Market Ethos

June 17, 2024

Is inflation beat? Not so fast.

Sign up here to receive the Market Ethos by email.

It seems like just yesterday that you could buy a pint of Stella for $7 or so. Now, more often than not, it is closer to $10. Yep, inflation. It is kind of like a tax on doing things, as just about everything costs more over the past few years. Hop on a flight, eat at a nice restaurant, refinance your mortgage, the list goes on. With the benefit of hindsight, the current higher inflationary environment can be blamed on a few pretty big factors. Changes in behaviour during and coming out of the pandemic blew up supply changes, as capacity was unable to keep pace with demand. Then of course unprecedented money printing magnified the situation, as it made everyone wealthier and more willing to pay $10 for a pint.

Of course the textbook solution is to raise interest rates, which clearly occurred around the world. These monetary policy shifts are effective but have variable lags. Making those lags longer, or even temporally offsetting them, was fiscal policy. It doesn’t take an economist to understand if the monetary policy is trying to slow the economy to tame inflation, materially elevated fiscal spending in an economy that is still growing at a decent pace is counterproductive for the inflation fight.

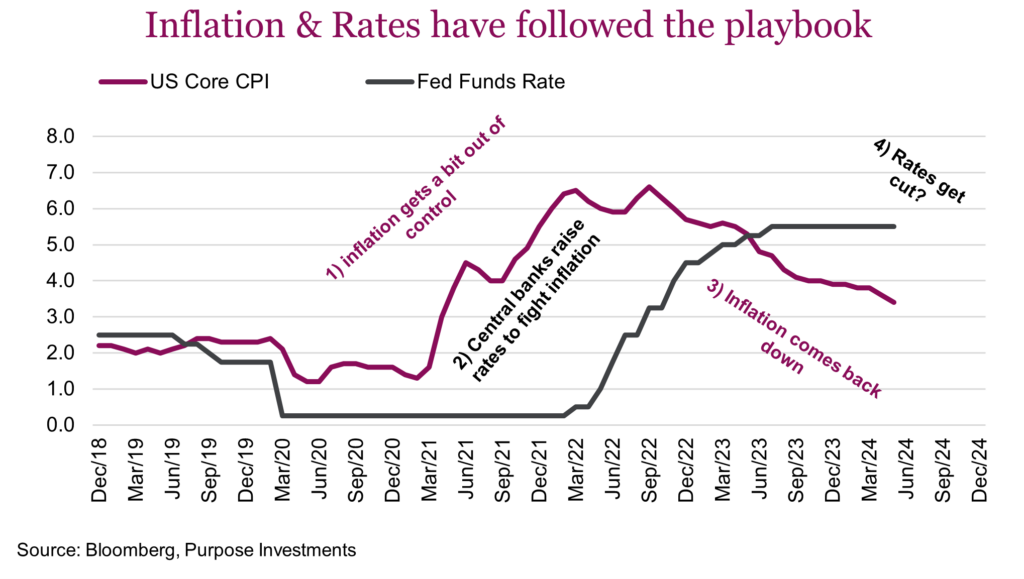

Despite contrary policies, perhaps motivated by short-term thinking (or upcoming elections), inflation has taken a decent turn down and continues to cool. But clearly not in a straight line. In the chart above, you can note a quicker decline in the purple line tracking U.S. year-over-year core inflation with the latest reading after a period where little progress was made. This chart really goes back to show how inflation got started, when it was initially called ‘transitory’, then finally when central banks jumped into action (coincidentally when inflation had already peaked). Central bankers are rarely ahead of the curve.

Inflation declined a good amount in 2023 but the previous few months in 2024 showed it picking up or being much stickier. This latest reading has things cooling again, good news.

The above chart shows U.S. inflation, but the pattern is similar around the world for the most part. Inflation and the economy in Canada has cooled enough to open the door for the Bank of Canada to cut rates. In fact, the number of central banks cutting rates has been on the rise, including some of the biggies like the BoC and ECB. We will talk more about U.S. inflation simply because that is what moves global markets more.

