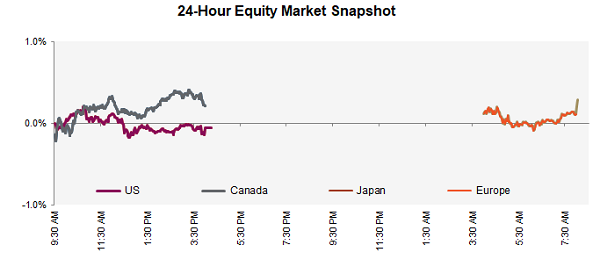

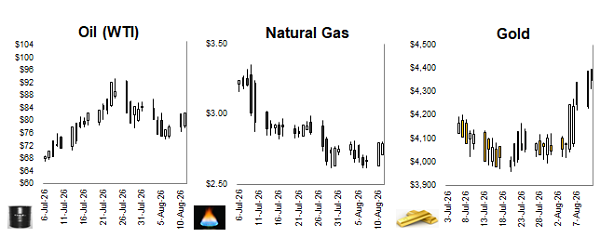

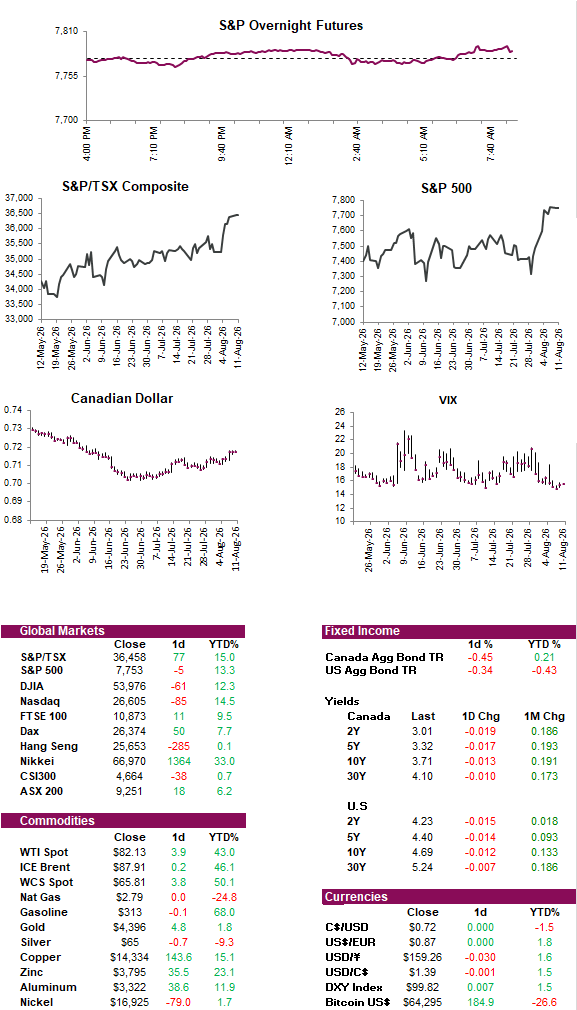

Stock futures are higher this morning following modest losses for U.S. indexes yesterday, while the TSX edged higher. Trading volumes fell to their lowest level of the year, an unsurprising development during the peak summer vacation season and likely a reflection of investor caution ahead of tomorrow’s July CPI report. Oil prices are volatile this morning, with Brent crude briefly approaching $90 a barrel before retreating to around $87 at the time of writing after Pakistan’s defense minister said the U.S. and Iran are “close to some sort of arrangement” over the Strait of Hormuz, despite both sides hardening their positions in the long-deadlocked negotiation. The initial rally followed renewed uncertainty over the reopening of the Strait of Hormuz after the U.S. administration made new demands on Iran. Higher energy prices have also revived inflation concerns, pushing the 10-year U.S. Treasury yield as high as 4.73% just below its year-to-date high, before easing to around 4.70% at the time of writing.

