Background

News of Silicon Valley Bank (SVB) has dominated the headlines in recent days, with concerns that the bank’s failure will spread throughout the banking sector. To understand what happened, we first delve into what Silicon Valley Bank was. As the name suggests, the bank catered to startups, venture capitalists and tech firms for nearly 40 years. With the tech industry growing exponentially, so did the lender, with total deposits rising from about $61 billion in 2019 to $173 billion as of December 2022. SVB invested much of these deposits into government bonds, which incurred steep price declines last year as the Fed’s aggressive hike campaign ensued. The rate hikes hurt tech stocks and triggered faster-than-anticipated withdrawals from SVB, forcing the sale of the lender’s treasury holdings at a loss. While banks typically avoid losses on their bond portfolios if they are held until maturity, any sudden liquidity requirements disrupt this safety.

FDIC to the rescue

Following a run on SVB’s deposits, the Federal Deposit Insurance Corporation (FDIC) stepped in last Friday, March 10 and took control of the bank. Then on Sunday, March 12, U.S. regulators announced the closure of a second bank, New York-based Signature Bank, a commercial bank with $110 billion in assets that also experienced a bank run in the billions leading up to its closure.

In a coordinated effort, the Federal Reserve, Treasury Department, and FDIC announced measures to lower the contagion risk to the financial sector. First, the Treasury Department instructed the FDIC to make whole all deposits at both banks, including deposits above the $250,000 threshold for deposit insurance, and announcing that insured depositors would have access to their funds by Monday. Second, the Fed introduced a new emergency lending facility which will make loans up to a year to depository institutions where qualifying assets used as collateral for the loans will be valued at par, rather than marked to market.

Market reaction

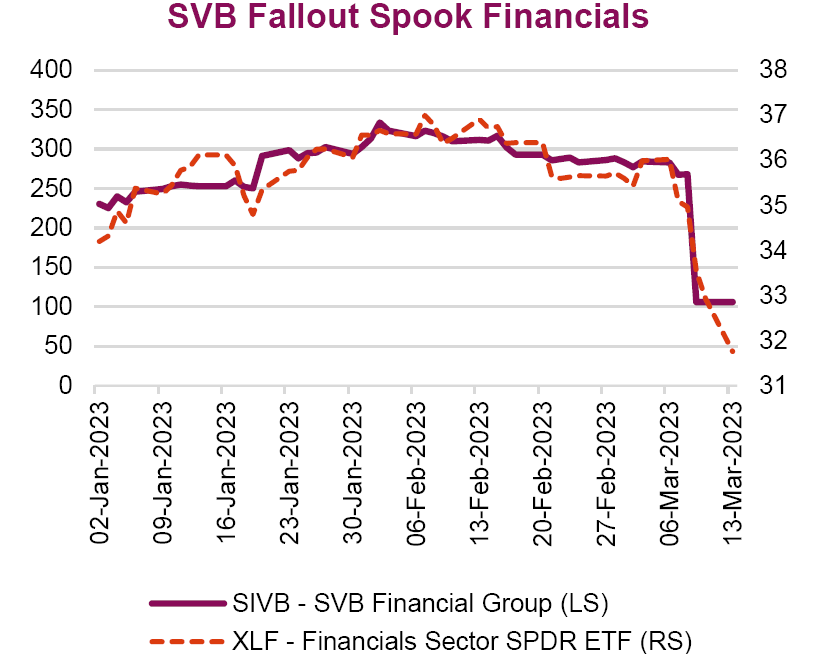

The impact was swift as investors recalibrated their expectations amidst SVB’s collapse. Contagion worries pushed shares of financial stocks lower as SVB’s failure raised concerns of larger systemic risks across the financial sector. In the U.S., regional banks largely took the brunt, while in Canada, the big six banks were also feeling some pressure and were flat to -3% at the time of writing. In Canada, a liquidity strain forcing the sale of debt securities at a loss is viewed as unlikely due to the banks’ diversified base of deposits across geography and sectors, and relatively strong liquidity coverage ratios.

