Market Ethos

May 13, 2024

Getting positive on Emerging Markets

Sign up here to receive the Market Ethos by email.

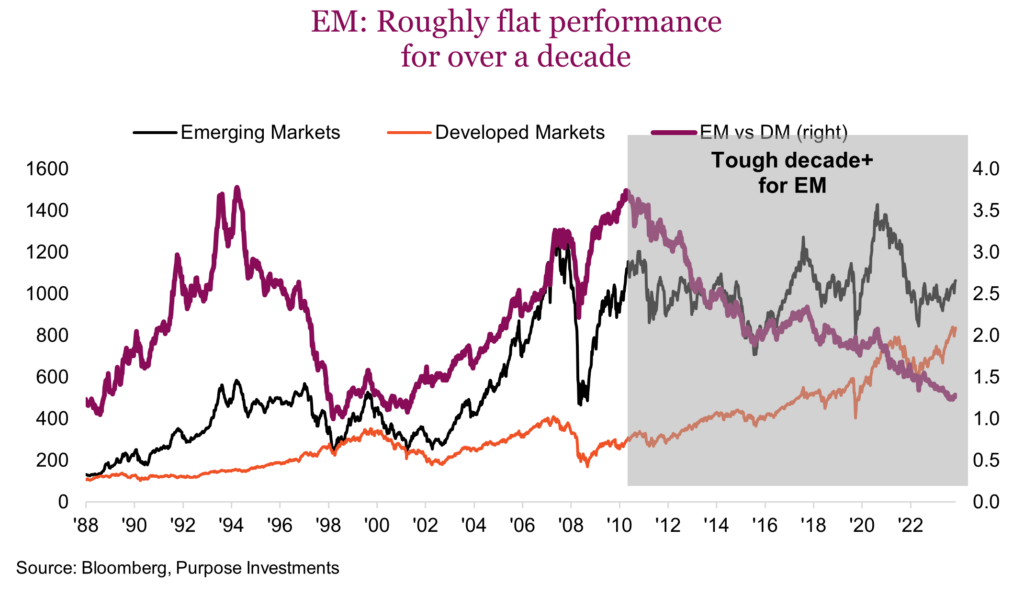

The normal narrative for encouraging investors to look at emerging markets typically goes like this: The valuations are cheap, the demographics/rising incomes are supportive of growth, and they offer diversification. Perhaps this is more of a marketing narrative. Kind of how, like for infrastructure strategies, they always talk about how many bridges need repairing. We are not refuting any of the above reasons, as they have been perennial for many, many years. And yet, for those who know us, we have been negative or at least cool on emerging markets for a long time. How long? Well, this negative view persisted for more than a decade. This is us giving ourselves a pat on the back since Emerging Markets (EM) have done roughly nothing for the past 12 years as Developed Markets (DM) have charged higher (chart).

So why are we turning more positive now after so long? First off, it is not all rosy, as there are some big headwinds as well as tailwinds. If everything were positive, EM would have already ripped higher. Investing is about probabilities, with an eye on risk to both the upside and downside. Today, we feel there is a good tilt in favour of EM. But first, we will talk about the negatives.

Trade restrictions – For EM nations, exports make up a larger portion of their economies than developed markets, so any increase in tariffs or trade restrictions is negative. Given that China comprises a bit over 20% of the EM universe, the China/US trade conflict escalation is a clear risk. When the U.S. raised China tariffs from 3% to 12% during Trump’s presidency, trade gradually adjusted. Exports out of China bound for the U.S. fell from 21% to 14%. Other countries, such as Mexico, experienced increases in their economy.

We are not going to try to guess who wins the election or to what degree campaign boasting actually affects policy. However, the escalation of trade restrictions, or Trade War 2.0, if you prefer, is a risk for China and other EM nations.

Polarization – The world has become marginally more polarized over the past years. This has led to increased geopolitical conflicts, or geopolitics have led to increased polarization, which is a bit of a chicken-and-egg question. Regardless, this trend is away from globalization, which is not great for emerging markets.

