Market Ethos

September 15, 2025

Springtime for emerging markets

Sign up here to receive the Market Ethos by email.

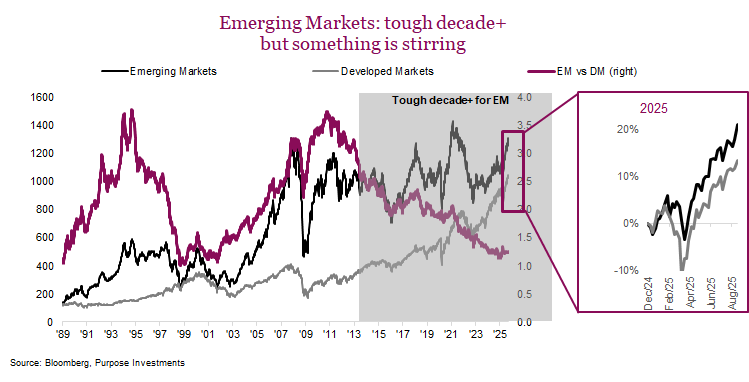

Emerging markets (EM), on a global equity market capitalization basis, represent between 10-15%. This is not small, but also not huge — making it easy for many investors to ignore the space. That tendency has been further supported by poor relative performance over the past few decades. Using Bloomberg equity indices, EM has returned 4.6% annualized over the past 15 years, and developed markets (DM), a much healthier 11.4%. That isn’t only America, as developed international markets managed 7.3%. This poor relative performance led to a ‘long winter’ for EM.

This long winter led to the shuttering of many EM funds and ETFs. Frontier markets, gone, emerging markets equal weight, gone, the list goes on. More on that equal weight shortly. In 2025, a year in which everything seems to be going up nicely, EM has certainly been a bit of a star, up about 21% vs 13% for broader markets. Don’t worry, we are not going to spin the normal product marketing stuff like demographics, better economic growth, rising per capita incomes, etc. All legit, but that has been the case for both EM bulls and bears. Good to know yet not super useful.

Here is our current thinking:

Resilience – If you had told anyone that central bank rates were going to go from near zero in in 2021 to 5.5% by the end of 2023 (Fed Funds as our proxy), most EM investors would run for the hills. And rightfully so, EM tends to underperform in a rising rate environment. True to form, this did occur during the rising rate period and continued as rates remained high. But there is a more important takeaway and that is resilience.

There weren’t any big blow-ups. Apart from a few tiny markets with unique issues, overall EM managed the hiking cycle well — arguably better than past cycles. The markets and economies have grown, with increased diversification making them somewhat less risky than years past. Now with rates coming down, a headwind has become a tailwind.

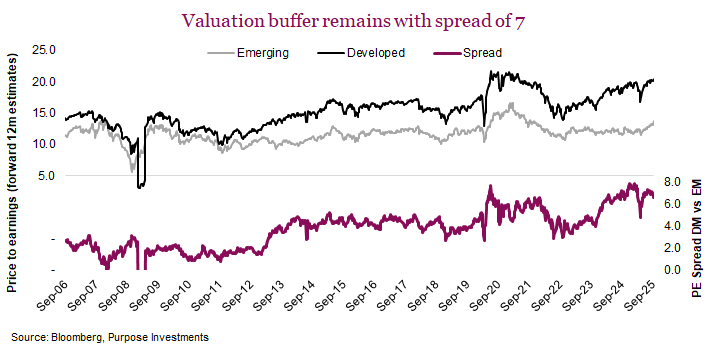

Relative earnings growth and valuations – OK, it is true EM are typically cheaper, and for good reason. Riskier, more cyclical, markets don’t pay as much for those kinds of earnings. That being said, a multiple spread of 6.6, 20.4x for developed and 13.8x for emerging, is historically very wide. Plus, this is after the strong relative outperformance of EM so far this year. This valuation spread is supportive.

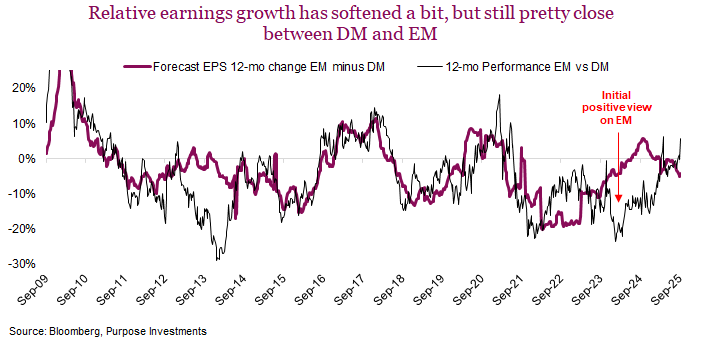

Attractive valuations are nice, but they don’t capture growth — that is often key. There is a long-term relationship of relative EM vs DM market performance and relative earnings growth. Whichever market has higher earnings growth tends to outperform [we’ll let you in on a little secret, that is often the case for many markets and stocks]. After a few years when DM earnings growth was stronger and DM outperformed, relative earnings growth moved closer to even steven. Add in the valuation discount, and we became more positive on EM in 2024.