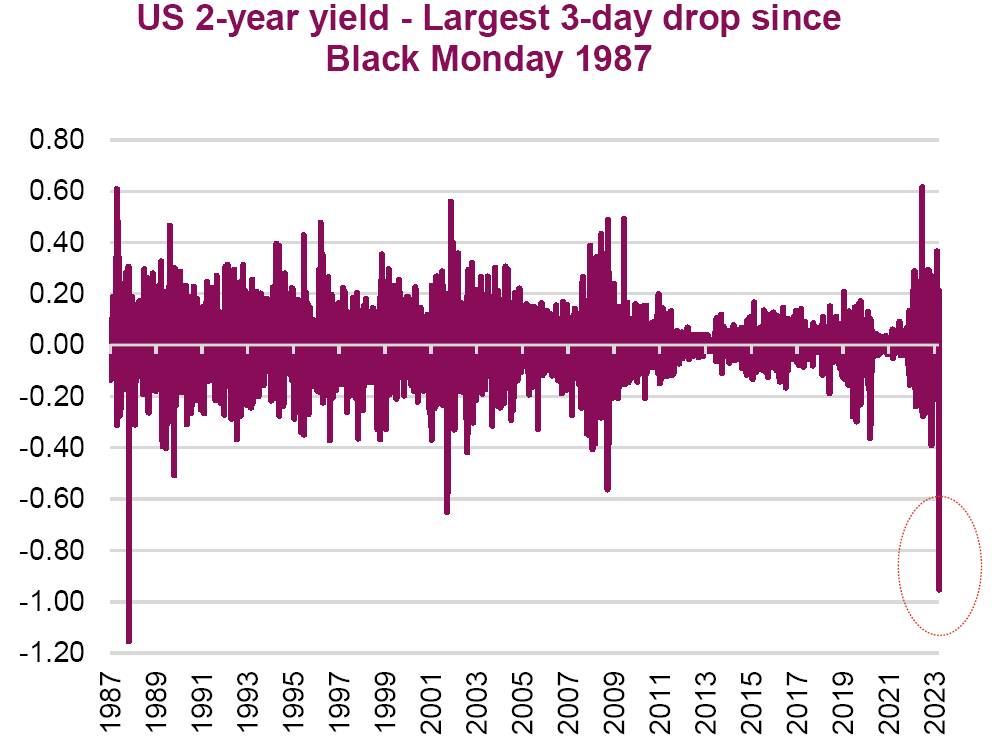

While the financial sector has borne the brunt of SVB’s demise, safe-haven assets such as bonds and gold have rallied. Bond yields in the U.S. plummeted, with the two-year Treasury yields on track for its largest one-day decline in decades, falling 60 bps to 3.99% at one point. Meanwhile, benchmark 10-year treasury yields also declined to 3.52% at the time of writing, after reaching 4.05% less than two weeks ago. Meanwhile, gold has rallied back above $1900, the first time in over a month as investors flocked to the perceived safety of the metal. Gold has historically performed well during times of market uncertainty or geopolitical strife.

What’s next

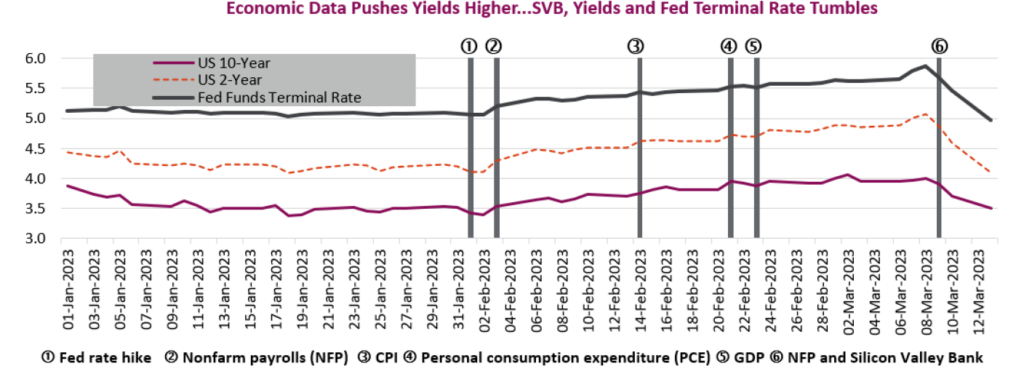

The markets have already repriced rate-hike expectations. Just last week, investors had succumbed to the central bank’s view of ‘higher for longer’ and pushed out any rate cut expectations. Fast forward today, and the market has once again priced in a rate cut as early as the summer. With CPI data due tomorrow and the next rate hike meeting next week, we anticipate that the Fed will have to balance reining in pricing pressures with managing the impact of higher rates on financial conditions.

In all, the regulatory safety net (some would argue it’s another bank bailout) by the combined Treasury, Federal Reserve and FDIC has helped ease market angst, at least temporarily. Nonetheless, the recent bank runs, albeit isolated, will shine a spotlight on bank liquidity and the ongoing challenges that banks may face amid a rising rate environment.

Source: Charts are sourced to Bloomberg L.P., and Richardson Wealth unless otherwise noted.

Authors: An Nguyen, VP Investment Services; Phil Kwon, Head of Portfolio Analytics; Andrew Innis, Analyst

Disclaimers

Richardson Wealth Limited

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson Wealth Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by the author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Richardson Wealth does not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise.

Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice.

The particulars contained herein were obtained from sources which we believe are reliable, but are not guaranteed by us and may be incomplete. This is not an official publication or research report from Richardson Wealth, and is not to be used as a solicitation in any jurisdiction.

This document is for informational purposes only, and is not being delivered to you in the context of an offering of any securities, nor is it a recommendation or solicitation to buy, hold or sell any security.

Richardson Wealth Limited, Member Canadian Investor Protection Fund.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.