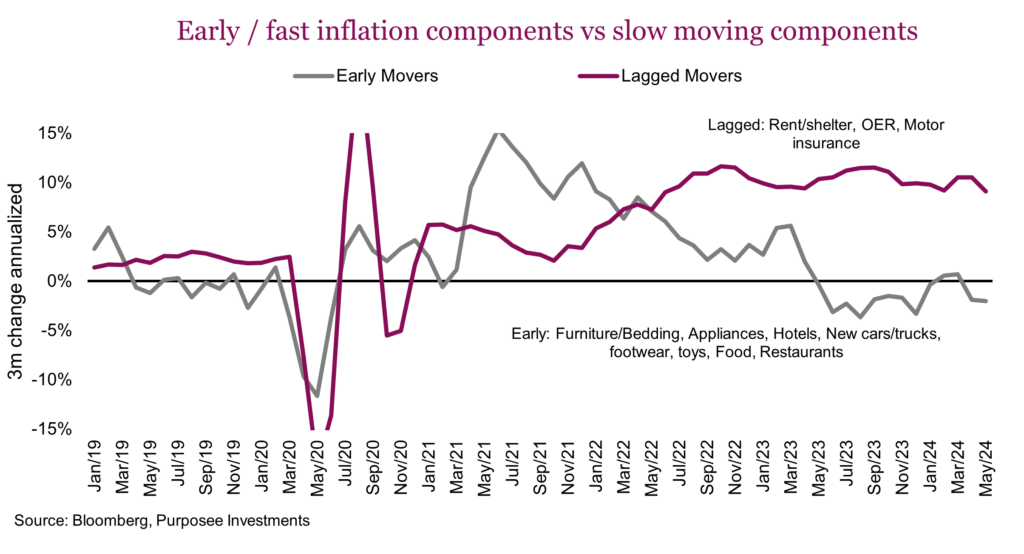

The fast or early movers in the CPI data have been improving for some time. These are the categories of CPI that simply change faster as other components are much slower to react to changes in behaviour. Many goods categories, hotels, autos, restaurants are examples of areas of the economy that change prices more fluidly. Rent, owner occupied rent, insurance are examples of areas where prices change very slowly or even lag in their reaction. Rents often don’t reset until the end of a lease and are further slowed by rent controls. Insurance too doesn’t reset often, so changes in actual prices take time to show up in the aggregate data.

This chart focuses on several early or fast movers vs slower or lagged ones. Clearly, since the spring of ’23 we have seen the fast moving components showing some disinflationary pressures. But the lagged movers remained high, owing to their name. Yet those too have finally started to turn down a bit.

Where to next?

Back down to 3% or so is likely the easy part, then things get a bit less clear cut. Helping out, there remain a number of factors that should continue to put downward pressure on inflation:

✔️

The nature of the price resetting in the lagged movers should continue to put some downward pressure on overall inflation.

✔️

Given how much of inflation is services, employment certainly matters. While nonfarm payrolls remain healthy, that is contrary to other metrics. Household survey is less enthusiastic, temp workers remain on the decline and job openings continue a downward trend. Quitters too; the quit rate drops when it becomes more challenging to get a new job. We believe labour will continue to soften, which should help on wages and the flow through to inflation.

✔️

Supply chain bottlenecks are very low again, with China PPI, producer prices, remaining negative. Given its global manufacturing market share, lower prices for goods coming out of China is disinflationary.

But don’t get too excited. While we think inflation will likely cool a bit more, there are some counter forces that will probably limit the improvements.

❌

Over the past few months, global trade and manufacturing activity have been turning back up. This could just be an echo coming out of the manufacturing recession of ‘22/ early ’23, or it may have longevity. Regardless, in the near term, rising global economic activity will not help prices come down.

❌

Price intentions among survey data, which improved a lot last year, have stabilized. Companies will charge as much as they can and given consumers’ continued fortitude to suck it up and pay higher prices, well, that keeps prices higher. There is some evidence the consumer is starting to change, but for now they keep hitting the ask for flights, trips, dinners, etc.

Inflation may fall further but the gains are likely getting harder to come by.

Final thoughts

We do believe inflation is likely back to being influenced more by the economy and less by the pandemic-induced gyrating behaviors. If the economy reaccelerates, we could easily see inflation pick up again. And if the recent uptick in economic growth proves fleeting, inflation will likely back down. At the very least, this is an easier world to navigate compared to the previous years.