Sign up here to receive the Market Ethos by email.

March 2023.

Investor Strategy.

Executive summary

Our view remains – markets can move higher on signs of softening inflation and clearly can move lower on signs of more inflation. Looking through the zigs and zags, we see the inflation data trend to the downside, just not in a straight, smooth line. BUT, the good news will be short-lived as the signs of a slowing economy grow louder and garner more attention. We remain renters of any rally and like bonds a little more with every tick higher in yield.

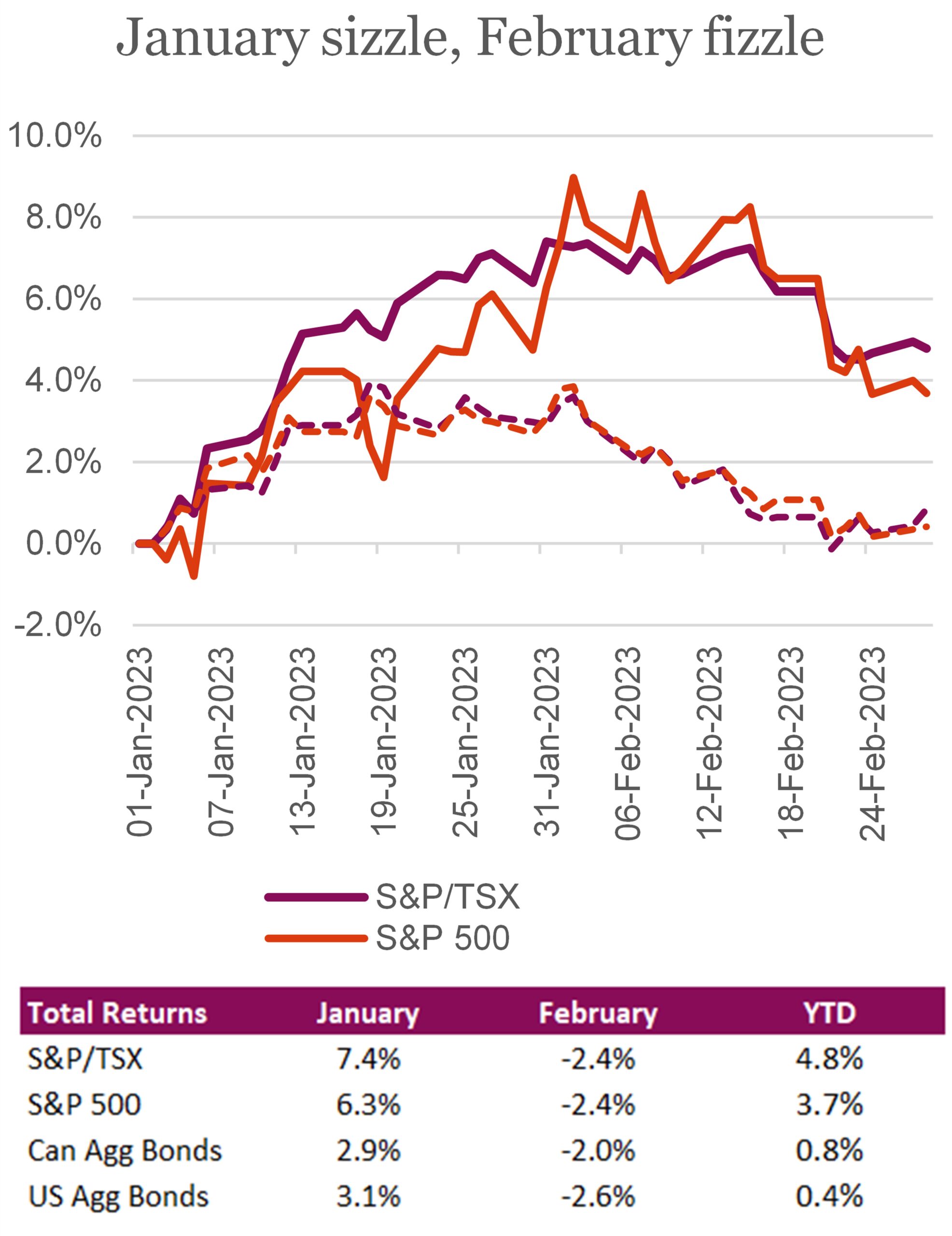

No love in February

Well, that didn’t last long. Investors in February were faced with the realization that inflation is not cooling to the extent most central banks would like to see. The uncertainty surrounding inflation and future interest rate hikes, particularly in the U.S., came roaring back in February. Unless you were sitting in cash, there were few places to hide over the month, with both bond and equity indexes falling over the month. Key economic indicators that central banks pay close attention to came in hotter than expected, muting the optimism that sent stocks soaring in January. On a total return basis and in local terms, the S&P 500 fell -2.4%, the Nasdaq fell -1.0%, and the TSX end -2.4% lower for the month. While down for the month, all three indexes remain comfortably higher YTD, thanks to strong returns in January. The same cannot be said for the Dow, which had a total return of -3.9% for the month and is now down -1.1% for the year.

Investors who were looking to move on from last year’s bond market drop were once again faced with rising yields and falling bond prices. Bond markets once again needed to reprice expectations for how high policymakers will raise rates, with expectations now being that the Fed will raise rates beyond the previous 5% target and leave rates above that level for at least the remainder of the year. As yields pushed higher throughout the month, the U.S. aggregate bond index ended the month down -2.6% while the Canadian Aggregate bond index c losed -2.0% lower.

Canada appears to be in a better position than other developed markets. The January CPI rose 5.9% YoY, a sign that inflation is trending downwards, a smaller climb than the 6.1% expected from economists. Although inflation data continue to come in well above the Bank of Canada’s 2% target, the market is anticipating that the central bank will hold rates at 4.5% at its next policy meeting on March 8.