Fast forward to today, relative earnings growth is a bit of a mild headwind. Emerging market earnings growth has slowed a bit as the impact of a more tariffed global trade environment seeps into consensus earnings estimates.

This is a headwind, but we do not believe it will become insurmountable.

Flows and currency – With relative earnings growth less compelling, there are a few other factors that provide solace. There is a broader global trend that isn’t causing dollars to leave the U.S. equity market, but it appears incremental dollars are looking more internationally. These incremental dollars appear enough to move smaller markets. For instance, the TSX’s gangbuster year so far has a few drivers and flows is certainly one. The same flow trend goes for emerging markets.

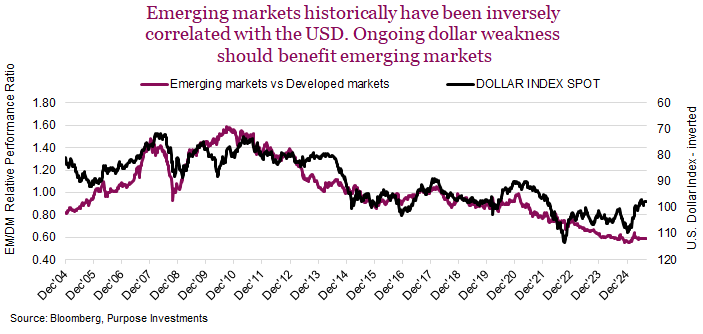

Currency, assuming you have a mild bearish view for the US dollar as we do, is a tailwind as well. Most of those periods of relative EM versus developed market performance map to periods of falling or strengthening US dollar. A weaker dollar is generally positive for EM.

Plus, many of the developing economies, which are home to the emerging market, have a close connection with resources. One of the risks down the road is that developed economies allow inflation to run hotter, gradually erode their currency purchasing power and thus reduce the real value of government debt. Currencies attached to economies that have more natural resources may be viewed as more of a ‘hard’ currency.

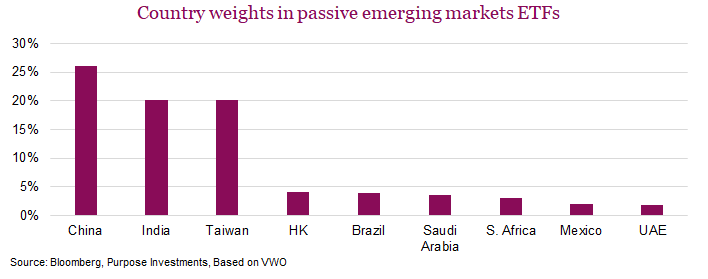

Concentration problem – Over the past year a concentration issue has become increasingly apparent within emerging markets. In part this has been caused by the success, in terms of price appreciation, of some of underlying markets. Over the past year China is up about 45%, Hong Kong 60% and Taiwan just over 30%, all in Canadian dollar terms. This has led to a dramatic rise in concentration.

We will not broach the topic of one China, but you can clearly see emerging markets have a concentration problem. We would add, the Chinese equity market is rather tech tilted, especially if you agree companies like Tencent, Alibaba, Baidu and JD.com are still tech despite being re-classified into other sectors. There is no doubt about Taiwan’s technology weight that sits at almost 80% of the market.

The S&P 500 has taught us a lesson; index concentration is only a problem if what you are concentrated in isn’t crushing it. That being said, most investors in emerging markets may not be aware of the concentration in just a few

of the countries and the high overall technology exposure. Or how little is in countries such as Brazil, South Africa or Mexico. Wouldn’t an equal weight be great? Sadly, none exists from our searches, but if you want emerging markets exposure that is better balanced, there are differently constructed ETFs and active managers with much less concentration risk.

Final thoughts

As with all investment ideas, there are clear positives and negatives. Some slowing of relative earnings growth, the impact on global trade from tariffs and concentration risks remain top of mind for negatives. Of course, concentration could be a positive. America appears to be winning the AI race at the moment, with China arguably in the #2 spot. But who knows who will win or if there will be multiple winners. With a good chunk of EM exposure from technology in China and Taiwan, this does provide some exposure to AI. And it’s worth noting that China taking a great idea, doing it cheaper and making it more broadly available is certainly part of the playbook.

We do believe the positives outweigh the negatives at this point. Valuations are attractive, especially in a global market where everything seems expensive these days. The fund flows appear to be increasingly going more international —that trend could easily persist for a long time. EM will likely capture its share of those flows. And it does provide a bit of protection should the U.S. dollar continue to weaken. We believe the winter for EM has moved into spring time and some of the shoots are starting to sprout.