Sign up here to receive the Market Ethos by email.

Most would agree that this has been a rather unique year so far. The TSX is making new all-time highs at the same time both earnings and economic growth forecasts keep coming down. The TSX isn’t just up, it is up nicely at almost 9% as we near the halfway point. It isn’t abnormal for the top 10 contributors to make up over half the gains of this index that contains 223 companies, but the mix is odd with 5 gold companies, two financials, one consumer, one technology, and one energy.

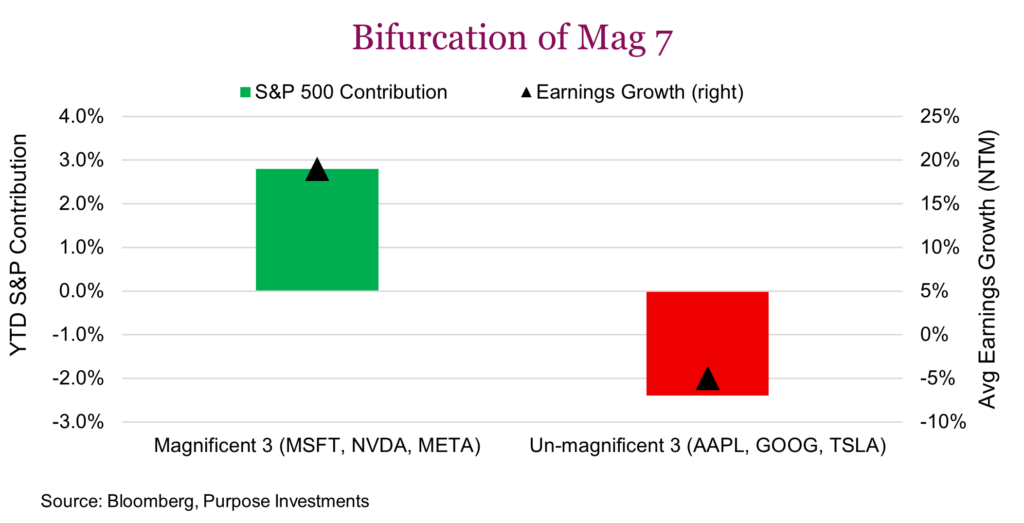

The S&P is even more odd. Up only 4.2%, everyone knows how concentrated the index has become given the market caps of the Mag 7 which carry a 31% weight in the index. This isn’t anything new, but the divergence sure is. Microsoft, Nvidia and Meta are the biggest three contributors to the S&P so far this year, adding +2.8%, while Apple, Tesla and Alphabet are the biggest detractors, subtracting -2.4%. Clearly we have a bifurcation of the Mag 7.

There is a clear distinction between the Mag 7 winners and losers, its earnings growth. Led by Nvidia, the average earnings growth over the next 12 months is +19% for Nvidia, Microsoft & Meta, the positive index contributors. The average earnings growth for the laggard Apple, Tesla and Alphabet is -5%. High valuations are not necessarily a headwind for stock performance, unless those earnings start to wobble, then it is a big problem.

Q2 earnings season is critical

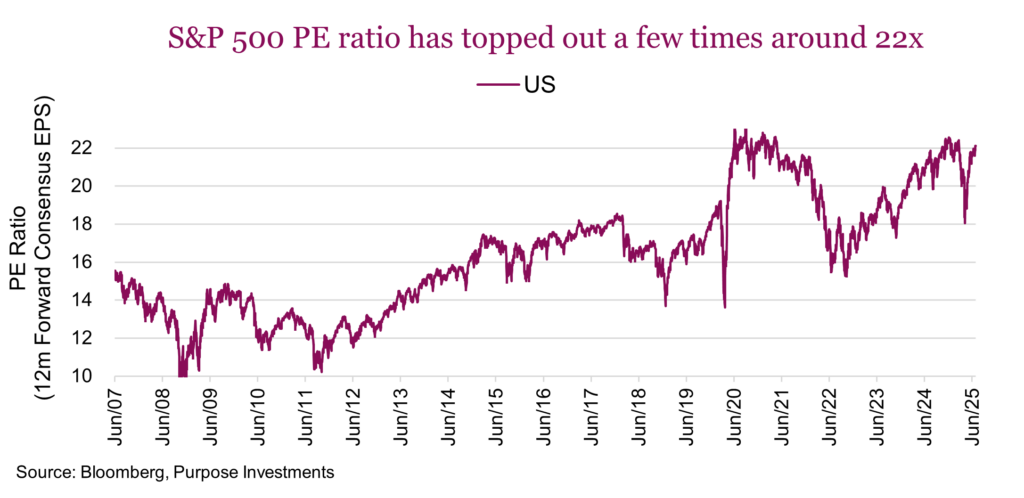

In a few weeks, earnings season for the 2nd quarter will kick off. While every earnings season is important, this one may be more so. After the recent market rally and with indices making new highs, valuations are rather elevated. The S&P 500 has peaked out at around 22x a few times over the past five years. And while the TSX has seen valuations as high as 18x over the past decade, it certainly isn’t cheap anymore.