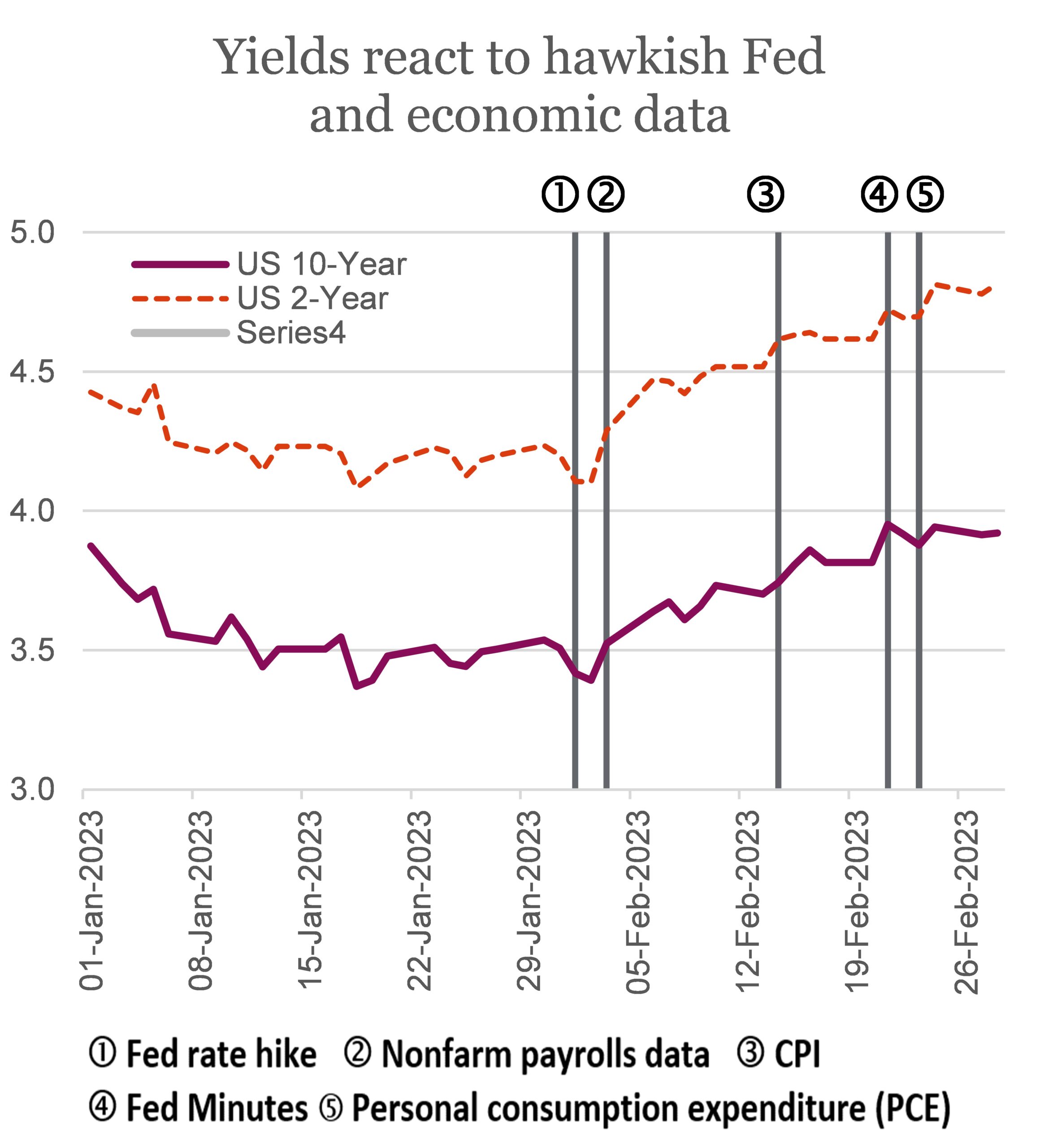

The same cannot be said about the Fed, who signaled over the month its intention to raise rates higher than the market had been anticipating. The minutes from the Fed’s most recent meeting emphasized the need for additional rate hikes as the central bank continues to fight inflation. Data released this month, which included resilient consumer spending, strong labour numbers, and higher inflation figures strengthened the case for tighter policy from the Fed. Investors are now pricing U.S. rates to peak at 5.4% this year, compared with about 5% just a month ago. The Fed’s rate hike cycle could persist into the summer, with a higher probability of the federal funds rate rising another 75 bps between now and the central bank’s June or July policy meetings.

Helped by warmer temperatures and falling commodity prices, economies across Europe held up better than expected in February. Both UK and European economies surprised to the upside of economists’ consensus, with the February S&P Global Eurozone Composite PMI jumping while earnings in the region have also been resilient. With just over half of companies having reported, positive trends are becoming apparent. Still, European central banks are expected to remain hawkish this year with market expectations seeing the ECB rates through February 2024, with a 4% ECB terminal rate fully priced.

Worth a read or two

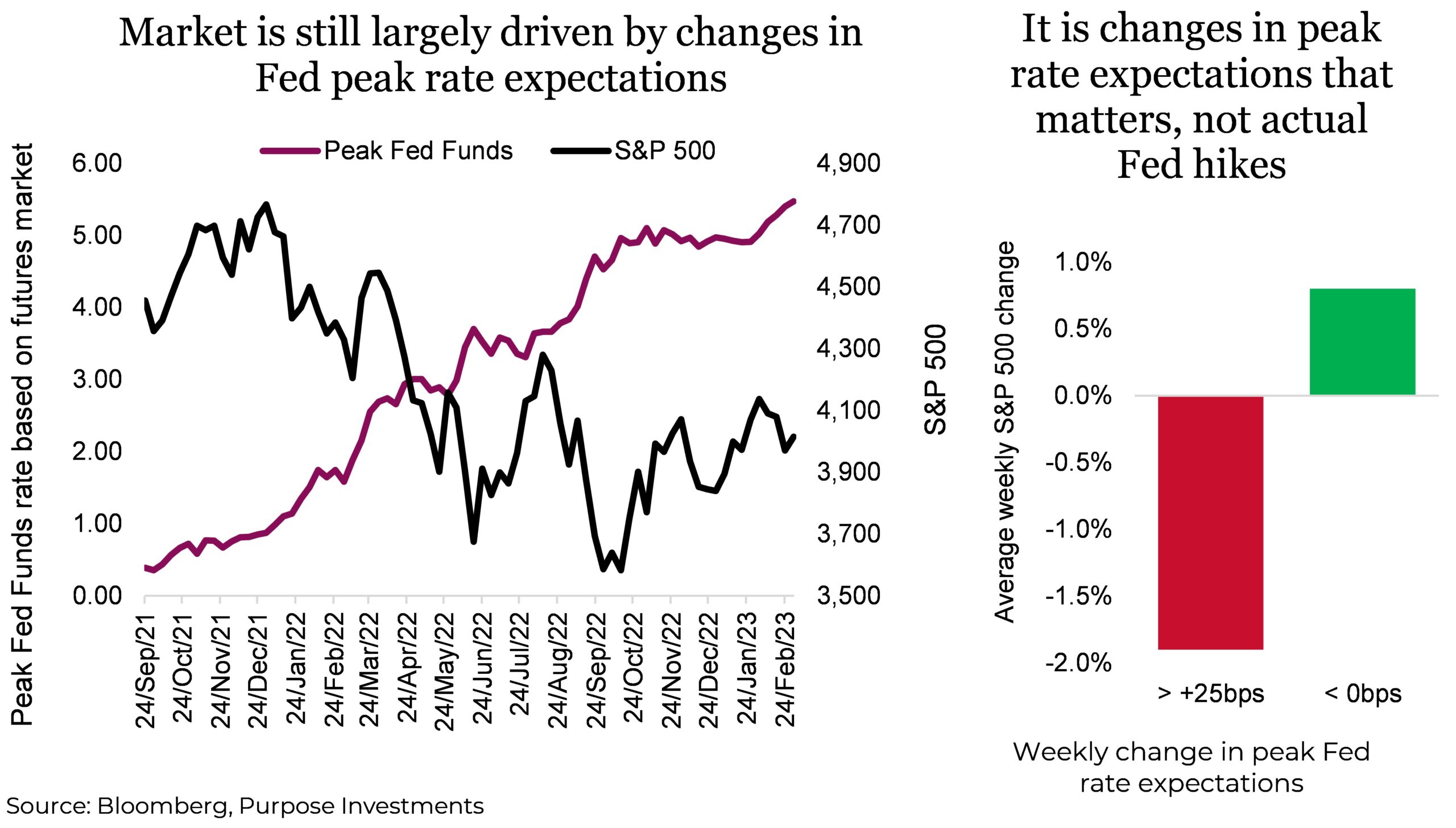

Markets and the economy never travel in a straight line, and the last few months have had more than their normal share of zigs and zags. In October, after rising steadily all year from less than 1%, the market started pricing in a stable peak federal funds rate of about 5%, expected to be reached sometime in 2023. Parts of inflation had started rolling over a few months prior, and the data was accumulating that inflation was starting to ease. Markets reacted positively, bond yields came back down, and equities moved higher. This move accelerated in January, largely due to more cooling inflation evidence and a bit of a junk rally. But neither markets nor the data move in a straight line.

More recently, we have seen a tick higher in inflationary data and an improvement in the economic data, two things the markets don’t like. This has woken up that stable peak federal funds rate pushing it up 50bps to 5.5%, with the 10-year U.S. Treasury yields back over 4% and the S&P back below 4,000. Clearly, the decline of inflation is not going to be a straight or smooth line.

