Market Ethos

January 20, 2025

Let the show begin

Sign up here to receive the Market Ethos by email.

Summary: Trump 2.0 premiers this week and everyone is sure it will be an attention grabber, if the trailers have been any indication. In this Ethos we talk a bit about the likelihood of politically driven volatility and dive into bond yields. At these yield levels, the equity market appears sensitive to ticks higher or lower.

We have seen the Trump 2.0 trailers: tariffs, efficiency, border, absorbing Greenland and renaming large bodies of water. Trailers, for movies anyhow, often highlight the most attention-grabbing content, while lacking context and details. This week, the actual show begins.

There is no shortage of content floating around saying if they do this, then that, if they do that, then this. We too have contributed to that wave of content. The challenge with all this political science talk is threefold. 1) Nobody knows what will become policy, 2) Will policy announcements get backpedaled, as was often the case during Trump 1.0, and 3) How, or will, the market react. It may prove more resilient or ambivalent.

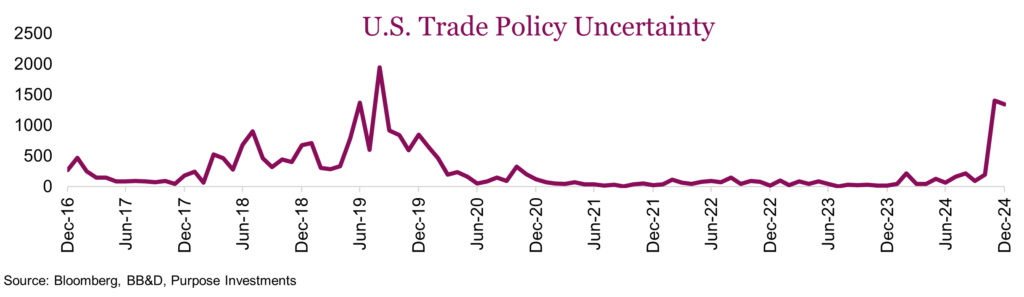

Of course we could rely on logic. Like for example, a tariff on Canadian energy would have a quick impact on U.S. inflation – not a desirable outcome. After all, the red sweep was arguably most attributable to voters’ distaste for enduring inflation. Or what about farmers’ reaction to a large tariff on potash imports? The state governors, congressmen or senators have remained quiet during the ‘trailer’ period but will likely become more vocal as policies get closer. Then again, anything is possible. Trade uncertainty, based on a business conditions survey in the U.S., is near the peak from Trump 1.0.

The only thing everyone can agree on: the headlines are going to become more exciting and volatility will climb in 2025. Volatility in 2024 was certainly on the lower side, with the VIX averaging 15.5. A repeat of this is unlikely, as is a repeat of 20%+ returns, given rather lofty expectations heading into 2025.