China – When talking EM, you can’t ignore China. Now, China used to have about a 40% weighting in EM, but this has fallen to around 22% as their market has suffered and other EM countries, including Mexico, Brazil and India, have risen. China is very cheap for some clear reasons, including the trade war risk, the fact their index has a strong technology weighting, and, of course, the ongoing property crisis.

As we said, if everything were positive, there wouldn’t be much of an opportunity. The real question is whether these negatives are bigger than the positives, given the current entry point available. We think the positives are great, and the low entry point offers enough of a margin of safety. Here is the other side, and we are skipping over the standard demographics and diversification arguments.

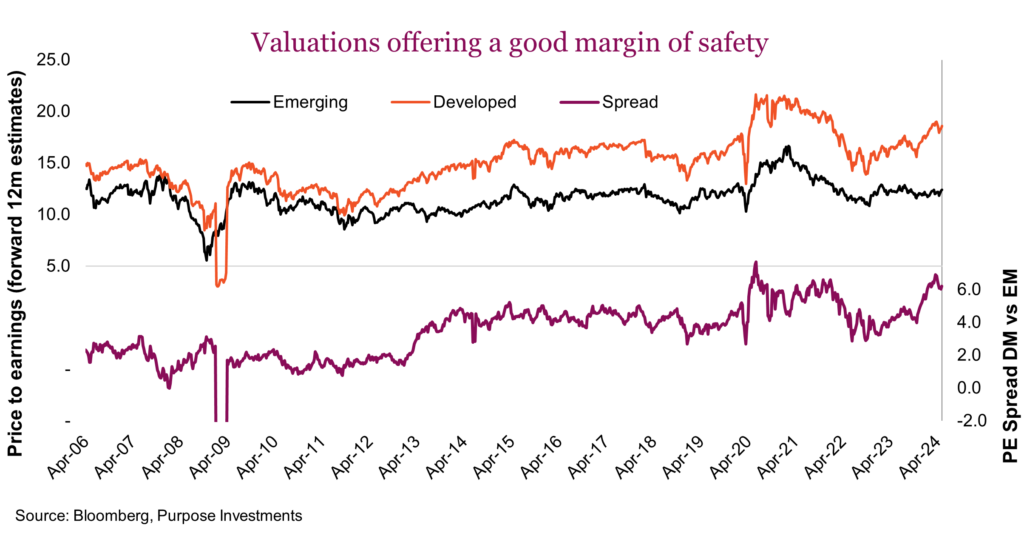

Valuations – Yes, EM is almost always cheaper than DM, mainly because of greater earnings variability. A dollar of more cyclical earnings is simply worth less. Normally, this would not be a reason, in our opinion. However, the price-to-earnings spread between EM and DM is over 6 points, which is historically very high. Developed markets globally are trading at 18x while EM is around 12x. That kind of spread does have us talking about valuations as a reason to be more positive EM, or at the very least, less fearful of the negatives.