Taking a step back, which often helps to provide perspective for both the economy and markets, the inflation trend is to the downside. The 3-month change in CPI is trending lower, wage growth has come off a bit, and inflation expectations have come down both in the short and longer term. Supply chain pressures are largely gone, based on CitiGroup’s aggregate measure. There are always some data points that counter the trend – the NFIB survey of small businesses indicated a small rise in pricing plans and ISM service pricing too. Inflation moved higher in Europe, and the U.S. PCE Deflator was higher than expected (happy to explain what a deflator is, just ring or email us). But at the moment, the majority of the data is pointing to less inflation going forward.

And let’s not forget what causes inflation: too much money chasing too few goods/services/assets. Well, the supply of goods logistic issues are resolved, and the amount of money is shrinking. M2, a measure of the U.S. money supply, peaked in March 2022 and has gradually declined. A peak in M2 growth has preceded all past peaks in CPI; sometimes, it takes a few months and sometimes more than a few.

Our view remains – markets can move higher on signs of softening inflation and clearly can move lower on signs of more inflation. Looking through the zigs and zags, we see the inflation data trend to the downside, just not in a straight, smooth line. BUT, the good news will be short-lived as the signs of a slowing economy grow louder and garner more attention. We remain renters of any rally and like bonds a little more with every tick higher in yield.

Market cycle

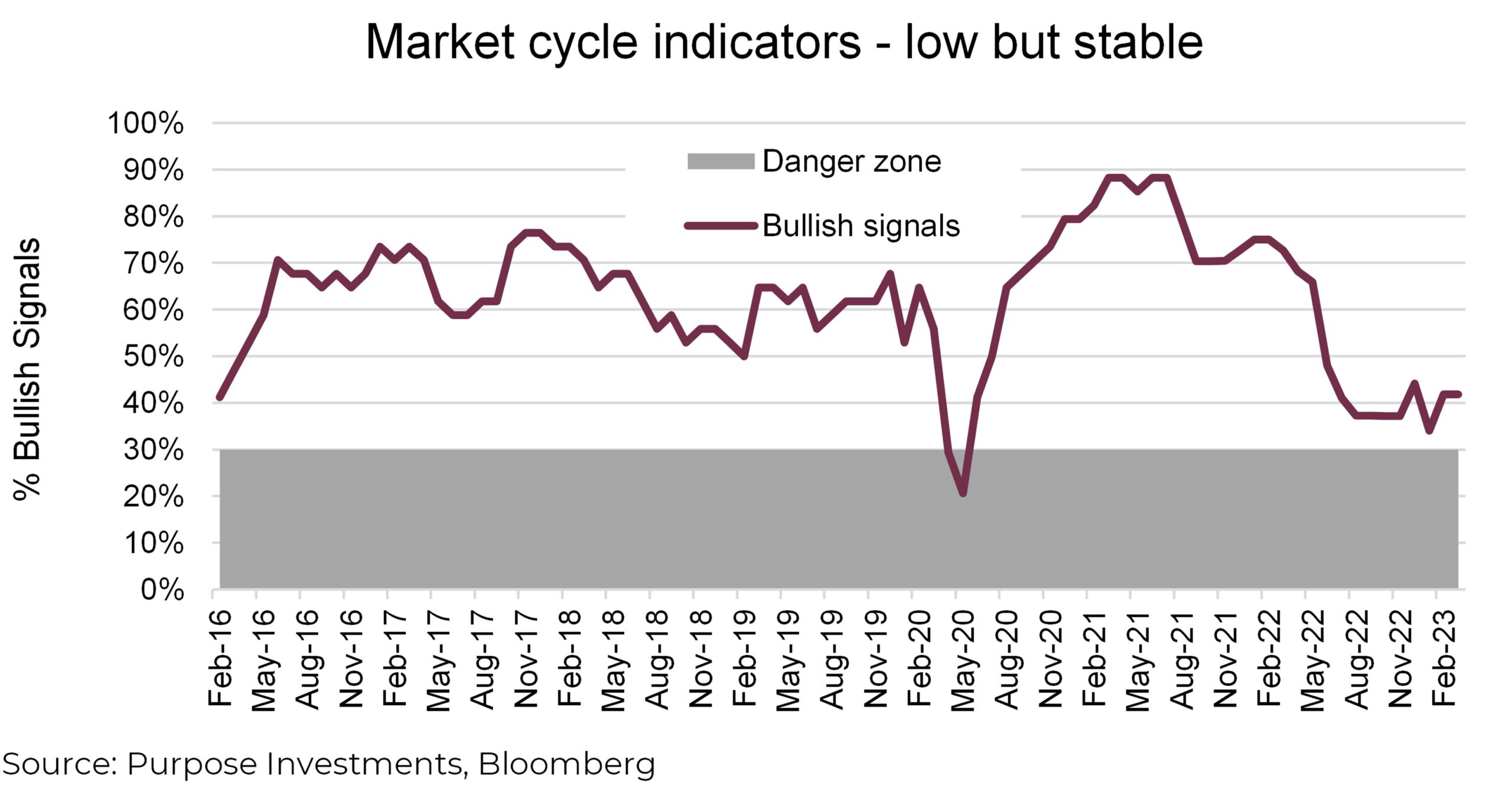

Our market cycle indicators continue to hover just above the zone that has a good reliability of signalling a pending recession. But things are actually a bit better than they appear on the surface. On the signal side, we have seen a few improvements in the fundamental data, meaning earnings revisions/growth. Offsetting this was a few signals turning negative for the global economy. The U.S. economy improved, notably on the housing side.

Housing data in the U.S. is very important. Just about every recession in the U.S. can be traced back to changes in activity in housing and/or manufacturing. These are the more cyclical components of the U.S. economy which is, on a relative basis, more insulated from global factors. Housing activity had been softening for many months as the impact of higher mortgage rates took its toll, similar to trends here in Canada. The question is whether the recent improvement in U.S. data is a turning point or just a temporary counter-trend move. We don’t believe it will last, as the housing part of the economy will still be absorbing the past rate hikes for many months. And this recent move in yields has mortgage rates moving up again.

There is more good news, though. The trend for most signals is improving. With 34 signals improving and only 8 deteriorating, we expect to see more green signals in the coming weeks. Nothing moves in a straight line, and with economic data getting a bit better, the market cycle is picking this up.