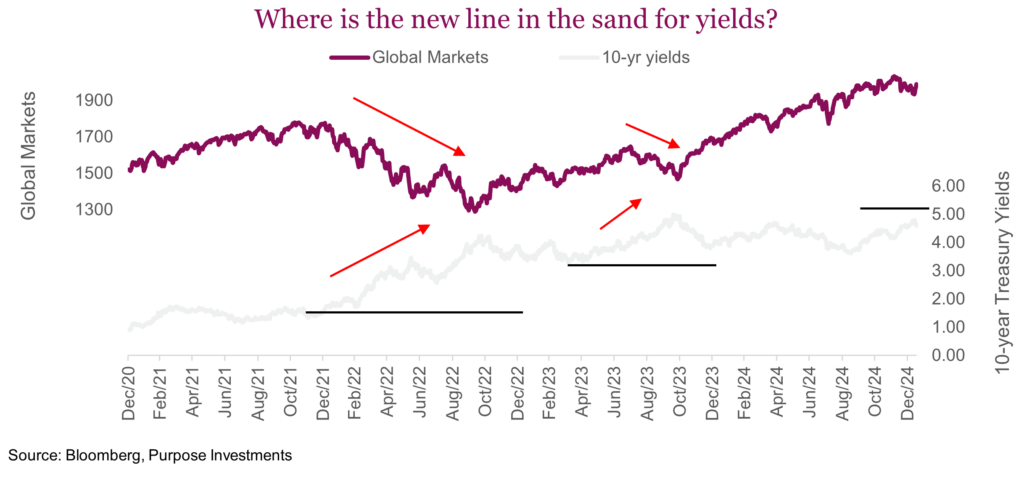

So far though, we would have to say that even with the increased uncertainty, markets have held in well. Volatility picked up a bit but that appears more driven by concern over higher yields than politics. There is an invisible line in the sand for the equity markets – if bond yields (10-year Treasury) move close to this line or above it, the equity market starts to care. And when we say care, we mean go down as higher bond yields put downward pressure on valuations.

This bond / equity relationship is anything but constant. The fact is, rising bond yields on better economic data is often positive for equities. But if it goes too far, too fast, well then equity prices are not a fan. Complicating things further, this line in the sand for yields moves. Back in 2021, the markets didn’t care as yields moved up from 0.50% to 1.0%. They still didn’t care at 1.5% but as 2.0% approached, well then equities fell. Once over 2% and all the way to 4%, it was a really strong correlated market between equities and bonds.

Then things cooled down and the relationship softened. That was until bond yields started rising through 4.0% and equities started to care again about bond yields. Yields touched 5% as the equity market bottomed, then yields fell and equities recovered. Once again, the relationship softened and when bond yields marched above 4% again, equities didn’t care about this level. That was until yields got closer to 4.5 or 4.75%, then it started all over again.

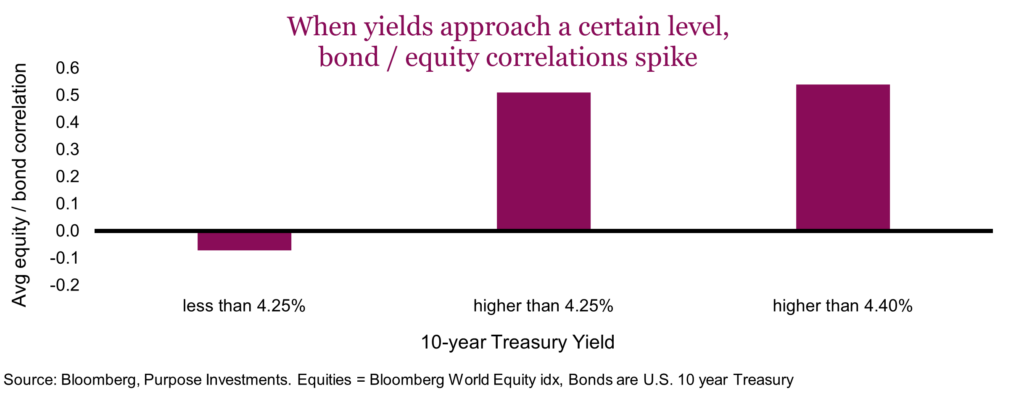

Here is some math on it. In 2024 and so far in 2025, the median 10-year Treasury yield has been 4.25%. Equities and bonds had almost no correlation when yields were below 4.25% and much higher above that level. In fact, even higher north of 4.4%.

This really highlights an instability of equity / bond correlations and the fact that it is often level- dependent – and that level changes over time.

Final thoughts

We are close to yield levels that the stock market seems to care about. That means if yields push higher, given the tilt of economic surprises being positive, that is going to be a big headwind. If yields retreat, well, that could prove a tailwind for equities. At the moment, that appears to be more likely a risk given the data.

Regarding the start of the ‘show’, it is likely going to be a wild ride headline-wise. And markets will react to new information as they always do. If they overreact, that may be the opportunity given that even announced policy often gets massaged once other voices weigh in. Or sometimes things have been said and then never heard again.

Let the show begin.