Another strong quarter. As the Q2 earnings season draws to a close, FactSet’s latest Earnings Insight report suggests corporate America has delivered one of its strongest reporting seasons since 2021. With 88% of S&P 500 companies having reported, 86% have exceeded earnings estimates and 76% have beaten revenue expectations, both above historical averages. The index is now on track for 50.4% y/y earnings growth and 15.0% revenue growth, marking the strongest quarterly earnings and revenue growth since 2021 and the seventh consecutive quarter of double-digit earnings growth. While unusually large gains at Alphabet and Amazon boosted the headline figures, FactSet notes earnings growth would still be a healthy 32% excluding those two companies, highlighting the broad strength of corporate profits.

FOMO? The recent stock rally which has lifted the TSX and S&P 500 to new highs may be fuelled by fear of missing out, with several options-market indicators showing some of the most bullish positioning in years. The S&P 500 call-to-put ratio has climbed to 0.9, short-term call skew reached a two-year high, and the Bullish Percent Index moved above 70%, suggesting investors are aggressively chasing further upside and the market may be becoming overbought. Strong earnings, easing Middle East tensions, and lower oil prices have provided support, but analysts say technical factors and investors scrambling to increase exposure have boosted the recent gains, even causing volatility to rise alongside stocks on some days. While this enthusiasm could be a contrarian warning that the rally is becoming stretched, bulls continue to point to solid fundamentals and strong AI investment as reasons the market can remain supported.

Intervention rejection. The yen has given back roughly half of the gains from last week’s U.S.-Japan currency intervention, weakening to around 159 per dollar after briefly strengthening from about 164 to 155. The reversal highlights the difficulty of using intervention alone to change the currency’s direction, as wide U.S.-Japan interest-rate differentials, concerns about Japan’s fiscal outlook, and geopolitical uncertainty continue to weigh on the yen. Authorities have spent tens of billions of dollars supporting the currency, but investors remain aware to the possibility of further intervention, especially during periods of thinner market liquidity. Attention is now shifting towards the Bank of Japan, where rising inflation risks have strengthened expectations for additional tightening, with markets pricing a roughly 63% chance of a September rate hike. However, some argue that a sustained yen recovery may require even more intervention, a faster pace of BOJ tightening, or a shift in the global economic and interest-rate backdrop.

Teachers make the grade. Ontario Teachers’, Canada’s largest teachers’ pension plan, reported a 9.5% net return for the first half of 2026, increasing net assets to a record $303.2 billion. Gains were broad based, with venture growth, public equities, and inflation-sensitive assets contributing the most, while the public listing of SpaceX was among the fund’s strongest investments during the period. The portfolio also increased its exposure to public equities, venture growth, and infrastructure, while reducing allocations to private equity and inflation-sensitive assets. The plan remains fully funded for a 13th consecutive year and has delivered annualized net returns of 7.8% over the past decade and 9.4% since inception in 1990.

Deep thoughts, courtesy of Jack Handey Mark Zuckerberg. Meta’s CEO recently published a long essay outlining his vision for AI and why he believes it can lead to a better world (assuming the robots don’t take over first). If you’re interested in hearing his take on where AI is headed, it’s worth a read. If not, “Mark,” as he signs off, also offers an audio version for your commute. For those looking for the Coles Notes version, Zuckerberg argues AI should be broadly accessible rather than controlled by a handful of governments or companies, with personal AI agents helping people invent, learn, build businesses, improve their health, and solve problems. He believes AI’s greatest contribution will be expanding human capabilities rather than simply automating jobs, and that distributing AI widely is ultimately the best safeguard against concentrating too much power in too few hands.

Wildfires continue to devastate parts of western Canada, with nearly 22,000 people across British Columbia under evacuation orders and another 11,000 on evacuation alert as a fast-moving wildfire west of Summerland in the Okanagan continues to spread. The province remains under a state of emergency, with officials warning that hot, dry conditions and the threat of lightning could ignite additional fires. The blaze is one of more than 600 active fires burning across Canada, as another difficult wildfire season continues to unfold. We hope everyone affected can return home safely soon and recognize the extraordinary efforts of the first responders and volunteers working tirelessly to protect communities.

Diversion: The music lessons paid off