Cooling on international and warming to bonds

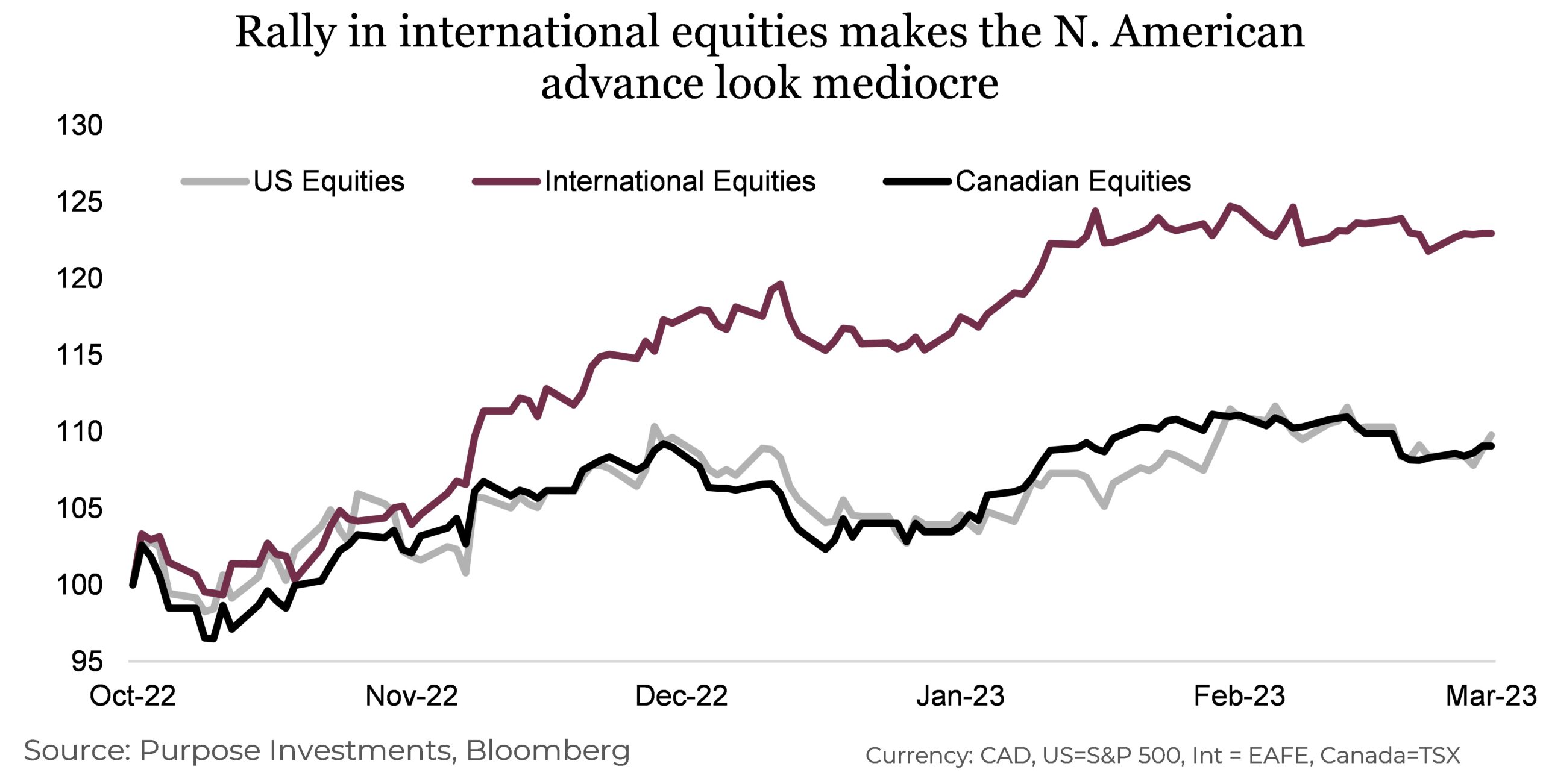

International equities are an area of the multi-asset universe that we have chosen to be much more overweight than your average Canadian balanced portfolio. So far, so good over the last five months, international markets have been on a tear of outperformance. A long-term cycle analysis drove the thesis for being overweight international equities. Looking back throughout decades of data, market dominance shifts between the U.S. and international markets. The 80s was international, the U.S. crushed it in the 90s, the 00s saw outperformance from international, and we all know what dominated in the 10s, U.S. mega caps. Markets like to move in cycles, and leadership changes each cycle. We believe international equities will likely be strong for the foreseeable future, but from a near-term tactical mindset, it might not be that simple.

The fact is, we remain in the camp that the move higher in equities over the last five months is a bear market rally, and the economic outlook remains challenging. Inflation remains high, especially for our counterparts across the ocean. Year-over-year core Eurozone inflation remains high at 5.6%, which moved higher as of March 2, and the UK Core CPI is at a similar level. The ECB has signalled that the interest rate hiking cycle is far from over. The widely forecasted earnings growth deceleration is coming, shown by tepid guidance from most companies in the U.S. and international markets. The economy is starting to slow, but there will always be some form of lingering tailwinds that keeps the bulls alive and well.

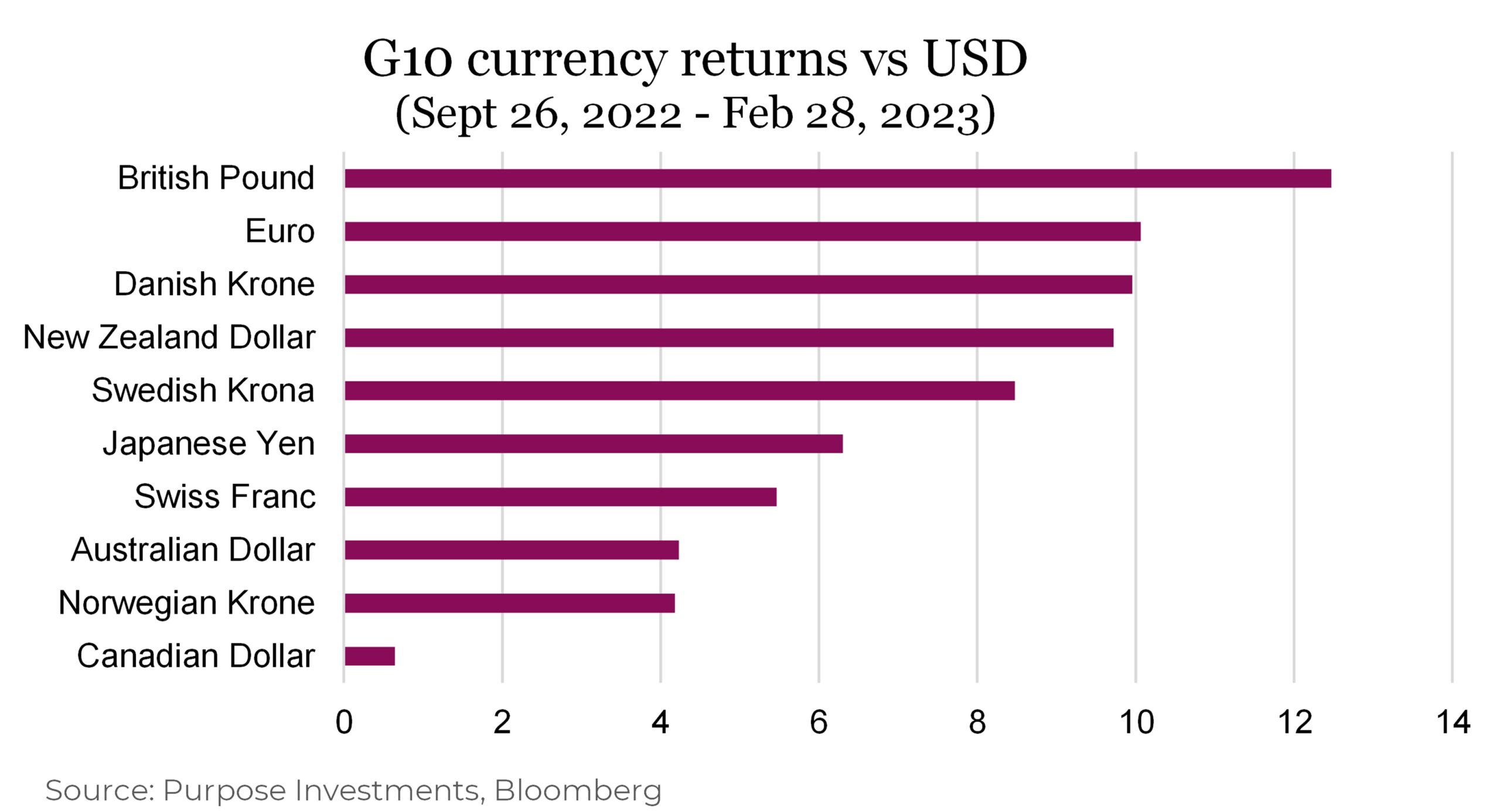

A surefire sign that things may have moved too quickly has been the rapid move in G10 currencies against the US dollar. This move has contributed towards the international returns for us North Americans. Albeit, for the majority of the below currencies, the starting point is from extremely depressed levels, especially the British Pound and the Euro. So, it is no surprise that these kinds of returns in a relatively risk-on environment were found internationally. Still, many of these currencies remain undervalued from a long-term perspective, another reason why our overweight in international will persist. The rapid movement of these currencies simply allows for a short-term tactical shift towards other multi-asset allocations.

