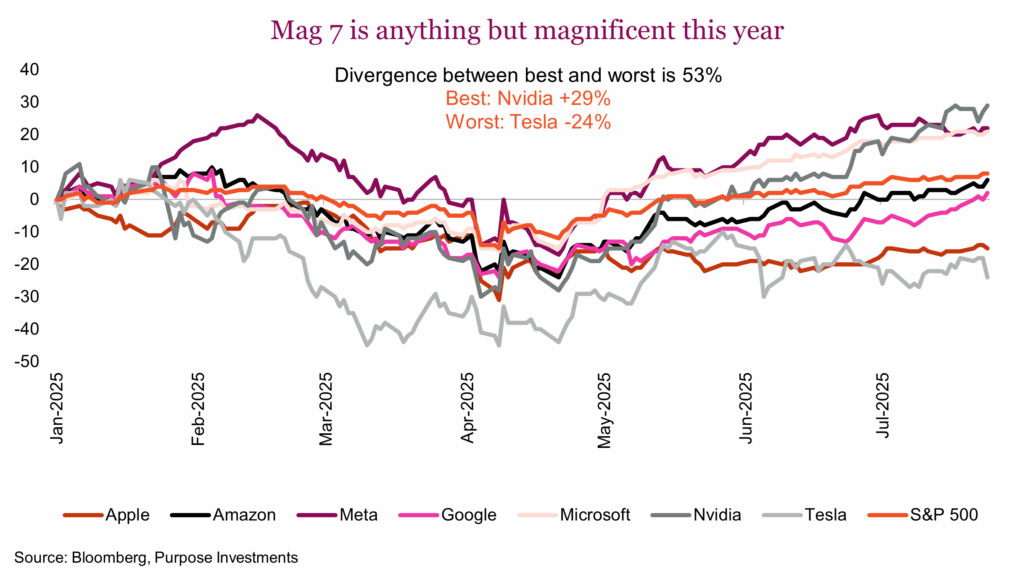

Even the Mag 7 is now dated. In aggregate, the group has lagged, up just 5.5%. There is nothing magnificent about Apple’s and Tesla’s performance this year, down -15% and -24% respectively. The divergence across the group is high; 53% separates the best (Nvidia) from the worst (Tesla). This is enough to finally put this term to bed. As a group, the market narrative of big tech dominance continues. Concentration fears remain front and centre for many investors. The combined market cap of the Mag 7 is now nearly $19 trillion, or roughly 4x the market cap of the Canadian stock market. Mag 7 now has nothing really to do with performance, but the sheer size of these companies remains magnificent.

Risk back on?

The meme stock revival comes amid a bigger risk-on move in markets that has sent the S&P 500 to fresh highs this week. Risky market behaviour is back in fifth gear, given the renewed focus of meme stocks, and fund flows pouring into US stock ETFs. In total, investors have poured a record $155 billion into US equity ETFs during the first half of the year. The similarities to 2021 are back in full view, however digging deeper into other market sentiment measures it’s not as clear that there is rampant euphoria. The AAII Bull-Bear index reading is back into positive territory at 2.58but is far from any sort of extreme bullish reading. The same can be said from Retail Investor Positioning survey data as well as S&P futures positioning. Certain market cohorts are back into full YOLO mode, but many others remain somewhat more modest regarding the near-term market path.

Final thoughts

By the time labels or acronyms get popular, its best returns are often behind them. Critical thinking remains as important as ever. Weighing the fundamentals alongside the catchiness of an acronym is the least you should do before putting in any capital work. Feel free to use narratives as a signal to spot the latest trends but make sure to balance it out with thoughtful analysis. From our perspective, narratives are fun to write and talk about, but we prefer cash flow to catchphrases and value to virality. Our process focuses on fundamentals and not the fads, and we’re just fine with that.