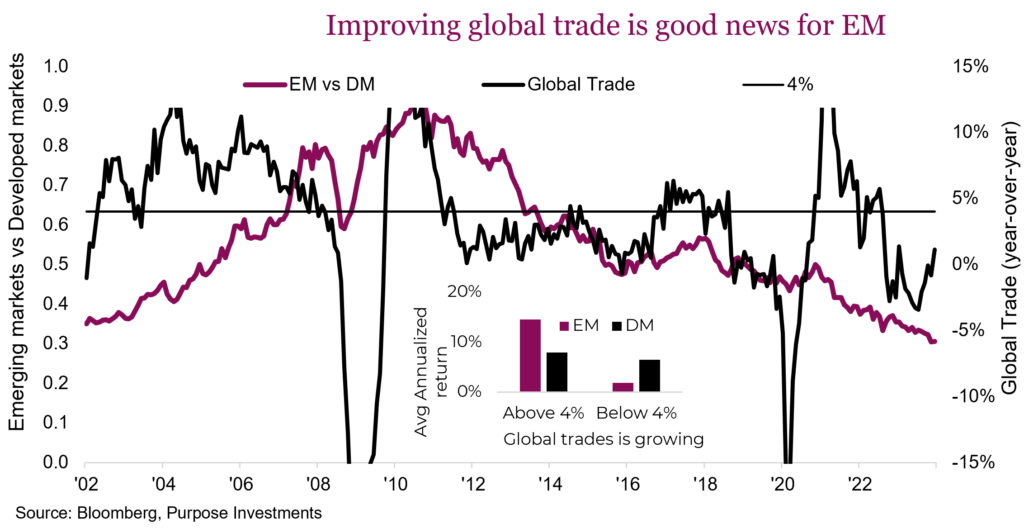

Economic momentum – Everyone knows the U.S. economy has been more resilient over the past year or two, while other economies have suffered. Today, we are seeing a broadening of economic improvement, including EM. Broader growth and less risk of global recession is good news for both DM and EM, just more so for EM. Notably, global trade is improving. While it is still being influenced by pandemic-induced behavioural changes, rising trade and higher manufacturing activity favour EM. The chart below is global trade, and it is clearly turning up (black line). It hasn’t reached the key 4% growth pace but is moving in the right direction. When global trade is higher, EM tends to outperform DM.

We would add to this central bank activity. Broadly speaking, EM nations raised rates before DM in the past rate hiking cycle. And they have started to cut rates sooner. Again, a positive impact on EM.

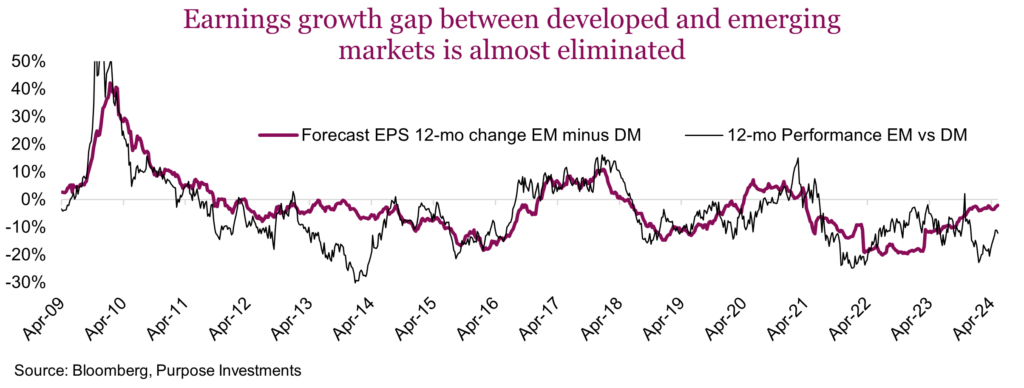

Earnings growth – The relative performance of EM vs DM tracks very well with the relative earnings growth in both. Whichever market grouping has better growth normally performs better. In fact, for much of the past decade, during which EM underperformed DM, earnings growth in EM was below that of DM. With forward earnings growth rising back close to parity, this is good news for EM vs DM that we do not believe has been reflected in the relative performance between the two.

While China used to be a much, much larger weight in EM, it is still the biggest single country weight, at just under 25%. The chart below outlines the current weights in one of the larger EM ETFs available. So, let’s talk China a little. The trade war risk is certainly real, with some of the risk mitigated by their gradual migration away from trade bound for the U.S. But the big risk is their real estate crisis. This has really been going on for about three years, and part of us wants to believe that after such a period, much of the bad news has become widely known. There is too much inventory, developers are going bankrupt, soft sales, etc. Often, the cure for a crisis is the passage of time. We’re not saying that ends a crisis, but markets will move on long before it’s all over.

So, is it over from a broader market perspective? Economic data from China is always a bit questionable. When Evergrande first surfaced as posterchild for this crisis (like Lehman Brothers for the GFC), we started tracking developers’ share prices, creating an equal-weighted index of real estate developers listed in China and Hong Kong. Our view was long before the data started to improve, this group of companies would start to recover. Call it our good news canary for China’s real estate crisis. We ignored the move higher in late 2022 as it was driven by some government intervention. And there have been many mini false dawns. Maybe the current uptick will fail again, yet we just don’t think there are many more shoes to drop that haven’t dropped in the past three years.

Final thoughts

Add all this up, and emerging markets aren’t filling us with jubilation. For the first time in many years, though, we are less fearful and believe the risk/return balance is tilted more toward return.