This is a good thing, in not so many words. Over the past few months, the overweight in international has been the right call. It is important to reiterate that looking ahead through the next cycle, our thesis remains for a period of desynchronized global growth, which should enhance the prospects of geographic diversification. Persistent inflation should alleviate, which could lead to large differences in country performance. Our long-term view has not changed; we just like to take profits.

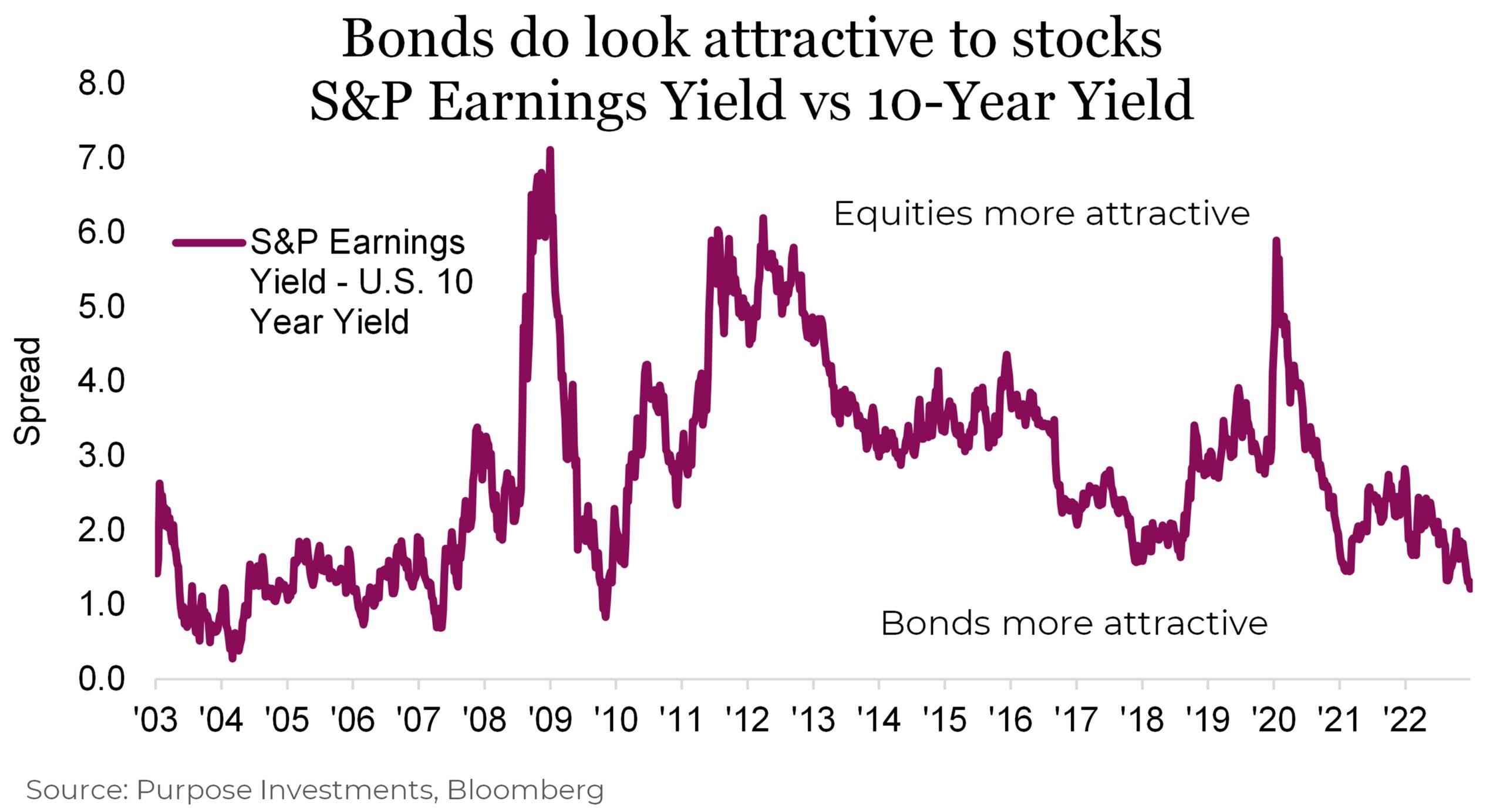

With earnings estimates falling, multiple expansions were doing the heavy lifting for equities this year. For example, blended forward valuations for the S&P 500 rose from a low of 15.2x in October to a high of 18.7 in early February. International stocks are still cheap relative to the S&P 500 but have also seen a similar degree of multiple expansion. The earnings yield is simply the reciprocal of the PE Ratio and is useful in comparing the relative valuations between stock and bond markets. The chart below shows that equities are now the least attractive relative to 10-year Treasuries since 2010. The spread is not historically high going back decades but is at a level that begs some attention. The disparity is even more apparent on the short end of the curve, with the S&P earnings yield nearly equal to the U.S.

2-year bond yields. Falling risk premiums indicates an overbought equity market relative to bonds. The historical risk premium in equities relative to treasuries exists for a reason: a necessary payment for the risk of volatility and drawdown.

For investors, it’s important not to get caught up in bond market recency bias. The experience in 2022 for the fixed-income market was terrible, and we’re not going to sugarcoat that. Unprecedented is just a way to sugarcoat a poor investment decision. We’re not going to deny that pace and magnitude of rate hikes were a surprise last year. However, we won’t abandon a key tenant of portfolio diversification because of a bad year. Over the past year, the FTSE TMX Universe is down -7%, compared to just -1.1% for the S&P/TSX Composite – not the type of defence we anticipated in a drawdown environment, but also not the type of performance we expect looking forward. The future path of bond yields is uncertain, and there will always be a degree of rate risk in the bond market. Investors need to remind themselves why they want bond exposure in the first place; that is diversification, plain and simple.