The challenge is, valuations are elevated, at the same time earnings growth is slowing. We would be more comfortable with a 22x multiple for the S&P 500 if earnings were still growing at 12%. But at 7%, that is precarious. Same issue with Canada but to a lesser extent.

There are some optimistic factors though. The bar may be set reasonably low for Q2 earnings after all these negative revisions. There are some signs the revisions have slowed or even turned a bit positive in the past couple weeks. The U.S. dollar is also lower, that is generally positive for U.S. S&P 500 earnings given the decent percentage of sales/operations overseas.

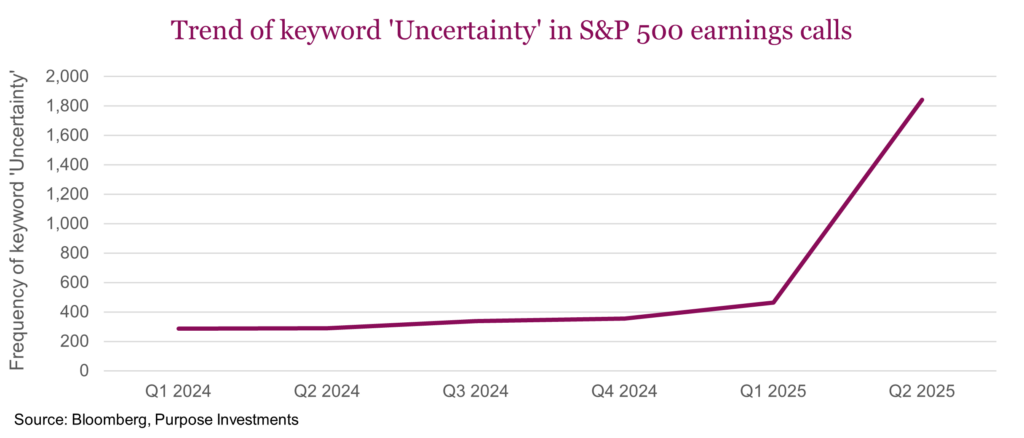

The headwind is well known, that is Mr. Uncertainty. The extended period with uncertainty around tariffs has certainly reduced the confidence of company leaders in the outlook. During Q1 earnings season, the trend was for companies to pull guidance as they just don’t know what will happen. Still without clarity, will we see more companies pull guidance or are they going to start reducing guidance? That is likely a more important factor in this coming earnings season compared to how many companies exceed estimates.

The valuations or market multiple is certainly elevated, but it is influenced by many other factors than just earnings growth. Bond yields have come down over the past few weeks, that has helped the multiple expand. Investor sentiment has improved from overly bearish to more of a neutral mood. The geopolitical headlines certainly impact the multiple, and most of this news flow has been market friendly of late.

The challenge is these positive levers have already been pulled. To help this market keep going we would likely need to see a re-acceleration of earnings growth to maintain or improve the current multiple. That may be a big ask.

Final Thoughts

Will the months of uncertainty which is starting to show up in some pockets of economic data also show up in earnings this season? Maybe, but the stock moving factor will likely be the tone and guidance from company leadership. And given valuations are already at the upper echelon, stumbles may prove painful.

Source: Charts are sourced to Bloomberg L.P., Purpose Investments Inc., and Richardson Wealth unless otherwise noted.

The contents of this publication were researched, written and produced by Purpose Investments Inc. and are used by Richardson Wealth Limited for information purposes only.

*This report is authored by Craig Basinger, Chief Market Strategist at Purpose Investments Inc. Effective September 1, 2021, Craig Basinger has transitioned to Purpose Investments Inc.

Disclaimers

Richardson Wealth Limited

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson Wealth Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.

Purpose Investments Inc.

Purpose Investments Inc. is a registered securities entity. Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Neither Purpose Investments nor Richardson Wealth warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise.

Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice.

The particulars contained herein were obtained from sources which we believe are reliable but are not guaranteed by us and may be incomplete. This is not an official publication or research report of either Richardson Wealth or Purpose Investments, and this is not to be used as a solicitation in any jurisdiction.

This document is not for public distribution, is for informational purposes only, and is not being delivered to you in the context of an offering of any securities, nor is it a recommendation or solicitation to buy, hold or sell any security.

Richardson Wealth Limited, Member Canadian Investor Protection Fund.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.

Related articles

Market Ethos

Waiting at the train station

23 March 2026. Market Ethos. As hostilities broke out in the Middle East, markets were initially rather resilient. But after three weeks, that resilience is…

12 March 2026. Market Ethos. Over the past three decades banks have delivered standout returns. But with valuations pushed higher, the question now is: How…