Bond market volatility picking up – so long, Fed pivot

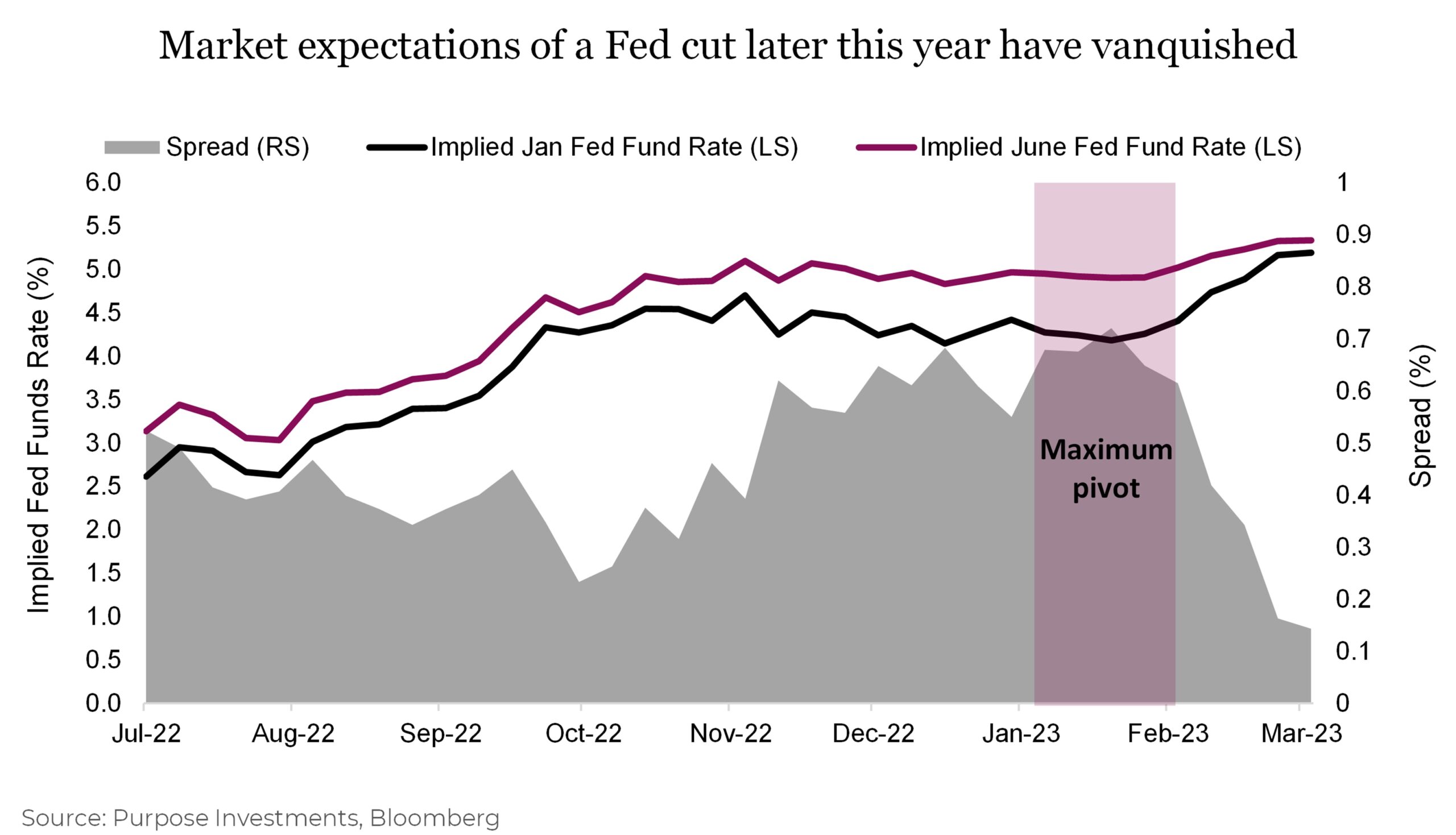

Rates and equity volatility have been on a round trip so far this year, with the narrative changing from soft landing to higher for longer. Bond and equity markets rallied on expectations of a Fed pivot this year, but those vanquished in February. The chart below shows the expected Fed funds rate differences from June ’23 to Jan ’24. The 72bps difference reached in January represented maximum pivot or a high degree of conviction that rates would max out in the summer, followed by multiple cuts. That’s been eliminated from the market’s view in a matter of weeks, with a slim chance of a pivot this year.

Peak rates went from around 5% last October to a new high of 5.4% based on the current market-implied overnight rates. Also interesting is that the timing of the terminal rate continues to be pushed out. For most of last year, peak rates were expected to be from March to May. Then in the fall, it was pushed out to June. And just this month, the terminal rate has been pushed out to September. The trend is clear, but for some reason, it’s not obvious to the equity markets. We increasingly prefer the relative safety of fixed income because of the implications.

Portfolio thoughts

The renewed volatility in the rates market and still subdued volatility in the equity market has created a divergence between stocks and bonds that concerns us. So far, we’ve seen only a modest decline in stocks. Just like Nick Nurse, coach of the Toronto Raptors, we have a defence-first mentality. This can be done on the equity side through sector allocation, factor tilts or certain alternative strategies. At the portfolio level, the most important decision is the stock/bond mix. We’re currently slightly overweight fixed income and are very near tilting further in this direction. For months now, we’ve pegged around 4% on the U.S. 10-year as a level where we’re comfortable adding to fixed income and even duration.

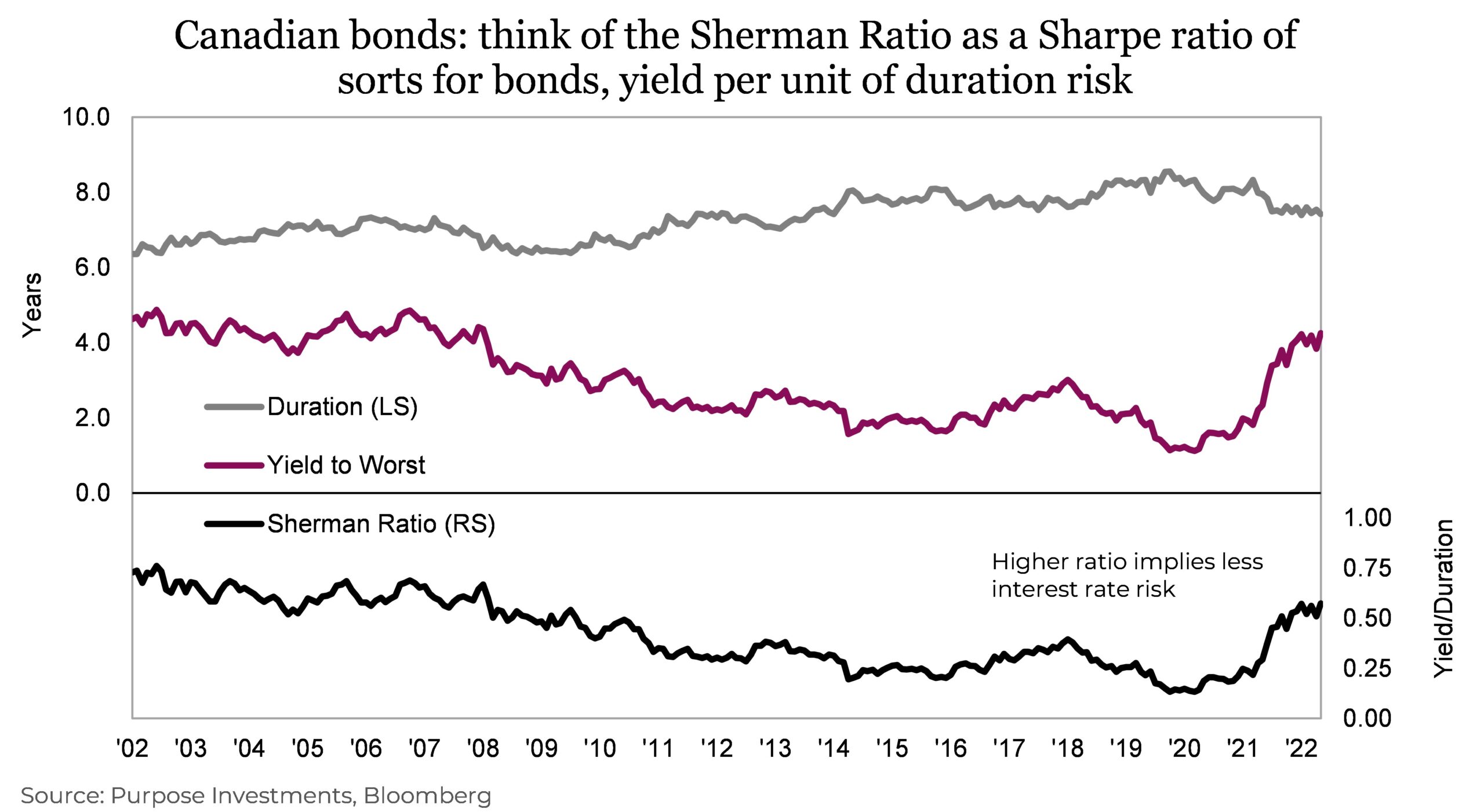

The current duration for the FTSE TMX Universe is 7.35 years. This is the lowest it has been in six years, and with U.S. 10-yr yields now over 4%, some duration here is again looking attractive. The break-even ratio, also known as the Sherman Ratio (yield/duration), is a measure of interest rate risk, representing yield per unit of duration. The current ratio for the Canadian Aggregate Bond Universe is 0.57, implying that yields would have to rise 57bps from here for the decline in bond prices to offset the yield over the next year. Compare this with a low of 0.13 in 2021 or 0.21 at the beginning of 2022, and the risk/reward trade-off is very different. While interest rate risk is still present, the risk/reward ratio is as high as it’s been in nearly 15 years.

Investing is a constant exercise in risk-taking. With thoughtful consideration, we believe the scale is modestly stacked against equities in favour of bonds in the near term, especially if the economy really starts to slow down. Looking at valuations relative to history and our near-term outlook, we believe now is a good time to tilt further towards defence. From an asset allocation perspective, risk is paramount and given our healthy respect for the unknown, this is why we invest in bonds in the first place.

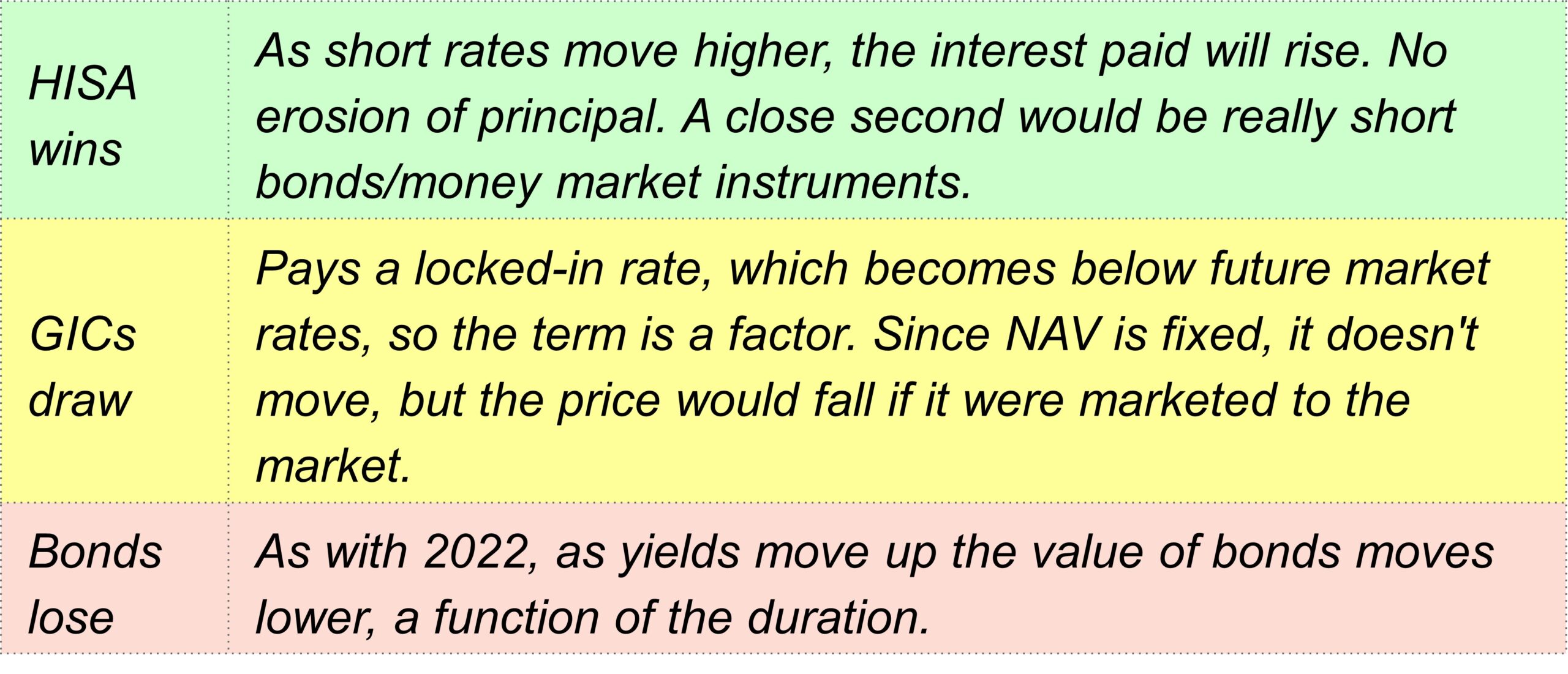

Bonds, GICs, or HISA?

One of the most recurring questions from investors over the past few months has been on the fixed-income side of their portfolios. Many are licking the wounds of a bond bear market that saw Canadian bonds (based on a broad-based ETF) drop by -2.8% in 2021, -11.7% in 2022, and currently sitting flat in 2023. Limited joy from the part of the portfolio that is supposed to be the stabilizer. This has been fostering a mindset that maybe bonds are broken.

Meanwhile, with yields up across all maturities, including cash products, not surprising there has been a rush into other solutions. High-interest savings accounts (HISAs) enjoy a current yield of just under 5%, while with GICs, you can lock in 4.8% for a year or 4% for five years. And your principal won’t go down should yields continue to rise. Clearly, there is a lot of money in motion around these three options at the moment.

Bonds, GICs or HISA – which is the right choice? Each has a unique return profile that depends on what happens next. So, sadly, there is no clear answer unless you know the future path of inflation, short- and long-term rates, the pace of economic growth, plus much more.

So, what could be next:

More inflation scenario – Inflation has cooled over the past few months, thanks to supply chains getting sorted and some cooling in the economy. But let’s say it re-accelerates either due to the service component of inflation continuing to ascend, or the global economy speeds up. There are some signs of improving growth out there, including in China. If this were to occur, central banks would likely continue to raise short-term rates, and longer yields would also move higher.

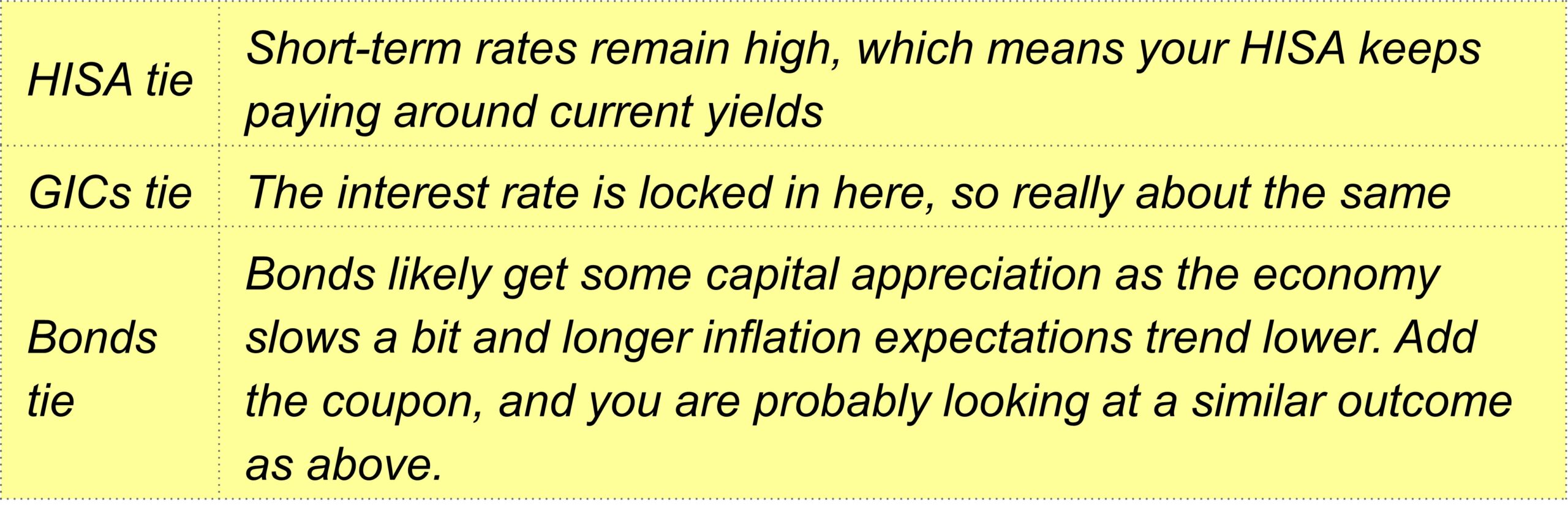

Goldilocks scenario – Inflation gradually comes back down thanks to supply catching up, and the economy slows but remains decent. This is that magical soft landing that is so often hoped for or attempted. It’s certainly possible. The global consumer is in good shape, employment is strong, there are pent-up demand/savings, and some signs of growth are out there, along with some signs of slowing. As the impact of past rate hikes is fully felt, the economy adjusted to a slower pace of growth.

Central bankers arrest their hiking ways, and longer yields remain stable or come down a little. This could result in a three-way tie.

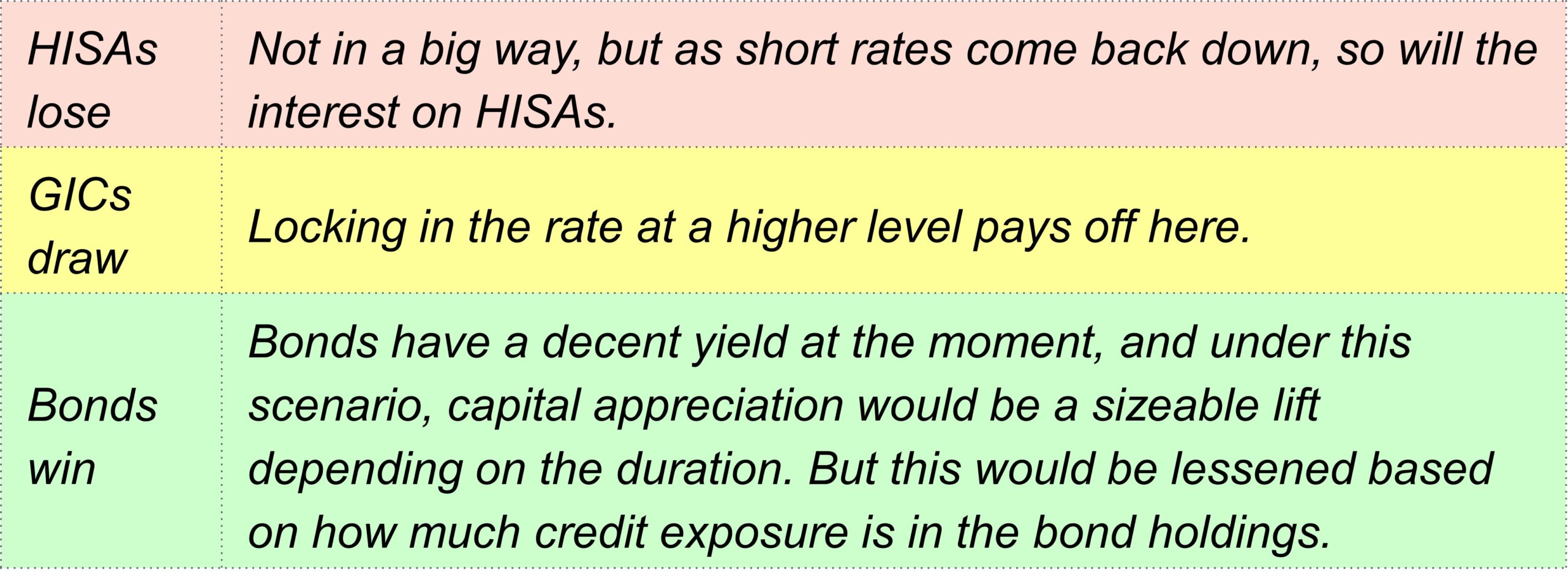

Slowing growth or recession – Inflation has peaked and is on its way back down, thanks to supply chain improvements and slowing economic growth. The magnitude and speed of rate hikes around the world in 2022 will have a bigger economic impact in 2023, causing economic growth to slow substantially or even trigger a recession. Hitting the air brakes does not result in soft landings.

As the economic slowdown’s magnitude and timing become clearer, central bankers may even start to cut rates. And bond yields will fall.

Of course, there are other scenarios out there or other combinations of events. Stagflation could be one, in which case cash likely wins, but it depends. We could see inflation pick up and an economic slowdown not materialize till later, 2024 perhaps. The economy is a mystery. It often doesn’t change despite big macro factors … then it suddenly moves quickly.

Two other factors worth considering:

Optionality – Maybe equity markets drop substantially, or yields jump higher. Ensuring you have enough liquidity to make changes to take advantage of any potential material mispricing is important on your portfolio’s cash/bond side. HISAs or cash take top honours here, with bonds in second. GICs in a distant last depending on how many years are left in the term as the money is locked in or would suffer a penalty to redeem early. Don’t underprice optionality –it has value that could be more than a few basis points of yield.

Big picture – Part of a portfolio – It is important not to suffer tunnel vision on one or two line items in a portfolio. It is the aggregate portfolio structure that matters. For instance, you may be inclined to shed all duration (go super short term) for your bonds and add more credit. That would have helped a lot in 2022. But if a recession is coming, all of a sudden that credit exposure isn’t so great, and you will want duration. A recession will also weigh heavily on the equity side of your portfolio. Again, it is important to think of the big picture of the entire portfolio.

There is no perfect answer for the path ahead, primarily because of the uncertainty. The good news is just about every option available now carries a decent yield, a far cry from years past. We like optionality for our portfolio management work, so we lean towards good old fashion bonds and liquid cash vehicles.

Sign up here to receive the Market Ethos by email.

Source: Charts are sourced to Bloomberg L.P., Purpose Investments Inc., and Richardson Wealth unless otherwise noted.

*Authors:

Purpose Investments: Craig Basinger, Chief Market Strategist; Derek Benedet, Portfolio Manager

Richardson Wealth: Andrew Innis, Analyst; Phil Kwon, Head of Portfolio Analytics; Mark Letchumanan, Research; An Nguyen, VP Investment Services

Disclaimers

Richardson Wealth Limited

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson Wealth Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.

Purpose Investments Inc.

Purpose Investments Inc. is a registered securities entity. Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Neither Purpose Investments nor Richardson Wealth warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise.

Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice.

The particulars contained herein were obtained from sources which we believe are reliable, but are not guaranteed by us and may be incomplete. This is not an official publication or research report of either Richardson Wealth or Purpose Investments, and this is not to be used as a solicitation in any jurisdiction.

This document is not for public distribution, is for informational purposes only, and is not being delivered to you in the context of an offering of any securities, nor is it a recommendation or solicitation to buy, hold or sell any security.

Richardson Wealth Limited, Member Canadian Investor Protection Fund.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.